|

시장보고서

상품코드

2072685

E-Commerce 마케팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Ecommerce Marketing Services Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

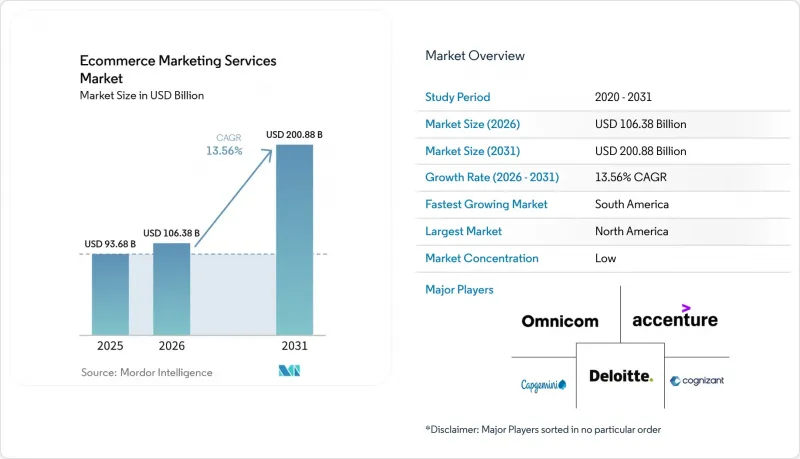

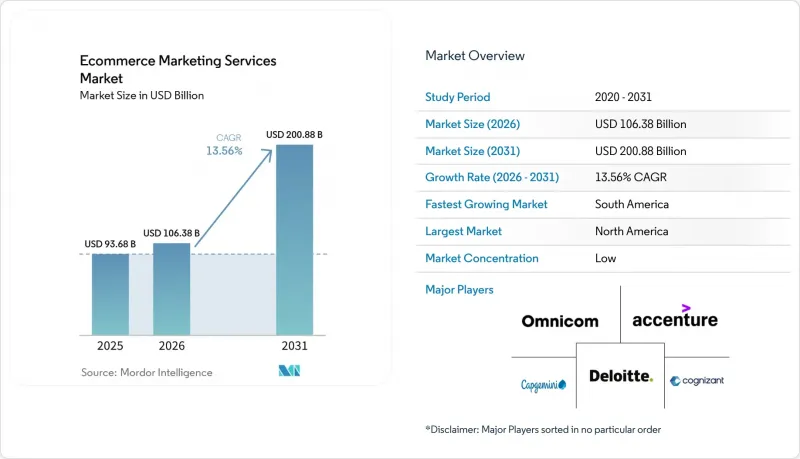

Mordor Intelligence에 의하면, E-Commerce 마케팅 서비스 시장 규모는 2025년에 936억 8,000만 달러로 평가되었고, 2026년에 1,063억 8,000만 달러로 추정되고, 2031년까지 2,008억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 13.56%로 성장할 전망입니다.

본 보고서는 서비스 유형별(검색 엔진 최적화(SEO), 유료 검색 및 쇼핑 광고, 유료 소셜 및 소셜 커머스 마케팅 등), 조직 규모별(중소기업 및 대기업), 최종 사용자 산업 분야별(소매 및 소비재, 패션 및 의류, 미용 및 퍼스널케어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 E-Commerce 마케팅 서비스 시장 동향 및 인사이트

AI를 활용한 개인화 및 크리에이티브 자동화가 전자상거래의 ROI를 향상시킵니다.

E-Commerce 마케팅 서비스 시장은 개인화가 더 이상 선택적 기능이 아니라 기본적인 기대 사항이 됨에 따라, AI 주도의 실행 단계로 전환되고 있습니다. Shopify의 보고서에 따르면, 2026년 1분기 기준 AI를 통해 유입된 방문자의 전환율은 자연 검색을 통해 유입된 방문자보다 약 50% 높았으며, 평균 주문 금액도 14% 더 높았다고 합니다. 이는 발견, 상품 데이터, 전환 워크플로우를 단일 프로그램에서 연동할 수 있는 대행사에게 있어 그 경쟁 우위를 입증하는 것입니다. 이러한 변화로 인해 대리점에 대한 업무 기준이 높아지고 있습니다. 왜냐하면, 오로지 인간으로만 구성된 크리에이티브 팀은 AI를 활용한 팀이 현재 달성하고 있는 테스트 속도나 컨텐츠 양에 대항할 수 없기 때문입니다. 또한, 이러한 변화로 인해 E-Commerce 마케팅 서비스 시장에서 고객들은 독자적인 워크플로우 도구, 강력한 피드 관리 기능, 그리고 보다 체계적인 카탈로그 운영 방식을 갖춘 파트너를 우선적으로 선택하게 되었습니다. 그 결과, 카탈로그의 내용 확충, 크리에이티브 작업의 자동화, 그리고 AI 기반 컨텐츠 제작은 단순한 부수적인 프로젝트를 넘어 핵심적인 정기 계약 업무로 전환되고 있습니다.

리테일 미디어와 마켓플레이스 광고 예산은 계속해서 증가하고 있습니다.

E-Commerce 마케팅 서비스 시장은 리테일 미디어와 마켓플레이스 광고의 확대를 발판으로 성장세를 이어가고 있습니다. 이는 브랜드가 구매 행동과 밀접한 관련이 있는 채널에 더 많은 예산을 배정하고 있기 때문입니다. 광고주들이 어트리뷰션이 불분명한 인지도 중심의 광고 공간보다 클로즈드 루프 측정이나 퍼스트 파티 거래 데이터를 우선시하게 되면서, 리테일 미디어의 매력이 높아지고 있습니다. 이러한 변화는 계정의 경제성에도 영향을 미치고 있으며, 스폰서십 상품 미디어, 진열대 가시성, 크로스 플랫폼 보고서 관리를 할 수 있는 대행사가 성과 중심의 예산에서 더 큰 점유율을 확보하고 있습니다. 가장 강력한 성장세는 여전히 북미와 유럽의 주요 리테일 미디어 생태계에 집중되어 있지만, 마켓플레이스 간의 경쟁이 치열해짐에 따라 유사한 구매 논리가 다른 지역으로도 확산되고 있습니다. 카테고리별 수요가 균일하게 변화하는 것은 아니기 때문에 미용, 퍼스널케어, 헬스케어, 기타 회전율이 높은 소비재 분야에서 강력한 입지를 확보한 대행사는 E-Commerce 마케팅 서비스 시장에서 더 유리한 위치에 있습니다.

고객 획득 비용(CAC)의 상승이 캠페인 효율을 저해하고 있습니다.

많은 대행사의 업무 범위가 유료 채널의 성과와 직접적으로 연결되어 있기 때문에 E-Commerce 마케팅 서비스 시장은 여전히 고객 확보 비용 상승으로 인한 압박에 직면해 있습니다. Shopify 가맹점 데이터에 따르면, CAC(고객 확보 비용)는 전년도의 274달러에서 2026년에는 318달러로 상승할 것으로 예상되며, 이는 대행사가 유료 고객 확보 예산의 타당성을 입증하고 투자 수익률(ROAS)을 유지하기 위해 더욱 노력해야 함을 의미합니다. 비용 증가가 전환율 향상보다 클 경우, 브랜드는 자금을 이메일, SMS, 로열티 프로그램, 제휴 프로그램 등의 고객 유지 채널로 전환합니다. 이러한 채널 구성의 변화로 인해 대행사에 대한 수요가 사라지는 것은 아니지만, E-Commerce 마케팅 서비스 시장에서 유료 고객 확보 관리에만 지나치게 의존하고 있는 기업의 성장세는 약화될 것입니다. 또한, 성과에 대한 설명 책임을 저해하지 않으면서 고객 확보 채널과 라이프사이클 채널 간에 클라이언트의 예산을 재분배할 수 있는 대행사가 유리해집니다.

부문별 분석

2025년, 유료 검색 및 쇼핑 광고는 E-Commerce 마케팅 서비스 시장 규모의 27.13%를 차지했으며, 여전히 최대 서비스 분야로서의 위상을 유지했습니다. 이는 구매 의도가 담긴 검색어가 여전히 구매 결정과 가장 밀접한 관련이 있기 때문입니다. 이 채널은 비용 압박이 커지더라도 여전히 지출의 대부분을 차지하고 있습니다. 이는 온라인으로 상품을 판매하는 브랜드에게 있어 여전히 수익과 가장 직접적으로 연결되는 경로 중 하나이기 때문입니다. 이 입지는 구글과 아마존이 상품 주도형 수요를 포착하는 데 있어 강점을 가지고 있다는 점에 힘입어 더욱 공고해지고 있습니다. 쇼핑객들은 이미 여러 선택지를 비교 검토하고 있기 때문입니다. E-Commerce 마케팅 서비스 시장에서 이는 피드 관리, 입찰 전략, 랜딩 페이지 최적화, 마켓플레이스와의 통합에 강점을 가진 대행사가 앞으로도 계속해서 고객과의 관계에서 중심적인 위치를 차지할 것임을 의미합니다.

유료 소셜 및 소셜 커머스 마케팅은 2026-2031년 연평균 성장률(CAGR) 16.53%를 나타낼 것으로 예측되며, E-Commerce 마케팅 서비스 시장에서 가장 빠르게 성장하는 서비스 유형이 될 전망입니다. 2025년 전 세계 소셜 미디어 광고 매출은 1,177억 달러에 달하고, 전년 대비 32.6% 증가를 기록했습니다. 이는 소셜 미디어가 주도하는 수요 환경의 규모와 상업적 견인력을 보여줍니다. 또한, 컨텐츠 및 인플루언서 프로그램도 직접 판매와 더욱 밀접하게 연계된 '구매 가능' 형태로 전환되고 있으며, 이에 따라 브랜드가 크리에이티브 성과나 채널의 가치를 평가하는 방식도 변화하고 있습니다. 동시에, 고객 확보 비용의 상승으로 인해 더 많은 성장 계획이 자사 채널의 재활성화로 전환되고 있어, 이메일, SMS, 푸시 알림을 활용한 고객 유지 마케팅의 중요성이 커지고 있습니다. 또한, 브랜드들이 소매 플랫폼 내 검색 가시성이 전환율과 통합 획득 비용 모두에 점점 더 큰 영향을 미칩니다는 사실을 인식함에 따라, 마켓플레이스 광고 및 디지털 선반 최적화도 확대되고 있습니다.

지역별 분석

2025년 E-Commerce 마케팅 서비스 시장에서 북미는 32.73%의 점유율을 차지했으며, 여전히 가장 규모가 큰 지역 수익 기반이 되었습니다. 한편, 아시아태평양은 2031년까지 가장 빠른 성장세를 보일 것으로 예측됩니다. 이 지역의 경쟁력은 기업의 마케팅 예산 확충, 리테일 미디어의 광범위한 도입, 그리고 이미 통합형 커머스 실행을 뒷받침하고 있는 성숙한 에이전시 생태계에 기인합니다. 미국에서는 2025년에 크리에이터 광고 시장 규모가 370억 달러에 달할 것으로 예상되며, 브랜드 예산이 커머스 연계형 컨텐츠 및 크리에이터 주도의 고객 유치로 빠르게 전환되고 있는 것으로 나타났습니다. 캐나다와 멕시코에서도 수요가 확대되고 있으며, 특히 모바일 커머스의 성장에 따라 현지화된 유료 소셜 광고, 마켓플레이스 광고 및 성과 측정 수요가 높아지고 있습니다. 또한, 개인정보 보호 규정 및 AI를 활용한 추천에 관한 지침이 대행사의 타겟팅, 컨텐츠 공개, 소비자 데이터 처리 방식을 형성하고 있기 때문에 규제 환경의 중요성도 점점 더 커지고 있습니다.

아시아태평양은 전자상거래의 보급이 계속해서 견조한 추세를 보이고 있으며, 브랜드들이 AI를 활용한 새로운 상거래 실행 방식으로 신속하게 전환하고 있는 만큼, E-Commerce 마케팅 서비스의 연평균 성장률(CAGR)이 15.29%로 가장 빠르게 성장하고 있는 지역 시장입니다. 중국은 해당 지역 최대의 내수 시장일 뿐만 아니라, AI 기반 상품 탐색, 소셜 커머스, 마켓플레이스 중심의 고객 유치 분야에서 주요 실험장으로 두각을 나타내고 있습니다. 인도, 한국, 호주에서도 국내 브랜드들이 유료 소셜 광고, 마켓플레이스 관리, 전환율 중심의 캠페인 업무를 외부에 위탁하는 경향이 강해짐에 따라 새로운 수요가 생겨나고 있습니다. 이로 인해 아시아태평양의 E-Commerce 마케팅 서비스 시장은 순수한 미디어 구매 규모와 마찬가지로 속도, 플랫폼 활용 능력, 현지화가 중요시되는 독특한 특징을 띠게 되었습니다.

유럽은 개인정보 보호 규제와 플랫폼 감독이 대행사의 데이터 수집 및 성과 측정 방식에 영향을 미치고 있기 때문에 E-Commerce 마케팅 서비스 시장에서 중요성은 있지만 구조적인 제약이 더 큰 지역입니다. 영국, 독일, 프랑스는 확립된 대리점 생태계와 견고한 소매 인프라를 통해 계속해서 지역 내 수요를 뒷받침하고 있습니다. 남미는 모바일 커머스와 마켓플레이스의 보급이 확대됨에 따라 중요한 성장 분야로 부상하고 있습니다. 특히 브라질에서는 플랫폼 간 경쟁이 치열해지는 가운데, 현지에서의 실행력과 디지털 진열대에서의 가시성이 더욱 중요시되고 있습니다. 중동 및 아프리카 역시 아랍에미리트와 사우디아라비아 등 여러 국가들이 디지털 상거래 인프라에 대한 투자를 지속하고 있을 뿐만 아니라, 나이지리아와 남아프리카공화국에서는 모바일 우선의 구매 행동을 중심으로 서비스 수요가 형성되고 있어 장기적인 성장 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the ecommerce marketing services market size is projected to be USD 93.68 billion in 2025, USD 106.38 billion in 2026, and reach USD 200.88 billion by 2031, growing at a CAGR of 13.56% from 2026 to 2031.

This report is Segmented by Service Type (Search Engine Optimization (SEO), Paid Search and Shopping Advertising, Paid Social and Social Commerce Marketing, and More), Organization Size (SMEs, and Large Enterprises), End-User Industry (Retail and Consumer Goods, Fashion and Apparel, Beauty and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Ecommerce Marketing Services Market Trends and Insights

AI-Driven Personalization and Creative Automation Improve Commerce ROI

The ecommerce marketing services market is moving toward AI-led execution because personalization has become a baseline expectation rather than an optional feature. Shopify reported that AI-referred visitors converted at nearly 50% higher rates than organic search visitors and had 14% higher average order values in Q1 2026, which strengthens the case for agencies that can connect discovery, product data, and conversion workflows in a single program. That shift is raising the operating standard for agencies because human-only creative teams cannot match the testing speed or content volume that AI-supported teams can now deliver. It is also pushing clients to favor partners with proprietary workflow tools, stronger feed management, and better-structured catalog practices in the ecommerce marketing services market. As a result, catalog enrichment, creative automation, and AI-ready content production are moving into core retainers instead of sitting in side projects.

Retail Media and Marketplace Advertising Budgets Keep Expanding

The ecommerce marketing services market is gaining momentum from the expansion of retail media and marketplace advertising, as brands are directing more budget to channels closely tied to purchase behavior. Retail media has become more attractive as advertisers prioritize closed-loop measurement and first-party transaction data over awareness-led placements with weaker attribution. That shift is also changing account economics because agencies that can manage sponsored product media, shelf visibility, and cross-platform reporting are winning a larger share of performance-led budgets. The strongest momentum remains concentrated in major retail media ecosystems in North America and Europe, though the same buying logic is now spreading to other regions as marketplace competition deepens. Category demand is not moving evenly, which means agencies with strong presence in beauty, personal care, health, and other fast-turning consumer verticals are better positioned in the ecommerce marketing services market.

Customer Acquisition Cost Inflation Compresses Campaign Efficiency

The ecommerce marketing services market still faces pressure from rising acquisition costs because many agency scopes are tied directly to paid channel performance. Shopify's merchant data showed CAC rising to USD 318 in 2026 from USD 274 a year earlier, which means agencies must work harder to justify paid acquisition budgets and defend return on spend. When costs rise faster than conversion efficiency, brands shift funds toward retention channels such as email, SMS, loyalty programs, and affiliate programs. That mix shift does not eliminate agency demand, but it does reduce momentum for firms that depend too heavily on paid acquisition management alone in the ecommerce marketing services market. It also favors agencies that can rebalance client budgets across acquisition and lifecycle channels without losing performance accountability.

Other drivers and restraints analyzed in the detailed report include:

- Rising Performance Pressure as Ecommerce Competition Intensifies

- Omnichannel Shopping and Social Commerce Raise Demand For Integrated Execution

- Signal Loss From Privacy Changes and Cookie Deprecation Weakens Targeting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paid search and shopping advertising held 27.13% of ecommerce marketing services market size in 2025, which kept it as the largest service line because commercial-intent queries still sit closest to purchase decisions. The channel continues to command spend even when cost pressure rises, because it remains one of the most directly attributable paths to revenue for brands selling online. That position is reinforced by Google's and Amazon's strength in capturing product-led demand; shoppers are already comparing options. In the ecommerce marketing services market, this means agencies with strong feed management, bid strategy, landing page discipline, and marketplace integration continue to sit in the center of client relationships.

Paid social and social commerce marketing is projected to grow at a 16.53% CAGR from 2026 to 2031, making it the fastest-growing service type in the ecommerce marketing services market. Social media advertising revenues reached USD 117.7 billion globally in 2025, rising 32.6% year over year, which shows the scale and commercial pull of social-led demand environments. Content and influencer programs are also shifting toward shoppable formats tied more closely to direct sales, which is changing how brands assess creative output and channel value. Email, SMS, and push retention marketing are gaining weight at the same time because rising acquisition costs are pushing more growth plans toward owned-channel reactivation. Marketplace advertising and digital shelf optimization are also expanding as brands recognize that search visibility inside retail platforms increasingly shapes both conversion and blended acquisition costs.

Complete Report Scope:

- By Service Type

- Search Engine Optimization (SEO)

- Paid Search and Shopping Advertising

- Paid Social and Social Commerce Marketing

- Marketplace Advertising and Digital Shelf Optimization

- Content and Influencer Marketing

- Email, SMS and Push Retention Marketing

- Affiliate and Partnership Marketing

- Other Service Types

- By Organization Size

- SMEs

- Large Enterprises

- By End-user Industry

- Retail and Consumer Goods

- Fashion and Apparel

- Beauty and Personal Care

- Consumer Electronics

- Grocery and Food and Beverage

- Home and Furniture

- Health and Wellness

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America remained the leading regional revenue base with 32.73% share in the ecommerce marketing services market in 2025, while Asia-Pacific is expected to post the fastest growth through 2031. The region's lead comes from deeper enterprise marketing budgets, broad adoption of retail media, and a more mature agency ecosystem that already supports integrated commerce execution. In the United States, creator advertising reached USD 37 billion in 2025, showing how quickly brand budgets are moving toward commerce-linked content and creator-led customer acquisition. Canada and Mexico are also adding demand, especially as mobile commerce growth increases the need for localized paid social, marketplace advertising, and performance measurement. The regulatory environment is also becoming increasingly important, as privacy rules and guidance on AI-led endorsements are shaping how agencies handle targeting, content disclosure, and consumer data use.

Asia-Pacific is the fastest-growing regional market, with a 15.29% CAGR in ecommerce marketing services, as ecommerce adoption remains strong and brands move quickly to newer forms of AI-assisted commerce execution. China stands out as the largest national market in the region and as a major testing ground for AI-led product discovery, social commerce, and marketplace-led customer acquisition. India, South Korea, and Australia are also adding new demand as domestic brands become more willing to outsource paid social, marketplace management, and conversion-focused campaign work. This is giving the ecommerce marketing services market in Asia-Pacific a distinct profile in which speed, platform fluency, and localization matter as much as pure media-buying scale.

Europe remains an important but more structurally constrained part of the ecommerce marketing services market because privacy regulation and platform oversight affect how agencies collect data and measure performance. The United Kingdom, Germany, and France continue to anchor regional demand through established agency ecosystems and strong retail infrastructure. South America is emerging as a meaningful growth pocket as mobile commerce and marketplace adoption improve, especially in Brazil, where local execution and digital shelf visibility matter more amid rising platform competition. The Middle East and Africa also offer long-term growth opportunities as countries such as the United Arab Emirates and Saudi Arabia continue to invest in digital commerce infrastructure, while Nigeria and South Africa build service demand around mobile-first shopping behavior.

- Accenture plc

- Omnicom Group Inc.

- Capgemini SE

- Cognizant Technology Solutions Corporation

- Deloitte Touche Tohmatsu Limited

- Infosys Limited

- International Business Machines Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Genpact Limited

- Adobe Inc.

- Merkle, Inc.

- Publicis Groupe S.A.

- WPP plc

- Stagwell Inc.

- Pattern, Inc.

- Cart.com, Inc.

- WebFX, Inc.

- SmartSites LLC

- NP Digital, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Performance Pressure as Ecommerce Competition Intensifies

- 4.2.2 AI-Driven Personalization and Creative Automation Improve Commerce ROI

- 4.2.3 Retail Media and Marketplace Advertising Budgets Keep Expanding

- 4.2.4 Omnichannel Shopping and Social Commerce Raise Demand for Integrated Execution

- 4.2.5 Agentic Commerce and AI Product Discovery Reward Structured Catalog Optimization

- 4.2.6 Cross-Border Marketplace Diversification Increases Need for Localized Digital Shelf Services

- 4.3 Market Restraints

- 4.3.1 Signal Loss from Privacy Changes and Cookie Deprecation Weakens Targeting

- 4.3.2 Customer Acquisition Cost Inflation Compresses Campaign Efficiency

- 4.3.3 Poor Product Data Readiness Limits Personalization and AI Scale-Up

- 4.3.4 Black-Box Platform Automation Reduces Control and Measurement Transparency

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Search Engine Optimization (SEO)

- 5.1.2 Paid Search and Shopping Advertising

- 5.1.3 Paid Social and Social Commerce Marketing

- 5.1.4 Marketplace Advertising and Digital Shelf Optimization

- 5.1.5 Content and Influencer Marketing

- 5.1.6 Email, SMS and Push Retention Marketing

- 5.1.7 Affiliate and Partnership Marketing

- 5.1.8 Other Service Types

- 5.2 By Organization Size

- 5.2.1 SMEs

- 5.2.2 Large Enterprises

- 5.3 By End-user Industry

- 5.3.1 Retail and Consumer Goods

- 5.3.2 Fashion and Apparel

- 5.3.3 Beauty and Personal Care

- 5.3.4 Consumer Electronics

- 5.3.5 Grocery and Food and Beverage

- 5.3.6 Home and Furniture

- 5.3.7 Health and Wellness

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Qatar

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Omnicom Group Inc.

- 6.4.3 Capgemini SE

- 6.4.4 Cognizant Technology Solutions Corporation

- 6.4.5 Deloitte Touche Tohmatsu Limited

- 6.4.6 Infosys Limited

- 6.4.7 International Business Machines Corporation

- 6.4.8 Tata Consultancy Services Limited

- 6.4.9 Wipro Limited

- 6.4.10 Genpact Limited

- 6.4.11 Adobe Inc.

- 6.4.12 Merkle, Inc.

- 6.4.13 Publicis Groupe S.A.

- 6.4.14 WPP plc

- 6.4.15 Stagwell Inc.

- 6.4.16 Pattern, Inc.

- 6.4.17 Cart.com, Inc.

- 6.4.18 WebFX, Inc.

- 6.4.19 SmartSites LLC

- 6.4.20 NP Digital, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment