|

시장보고서

상품코드

2072616

VRLA 배터리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)VRLA Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

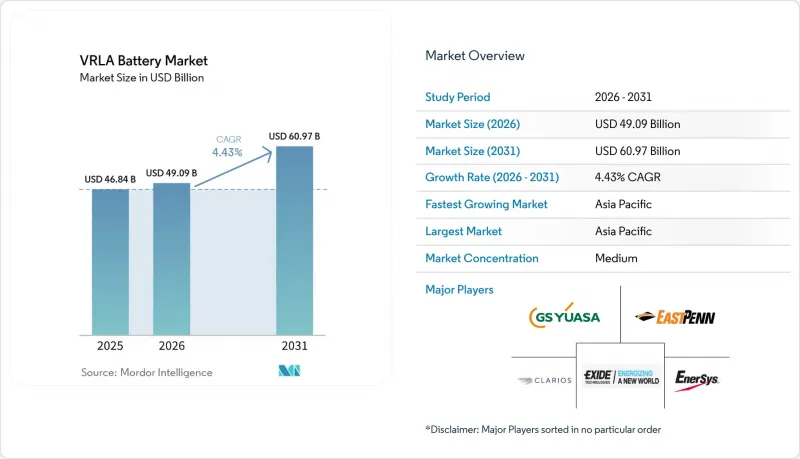

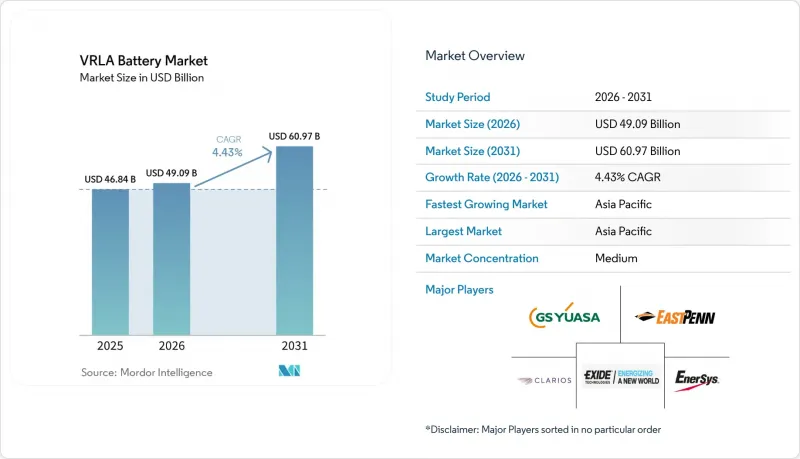

Mordor Intelligence에 의하면, VRLA 배터리 시장 규모는 2025년 468억 4,000만 달러로 평가되었고, 2026년에는 490억 9,000만 달러로 추정되고, 2031년까지 609억 7,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 4.43%로 성장할 전망입니다.

본 보고서는 유형별(AGM, 젤, TPPL, 하이브리드 젤 및 AGM), 용도별(UPS, 통신 및 데이터센터, 에너지 저장, 자동차, 산업용, 비상 조명, 의료기기), 최종 사용자별(주거용, 상업용, 산업용, 유틸리티), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 VRLA 배터리 시장 동향 및 분석

통신 인프라 분야에서 신뢰성이 높은 백업 전원에 대한 수요 증가

스몰 셀 5G를 구축하려면 2-4시간의 자율 작동 시간이 필요하지만, 리튬 이온 배터리로 인한 화재 위험을 방지해야 합니다. 리튬 이온 배터리는 인허가 절차가 복잡하기 때문에 AGM VRLA(흡수성 유리섬유 매트 방식 밸브 제어 납축전지)가 여전히 선호되는 선택지로 남아 있습니다. 이는 능동적인 냉각이 필요하지 않아, 인구 밀도가 높은 도시 지역의 보험 비용을 절감할 수 있기 때문입니다. 인도에서는 타워 사업자들이 리튬 배터리의 열 관리 비용을 피하기 위해 AGM 배터리의 교체 주기를 5년으로 정하고 있습니다. 이 접근 방식은 아프리카의 18,000개 Off-grid 현장에서도 마찬가지로 채택되어 있으며, 디젤 발전기 사용을 최소화하기 위해 태양광 발전 시스템과 VRLA 배터리가 결합되어 있습니다. 오픈 RAN 아키텍처 역시 소형 VRLA 배터리 구성의 이점을 누리고 있지만, 서유럽에서 진행된 시범 프로젝트에 따르면 2028년까지 전력망이 안정적인 시장에서는 리튬 배터리가 이러한 추세에 변화를 가져올 가능성이 있는 것으로 나타났습니다.

제2·제3급 도시의 엣지 데이터센터 및 UPS 확충

지연 시간에 민감한 용도의 경우, 연산 능력이 소규모 시설로 이전되고 있으며, 이러한 시설에서는 일반적으로 10-50kW급 UPS 시스템이 사용되고 있습니다. 20kW 규모의 엣지 사이트의 경우, AGM VRLA 배터리의 비용은 약 8,000달러인 반면, 동등한 성능의 리튬 이온 배터리는 1만 4,000달러가 듭니다. 또한, VRLA 배터리의 경우, 설치 작업을 30%나 늘리게 되는 배터리 관리의 복잡성을 피할 수도 있습니다. 그러나 여유 공간이 제한되면, 그 경향은 달라집니다. 에너지 밀도가 3배 더 높은 리튬 이온 배터리를 채택함으로써, 수익을 창출할 수 있는 서버용 바닥 면적을 확보할 수 있습니다. 이러한 추세는 2027년 이후 리튬 이온 배터리 팩 가격이 1kWh당 100달러 아래로 떨어질 것으로 예상되는 시점에서 더욱 가속화될 것으로 전망됩니다.

LFP 배터리 팩의 급격한 가격 하락

공급 과잉으로 인해 2025년 상반기에는 중국의 LFP 배터리 팩 가격이 톤당 3,000위안 이상 하락했으며, 3년 가동 주기 기준 VRLA 배터리와의 비용 차이는 한 자릿수 수준으로 좁혀졌습니다. 엣지 데이터센터 운영사들은 현재 리튬 배터리가 랙 공간을 60-70% 절약할 수 있다는 점을 고려해, 10-15%의 할증 요금을 지불할 의향이 있습니다. 이는 콜로케이션 수익 증가로 직결되는 사항입니다. 베트남에서는 전기 이륜차 OEM 업체들이 2025년까지 납축전지 사용률을 85%로 줄일 예정이어서, 대체재 확보에 대한 위험이 부각되고 있습니다. 그러나 고정형 LFP 배터리는 사이클 수명 인증으로 인해 여전히 25-30%의 프리미엄 가격을 유지하고 있으며, 배터리 수명의 95%를 플로트 모드에서 사용하는 용도에서는 VRLA와 경쟁 구도가 유지되고 있습니다.

부문별 분석

AGM 기술은 UPS 시스템 및 통신 캐비닛에서의 광범위한 채택에 힘입어 2025년 예상 매출의 63.3%를 차지했습니다. 하이브리드 젤 및 AGM은 현재 매출 점유율이 9.8%이지만, 기온이 55°C에 달하는 환경에서 12-15년의 플로트 수명에 대한 수요에 힘입어 연평균 성장률(CAGR) 7.8%로 성장하고 있습니다. TPPL은 엔터프라이즈 데이터센터나 철도 신호 시스템 등 프리미엄 틈새 시장을 대상으로 하며, 30-40%의 가격 프리미엄을 적용하고 15-20년의 수명을 제공함으로써 교체 주기를 연장하고 있습니다.

시장 세분화에서는 비용 고려가 중요한 역할을 합니다. 12V 100Ah AGM 유닛의 가격은 약 200달러로, 하이브리드 겔 배터리보다 약 25% 저렴합니다. 그러나 AGM 배터리는 열로 인한 성능 저하(열적 디레이팅)가 발생하며, 45°C를 초과하는 온도에서는 수명이 절반으로 단축됩니다. FIAMM이 2026년에 'Pure Guard'를 출시함에 따라 하이브리드 겔 배터리의 수량은 20% 감소했으며, 리튬 배터리와의 폼 팩터 차이가 좁혀졌습니다. EnerSys는 TPPL 배터리 팩에 IoT 센서를 탑재하여, 부적절한 충전 작업으로 인한 VRLA 배터리의 조기 고장(전체 고장의 18-22%)을 해결하기 위한 예측 유지보수를 실현했습니다. 향후 도입될 디지털 여권의 요건에 따라, TPPL이나 하이브리드 젤 등 상태(SoH) 프로파일이 안정적인 화학계 배터리는 시장 점유율을 더욱 확대할 수 있는 위치에 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 43.1%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 5.1%로 성장할 것으로 전망됩니다. 중국은 범용 AGM 배터리 수출 분야에서 계속해서 주도적인 위치를 유지하고 있는 반면, 인도는 가정용 UPS 판매를 통해 국내 시장의 성장을 이끌고 있습니다. 아세안 시장의 상황은 제각각입니다. 베트남의 이륜차 시장에서는 여전히 납축전지가 85%를 차지하고 있지만, 태국 정부의 보조금 덕분에 납축전지와 리튬이온전지의 가격 차이는 한 자릿수 수준으로 좁혀졌습니다.

북미에서는 하이퍼스케일 데이터센터 사업자들이 기존 엔터프라이즈 시설의 TPPL 배터리를 교체하는 한편, 신규 엣지 시설 건설에는 리튬 이온 배터리를 우선적으로 채택하고 있습니다. 2025 회계연도에는 섹션 45X 세액 공제를 통해 EnerSys에 1억 8,460만 달러가 배정되어, 국내 TPPL 생산을 지원함과 동시에 아시아 공급망에 대한 의존도를 낮췄습니다. 그러나 이러한 세액 공제가 2032년에 만료됨에 따라, 미래에 대한 우려가 커지고 있습니다.

유럽에서는 EU 배터리 규제로 인한 과제에 직면해 있습니다. 이 규제로 인해 단가 비용은 상승했으나, 폐쇄형 재활용 시스템을 갖춘 기존 기업들에게는 경쟁상의 우위도 가져다주었습니다. 규정 준수 요건으로 인해 역물류 비용이 12-15% 상승하여 전반적인 수익성에 영향을 미치고 있습니다.

중국에서는 도시 지역의 데이터센터에 리튬 이온 배터리가 보급됨에 따라, 국내 VRLA 시장은 점차 안정화되고 있습니다. 수출 지향적인 제조업체들은 중동 및 아프리카의 고수익 사업 기회를 포착하기 위해 하이브리드 젤형 및 TPPL형 제품에 주력하고 있습니다.

인도에서는 2025년에 엣지 데이터센터의 용량이 180MW 증가한 것으로 평가되었으며, 그 중 68%의 도입 사례에서 내구성과 전력망과의 호환성을 이유로 AGM VRLA 배터리가 채택되었습니다. 아세안(ASEAN)에서는 베트남의 전기 이륜차 시장에서 여전히 85%가 납축전지를 주로 사용하는 반면, 인도네시아와 태국에서는 정부의 보조금 지원에 힘입어 리튬이온전지 도입이 가속화되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the VRLA battery market size is expected to increase from USD 46.84 billion in 2025 to USD 49.09 billion in 2026 and reach USD 60.97 billion by 2031, growing at a CAGR of 4.43% over 2026-2031.

This report is Segmented by Type (AGM, Gel, TPPL, Hybrid-Gel/AGM), Application (UPS, Telecom & Data Centers, Energy Storage, Automotive, Industrial, Emergency Lighting, Medical Devices), End-User (Residential, Commercial, Industrial, Utilities), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global VRLA Battery Market Trends and Insights

Rising demand for reliable back-up power in telecom infrastructure

Small-cell 5G deployments require 2-4 hours of autonomy without the fire-risk profile associated with lithium-ion batteries, which complicates permitting processes. AGM VRLA (Absorbent Glass Mat Valve-Regulated Lead-Acid) batteries remain the preferred choice as they eliminate the need for active cooling and reduce insurance costs in densely populated urban areas. In India, tower operators adopt five-year AGM replacement cycles to avoid the thermal management expenses of lithium batteries. This approach is similarly observed across 18,000 off-grid sites in Africa, where solar arrays are paired with VRLA batteries to minimize diesel generator usage. Open RAN architectures also benefit from compact VRLA battery configurations; however, pilot projects in Western Europe indicate that lithium batteries could challenge this preference in stable-grid markets by 2028.

Edge Data-Center & UPS Build-Outs in Tier-2/3 Cities

Latency-sensitive applications are shifting compute capacity to smaller facilities, which typically utilize 10-50 kW UPS systems. A 20 kW edge site incurs approximately USD 8,000 for AGM VRLA batteries compared to USD 14,000 for equivalent lithium-ion batteries, while also avoiding the added battery-management complexity that increases installation labor by 30%. However, the preference shifts when rack space becomes limited; lithium-ion batteries, with their threefold energy density, free up floor space for revenue-generating servers. This shift is anticipated to gain momentum once lithium-ion pack prices fall below USD 100/kWh, projected after 2027.

Rapid price decline of LFP battery packs

Overcapacity led to a reduction in Chinese LFP pack prices by more than CNY 3,000 per ton in the first half of 2025, narrowing the cost difference with VRLA batteries to single digits for three-year duty cycles. Edge data center operators are now willing to pay a 10-15% premium for lithium batteries due to their ability to save 60-70% of rack space, which can be directly translated into increased colocation revenue. In Vietnam, electric two-wheeler OEMs reduced lead-acid battery usage to 85% in 2025, highlighting the risk of substitution. However, stationary-grade LFP batteries continue to command a 25-30% premium due to cycle-life certifications, maintaining VRLA's competitiveness in applications where batteries spend 95% of their lifespan in float mode.

Other drivers and restraints analyzed in the detailed report include:

- Renewable Micro-Grids Needing Low-CAPEX Storage

- Cost Advantage Versus Lithium-Ion for <= 3-Year Duty Cycles

- Lead Price Volatility & Stringent Recycling Directives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AGM technology accounted for 63.3% of the projected 2025 revenue, driven by its widespread use in UPS systems and telecom cabinets. Hybrid-Gel/AGM currently holds a 9.8% revenue share but is growing at a compound annual growth rate (CAGR) of 7.8%, supported by demand for 12-15-year float life in environments with temperatures reaching 55 °C. TPPL caters to premium niche markets, including enterprise data centers and rail signaling, offering 15-20-year lifespans at a 30-40% price premium, which extends replacement intervals.

Cost considerations play a significant role in market segmentation. A 12 V 100 Ah AGM unit is priced at approximately USD 200, about 25% less than Hybrid-Gel. However, AGM batteries experience thermal derating, which reduces their lifespan by half in temperatures exceeding 45 °C. FIAMM's 2026 Pure Guard launch led to a 20% reduction in Hybrid-Gel volume, narrowing the form-factor gap with lithium batteries. EnerSys has integrated IoT sensors into TPPL battery packs, enabling predictive maintenance to address the 18-22% of premature VRLA failures caused by inadequate topping-up practices. With the upcoming digital passport requirement, chemistries with stable state-of-health profiles, such as TPPL and Hybrid-Gel, are positioned to capture additional market share.

Complete Report Scope:

- By Type

- Absorbent Glass Mat (AGM)

- Gel

- Thin-Plate Pure Lead (TPPL)

- Hybrid-Gel/AGM

- By Application

- Uninterruptible Power Supply (UPS)

- Telecom and Data Centers

- Energy Storage Systems

- Automotive and Transportation

- Industrial Equipment

- Emergency Lighting

- Medical Devices and Toys

- By End-user

- Residential

- Commercial

- Industrial

- Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

In 2025, the Asia-Pacific region accounted for 43.1% of global revenue and is projected to grow at a 5.1% CAGR through 2031. China remains a leader in commodity AGM exports, while India drives domestic growth through residential UPS sales. ASEAN markets show a mixed landscape: Vietnam's two-wheeler market remains 85% lead-acid, whereas Thai government subsidies have reduced the cost gap between lead-acid and lithium-ion batteries to single digits.

In North America, hyperscale data center operators are retrofitting enterprise facilities with TPPL batteries while favoring lithium-ion for new edge builds. Section 45X tax credits allocated USD 184.6 million to EnerSys in FY2025, supporting domestic TPPL production and mitigating reliance on Asian supply chains. However, the expiration of these credits in 2032 raises future concerns.

Europe faces challenges from the EU Battery Regulation, which has increased per-unit costs but also created competitive advantages for established players with closed-loop recycling systems. Reverse-logistics costs have risen by 12-15% due to compliance requirements, impacting overall profitability.

China's VRLA market is stabilizing domestically as lithium-ion batteries gain popularity in urban data centers. Export-oriented manufacturers are focusing on Hybrid-Gel and TPPL variants to capture higher-margin opportunities in the Middle East and Africa.

India added 180 MW of edge data center capacity in 2025, with 68% of installations specifying AGM VRLA batteries due to their durability and compatibility with the grid. In ASEAN, Vietnam's electric two-wheeler market remains predominantly lead-acid at 85%, while Indonesia and Thailand are accelerating lithium-ion adoption through government subsidies.

- GS Yuasa Corporation

- Panasonic Corporation

- Exide Technologies

- EnerSys

- C&D Technologies

- Clarios

- East Penn Manufacturing

- Leoch International

- Amara Raja Batteries

- Haze Battery Company

- Narada Power Source

- Vision Group

- Koyo Battery

- B.B. Battery

- FIAMM Energy Technology

- Saft ( TotalEnergies )

- HOPPECKE Batterien

- Trojan Battery

- NorthStar Battery

- Eternity Technologies

- Other Notable Players

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for reliable back-up power in telecom infrastructure

- 4.2.2 Data-center & UPS build-outs in Tier-2/3 cities

- 4.2.3 Renewable micro-grids needing low-CAPEX storage

- 4.2.4 Cost advantage vs. lithium-ion for <= 3-yr duty cycles

- 4.2.5 Micro-mobility boom in ASEAN & Africa

- 4.2.6 Hybrid-gel VRLA designs for 55 °C climates

- 4.3 Market Restraints

- 4.3.1 Rapid price decline of LFP battery packs

- 4.3.2 Lead price volatility & stringent recycling directives

- 4.3.3 Rack-space premium in edge UPS (Below 10 kW)

- 4.3.4 Premature failures due to maintenance myths

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Absorbent Glass Mat (AGM)

- 5.1.2 Gel

- 5.1.3 Thin-Plate Pure Lead (TPPL)

- 5.1.4 Hybrid-Gel/AGM

- 5.2 By Application

- 5.2.1 Uninterruptible Power Supply (UPS)

- 5.2.2 Telecom and Data Centers

- 5.2.3 Energy Storage Systems

- 5.2.4 Automotive and Transportation

- 5.2.5 Industrial Equipment

- 5.2.6 Emergency Lighting

- 5.2.7 Medical Devices and Toys

- 5.3 By End-user

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Utilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 GS Yuasa Corporation

- 6.4.2 Panasonic Corporation

- 6.4.3 Exide Technologies

- 6.4.4 EnerSys

- 6.4.5 C&D Technologies

- 6.4.6 Clarios

- 6.4.7 East Penn Manufacturing

- 6.4.8 Leoch International

- 6.4.9 Amara Raja Batteries

- 6.4.10 Haze Battery Company

- 6.4.11 Narada Power Source

- 6.4.12 Vision Group

- 6.4.13 Koyo Battery

- 6.4.14 B.B. Battery

- 6.4.15 FIAMM Energy Technology

- 6.4.16 Saft ( TotalEnergies )

- 6.4.17 HOPPECKE Batterien

- 6.4.18 Trojan Battery

- 6.4.19 NorthStar Battery

- 6.4.20 Eternity Technologies

- 6.4.21 Other Notable Players

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment