|

시장보고서

상품코드

2072711

아시아태평양의 지붕재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

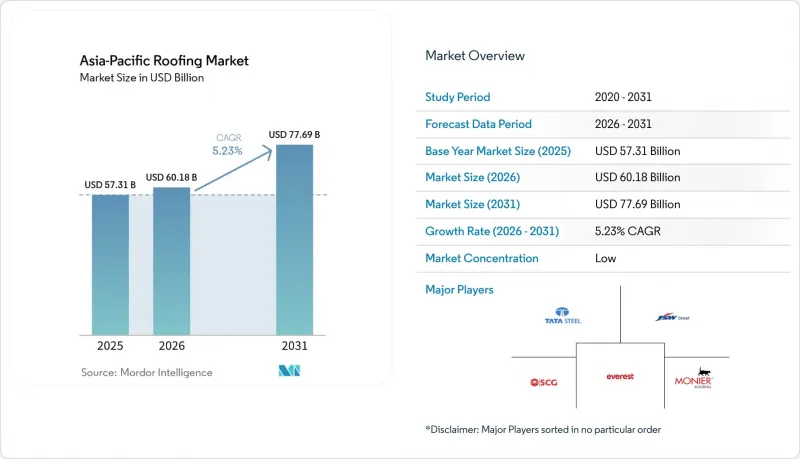

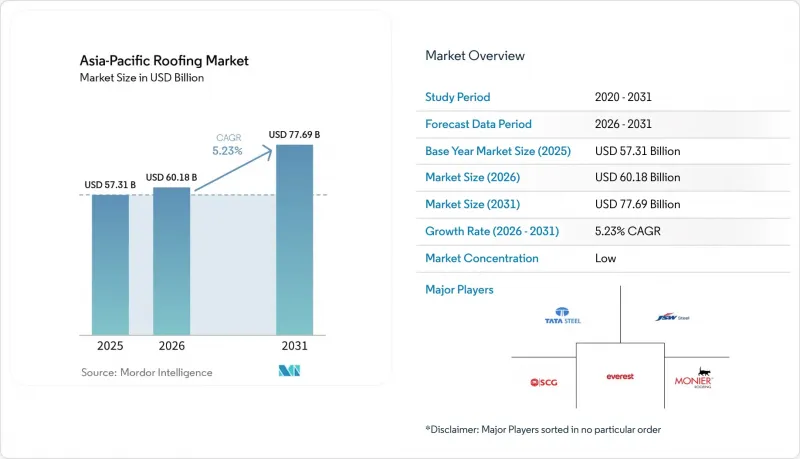

Mordor Intelligence에 의하면, 아시아태평양의 지붕재 시장 규모는 2025년에 573억 1,000만 달러로 평가되었고, 2026년에 601억 8,000만 달러로 추정되고, 2031년까지 776억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.23%로 성장할 전망입니다.

본 보고서는 자재 유형별(아스팔트 슁글, 점토 및 콘크리트 기와, 금속 지붕, 역청 및 개질 역청 막 등), 시공 유형별(신축, 지붕 재시공 및 교체), 용도별(주택, 상업시설 등), 지역별(중국, 일본, 인도, 호주, 한국, 아시아태평양의 기타 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 지붕재 시장 동향 및 분석

건설 및 인프라 중심의 지붕재 수요

교통 회랑, 물류 단지, 산업 클러스터, 도시 주택은 모두 대규모의 지속적인 지붕재 조달이 필요하기 때문에 건설 활동은 아시아태평양 지붕재 시장의 주요 수요 동력으로 계속 작용하고 있습니다. 인도 및 동남아시아에서는 신속한 설치가 가능한 금속 시스템 및 기타 확장성이 뛰어난 지붕재 형태를 선호하는 창고 네트워크, 공장용 셸, 공공 인프라 사업의 확장을 통해 이러한 추세가 지속적으로 뒷받침되고 있습니다. 베트남, 태국, 인도네시아의 산업단지도 이러한 수요를 뒷받침하고 있습니다. 이는 프리엔지니어링 구조물의 경우 일반적으로 프로젝트 주기의 초기 단계에서 지붕재 선정이 표준화되기 때문에 공급업체에 대한 가시성이 향상되고, 이는 재구매로 이어지기 때문입니다. 주택 중심 수요도 이를 더욱 뒷받침하고 있습니다. 대규모 주택 프로젝트에서는 단발성 주문이 아니라, 반복적으로 구매되는 제품군에 구매가 집중되기 때문입니다. 이에 따라 아시아태평양의 지붕재 시장은 경기 순환에 좌우되는 착공 동향뿐만 아니라, 초기 비용의 경제성은 물론 규제 준수, 시공 속도, 수명 주기 전반에 걸친 내구성이 중시되는 보다 광범위한 조달 시스템과도 밀접하게 연결되어 있습니다.

지붕 교체 및 보수 수요의 확대

일본, 호주, 한국 등 성숙한 경제권에서는 수십년전에 준공된 건축물의 대부분이 재건축되었기 때문에 지붕 교체 및 개보수는 아시아태평양의 지붕재 시장에서 여전히 중심적인 위치를 차지하고 있습니다. 이러한 업데이트 주기에서는 기존과 동일한 소재가 선정되는 경우가 거의 없습니다. 이는 소유주나 시공업체가 단열 성능 향상, 구조 하중 경감, 혹은 내구 연한 연장을 목적으로 지붕 교체 공사를 활용하는 사례가 늘어나고 있기 때문입니다. 이러한 추세는 특히 단열 및 방수 공사가 단일 프로젝트에 포함될 경우, 고급 금속 시스템, 코팅 제품 및 방수 시트 수요를 뒷받침하고 있습니다. 호주에서는 주요 제조업체들공급 확대가, 현재 경기 사이클 전반에 걸쳐 신축 및 주택 재건축 수요가 계속해서 활발할 것이라는 확신을 반영하고 있습니다. 따라서 아시아태평양의 지붕재 시장은 리모델링 공사의 혜택을 받고 있습니다. 이는 재건축 공사가 신축 공사에 비해 수요 변동이 적고, 프로젝트당 사양 가치가 높은 경향이 있기 때문입니다.

원자재 가격 변동

원자재 가격 변동은 아시아태평양의 지붕재 시장에 있어 여전히 단기적인 제약 요인으로 작용하고 있습니다. 철강, 알루미늄, 역청의 원가는 공장의 이익률과 입찰 규율 모두에 영향을 미치기 때문입니다. 수입에 의존하는 시장은 현지에서의 수직 통합이 제한적이기 때문에 원자재 비용의 급격한 변동을 흡수하기 어렵고, 더 큰 영향을 받기 쉬운 상황에 놓여 있습니다. 더 큰 문제는 프로젝트의 완전한 중단이라기보다는 대부분의 경우 공사 기간의 지연입니다. 지붕 공사 패키지의 가격이 불투명하기 때문에 시공업체나 개발업체는 입찰 가격이 안정될 때까지 착공을 연기하는 경우가 있기 때문입니다. 비투멘 관련 제품도 비슷한 문제에 직면해 있습니다. 이는 최종 수요가 견조하더라도 정유시설의 배분이나 원유 가격의 변동 주기에 따라 공급이 부족해질 가능성이 있기 때문입니다. 이러한 압박이 아시아태평양의 지붕재 시장 수요를 완전히 사라지게 하지는 않겠지만, 분기별 판매량을 감소시키고 제품 구성이 조달 시기의 영향을 더 쉽게 받게 할 가능성이 있습니다.

부문별 분석

2025년, 아스팔트 슁글은 가격에 민감한 주택 시장에서 비용 경쟁력과 시공의 간편함을 바탕으로 아시아태평양 지붕재 시장에서 31.8%의 점유율을 차지했습니다. 구매 결정에 있어 초기 비용의 저렴함이 단열 성능이나 긴 수명이라는 요건보다 여전히 우선시되는 지역에서는 그 위상이 여전히 가장 확고합니다. 한편, 에너지 효율 및 반사율에 관한 기준이 강화됨에 따라 명확한 중기적 한계가 나타나고 있습니다. 이는 기존의 어두운 색상 아스팔트 제품이, 확립된 쿨루프 측정 체계 하에서는 성능이 떨어지기 때문입니다. 점토 기와와 콘크리트 기와는 건축의 전통, 가파른 경사의 지붕 설계, 그리고 긴 수명이 여전히 중요하게 여겨지는 국가들에서 계속해서 큰 수요를 유지하고 있습니다. 금속 지붕 역시 아시아태평양의 지붕재 시장에서 주요 판매량 부문을 차지하고 있으며, 산업용 건물과 고사양 리모델링 프로젝트 모두에 활용되고 있습니다. 제조업체의 발표 내용도 이러한 역할을 뒷받침하고 있으며, JSW Steel사는 2024-25 회계연도에 갈바륨 및 아연 도금 강판의 판매량이 전년 대비 14% 증가했다고 보고했습니다.

열가소성 폴리올레핀(TPO), 에틸렌·프로파일렌·디엔 단량체(EPDM), 폴리염화비닐(PVC)을 포함한 단층 필름은 2031년까지 연평균 성장률(CAGR) 6.8%를 나타낼 것으로 예측되며, 해당 지역에서 가장 빠르게 성장하는 소재 그룹이 될 전망입니다. 이 부문에서 아시아태평양의 지붕재 시장 규모는 저경사 시스템, 시공 신속화, 그리고 높은 단열 성능이 점점 더 요구되는 상업 및 산업용 건축물에 의해 주도되고 있습니다. TPO는 소유주가 이음매의 기밀성, 시공 속도, 일관된 디테일 설계를 통해 광대한 지붕 면적을 관리할 수 있다는 점을 중시하기 때문에 데이터센터나 물류 시설 프로젝트에서 특히 주목받고 있습니다. EPDM은 외관의 아름다움보다는 내후성과 방수 성능이 중시되는 이미 성숙된 보수 공사 현장에 여전히 적합합니다. 아스팔트계 시트는 인프라 및 방수성이 중요한 용도에서 계속해서 사용되고 있지만, 목재의 경우 일부 선진국 시장에서 방화성 및 지속가능성에 대한 우려로 인해 그 사용이 제한되고 있습니다. '기타'가 카테고리에는 태양광 발전 기능을 통합한 지붕재, 그린 루프, 그리고 틈새 시장을 겨냥한 고성능 시스템 등이 포함됩니다. 이들은 아직 규모는 작지만, 도시 지역의 프로젝트에서 그 존재감을 높여가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the asia-Pacific roofing market size is projected to be USD 57.31 billion in 2025, USD 60.18 billion in 2026, and reach USD 77.69 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction and Reroofing and Replacement), Application (Residential, Commercial, and More), and Geography (China, Japan, India, Australia, South Korea, and Rest of APAC). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Roofing Market Trends and Insights

Construction and Infrastructure-Led Roofing Demand

Construction activity remains a core demand engine for the Asia-Pacific roofing market, as transport corridors, logistics parks, industrial clusters, and urban housing all require large, recurring roof procurement volumes. India and Southeast Asia continue to support this pattern through expanding warehouse networks, factory shells, and public infrastructure programs that favor fast-installing metal systems and other scalable roofing formats. Industrial parks in Vietnam, Thailand, and Indonesia also strengthen this demand because pre-engineered structures typically standardize roof selection early in the project cycle, which improves supplier visibility and repeat business. Housing-led demand adds another layer of support because large residential programs concentrate purchases into repeatable product categories instead of fragmented one-off orders. This keeps the Asia-Pacific roofing market tied not only to cyclical building starts, but also to a broader procurement system in which compliance, installation speed, and lifecycle durability matter as much as first-cost economics.

Reroofing and Renovation Demand Expansion

Reroofing and renovation remain central to the Asia-Pacific roofing market because mature economies such as Japan, Australia, and South Korea are replacing large portions of building stock that entered service decades ago. These replacement cycles rarely result in like-for-like material selection because owners and contractors increasingly use reroofing projects to improve thermal performance, reduce structural load, or extend service life. That pattern supports premium metal systems, coated products, and membranes, especially when insulation and waterproofing upgrades are bundled into a single project. In Australia, supply additions by major producers reflect confidence that both new and replacement housing demand will remain active through the current cycle. The Asia-Pacific roofing market, therefore, benefits from renovation activity, as replacement work tends to be less volatile than new construction and often carries a higher specification value per project.

Raw-Material Price Volatility

Raw-material volatility remains a near-term constraint for the Asia-Pacific roofing market, as steel, aluminum, and bitumen costs affect both factory margins and tendering discipline. Import-dependent markets are more exposed because sudden swings in feedstock costs are harder to absorb when local backward integration is limited. The bigger issue is often project delay rather than outright cancellation, since uncertain roof package pricing can cause contractors and developers to postpone starts until bids stabilize. Bitumen-linked products face a similar problem because refinery allocation and oil price cycles can tighten supply even when end demand remains intact. This pressure does not eliminate demand from the Asia-Pacific roofing market, but it can compress quarterly volumes and make the product mix more sensitive to procurement timing.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Energy-Efficient and Cool-Roof Systems

- Weather Resilience and Durable-Roof Adoption

- Cross-Country Regulatory Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asphalt shingles held 31.8% of the Asia-Pacific roofing market share in 2025, supported by their cost competitiveness and straightforward installation across price-sensitive residential markets. Their position remains strongest where upfront affordability still outweighs thermal performance or long-life requirements in the purchase decision. At the same time, rising energy and reflectance standards create a clear medium-term limit, as conventional dark asphalt products perform worse under established cool-roof measurement frameworks. Clay and concrete tiles continue to hold meaningful demand in countries where architectural tradition, steep-slope design, and long service life remain important. Metal roofing also remains a major volume category in the Asia-Pacific roofing market, serving both industrial buildings and higher-specification renovation projects. Producer commentary supports that role, with JSW Steel reporting 14% year-on-year growth in galvalume and galvanized sales in FY 2024-25.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are forecast to grow at a 6.8% CAGR through 2031, making them the fastest-rising material group in the region. The Asia-Pacific roofing market size for this segment is being lifted by commercial and industrial buildings where low-slope systems, faster installation, and higher thermal performance are increasingly specified. TPO is gaining particular traction in data-center and logistics projects because owners value seam integrity, installation speed, and the ability to manage large roof areas with consistent detailing. EPDM still fits mature renovation settings where weather exposure and waterproofing resilience matter more than aesthetic finish. Bituminous membranes continue to serve infrastructure and waterproofing-heavy applications, while wood remains limited by fire and sustainability concerns in several developed markets. The others category captures early adoption of solar-integrated roofing, green roof assemblies, and niche high-performance systems that are still small in volume but increasingly visible in urban projects.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Tata Steel Colors

- JSW Steel Ltd

- Everest Industries Limited

- The Siam Cement Public Company Limited

- CSR Monier Roofing

- Bristile Roofing

- NS BlueScope Lysaght

- BlueScope Steel Pacific

- Dimond Roofing

- Kingspan Group

- Sika AG

- Oriental Yuhong

- KMEW Co., Ltd.

- Gerard Roofs

- Puyat Steel Corporation

- Tatalogam Lestari

- Kanmuri Roof

- Hoa Sen Home

- Nippon Steel (Thailand) Co., Ltd.

- Onduline

- LCP Building Products Pte Ltd

- Taiyo Kogyo Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction and Infrastructure-Led Roofing Demand

- 4.2.2 Reroofing and Renovation Demand Expansion

- 4.2.3 Shift Toward Energy-Efficient and Cool-Roof Systems

- 4.2.4 Weather Resilience and Durable-Roof Adoption

- 4.2.5 Subnational Cool-Roof Mandates Accelerating Premium Roof Specifications

- 4.2.6 Data-Center Buildout Creating Demand for High-Performance Roofing Systems

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Cross-Country Regulatory Fragmentation

- 4.3.3 Roofing Labor and Installer Shortages

- 4.3.4 Cool-Roof Performance Degradation in Polluted and Humid Zones

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tata Steel Colors

- 6.4.2 JSW Steel Ltd

- 6.4.3 Everest Industries Limited

- 6.4.4 The Siam Cement Public Company Limited

- 6.4.5 CSR Monier Roofing

- 6.4.6 Bristile Roofing

- 6.4.7 NS BlueScope Lysaght

- 6.4.8 BlueScope Steel Pacific

- 6.4.9 Dimond Roofing

- 6.4.10 Kingspan Group

- 6.4.11 Sika AG

- 6.4.12 Oriental Yuhong

- 6.4.13 KMEW Co., Ltd.

- 6.4.14 Gerard Roofs

- 6.4.15 Puyat Steel Corporation

- 6.4.16 Tatalogam Lestari

- 6.4.17 Kanmuri Roof

- 6.4.18 Hoa Sen Home

- 6.4.19 Nippon Steel (Thailand) Co., Ltd.

- 6.4.20 Onduline

- 6.4.21 LCP Building Products Pte Ltd

- 6.4.22 Taiyo Kogyo Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment