|

시장보고서

상품코드

2073588

유럽의 납축전지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Lead-acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

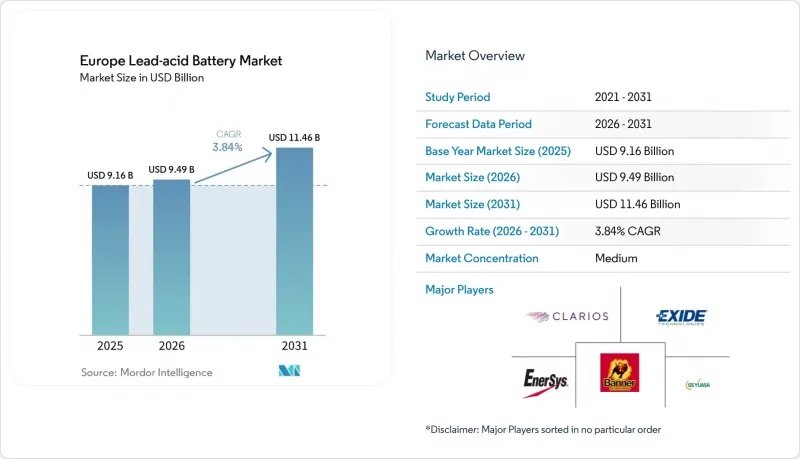

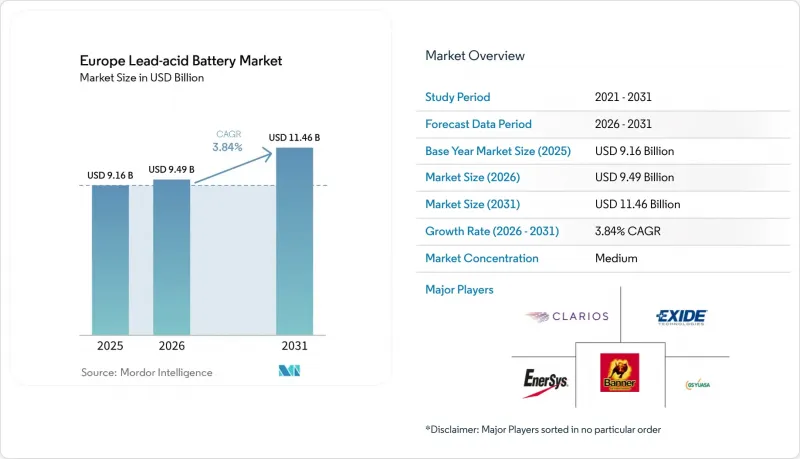

Mordor Intelligence에 의하면, 유럽의 납축전지 시장 규모는 2025년 91억 6,000만 달러로 평가되었습니다. 2026년에는 94억 9,000만 달러로 확대되어 2031년까지 114억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 3.84%로 성장할 전망입니다.

본 보고서는 구조 방식(액체식 및 VRLA), 용도(시동·조명·점화, 고정형, 동력·견인용, 휴대용 및 기타), 지역(독일, 영국, 프랑스, 스페인, 이탈리아, 북유럽 국가, 러시아 및 기타 유럽 국가)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

유럽의 납축전지 시장 동향 및 인사이트

내연기관(ICE) 및 마이크로 하이브리드 차량의 판매량 증가

2025년 11월까지 유럽의 신차 등록 대수의 83%를 내연기관 및 하이브리드 구동 시스템이 차지했으며, 4-6년마다 보조 배터리를 교체해야 하는 광범위한 도입 기반이 유지되었습니다. 독일에서는 2024년에 410만 대의 차량이 생산되었으며, 그 대부분에는 첨단 액체식 또는 AGM(흡수 유리 매트)형 배터리가 필요한 48볼트 마일드 하이브리드 시스템이 탑재되어 있습니다. 2024년 러시아의 경차 판매 대수는 147만 대였으나, 배터리식 전기차의 보급률은 1% 미만에 그쳤으며, 동유럽 전역에서 기존 SLI 배터리에 대한 수요가 계속되고 있습니다. 이탈리아에서는 2024년 배터리식 전기차 시장 점유율이 고작 4.2%에 그치고 있어, 유럽의 납축전지 시장에 유리한 영향을 미치는 지역 간 격차가 뚜렷이 드러나고 있습니다. 유럽 전역에서 차량의 평균 사용 연수가 9년에 육박함에 따라, 예측 가능한 애프터마켓 주기가 유지되고 있습니다.

데이터센터 및 UPS 설비의 확충

유럽 데이터센터의 용량은 2024년에 10GW에 달했으며, 프랑크푸르트, 암스테르담, 런던, 파리에서 클라우드 및 엣지 사업자들이 시설을 확장함에 따라 연간 8-10%의 성장세를 보였습니다. 백업 시간이 15분 미만이고, 비용 측면의 제약이 리튬 이온 배터리의 에너지 밀도 우위를 상회하는 경우, UPS 도입 시 밸브 제어형 납축전지(VRLA)가 여전히 약 80%를 차지하고 있습니다. 통신 사업자들은 약 50만 곳의 통신탑 부지를 운영하고 있으며, 2025년까지 10만 기의 5G 스몰셀을 추가할 예정입니다. 각 스몰 셀은 온도 변동에 강한 48볼트 VRLA 배터리 스트링에 의존하고 있습니다. 새로운 순수 납 AGM 설계는 부분 충전 상태에서 작동 시 사이클 수명을 20% 연장하여 사업자의 총 비용을 절감합니다. 지연 시간에 민감한 워크로드를 지원하는 엣지 데이터센터에서는 능동적인 환기가 필요 없는 밀폐형 유닛이 선호됩니다.

리튬 이온 배터리의 급격한 비용 하락

리튬 이온 배터리 팩의 가격은 2023년에 kWh당 140달러 아래로 떨어졌으며, 2030년까지 추가로 40% 하락할 것으로 예상되어, 많은 고정형 용도에서 VRLA와의 총 소유 비용(TCO) 격차가 좁혀지고 있습니다. 프랑크푸르트와 암스테르담의 하이퍼스케일 사업자들은 15년의 수명과 80%의 방전 깊이를 달성하기 위해, 신규 건설 시 이미 리튬이온 백업 시스템을 지정하고 있습니다. 스페인에서 계획 중인 10.5GW 규모의 유틸리티급 에너지 저장 시스템 프로젝트는 대부분 2-4시간의 에너지 이동(energy shift)을 목적으로 하고 있으며, 거의 전부가 리튬 이온 배터리로 구성되어 있습니다. 이로 인해 납축전지는 사용 시간이 더 짧은 용도로만 제한되게 되었습니다. 리튬 탄산염 가격의 급락으로 인해, 그동안 유럽의 납축전지 시장을 지탱해 온 원자재 비용 측면의 경쟁력이 사라졌습니다. 그럼에도 불구하고, 한랭 지역에서의 성능과 재활용 분야에서의 선도적 입지 덕분에 납축전지에는 여전히 확고한 틈새 시장이 남아 있습니다.

부문별 분석

2025년에는 4-6년마다 SLI 유닛을 교체하는 비용 효율성을 중시하는 자동차 애프터마켓 구매자들 덕분에 액체형 배터리가 매출의 63.8%를 차지했습니다. AGM 및 젤 유형을 포함한 VRLA는 통신 사업자와 데이터센터가 밀폐형 운영과 환기 요건 완화를 우선시함에 따라 연평균 6.1%의 성장률을 보이고 있습니다. 유체 기술 분야에서는 마이크로 하이브리드의 스타트-스톱 시스템의 수명을 30만 사이클까지 연장하는 칼슘-은 그리드의 개량이 계속되고 있습니다. AGM은 이미 프리미엄 SLI 수요의 25%를 차지하고 있으며, 클라리오스사가 하노버, 츠비카우 및 스페인에 신설한 2억 유로 규모의 생산 능력의 혜택을 받고 있습니다. 젤형 배터리는 절대적인 생산량은 적지만, 내진동성과 심방전 성능이 높은 가격을 정당화하는 태양광 발전용 축전 및 선박용 부문에서 시장 점유율을 확대되고 있습니다.

첨단 전해액 방식의 납축전지는 기존 충전실에 의존하는 독일, 네덜란드, 프랑스의 물류 허브에서 사용되는 지게차 분야에서 여전히 확고한 입지를 다지고 있습니다. EU의 "재활용 함량 85%" 이러한 의무화는 어떤 구조 유형에 있어서도 장애물이 되지 않습니다. 왜냐하면 유럽의 납축전지 시장은 이미 99%의 회수·재활용률을 달성한 반면, 리튬이온전지 재활용 업체들은 아직 규모 확대의 초기 단계에 있기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the europe lead-acid battery market size is expected to increase from USD 9.16 billion in 2025 to USD 9.49 billion in 2026 and reach USD 11.46 billion by 2031, growing at a CAGR of 3.84% over 2026-2031.

This report is Segmented by Construction Method (Flooded and VRLA), Application (Starting-Lighting-Ignition, Stationary, Motive/Traction, and Portable and Others), and Geography (Germany, United Kingdom, France, Spain, Italy, NORDIC Countries, Russia, and Rest of Europe). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Europe Lead-acid Battery Market Trends and Insights

Rising Sales of ICE and Micro-hybrid Vehicles

Internal-combustion and hybrid drivetrains represented 83% of European new-car registrations through November 2025, preserving a wide installed base that must replace auxiliary batteries every 4-6 years. Germany produced 4.1 million vehicles in 2024, most of which integrate 48-volt mild-hybrid systems needing advanced flooded or absorbed-glass-mat (AGM) units. Russia's 1.47 million light-vehicle sales in 2024 showed battery-electric penetration below 1%, extending demand for conventional SLI batteries across Eastern Europe. Italy reported only a 4.2% battery-electric share in 2024, highlighting regional divergence that benefits the European lead-acid battery market. A fleet age near nine years across the continent sustains predictable aftermarket cycles.

Expanding Data-center and UPS Installations

European data-center capacity reached 10 GW in 2024 and is growing 8-10% annually as cloud and edge operators scale facilities in Frankfurt, Amsterdam, London, and Paris. Valve-regulated lead-acid (VRLA) batteries still dominate roughly 80% of UPS deployments where backup duration is under 15 minutes and cost discipline outweighs lithium-ion's energy-density advantage. Telecom carriers operate about 500,000 tower sites and will add 100,000 5G small cells by 2025, each relying on 48-volt VRLA strings tolerant of temperature swings. New pure-lead AGM designs extend cycle life by 20% in partial-state-of-charge duty, reducing total cost for operators. Edge data centers that support latency-sensitive workloads favor sealed units requiring no active ventilation.

Rapid Cost Decline of Lithium-ion Chemistries

Lithium-ion pack prices slipped below USD 140 per kWh in 2023 and are set to fall another 40% by 2030, narrowing the total-cost-of-ownership gap with VRLA in many stationary uses. Hyperscale operators in Frankfurt and Amsterdam already specify lithium-ion backup for new builds to gain 15-year life and 80% depth of discharge. Spain's 10.5 GW utility-scale battery pipeline is almost entirely lithium-ion for two-to-four-hour energy-shifting projects, sidelining lead-acid to shorter-duration roles. Plunging lithium-carbonate prices removed a materials-cost advantage that previously supported the European lead-acid battery market. Even so, cold-weather performance and recycling leadership preserve defensible niches.

Other drivers and restraints analyzed in the detailed report include:

- EU Directives Driving Residential Solar-plus-storage

- Warehouse Automation Boosting Motive-power Demand

- Stringent Lead-emission Limits and Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flooded products delivered 63.8% revenue in 2025, thanks to cost-focused automotive aftermarket buyers who replace SLI units every four to six years. VRLA, encompassing AGM and gel types, is growing 6.1% annually as telecom carriers and data centers prioritize sealed operation and reduced ventilation demands. Flooded technology continues to refine calcium-silver grids that extend micro-hybrid start-stop life to 300,000 cycles. AGM already holds 25% of premium SLI demand and benefits from EUR 200 million of new capacity added by Clarios in Hanover, Zwickau, and Spain. Gel variants, though smaller in absolute volume, win share in solar-storage and marine segments where vibration resistance and deep-discharge capability justify higher price points.

Advanced flooded traction batteries remain entrenched in forklifts across German, Dutch, and French logistics hubs that rely on established charging rooms. The EU's 85% recycled-content mandate poses no hurdle to either construction type because the European lead-acid battery market already meets a 99% collection and recycling rate, whereas lithium-ion recyclers remain in early scale-up stages.

Complete Report Scope:

- By Construction Method

- Flooded

- VRLA

- By Application

- Starting-Lighting-Ignition (SLI)

- Stationary

- Motive/Traction (Forklifts, Golf-carts)

- Portable and Others

- By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Clarios (Johnson Controls Power Solutions)

- Exide Technologies

- GS Yuasa Corp.

- EnerSys

- Robert Bosch GmbH

- Amara Raja Batteries Ltd

- Leoch International

- BAE Batterien GmbH

- Banner GmbH

- FIAMM Energy Technology

- Hoppecke Batteries

- Saft Batteries

- Midac SpA

- Exmet Industries

- TAB d.d.

- Monbat AD

- Akkumulatorenfabrik MOLL

- C&D Technologies

- Narada Power

- NorthStar Battery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising sales of ICE & micro-hybrid vehicles

- 4.2.2 Expanding data-center & UPS installations

- 4.2.3 EU directives driving residential solar-plus-storage

- 4.2.4 Warehouse automation boosting motive-power demand

- 4.2.5 Partial-state-of-charge lead-carbon advances

- 4.2.6 EU circular-economy rules favouring 99% recyclability

- 4.3 Market Restraints

- 4.3.1 Rapid cost decline of Li-ion chemistries

- 4.3.2 Stringent lead-emission limits & compliance costs

- 4.3.3 Tight supply of high-purity primary lead concentrate

- 4.3.4 Growing OEM trials of solid-state starter batteries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Construction Method

- 5.1.1 Flooded

- 5.1.2 VRLA

- 5.2 By Application

- 5.2.1 Starting-Lighting-Ignition (SLI)

- 5.2.2 Stationary

- 5.2.3 Motive/Traction (Forklifts, Golf-carts)

- 5.2.4 Portable and Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 NORDIC Countries

- 5.3.7 Russia

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Clarios (Johnson Controls Power Solutions)

- 6.4.2 Exide Technologies

- 6.4.3 GS Yuasa Corp.

- 6.4.4 EnerSys

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Amara Raja Batteries Ltd

- 6.4.7 Leoch International

- 6.4.8 BAE Batterien GmbH

- 6.4.9 Banner GmbH

- 6.4.10 FIAMM Energy Technology

- 6.4.11 Hoppecke Batteries

- 6.4.12 Saft Batteries

- 6.4.13 Midac SpA

- 6.4.14 Exmet Industries

- 6.4.15 TAB d.d.

- 6.4.16 Monbat AD

- 6.4.17 Akkumulatorenfabrik MOLL

- 6.4.18 C&D Technologies

- 6.4.19 Narada Power

- 6.4.20 NorthStar Battery

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment