|

시장보고서

상품코드

2066727

북미의 규사 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Silica Sand - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

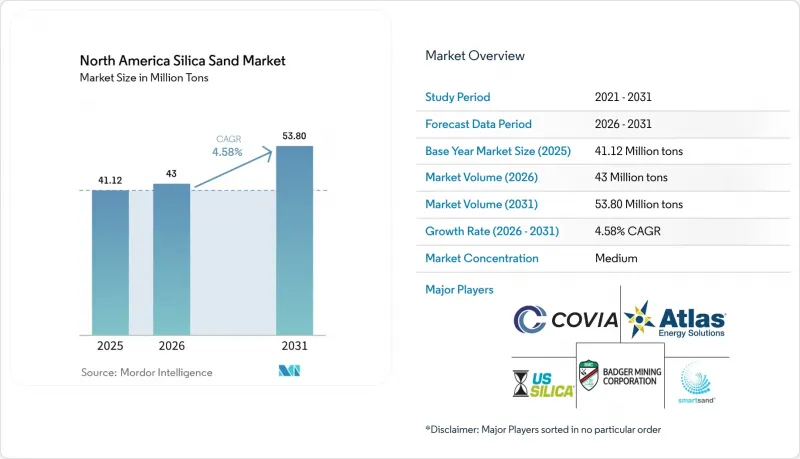

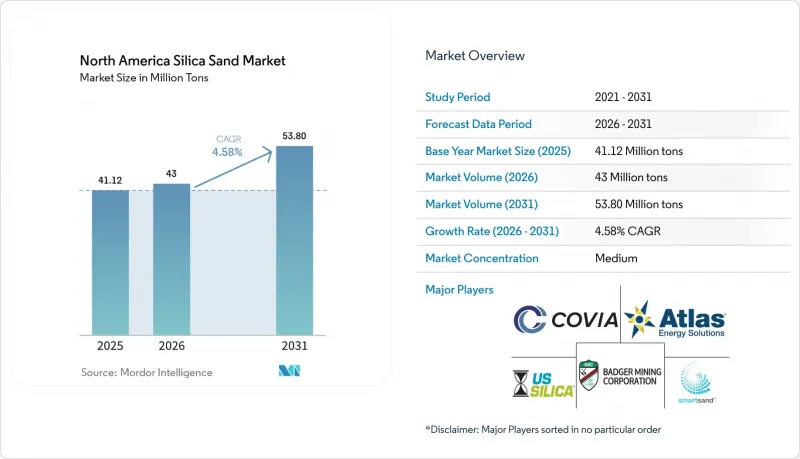

Mordor Intelligence에 의하면, 북미의 규사 시장 규모는 2025년 4,112만 톤으로 평가되었고, 2026년 4,300만 톤으로 추정되고, 2031년까지 5,380만 톤으로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.58%를 나타낼 전망입니다.

본 보고서는 최종 사용자 산업별(유리 제조, 주조업 등), 제품 형태별(천연 플랙 샌드, 노던 화이트 샌드 등), 메쉬 및 입도별(70메쉬 미만, 70-120메쉬 등), 가공 방법별(습식 규사, 건식·선별 완료 샌드), 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

북미의 규사 시장 동향 및 분석

주조 생산량의 회복

미국 주조협회(American Foundry Society)는 주조 제품의 매출액이 2025년에 1.9%, 2026년에 4.1% 증가할 것이며, 이후 2030년까지 연평균 4.6%의 성장률을 보일 것으로 전망하고 있습니다. 미국 파운드리의 41%가 생산의 국내 복귀(리쇼어링)에 따른 수주 증가를 보고하고 있으며, 96%가 2026년에 설비 투자를 계획하고 있습니다. 이는 주형용 규사에 대한 수요가 지속될 것임을 시사합니다. 주조용 모래의 사용량은 철계 주물 생산량과 톤 단위로 연동되기 때문에 중서부 주변의 모래 광상에 집중된 520억 달러 규모의 국내 주조 업계는 운송 비용을 절감하고 공급망을 강화하고 있습니다. 소규모 파운드리은 가스 비용 급등에 직면해 있으며, 전기 아크 용해가 보급되면 모래 사용량이 줄어들 가능성이 있지만, 입지상의 이점과 자동차 경량화 추세가 가속화되고 있는 점을 고려할 때, 북미의 규사 시장은 꾸준한 성장이 예상됩니다.

셰일 시추 장비 수 증가 주기와 분지 내의 플랙 샌드

퍼미안 분지의 프로판트 수요는 2016년 1,400만 톤에서 2025년에는 약 8,000만 톤으로 증가하여, 미국 전체 수요의 60%를 차지할 것으로 전망됩니다. 현재, 시추공 1개당 수평 시추공 길이에 해당하는 모래의 평균 사용량은 1만-1만 5,000톤이며, 2026년 1월 시추 장비 수가 전년 대비 36대 감소한 546대를 기록했음에도 불구하고, 단기적인 수요는 견조한 추세를 보이고 있습니다. 이 분지에서 생산되는 브라운 샌드의 가격은 노던 화이트보다 톤당 10-15달러 저렴하며, 중간 깊이의 파쇄 기준을 충족하고 있어 월스트리트 샌드사가 2026년 2월 가동을 예정하고 있는 커밋 공장과 같은 생산 능력 확대를 뒷받침하고 있습니다. 이러한 추세로 인해 위스콘신주 광산의 철도 운송 수익성이 압박을 받고 있으며, 북미 규사 시장에서 산업용 틈새 시장으로의 다각화가 진행되고 있습니다.

물류 비용의 변동성이 크다는 점

SCTG 11 산업용 모래의 철도 운임은 벌크 상품의 경기 사이클에 연동되어 변동하고 있으며, 텍사스주와 앨버타주로 출하하는 북부 광산의 이익률을 압박하고 있습니다. PropFlow사의 습식 모래 파이프라인은 톤당 6달러의 운송 비용을 내세우고 있지만, 고정식 파이프라인이 필요하기 때문에 보급에는 한계가 있습니다. 사업자들이 분지 내의 건식 모래로 사업 중심을 옮기는 가운데, 원거리 생산자들은 톤당 40-60달러의 철도 운임 차액을 부담하거나, 품질 프리미엄이 운임을 상쇄해 줄 수 있는 여과용, 유리용, 특수 등급으로의 전환을 모색하고 있습니다. 다년 계약을 체결하지 않은 중소기업들은 현물 가격의 급등을 감당할 수밖에 없어, 북미 규사 시장에서 운전자금이 부족해지고 있습니다.

부문별 분석

석유 및 가스 부문은 2025년 공급량의 51.89%를 차지했으며, 북미 규사 시장에서 핵심적인 역할을 하고 있음을 입증하고 있습니다. 한편, 여과·수처리 부문은 도시들이 ‘안전한 음용수법’의 기준을 충족하기 위해 노후화된 시설을 교체하는 추세에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.31%를 기록하며 다른 부문을 앞지를 것으로 전망됩니다.

유리 제조는 2위를 차지하고 있으며, SiO₂ 함량 98% 이상, Fe₂O₃ 함량 0.03% 이하의 모래가 요구됩니다. 이러한 사양은 산지 내의 브라운 샌드에서는 거의 충족되지 않기 때문에 노던 화이트의 프리미엄 가격을 뒷받침하고 있습니다. 주조 분야는 자동차 경량화 및 생산의 국내 복귀에 따른 주조 수요 증가에 힘입어 성장세를 보였습니다. 화학, 세라믹, 코팅 및 틈새 레저 용도가 수요를 보완하고 있으며, 각각은 메쉬 크기와 순도를 조절함으로써 부가가치를 창출하고 있습니다. 따라서 여과 및 유리 분야에 할당되는 북미 규사 시장 규모는 꾸준한 성장이 예상되며, 이는 채굴 업체들을 프로판 시장의 주기적인 변동으로부터 보호하고 있습니다.

노던 화이트는 2025년 총 공급량의 40.88%를 차지했으며, 심정용 프로판, 유리, 주조 각 분야를 뒷받침하고 있습니다. SiO₂ 함량이 99.9%를 초과하는 고순도 실리카는 엄격한 금속 규격을 중시하는 반도체 및 태양광 발전 분야 수요에 힘입어 2031년까지 연평균 5.51%의 성장률을 보일 것으로 전망됩니다.

이 분지에서 생산되는 브라운 샌드는 톤당 10-15달러 저렴하게 판매되고 있으며, 중간 깊이의 프로판트 시장에서 일정한 점유율을 차지하고 있지만, 유리나 반도체 용도로는 여전히 적합하지 않습니다. 부가가치는 선광 공정에 있습니다. 자력 분리, 부선, 산 침출 공정을 통해 저품위 원료를 유리용 및 고순도 제품으로 고품위화하여, 1톤당 50-100달러의 이익을 확보하고 있습니다. 이러한 이익률 향상은 북미 규사 업계 전체의 수익 구조에도 변화를 가져오고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the north america silica sand market size is projected to expand from 41.12 Million tons in 2025 and 43 Million tons in 2026 to 53.80 Million tons by 2031, registering a CAGR of 4.58% between 2026 to 2031.

This report is Segmented by End-User Industry (Glass Manufacturing, Foundry, and More), Product Form (Natural Frac Sand, Northern White Sand, and More), Mesh/Grain Size (less Than 70 Mesh, 70-120 Mesh, and More), Processing Method (Wet Silica Sand and Dry and Screened Sand), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Volume (Tons).

North America Silica Sand Market Trends and Insights

Foundry-Casting Output Recovery

The American Foundry Society projects casting sales to rise 1.9% in 2025 and 4.1% in 2026, then average 4.6% a year to 2030. Forty-one percent of US foundries reported order gains tied to reshoring, and 96% plan capital spending in 2026, signaling sustained silica demand for molds. Foundry-grade sand usage tracks ton-for-ton with ferrous castings, so a USD 52 billion domestic foundry sector concentrated near Midwestern sand deposits cuts inbound freight and tightens supply chains. Smaller shops face higher gas costs that could temper sand intensity if electric-arc melting spreads, yet proximity advantages and rising automotive lightweighting favor steady growth in the North America silica sand market.

Shale Rig-Count Up-Cycle and In-Basin Frac Sand

Permian proppant needs climbed from 14 million tons in 2016 to almost 80 million tons in 2025, equaling 60% of US demand. Lateral lengths now average 10,000-15,000 tons of sand per well, keeping near-term pull firm despite a January 2026 rig count of 546, down 36 year-over-year. In-basin brown sand prices run USD 10-15 per ton below Northern White and meet crush thresholds for moderate depths, spurring capacity additions like Wallstreet Sand's February 2026 Kermit plant. The dynamic compresses rail-delivered margins for Wisconsin mines and drives diversification into industrial niches within the North America silica sand market.

High Logistics-Cost Volatility

Rail rates for SCTG 11 industrial sand move with bulk-commodity cycles, eroding margins for northern mines shipping to Texas and Alberta. PropFlow's wet-sand pipe claims USD 6 per-ton delivery costs yet requires fixed pipelines, limiting uptake. As operators pivot to in-basin dry sand, distant producers either swallow USD 40-60 per-ton rail spreads or pivot into filtration, glass, and specialty grades where quality premiums cover freight. Smaller firms that lack multi-year contracts absorb spot-rate spikes, tightening working capital in the North America silica sand market.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure-Led Construction Sand Needs

- Semiconductor-Grade HP-Silica Reshoring

- Water-Stress Restrictions in Arid Basins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oil and Gas held 51.89% of the 2025 volume, confirming its anchor role in the North America Silica Sand market share. Filtration and Water Treatment, however, is set to outpace at 5.31% CAGR through 2031 as cities replace aging plants to meet Safe Drinking Water Act thresholds.

Glass manufacturing ranks second, demanding sand above 98% SiO2 and iron below 0.03% Fe2O3, specs that in-basin brown sand rarely meets and which sustain Northern White premiums. Foundry applications were boosted with casting growth tied to automotive lightweighting and reshoring. Chemicals, ceramics, coatings, and niche recreational uses round out demand, each rewarding mesh-size and purity tailoring. The North America silica sand market size allocated to filtration and glass, therefore, looks positioned for consistent expansion, insulating miners from proppant cyclicality.

Northern White supplied 40.88% of 2025 tonnage, anchoring deep-well proppant, glass, and foundry channels. High-purity silica exceeding 99.9% SiO2 will grow 5.51% a year to 2031, buoyed by semiconductor and photovoltaic demand that values tight metal specs.

In-basin brown sand, selling USD 10-15 per ton cheaper, commands a proppant share for moderate depths but remains unsuitable for glass or semiconductor use. Value lies in beneficiation: magnetic separation, flotation, and acid-leach lines upgrade lower-grade feed into glass or high-purity outputs, capturing USD 50-100 per-ton margins. That margin lift shifts revenue mix across the North America silica sand industry even.

List of Companies Covered in this Report:

- AGSCO Corp

- Alpine Silica

- American Silica.

- Atlas Energy Solutions

- Badger Mining Corporation

- Black Mountain Sand

- Capital Sand Company

- CARBO Ceramics Inc.

- Covia Holdings LLC

- Freedom Proppant

- Sibelco

- Signal Peak Silica

- Sil Industrial Minerals

- SiO Silica, Inc.

- SmartSand, Inc.

- Source Energy Services Ltd.

- Superior Silica Sands

- U.S. Silica

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Foundry-casting output recovery

- 4.2.2 Shale rig-count up-cycle and in-basin frac sand

- 4.2.3 Infrastructure-led construction sand needs

- 4.2.4 Semiconductor-grade HP-silica reshoring

- 4.2.5 Closed-loop sand-reuse pilots at E&Ps

- 4.3 Market Restraints

- 4.3.1 High logistics-cost volatility

- 4.3.2 Water-stress restrictions in arid basins

- 4.3.3 Cap-ex freeze among Tier-2 drillers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-User Industry

- 5.1.1 Glass Manufacturing

- 5.1.2 Foundry

- 5.1.3 Oil and Gas (Frac/Proppant)

- 5.1.4 Construction Materials

- 5.1.5 Filtration and Water Treatment

- 5.1.6 Chemicals Production

- 5.1.7 Ceramics and Refractories

- 5.1.8 Paints and Coatings

- 5.1.9 Other Niche Uses

- 5.2 By Product Form

- 5.2.1 Natural Frac Sand

- 5.2.2 Northern White Sand

- 5.2.3 In-Basin Brown Sand

- 5.2.4 Glass-Grade Sand

- 5.2.5 Foundry-Grade Sand

- 5.2.6 High-Purity Silica (more than 99.9% SiO2)

- 5.3 By Mesh/Grain Size

- 5.3.1 less than 70 Mesh

- 5.3.2 70-120 Mesh

- 5.3.3 120-200 Mesh

- 5.3.4 more than 200 Mesh

- 5.4 By Processing Method

- 5.4.1 Wet Silic Sand

- 5.4.2 Dry and Screened Sand

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AGSCO Corp

- 6.4.2 Alpine Silica

- 6.4.3 American Silica.

- 6.4.4 Atlas Energy Solutions

- 6.4.5 Badger Mining Corporation

- 6.4.6 Black Mountain Sand

- 6.4.7 Capital Sand Company

- 6.4.8 CARBO Ceramics Inc.

- 6.4.9 Covia Holdings LLC

- 6.4.10 Freedom Proppant

- 6.4.11 Sibelco

- 6.4.12 Signal Peak Silica

- 6.4.13 Sil Industrial Minerals

- 6.4.14 SiO Silica, Inc.

- 6.4.15 SmartSand, Inc.

- 6.4.16 Source Energy Services Ltd.

- 6.4.17 Superior Silica Sands

- 6.4.18 U.S. Silica

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment