|

시장보고서

상품코드

2072738

세포 및 유전자 치료 분야 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Cell and Gene Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

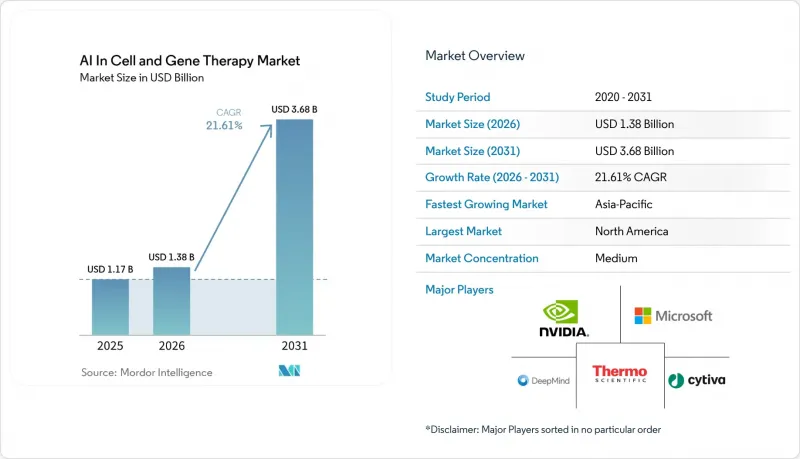

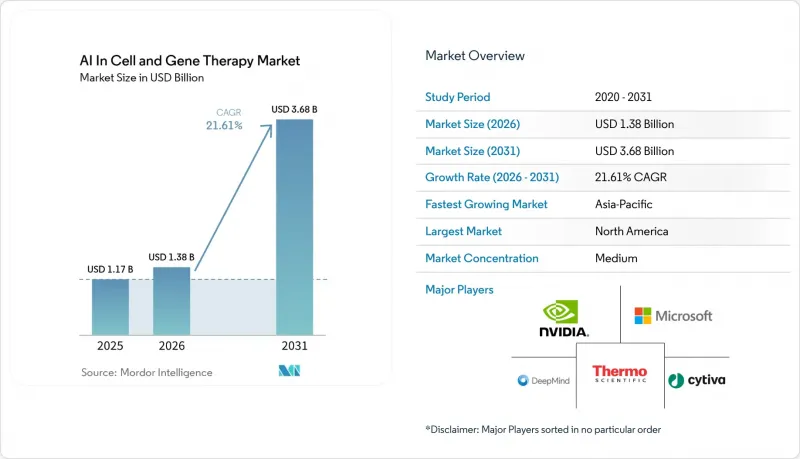

Mordor Intelligence에 의하면, 세포 및 유전자 치료 분야 AI 시장은 2025년 11억 7,000만 달러로 평가되었고, 2026년에는 13억 8,000만 달러로 추정되고, 2026-2031년 CAGR 21.61%로 성장을 지속할 전망이며, 2031년에는 36억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어 및 AI 플랫폼, 서비스), 도입 형태별(클라우드 기반, 기타), 치료법 유형별(세포 치료, 유전자 치료), 용도별(신약 개발 및 전임상, 기타), 최종 사용자별(제약 및 바이오기술 기업, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 세포 및 유전자 치료 분야 AI 동향 및 인사이트

고속 처리 가능한 유전자 편집 데이터 세트의 급격한 증가로 인해, AI를 활용한 분석이 요구되고 있습니다.

세포 및 유전자 치료 분야 AI 시장은 현재 과학적 과제이자 인프라적 과제로 대두되고 있는 데이터 양의 급증이라는 흐름의 혜택을 누리고 있습니다. 일루미나사는 2026년 1월, AI를 활용한 신약 개발 워크플로우를 지원하기 위해 구축된, 계획 중인 50억 세포 프로그램의 첫 번째 단계로, 'Billion Cell Atlas'를 발표했습니다. 시퀀싱 처리량이 향상됨에 따라, 운영상의 병목 현상은 데이터 생성에서 주석 품질로 점차 이동하고 있습니다. 이는 모델이 진정한 치료 신호를 배경의 생물학적 잡음과 구별하기 위해 여전히 임상적으로 의미 있는 라벨이 필요하기 때문입니다. 리커션사는 2026년, 로슈 및 제넨테크와 공동 개발한 자사의 바이오로지 맵이 1조 개 이상의 iPS 세포 유래 신경세포로 구성되어 있다고 발표했습니다. 이는 엄선된 멀티모달 데이터가 일회용 연구용 입력 데이터가 아니라, 지속적인 상업적 자산이 될 수 있음을 보여줍니다. 따라서 세포 및 유전자 치료 시장의 AI 분야에서는 우수한 모델 아키텍처를 공개하는 기업뿐만 아니라, 독자적인 세포 데이터셋을 보유한 기업에 대한 평가도 높아지고 있습니다. 장기적으로는 가장 광범위하고 고품질의 라이브러리를 보유한 데이터 소유자가 세포 및 유전자 치료 분야 AI 시장에서 가장 강력한 가격 결정권을 행사하게 될 것입니다.

CGT 개발 주기를 단축하기 위해 대형 제약사와 AI 스타트업간의 제휴가 증가하고 있습니다.

세포 및 유전자 치료 분야 AI 시장은 대형 제약사들이 AI를 핵심 개발 인프라로 삼고 있는 자금 조달 환경의 혜택도 누리고 있습니다. NVIDIA와 일라이 릴리는 2026년 1월, 단백질 확산 모델, 유전체학 기반 모델, 제조 디지털 트윈 개발을 위해 향후 5년간 최대 10억 달러를 투자하는 공동 혁신 AI 연구소 설립을 발표했습니다. 이어 로슈는 2026년 3월, 미국 및 유럽 거점에 3,500대 이상의 Blackwell GPU를 도입하며 AI 팩토리 전략을 확대했습니다. 이는 대형 제약 기업들이 퍼블릭 클라우드에 대한 접근에만 의존하지 않고, 시간적 제약이 엄격한 규제 대상 워크플로우를 위해 독자적인 컴퓨팅 역량을 구축해 나가고 있음을 보여줍니다. 이러한 제휴는 개발 주기를 단축시키는 한편, 스폰서의 워크플로우에 통합된 AI 스타트업은 나중에 대체하기 어려워지기 때문에 경쟁 양상도 변화시키고 있습니다. 실제로, 세포 및 유전자 치료 분야 AI 시장은 모델, 데이터 파이프라인, 과학적 판단이 특정 플랫폼에 묶이게 되면 전환 비용이 높아지는 기업 소프트웨어와 점점 더 닮아가고 있습니다. 따라서 세포 및 유전자 치료 분야 AI 시장 내 상업적 관계는 일반적인 프로젝트 기반의 아웃소싱보다 지속성이 더 높습니다.

분산되어 있고 독자적인 사양을 가진 임상 데이터셋이 모델의 일반화 가능성을 제한합니다.

세포 및 유전자 치료 분야 AI 시장은 기증자, 질환 상태, 제조 거점 간에 원활하게 공유되지 않는 사일로화된 데이터 세트라는 심각한 제약에 여전히 직면해 있습니다. 2026년 3월 『Pharmaceutics』지에 실린 리뷰에 따르면, 세포 및 유전자 치료 분야 AI 모델이 후원사 고유의 제한된 데이터 환경 내에서 학습될 경우, 일반화에 어려움을 겪는 경우가 많다고 설명되어 있습니다. 이는 학습 데이터가 파편화되어 있고 독자적인 사양으로 남아 있는 한, 아키텍처의 발전만으로는 성능 격차를 해소할 수 없음을 의미합니다. 또한, 다양한 다기관·다후원자 제조 및 임상 데이터 세트를 하나의 실용적인 프레임워크로 통합할 수 있는 조직에는 강력한 선점 우위가 생깁니다. 연방 학습(Federated Learning)은 데이터 공유의 장벽을 일부 완화할 수 있지만, 각 기관이 서로 다른 거버넌스, 개인정보 보호 및 운영 기준에 따라 운영되는 경우가 많기 때문에 실행 속도를 저하시키는 요인이 되기도 합니다. 세포 및 유전자 치료 분야 AI 시장에서 보다 강력한 상호운용성 규칙이 확립되기 전까지는 실험실에서의 모델 성능이 상용 프로그램에서 일관되게 구현할 수 있는 성능을 계속해서 능가할 것입니다.

부문별 분석

2025년, 세포 및 유전자 치료 분야 AI 시장 점유율 중 소프트웨어 및 AI 플랫폼이 48.24%를 차지하며 가장 큰 비중을 차지했습니다. 이러한 위상은 모델 개발, 워크플로우 오케스트레이션, 예측 분석이 주요 산출물로 간주되는 반면, 기반이 되는 데이터 스토리지와 범용 컴퓨팅이 점점 더 표준화되고 있다는 점에서 구매자들이 현재 가장 큰 가치를 두고 있는 영역을 반영하고 있습니다. 따라서 세포 및 유전자 치료 분야 AI 시장에서는 단순한 기본 구현 작업보다 실험, 데이터, 의사결정 지원을 연결하는 제어 계층에 더 큰 가치가 부여되고 있습니다. 2026년 5월, Benchling사가 Baseten사와 제휴하여 생명공학 연구 개발 워크플로우에 GPU 규모의 추론 기능을 도입한 사례는 소프트웨어 벤더들이 이전에는 별도의 인프라 제공업체가 담당하던 기능을 점차 흡수하고 있음을 보여줍니다. 이 소프트웨어 부문은 2031년까지 연평균 성장률(CAGR) 22.17%로 확대될 것으로 예상되며, 이는 세포 및 유전자 치료 분야 AI 시장에서 가장 큰 비중을 차지하는 요소가 가장 빠르게 성장하는 분야 중 하나임을 의미합니다.

서비스는 여전히 수익의 상당 부분을 차지하고 있지만, 그 역할은 보다 복잡한 도입과 관련된 구현 지원, 검증 및 규제 관련 자문 업무로 점차 전환되고 있습니다. 표준적인 전임상 업무는 점점 더 자동화되고 있으며, 이로 인해 노동 집약도가 낮아지면서 소프트웨어 주도형 플랫폼에 비해 서비스의 상대적 성장세가 둔화되고 있습니다. 또한, 세포 및 유전자 치료 분야 AI 업계에서는 빈번한 모델 업데이트나 지속적인 워크플로우 통합이 요구되는 경우, 구매자들은 일회성 서비스 계약보다는 반복적으로 이용할 수 있는 플랫폼 구독을 선호하는 경향이 있습니다. 시판 후 조사나 GMP 품질 관리 기능은 신약 개발 단계에 비해 소프트웨어 지출에서 차지하는 비중이 여전히 작지만, 제품 수명 주기에 대한 기대치가 엄격해짐에 따라 그 균형은 변화할 가능성이 있습니다. 세포 및 유전자 치료 분야 AI 시장 전체를 살펴보면, 구성 요소의 조합부터 실험 맥락, 모델 출력, 의사결정 이력에 이르기까지 모든 요소를 단일 운영 환경에 통합할 수 있는 플랫폼을 중심으로 지속적인 가치가 구축되고 있음을 시사하고 있습니다.

클라우드 기반 도입은 2025년에 53.26%의 점유율을 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 22.38%로 성장할 것으로 전망되어, 세포 및 유전자 치료 분야 AI 시장에서 가장 빠르게 성장하고 있는 도입 형태로 자리매김하고 있습니다. 이러한 경향은 분산형 GPU 인프라에 대한 접근을 로컬 하드웨어 설치나 검증보다 더 신속하게 확대할 수 있다는 신약 개발 및 전임상 팀의 실질적인 요구를 반영하고 있습니다. 또한, 클라우드 도입은 스크리닝 주기에 따라 워크로드가 증감하는 경우에도 적합합니다. 조직은 현장에 모든 자본 부담을 지우지 않고도 연산 능력을 확장할 수 있기 때문입니다. 그런 의미에서 세포 및 유전자 치료 분야 AI 시장에서는 클라우드가 단순한 호스팅 옵션이라기보다는 운영 모델로 활용되고 있습니다. 이로 인해, 고도의 훈련 및 추론 능력에 필요한 자금 조달에 어려움을 겪던 소규모 개발자들에게도 접근성이 확대되고 있습니다.

그렇긴 하지만, 규제 대상인 제조 환경에서는 데이터 저장 위치, 감사 추적, 지연, 시스템 검증에 대한 보다 엄격한 관리가 여전히 요구되고 있기 때문에 도입 현황에는 편차가 나타나고 있습니다. 로슈가 2026년 3월에 예정하고 있는 AI 팩토리 확장 계획(미국 및 유럽 거점에 대규모 GPU 클러스터를 구축하는 것)은 주요 제조업체들이 여전히 특정 규제 대상 워크플로우에서 사설 인프라를 전략적 요건으로 간주하고 있음을 분명히 보여줍니다. 따라서 클라우드 시장이 전반적으로 급속히 성장하고 있는 반면, 세포 및 유전자 치료 분야 AI 시장에서는 온프레미스, 엣지, 혹은 하이브리드 모델이 여전히 중요한 위치를 차지하고 있습니다. 엣지 및 하이브리드 아키텍처는 현재로서는 수익 규모가 작지만, 로컬 거버넌스와 외부 컴퓨팅 리소스에 대한 선택적 접근을 결합하고 있기 때문에 향후 상업적 생산 분야에서 성장할 수 있는 유리한 입지에 있습니다. 앞으로 세포 및 유전자 치료 분야 AI 시장은 기능별로 세분화될 가능성이 높으며, 초기 단계의 실험에서는 클라우드가 주도적인 역할을 수행하고, GMP 감독이 가장 엄격한 분야에서는 하이브리드 방식의 도입이 입지를 다져나갈 것입니다.

지역별 분석

2025년, 북미는 세포 및 유전자 치료 분야 AI 시장 점유율의 51.62%를 차지했으며, 계속해서 주요 지역 클러스터로서의 위상을 유지했습니다. 이 지역은 후원 기업의 높은 집중도, 탄탄한 벤처 지원, 그리고 AI 관련 규제 대상 소프트웨어 환경에서의 라이프사이클 관리 및 위험 기반 검증을 위한 FDA의 적극적인 노력 등의 혜택을 누리고 있습니다. 대형 제약사의 본사, 학술적인 세포 치료 연구 거점, 그리고 첨단 컴퓨팅 인프라가 서로 인접해 위치해 있기 때문에 미국은 여전히 핵심적인 원동력으로 자리 잡고 있습니다. NVIDIA는 2026년, LillyPod가 DGX B300 시스템을 탑재한 세계 최초의 NVIDIA DGX SuperPOD가 되었다고 발표했으며, 이를 통해 북미 개발자들은 대규모 모델 개발 및 배포에 있어 상당한 연산상의 이점을 얻게 되었습니다.

유럽은 강력한 바이오프로세스 엔지니어링 역량과 데이터 규정 준수에 대한 세심한 배려를 바탕으로, 세포 및 유전자 치료 분야 AI 시장에서 확고한 입지를 유지하고 있습니다. 독일은 장비, 공정 엔지니어링, 제조 노하우가 치료법 개발과 밀접하게 연결되어 있다는 점에서 두드러집니다. 살토리아스사는 2025년, 신약 개발 및 제조 분야의 AI 발전을 위해 NVIDIA와 협력하고 있다고 발표했습니다. 이는 계측 기기, 데이터 수집, 공정 관련 지식을 결합하는 유럽의 강점과 부합하는 것입니다. 영국, 프랑스, 이탈리아, 스페인 및 기타 유럽 국가들은 학술 기관에서 탄생한 AI 생명공학 기업, 전문적인 임상 프로그램, EU 차원의 지원 체계를 통해 지속적으로 부가가치를 창출하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.62%로 확대될 것으로 예측되며, 세포 및 유전자 치료 분야 AI 시장에서 가장 두드러진 성장을 보이는 지역 부문으로 자리매김하고 있습니다. 중국, 일본, 한국이 주요 성장 거점으로 부상하고 있으며, 강력한 정책 지원, 임상시험 활동의 활성화, 그리고 지역 개발 생태계의 확대가 진행되고 있습니다. 일본은 히타치가 주도하는 고처리량 세포 설계 플랫폼 개발을 비롯해, 제조 최적화 및 세포 재프로그래밍과 관련된 기업 및 학계의 노력을 통해 기여하고 있습니다. 한국과 호주는 CRO의 성장과 임상시험 활동을 통해 지역 시장 규모를 확대하고 있으며, 이에 따라 세포 및 유전자 치료 분야 AI 시장 사업 기반이 각국의 최대 기업들을 넘어 확장되고 있습니다. 중동(특히 GCC 국가들과 남아프리카) 및 남미(브라질과 아르헨티나 포함)는 여전히 소규모 시장이지만, 정부가 지원하는 선별된 유전체 의료 및 첨단 치료 프로그램을 통해 그 중요성이 점차 커지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the AI in cell and gene therapy market is expected to grow from USD 1.17 billion in 2025 to USD 1.38 billion in 2026 and is forecasted to reach USD 3.68 billion by 2031 at 21.61% CAGR over 2026-2031.

This report is Segmented by Component (Software/AI Platforms, and Services), Deployment (Cloud-Based, and Others), Therapy Type (Cell Therapy and Gene Therapy), Application (Discovery and Pre-Clinical, and Others), End User (Pharmaceutical and Biotechnology Companies, and Others), and Geography (North America, Europe, Asia-Pacific, and Others). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Cell and Gene Therapy Market Trends and Insights

Exponential Growth in High-Throughput Gene-Editing Datasets Demands AI-Driven Analytics

The AI in cell and gene therapy market is benefiting from a data expansion wave that is now as much an infrastructure issue as a scientific one. Illumina introduced the Billion Cell Atlas in January 2026 as the first release in a planned 5-billion-cell program built to support AI-driven drug discovery workflows.As sequencing throughput rises, the operational bottleneck is moving away from data generation and toward annotation quality, because models still need clinically meaningful labels to separate real therapeutic signals from background biological noise. Recursion stated in 2026 that its biology maps, developed with Roche and Genentech, are built from more than 1 trillion iPSC-derived neuronal cells, which shows how curated multi-modal data can become a durable commercial asset rather than a disposable research input. This is why the AI in cell and gene therapy market is increasingly rewarding companies that control proprietary cellular datasets, not only those that publish stronger model architectures. Over time, the data owners with the broadest and cleanest libraries are likely to hold the strongest pricing power inside the AI in cell and gene therapy market.

Increasing Big-Pharma Alliances with AI Start-Ups to Shorten CGT Development Cycles

The AI in cell and gene therapy market is also gaining from a funding environment where large pharmaceutical companies treat AI as core development infrastructure. NVIDIA and Eli Lilly announced a co-innovation AI lab in January 2026, with a commitment of up to USD 1 billion over 5 years for protein diffusion models, genomics foundation models, and manufacturing digital twins. Roche then expanded its AI factory strategy in March 2026 with more than 3,500 Blackwell GPUs across U.S. and European sites, which signals that large drug makers are building private compute capacity for time-sensitive regulated workflows instead of relying only on public cloud access. These alliances are shortening development cycles, but they are also changing competitive behavior because AI start-ups that become embedded inside sponsor workflows are harder to replace later. In practice, the AI in cell and gene therapy market is starting to resemble enterprise software, where switching costs rise after models, data pipelines, and scientific decisions are tied to one platform. That makes commercial relationships in the AI in cell and gene therapy market more durable than standard project-based outsourcing.

Fragmented, Proprietary Clinical Datasets Limit Model Generalizability

The AI in cell and gene therapy market still faces a hard limit from siloed datasets that do not transfer cleanly across donors, disease settings, or manufacturing sites. A March 2026 review in Pharmaceutics described how AI models in cell and gene therapy often struggle to generalize when they are trained within narrow sponsor-specific data environments. This means architectural progress alone will not solve the performance gap if the training data remain fragmented and proprietary. It also creates a strong first-mover advantage for any organization that can aggregate diverse multi-site and multi-sponsor manufacturing and clinical datasets into one usable framework. Federated learning can reduce some of the sharing barriers, but it also slows execution because sites often work under different governance, privacy, and operational standards. Until the AI in cell and gene therapy market has stronger interoperability rules, model performance in the lab will continue to outpace what can be deployed consistently in commercial programs.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of Single-Cell Multi-Omics with Generative AI for Potency Prediction

- AI-Enabled Digital Twins Optimizing Bioreactor Parameters for Cell-Therapy Yields

- Data-Privacy and Governance Concerns in Patient-Level Genomic Information

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software/AI platforms accounted for 48.24% of the AI in cell and gene therapy market share in 2025, which made them the largest component category. That position reflects where buyers now see the most value, since model development, workflow orchestration, and predictive analytics are treated as the main deliverables, while underlying data storage and generic compute are becoming more standardized. The AI in cell and gene therapy market is therefore assigning more value to the control layer that links experiments, data, and decision support than to basic implementation work alone. Benchling's May 2026 work with Baseten to bring GPU-scale inference into biotech R&D workflows shows how software vendors are absorbing capabilities that were previously handled by separate infrastructure providers. The same software segment is projected to expand at 22.17% CAGR through 2031, which means the largest component in the AI in cell and gene therapy market is also one of the fastest-moving.

Services still account for a meaningful share of revenue, but their role is shifting toward implementation support, validation, and regulatory advisory work tied to more complex deployments. Standard pre-clinical tasks are becoming more automated, which reduces labor intensity and slows the relative growth of services compared with software-led platforms. The AI in cell and gene therapy industry is also seeing buyers prefer repeatable platform subscriptions over one-time service engagements when they expect frequent model updates and ongoing workflow integration. Post-market surveillance and GMP quality functions still represent a smaller part of software spending than discovery does, yet that balance is likely to change as lifecycle expectations become stricter. Across the AI in cell and gene therapy market, the component mix suggests that durable value is building around integrated platforms that can hold experimental context, model outputs, and decision history in one operating environment.

Cloud-based deployment held 53.26% share in 2025, and is projected to grow at 22.38% CAGR through 2031, which makes it the fastest-growing deployment format in the AI in cell and gene therapy market. This pattern reflects the practical needs of discovery and pre-clinical teams, where access to distributed GPU infrastructure can be expanded faster than local hardware can be installed and validated. Cloud deployment also suits workloads that rise and fall across screening cycles, because organizations can scale compute without carrying all of the capital burden on site. In that sense, the AI in cell and gene therapy market is using cloud more as an operating model than only as a hosting decision. It is widening access for smaller developers that would otherwise struggle to fund advanced training and inference capacity.

Adoption remains uneven, though, because regulated manufacturing environments still require tighter control over data location, audit trails, latency, and system validation. Roche's March 2026 AI factory expansion, with large GPU clusters across U.S. and European sites, is a clear signal that major manufacturers still view private infrastructure as a strategic requirement for certain regulated workflows. On-premises and edge or hybrid models therefore remain important in the AI in cell and gene therapy market even while cloud grows faster overall. Edge and hybrid architectures are currently smaller in revenue terms, but they are well placed for future growth in commercial manufacturing because they combine local governance with selected access to external compute. Over time, the AI in cell and gene therapy market is likely to separate by function, with cloud leading early-stage experimentation and hybrid deployment gaining ground where GMP oversight is strictest.

Complete Report Scope:

- By Component

- Software / AI platforms

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Edge / Hybrid

- By Therapy Type

- Cell Therapy

- Gene Therapy

- By Application

- Discovery and Pre-Clinical

- Clinical Validation

- Commercial Manufacturing

- Post-market Surveillance

- By End User

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs)

- Contract Development and Manufacturing Organizations (CDMOs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 51.62% of the AI in cell and gene therapy market share in 2025, which kept it as the leading regional cluster. The region benefits from strong sponsor concentration, deep venture support, and the FDA's active work on lifecycle management and risk-based validation for AI-related regulated software environments The U.S. remains the central driver because large pharmaceutical headquarters, academic cell therapy hubs, and advanced compute infrastructure are located close to one another. NVIDIA stated in 2026 that LillyPod became the world's first NVIDIA DGX SuperPOD with DGX B300 systems, giving North American developers a major compute advantage for scaled model development and deployment.

Europe remains an established part of the AI in cell and gene therapy market, supported by strong bioprocess engineering capabilities and tighter attention to data compliance. Germany stands out because equipment, process engineering, and manufacturing know-how are closely tied to therapeutic development. Sartorius announced in 2025 that it was working with NVIDIA to advance AI in drug discovery and manufacturing, which fits Europe's strength in linking instrumentation, data capture, and process insight. The United Kingdom, France, Italy, Spain, and the rest of Europe continue to add value through academic-originated AI biotech companies, specialized clinical programs, and EU-level support frameworks.

Asia-Pacific is projected to expand at 23.62% CAGR through 2031, which makes it the fastest-growing regional segment in the AI in cell and gene therapy market. China, Japan, and South Korea are the main growth centers, with stronger policy support, rising trial activity, and expanding local development ecosystems. Japan is contributing through company and academic work on manufacturing optimization and cell reprogramming, including Hitachi's platform development for high-throughput cell design. South Korea and Australia are adding regional volume through CRO growth and clinical trial activity, which broadens the operating base for the AI in cell and gene therapy market beyond the largest national players. Middle East and Africa, especially the GCC and South Africa, and South America, including Brazil and Argentina, remain smaller markets, but they are starting to build relevance through selective government-backed genomic medicine and advanced therapy programs.

- 10x Genomics

- Atara Biotherapeutics

- Benchling

- Cellarity

- Cytiva

- FUJIFILM

- Ginkgo Bioworks

- Google DeepMind

- IBM

- Illumina

- Insitro

- Lonza Group

- Microsoft

- NVIDIA

- Owkin

- PerkinElmer

- Recursion Pharmaceuticals

- Sartorius

- Strateos

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential Growth in High-Throughput Gene-Editing Datasets Demands AI-Driven Analytics

- 4.2.2 Increasing Big-Pharma Alliances with AI Start-Ups to Shorten CGT Development Cycles

- 4.2.3 Falling Cost of Cloud GPUs Accelerating AI Adoption Across the CGT Value Chain

- 4.2.4 Convergence of Single-Cell Multi-Omics with Generative AI For Potency Prediction

- 4.2.5 AI-Enabled Digital Twins Optimizing Bioreactor Parameters for Cell-Therapy Yields

- 4.2.6 Enterprise AI Platforms and GPU Access Enable Bundled, Scaled Deployments

- 4.3 Market Restraints

- 4.3.1 Fragmented, Proprietary Clinical Datasets Limit Model Generalizability

- 4.3.2 Data-Privacy & Governance Concerns in Patient-Level Genomic Information

- 4.3.3 Regulatory Ambiguity in Software-as-a-Medical-Device (SAMD) AI Validation in CGT

- 4.3.4 Supply-Chain Bottlenecks for GMP-Grade GPU Clusters

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software / AI platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Edge / Hybrid

- 5.3 By Therapy Type

- 5.3.1 Cell Therapy

- 5.3.2 Gene Therapy

- 5.4 By Application

- 5.4.1 Discovery and Pre-Clinical

- 5.4.2 Clinical Validation

- 5.4.3 Commercial Manufacturing

- 5.4.4 Post-market Surveillance

- 5.5 By End User

- 5.5.1 Pharmaceutical and Biotechnology Companies

- 5.5.2 Contract Research Organizations (CROs)

- 5.5.3 Contract Development and Manufacturing Organizations (CDMOs)

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 10x Genomics

- 6.3.2 Atara Biotherapeutics

- 6.3.3 Benchling

- 6.3.4 Cellarity

- 6.3.5 Cytiva (Danaher)

- 6.3.6 Fujifilm Diosynth Biotechnologies

- 6.3.7 Ginkgo Bioworks

- 6.3.8 Google DeepMind

- 6.3.9 IBM

- 6.3.10 Illumina, Inc.

- 6.3.11 Insitro

- 6.3.12 Lonza

- 6.3.13 Microsoft

- 6.3.14 NVIDIA

- 6.3.15 Owkin

- 6.3.16 PerkinElmer, Inc.

- 6.3.17 Recursion Pharmaceuticals

- 6.3.18 Sartorius AG

- 6.3.19 Strateos

- 6.3.20 Thermo Fisher Scientific, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment