|

시장보고서

상품코드

2072710

남미의 지붕재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

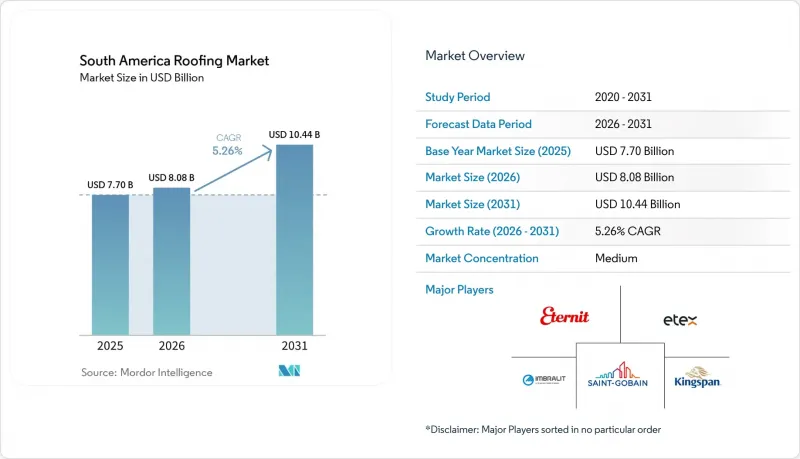

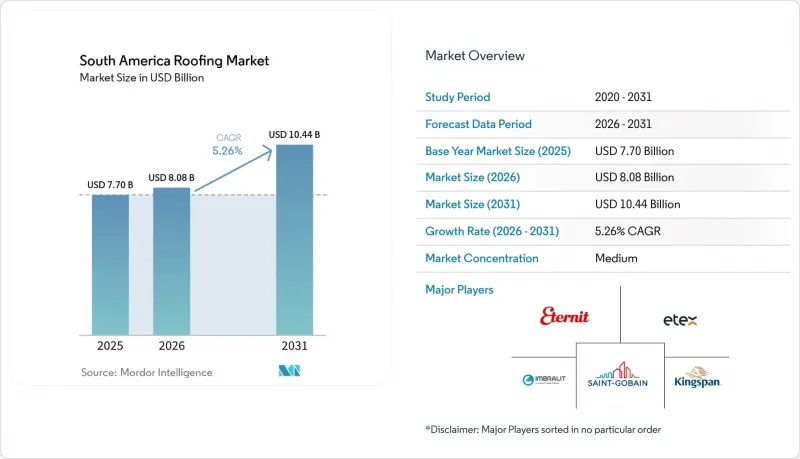

Mordor Intelligence에 의하면, 남미의 지붕재 시장 규모는 2025년에 77억 달러로 평가되었고, 2026년에 80억 8,000만 달러로 추정되고, 2031년까지 104억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.26%로 성장할 전망입니다.

본 보고서는 자재 유형별(아스팔트 슁글, 점토 및 콘크리트 기와, 금속 지붕재, 역청 및 개질 역청 막 등), 공사 유형별(신축, 지붕 재시공 및 개보수), 용도별(주택, 상업시설 등), 지역별(브라질, 아르헨티나, 콜롬비아, 칠레, 페루 및 기타 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 지붕 자재 시장 동향 및 인사이트

주택 보조금 지원 계획 사업 및 미착공 주택 건설 분

브라질의 'Minha Casa Minha Vida' 프로그램은 2025년 5월, 월총소득이 2,850BRL(502달러) 미만인 가구를 대상으로 13만 호의 신규 주택을 선정했습니다. 이번 발표에 따르면, 가구당 보조금 상한선을 14만 BRL(24,659.6 달러)에서 18만 500 BRL(31,793.3 달러)로 설정했습니다. 보조금이 지원되는 주택의 지붕 자재 수요 대부분은 일반적인 주택담보대출 이용 가능 여부에 영향을 받지 않기 때문에 이러한 제도를 통해 남미 지붕 자재 시장에 대한 수요 여지가 유지되고 있습니다. 콜롬비아와 페루의 이와 유사한 저소득층 주택 시장은 남미 지붕 자재 시장에서 보급형 주택용 지붕 자재 수요를 위한 보다 광범위한 지역 기반을 형성하고 있습니다. 이 시장의 제품 구성도 변화하고 있으며, 주택 규모가 축소되고 비용 상한선이 강화됨에 따라 기존의 점토 기와보다 섬유 시멘트나 평평한 콘크리트 지붕재가 선호되는 추세입니다. 이미 이 부문에 맞추어 생산 능력을 확대하고 있는 제조업체는 더 유리한 입장에 있습니다. 또한, Eternit이 1억 8,700만 BRL(3,290만 달러)을 투자한 카우카이아 공장은 2024년에 명목 생산 능력 기준 가동 첫 해를 마감하며, 공급 측면에서의 우위를 한층 더 공고히 했습니다.

노후된 기와 지붕 재고로 인한 재시공 수요

남미의 주택 건축물 대부분은 2000년 이전에 지어진 것으로, 당시에는 현재와 같이 지붕의 내구성과 단열 성능이 일관되게 중시되지 않았습니다. 1980년부터 2000년까지의 건축 주기 동안 설치된 점토 및 세라믹 지붕이 건축된 지 30년이 넘으면서, 브라질, 아르헨티나, 콜롬비아 전역에서 지붕 교체 수요가 더욱 체계적으로 증가하고 있습니다. 이는 남미의 지붕 자재 시장에 있어 중요한 의미를 지닙니다. 왜냐하면, 낡은 지붕을 교체하는 주택 소유자들 사이에서 세라믹 자재로 직접 교체하기보다는 섬유 시멘트, 코팅 금속, 혹은 경량 콘크리트를 선택하는 경향이 강해지고 있기 때문입니다. 이러한 고급화 추세는 이미 브라질에서 뚜렷하게 나타나고 있으며, Eternit의 2025년 1분기 섬유 시멘트 지붕 패널 판매량은 전년 동기 대비 15.1% 증가한 16만 7,600톤에 달했습니다. 이러한 성장의 한 가지 원인은 노후된 지붕 교체 작업이 활발히 진행되고 있는 브라질 북부 및 북동부 지역 수요 증가에 있습니다. 또한, 지붕 교체 공사에는 눈에 보이는 지붕 자재뿐만 아니라 지붕 밑받침재, 능선 판금, 개선된 고정 시스템 등이 포함되는 경우가 많기 때문에 이러한 교체 주기는 남미 지붕 자재 시장의 수익원을 확대하는 데에도 기여합니다.

높은 금리가 민간 건설 착공을 억제하고 있습니다.

2026년 초, 브라질의 세릭 금리는 15%로, 이는 2006년 이후 최고 수준이며, 민간 건설 활동에 명백한 제약 요인으로 작용하고 있습니다. 제출된 초안에 따르면, 2025년 중반까지의 신규 착공 건수는 6.2% 감소했으며, 브라질 전역에서 부진이 나타났습니다. 이것이 중산층을 대상으로 한 민간 프로젝트가 여전히 어려운 상황에 처해 있는 이유를 설명해 줍니다. 개발업체는 또한 셀릭 금리에 3%에서 3.5%를 가산한 자금 조달 비용은 물론, 건설 비용의 인플레이션을 따라가지 못하는 가계의 구매력 문제도 해결해야 합니다. 남미의 지붕 자재 시장에서 이는 민간 주택 분야의 수주 성사 속도가 둔화되고, 중산층 구매자를 대상으로 하는 개발업체의 경우 프로젝트 기간이 장기화됨을 의미합니다. 그렇긴 하지만, 2026년 3월 중앙은행이 발표한 '포커스' 조사에서는 연말 세릭 금리가 12.13%가 될 것이라는 예측이 제시되었으며, 기간 후반에 금리 인하가 이루어진다면 리스크가 다소 완화될 가능성이 시사되고 있습니다.

부문별 분석

2025년 기준으로, 점토 기와와 콘크리트 기와는 금액 기준 34.2%의 점유율을 차지했으며, 남미 지붕재 시장에서 가장 큰 소재 그룹을 이루고 있습니다. 이러한 주도적인 위상은 브라질, 아르헨티나, 콜롬비아에서 가장 확고하며, 이들 국가에서는 세라믹 지붕재가 여전히 현지 건축 관행과 저가형 주택 예산에 부합하고 있습니다. 금속 지붕 자재는 2026-2031년 연평균 성장률(CAGR) 6.4%를 기록할 전망이며, 가장 빠르게 성장하고 있는 소재 부문입니다. 이러한 성장률은 물류 창고, 냉장 창고, 광업 관련 시설 및 농업 관련 산업용 건물과 밀접한 관련이 있습니다. 남미의 점토 및 콘크리트 기와 지붕재 시장 규모는 여전히 대중 시장을 겨냥한 주택 수요에 힘입어 성장하고 있습니다. 동시에, 비주거용 프로젝트의 경우 성장의 주축이 코팅 및 단열 처리가 된 금속 지붕 시스템으로 이동하고 있습니다. 칠레와 콜롬비아의 단열 규제가 이러한 추세를 뒷받침하고 있으며, 산업 및 공공기관의 구매 담당자들은 프로젝트 설계 초기 단계부터 지붕 성능에 관한 보다 상세한 데이터를 요구하고 있습니다.

남미의 지붕재 시장에서 섬유시멘트는 여전히 합리적인 가격의 주택용 지붕재로 가장 많이 선택되는 제품이며, 브라질은 이 지역에서 가장 규모가 크고 확고하게 자리 잡은 섬유시멘트 지붕재 시장 중 하나입니다. 주요 제조업체 중 하나인 Eternit은 2024년 섬유시멘트 연간 판매량이 63만 3,242톤에 달했다고 보고했으며, 이는 브라질 내 이 부문의 규모와 시장 침투도가 얼마나 큰지를 여실히 보여주고 있습니다. 많은 상업용 평지붕에서는 아스팔트계 및 개질 아스팔트계 방수 시트가 여전히 주류를 이루고 있지만, 태양광 반사율과 이음매의 신뢰성을 중시하는 신규 프로젝트에서는 단층 시스템, 특히 열가소성 폴리올레핀(TPO)의 채택이 확대되고 있습니다. 에틸렌·프로파일렌·디엔 단량체(EPDM)는 고급 상업용 분야에서 여전히 중요한 위치를 차지하고 있는 반면, 폴리염화비닐(PVC)은 내화학성이 요구되는 환경에서 계속해서 중요한 역할을 수행하고 있습니다. 아스팔트 슁글과 목재 지붕재는 남미 지붕재 시장에서 비교적 낮은 점유율을 차지하고 있으며, 싱글은 도시 지역의 개보수라는 틈새 분야에 국한되어 있고, 목재 지붕재는 화재 위험에 대한 우려로 인해 더 광범위한 채택에 제약이 따르고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the south america roofing market size is projected to be USD 7.70 billion in 2025, USD 8.08 billion in 2026, and reach USD 10.44 billion by 2031, growing at a CAGR of 5.26% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, and More), & Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Roofing Market Trends and Insights

Subsidized Housing Pipelines and Housing Backlog

Brazil's Minha Casa Minha Vida program selected 130,000 new housing units in May 2025 for families with a monthly gross income below BRL 2,850 (USD 502). The same announcement set per-unit subsidy ceilings at BRL 140,000 (USD 24,659.6) to BRL 180,500 (USD 31,793.3). This structure keeps a demand corridor open for the South America roofing market because a large share of roofing demand in subsidized housing is not tied to standard mortgage availability. Comparable affordable housing channels in Colombia and Peru create a broader regional base for entry-level residential roofing demand within the South America roofing market. The mix in this channel is also shifting, with tighter unit sizes and cost ceilings favoring fiber-cement and flat concrete systems over traditional ceramic clay tiles. Manufacturers that already expanded capacity for this tier are in a stronger position, and Eternit's BRL 187 million (USD 32.9 million) Caucaia plant completed its first full year of nominal-capacity operation in 2024, reinforcing that supply-side advantage.

Replacement-Led Demand from Aging Tile-Heavy Roof Stock

A large share of South America's residential buildings were erected before 2000, when roofing durability and thermal performance were not consistently addressed as they are today. As clay and ceramic roofs installed during the 1980-2000 building cycle age past 30 years, replacement demand is becoming more systematic across Brazil, Argentina, and Colombia. This matters for the South America roofing market because homeowners replacing old roofs are increasingly choosing fiber cement, coated metal, or lightweight concrete instead of direct ceramic replacements. That trade-up pattern is already visible in Brazil, where Eternit's Q1 2025 fiber-cement roofing panel sales rose 15.1% year on year to 167,600 tonnes, with gains linked in part to North and Northeast Brazil, where older roofs are being replaced. The replacement cycle also expands the revenue pool for the South America roofing market because reroofing projects often include underlayments, ridge capping, and improved fastening systems rather than only the visible roof covering.

High Interest Rates Limiting Private Construction Starts

Brazil's Selic rate stood at 15% in early 2026, which was the highest level since 2006 and a clear constraint on private construction activity. The supplied draft noted that new construction starts declined 6.2% through mid-2025, with weakness seen across all Brazilian regions, which explains why mid-income private projects remain under pressure. Developers are also dealing with financing costs at Selic plus 3% to 3.5% and with household purchasing power that has not kept pace with construction cost inflation. In the South American roofing market, that means slower order conversion in private housing and longer project timelines for developers targeting middle-income buyers. Even so, the Central Bank's Focus survey in March 2026 pointed to a year-end Selic rate of 12.13%, suggesting some easing risk if rate cuts materialize later in the period.

Other drivers and restraints analyzed in the detailed report include:

- Metal and Insulated Roofing Adoption in Industrial Buildings

- Tightening Roof Thermal Efficiency Standards

- Input-Cost Volatility in Steel, Membranes, and Asphaltic Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clay & concrete tiles held a 34.2% value share in 2025, making them the largest material group in the South American roofing market. Their leading position remains strongest in Brazil, Argentina, and Colombia, where ceramic roofing continues to align with local building practices and entry-level residential budgets. Metal roofing is the fastest-growing material segment with a 6.4% CAGR through 2026-2031, and that rate is closely tied to logistics warehouses, cold storage, mining-support assets, and agro-industrial buildings. The South America roofing market size for clay & concrete tiles remained anchored by mass-market residential demand. At the same time, the growth premium shifted toward coated and insulated metal systems in non-residential projects. Thermal regulations in Chile and Colombia are reinforcing this move, as industrial and institutional buyers now need better-documented roof performance from the outset of project design.

Fiber cement remains the main affordable residential roofing alternative in the South America roofing market, with Brazil representing one of the largest and most established fiber-cement roofing markets in the region. As one of the leading manufacturers, Eternit reported full-year fiber-cement sales volume of 633,242 tonnes in 2024, highlighting the significant scale and depth of the segment in Brazil. Bituminous and modified bitumen membranes continue to dominate many flat commercial roofs, while single-ply systems, especially Thermoplastic Polyolefin (TPO), are gaining adoption in newer projects that prioritize solar reflectivity and seam reliability. Ethylene Propylene Diene Monomer (EPDM) remains relevant in premium commercial applications, while Polyvinyl Chloride (PVC) continues to be important in environments where chemical resistance is required. Asphalt shingles and wood roofing keep smaller positions in the South America roofing market, with shingles tied to urban renovation niches and wood limited by fire-risk concerns in broader adoption.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Eternit

- Saint-Gobain Brasilit

- Imbralit

- Etex

- Kingspan

- Ternium

- Cintac

- Tupemesa

- Ajover

- Sika

- Viapol

- Danica

- Multilit

- Aceros Arequipa

- Acesco Ecuador

- Onduline

- Hunter Douglas Architectural

- Rooftec Telhas Metalicas

- Thermo-Iso

- Brastetto

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidized Housing Pipelines and Housing Backlog

- 4.2.2 Replacement Demand from Aging Tile-Heavy Roof Stock

- 4.2.3 Metal and Insulated Roofing Adoption in Industrial Buildings

- 4.2.4 Tightening Roof Thermal Efficiency Standards

- 4.2.5 Climate-Resilience Reroofing After Extreme Weather Events

- 4.2.6 Cool-Roof Retrofit Economics in Hot-Climate Cities

- 4.3 Market Restraints

- 4.3.1 High Interest Rates Limiting Private Construction Starts

- 4.3.2 Input-Cost Volatility in Steel, Membranes, and Asphaltic Products

- 4.3.3 Installer Capability Gaps for Advanced Roofing Systems

- 4.3.4 Informal Self-Build Channel Slows Premium-System Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Eternit

- 6.4.2 Saint-Gobain Brasilit

- 6.4.3 Imbralit

- 6.4.4 Etex

- 6.4.5 Kingspan

- 6.4.6 Ternium

- 6.4.7 Cintac

- 6.4.8 Tupemesa

- 6.4.9 Ajover

- 6.4.10 Sika

- 6.4.11 Viapol

- 6.4.12 Danica

- 6.4.13 Multilit

- 6.4.14 Aceros Arequipa

- 6.4.15 Acesco Ecuador

- 6.4.16 Onduline

- 6.4.17 Hunter Douglas Architectural

- 6.4.18 Rooftec Telhas Metalicas

- 6.4.19 Thermo-Iso

- 6.4.20 Brastetto

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment