|

시장보고서

상품코드

2072760

루푸스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lupus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

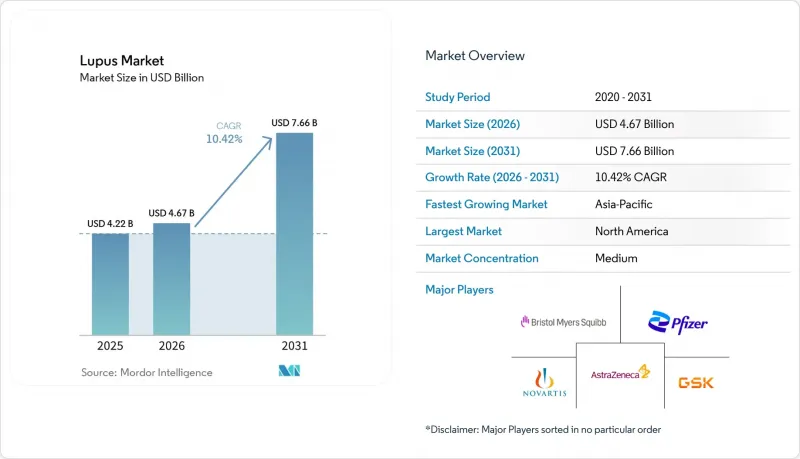

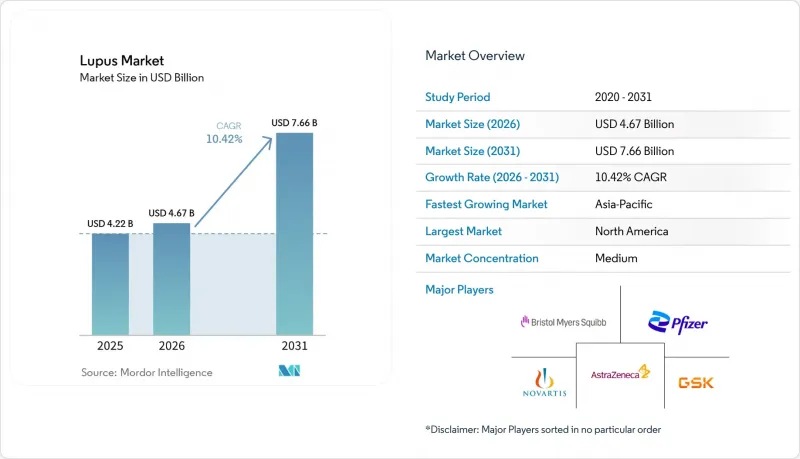

Mordor Intelligence에 의하면, 루푸스 시장 규모는 2025년에 42억 2,000만 달러로 평가되었고, 2026년 46억 7,000만 달러로 추정되고, 2031년까지 76억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.42%를 나타낼 전망입니다.

본 보고서는 질환 유형별(SLE, CLE, 기타), 치료법별(코르티코스테로이드, 면역억제제, 생물학적 제제, 항말라리아제, 항고혈압제, 기타), 진단법별(임상 검사, 생검, 영상 진단, 기타), 최종 사용자별(병원, 전문 클리닉, 재택치료, 진단 검사 기관), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 루푸스 시장 동향 및 인사이트

유병률 증가와 루푸스의 조기 발견

검사에 대한 접근성이 개선됨에 따라, 임상의들은 루푸스를 조기에 진단할 수 있게 되었으며, 돌이킬 수 없는 장기 손상이 발생하기 전에 치료를 시작하는 환자 수가 증가하고 있습니다. 남아시아와 동남아시아, 사하라 이남 아프리카, 라틴아메리카 등의 지역에서는 진단 지연이 여전히 과제로 남아 있지만, 검사 인프라의 발전으로 인해 이 문제가 해결될 것으로 기대되고 있습니다. 혈청 라만 분광법이나 딥러닝 분류기 등의 도구를 통해 확정 진단 과정이 신속해졌으며, 증상 발현부터 치료 시작까지의 지연 시간이 단축되고 있습니다. 또한, 전자차트의 대시보드는 의료진이 후속 관리의 공백을 메우는 데 도움이 되고 있으며, 치료 대상 환자층을 확대함으로써 시장 성장을 더욱 촉진하고 있습니다.

표적형 생물학적 제제 및 스테로이드 감량 치료로의 전환

2025년에 개정된 치료 지침에서는 생물학적 제제의 조기 도입이 강조되고 있으며, 이를 배경으로 루푸스 시장은 표적형 생물학적 제제로의 전환과 스테로이드 사용량 감축으로 나아가고 있습니다. 이러한 추세에 따라 베리무맙, 아니플로맙, 보크로스포린 등의 치료법에 대한 수요가 증가하고 있습니다. 중국의 2025년판 지침 개정에서 생물학적 제제의 적용 범위가 확대되고 JAK 억제제가 도입된 것은 전 세계적으로 이에 대한 수용이 확산되고 있음을 반영합니다. 실제 임상 데이터에 따르면, 바이오마커를 기반으로 한 테리타시셉트는 표준 치료에 비해 더 높은 반응률과 더 큰 폭의 코르티코스테로이드 감량을 실현하고 있으며, 합병증을 줄임으로써 이 첨단 치료법이 보험사 측에 더 설득력 있는 선택지가 되고 있습니다.

평생 치료비의 부담과 접근성 장벽

선진적인 치료법을 뒷받침하는 강력한 임상적 근거가 있음에도 불구하고, 고액의 치료비가 여전히 루푸스 치료 시장을 제약하고 있습니다. 미국에서는 생물학적 제제를 이용한 연간 치료비가 3만 달러를 넘는 경우가 흔합니다. 2025년 분석에 따르면, 환자의 15.4%가 경제적 불안정에 직면해 있으며, 8.2%는 교통편 확보에 어려움을 겪고 있고, 12%는 보험 적용 대상에서 제외된 것으로 나타났습니다. 사프네로나 베리무맙과 같은 약물에 대한 엄격한 사전 승인 요건으로 인해, 기존 치료법이 효과를 보이지 않거나 장기 침범이 악화될 때까지 치료가 지연되고 맙니다. 신흥 시장에서는 보험이나 전문의의 정기적인 진료를 받을 수 없는 한, 하이드록시클로로퀸이나 코르티코스테로이드와 같은 표준 치료를 유지하는 것이 여전히 어렵습니다. 모니터링 체계나 전문의 확보가 미흡한 경우, 보험 급여만으로는 치료의 보급을 촉진할 수 없습니다.

부문별 분석

2025년, 전신성 홍반성 루푸스(SLE)는 루푸스 시장의 85.14%를 차지했으며, 치료 및 진단의 주요 대상으로 자리매김했습니다. 이러한 우위는 SLE가 신장, 심장, 신경정신계, 점막·피부계 등 광범위한 장기에 영향을 미치기 때문에 집중적인 치료와 복잡한 경과 관찰이 필요하다는 점에 기인합니다. 2025년 중국 SLE 치료 지침에서는 생물학적 제제 및 JAK 억제제가 권장되었으며, 장기적인 관해와 장기 보호를 위한 전환이 제시되었습니다. SLE 환자들은 고부가가치 치료 요법을 채택하는 경향이 강하고, 빈번한 모니터링이 필요하기 때문에 시장 성장을 주도하고 있습니다.

피부형 홍반성 루푸스는 여전히 규모가 작은 분야로, 주로 피부과에서 외용제를 통한 치료나 전신 약물의 사용 빈도가 낮은 형태로 관리되고 있습니다. 그러나 피부를 주요 병변으로 하는 질환의 병태에 부합하는 면역 반응을 표적으로 삼는 제약 기업이 늘어남에 따라, 그 전략적 중요성은 높아지고 있습니다. 약물 유발성 루푸스나 신생아 루푸스는 상업적으로는 제한적이지만, 진단 활동 및 전문의의 진료 수요에 기여하고 있습니다. 류마티스학, 피부과, 신장내과, 정신보건에 걸친 다직종 연계 진료의 추진을 통해 이러한 아형의 식별 및 관리 범위가 확대됨에 따라, 규모가 작은 분야라 하더라도 향후 수요를 뒷받침하게 될 것입니다.

2025년, 루푸스 치료 시장에서 생물학적 제제는 48.34%의 점유율을 차지했으며, 환자 대상 사용이 제한적임에도 불구하고 매출 측면에서 지배적인 위치를 차지하고 있음을 알 수 있습니다. 이러한 우월한 입지는 높은 가격 책정, 중증 환자에 대한 전문적인 적용, 그리고 활동성 루푸스 신염 및 난치성 SLE에 대한 집중적인 대응에 기인합니다. 로슈사는 오비누츠주맙과 표준 요법의 병용 요법에서 완전 신장 반응률이 46.4%였던 반면, 표준 요법 단독으로는 33.1%였다고 보고했으며, 이는 생물학적 제제에 대한 막대한 투자가 정당화됨을 뒷받침하고 있습니다. 고도의 치료법은 비용이 많이 들기 때문에 중증도가 높은 소수의 환자 집단이 치료비의 대부분을 차지하고 있습니다.

면역억제제는 2026-2031년 연평균 성장률(CAGR) 9.56%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 치료 분야가 될 전망입니다. 보크로스포린은 최신 특성과 2024년 일본 내 출시를 포함한 광범위한 승인 범위를 통해 이 약물군에 새로운 활력을 불어넣었습니다. 미코페놀산 모페틸과 타클로리무스는 스테로이드 최소화 지침에 따라 병용 요법으로 점점 더 많이 사용되고 있습니다. 항말라리아제는 여전히 SLE 치료의 주축을 이루고 있는 반면, 항고혈압제는 심혈관계 합병증 관리에 사용되고 있습니다. 시장이 보다 안전한 장기 치료 옵션으로 전환됨에 따라, 코르티코스테로이드에 대한 의존도는 점차 낮아지고 있습니다.

지역별 분석

2025년, 북미는 루푸스 시장에서 39.25%의 점유율을 차지하며 시장을 주도했습니다. 이는 류마티스과 및 신장내과 전문의의 밀도가 높고, 새로운 치료법을 조기에 이용할 수 있으며, 다른 시장에 비해 보험 적용 범위가 넓기 때문입니다. 2025년 ACR 지침 및 메디케어 파트 D 개혁에 따라 생물학적 제제에 대한 접근성이 확대되고, 환자의 본인 부담금이 경감되었습니다. 2026년 4월 미국에서 '사프네로 펜' 조치가 승인됨에 따라, 수액 센터에 대한 의존도가 낮아지고, 지역 류마티스 진료 현장에서의 복약 순응도가 향상되었습니다. 캐나다에서는 활동성 루푸스 신염에 대한 오비누츠주맙의 보험 적용 범위가 확대되어, 첨단 치료에 대한 접근성이 향상되었습니다.

유럽은 루프스 시장에서 여전히 2위의 지역 기여도를 유지하고 있으며, 독일, 영국, 프랑스가 가장 큰 매출을 올리고 있습니다. 2025년 12월 피하 투여형 아니플로르맙의 승인은 다른 생물학적 제제와 비교했을 때 투여 측면에서 불리했던 점을 해소함으로써 경쟁을 더욱 치열하게 만들었습니다. 또한, 이 지역에서는 강력한 후기 단계 신염 데이터와 SLE에 관한 보다 광범위한 데이터를 바탕으로, 규제 당국의 심사가 진행됨에 따라 오비누츠주맙의 적응증 확대로 인한 혜택을 누릴 것으로 예측됩니다. 서유럽은 생물학적 제제에 대한 접근성 면에서 앞서 있지만, 중·동유럽에서는 보험 급여 제도가 제각각이어서 도입 속도가 더딘 실정입니다.

아시아태평양은 루푸스 시장에서 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 11.20%를 나타낼 것으로 전망됩니다. 중국과 일본은 대규모 환자 수, 규제 당국의 신속한 승인, 전문 의료 기관에 대한 접근성 개선에 힘입어 성장을 주도하고 있습니다. 일본에서는 루푸스 신염 치료제인 보크로스포린의 승인 및 출시가 고부가가치 치료 도입의 선례가 되었습니다. 중국에서는 2025년 치료 지침 개정을 통해 생물학적 제제의 사용 범위가 확대되고, 주요 병원에서 이를 공식적으로 처방할 수 있는 체계가 마련되고 있습니다. 인도, 한국, 호주도 성장에 기여하고 있지만, 남미, 중동 및 아프리카는 인프라가 미비하고 본인 부담 비용이 높기 때문에 여전히 초기 단계 시장에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the lupus market size was valued at USD 4.22 billion in 2025 and is estimated to grow from USD 4.67 billion in 2026 to reach USD 7.66 billion by 2031, at a CAGR of 10.42% during the forecast period (2026-2031).

This report is Segmented by Disease Type (SLE, CLE, Others), Treatment Type (Corticosteroids, Immunosuppressives, Biologics, Antimalarials, Antihypertensives, Others), Diagnosis (Laboratory Tests, Biopsy, Imaging, Others), End User (Hospitals, Specialty Clinics, Homecare, Diagnostic Labs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Lupus Market Trends and Insights

Rising Prevalence and Earlier Lupus Detection

As testing access improves, clinicians are diagnosing lupus earlier, increasing the number of patients entering treatment before irreversible organ damage occurs. Underdiagnosis remains a challenge in regions like South and Southeast Asia, Sub-Saharan Africa, and Latin America, but advancements in testing infrastructure are expected to address this issue. Tools such as serum Raman spectroscopy and deep-learning classifiers are expediting confirmation processes, reducing delays between symptom onset and treatment. Electronic health record dashboards are also helping providers close follow-up gaps, further supporting market growth by expanding the treated population.

Shift Toward Targeted Biologics and Steroid-Sparing Treatment

The lupus market is shifting towards targeted biologics and reduced steroid use, driven by updated 2025 treatment guidelines emphasizing early biologic initiation. This trend is increasing demand for therapies like belimumab, anifrolumab, and voclosporin. China's 2025 guideline update expanded biologic adoption and introduced JAK inhibitors, reflecting broader global acceptance. Real-world evidence shows biomarker-guided telitacicept achieves higher response rates and greater corticosteroid reduction compared to standard treatments, making advanced therapies more defensible to payers by reducing complications.

High Lifetime Treatment Cost and Access Barriers

High treatment costs continue to restrict the lupus market, despite strong clinical evidence supporting advanced therapies. In the U.S., annual biologic therapy costs often exceed USD 30,000. A 2025 analysis showed that 15.4% of patients faced financial instability, 8.2% encountered transportation challenges, and 12% lacked insurance coverage. Strict prior authorization requirements for agents like Saphnelo and belimumab delay treatment until earlier therapies fail or organ involvement worsens. In emerging markets, maintaining standard treatments like hydroxychloroquine and corticosteroids remains difficult without insurance or regular specialist access. Reimbursement alone cannot drive uptake if monitoring infrastructure and specialist availability are inadequate.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Expansion for Specialty Lupus Diagnostics and Therapeutics

- Rising Demand for Home-Based Administration and Self-Injection Devices

- Diagnostic Heterogeneity and Delayed Disease Confirmation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, systemic lupus erythematosus (SLE) accounted for 85.14% of the lupus market, establishing itself as the primary focus for treatment and diagnosis. This dominance is due to SLE's extensive organ involvement, including renal, cardiac, neuropsychiatric, and mucocutaneous systems, which necessitate intensive treatment and complex follow-ups. The 2025 Chinese guidelines for SLE endorsed biologics and JAK inhibitors, marking a shift toward long-term remission and organ protection. SLE patients are more likely to adopt high-value drug regimens and require frequent monitoring, driving market growth.

Cutaneous lupus erythematosus remains a smaller segment, primarily managed through dermatology with topical treatments and lower systemic drug intensity. However, its strategic importance is growing as companies target immune responses aligned with skin-dominant disease biology. Drug-induced and neonatal lupus, while commercially limited, contribute to diagnostic activities and specialist consultations. The push for multidisciplinary care across rheumatology, dermatology, nephrology, and mental health broadens the scope for identifying and managing these subtypes, supporting future demand even in smaller categories.

Biologic drugs held 48.34% of the lupus treatment market in 2025, reflecting their revenue dominance despite limited patient use. Their premium position stems from strong pricing, specialized application in severe cases, and focus on active lupus nephritis and refractory SLE. Roche reported a 46.4% complete renal response rate for obinutuzumab combined with standard therapy, compared to 33.1% for standard therapy alone, validating the high spending on biologics. A small group of high-acuity patients drives significant spending due to the high costs of advanced therapies.

Immunosuppressive drugs are projected to grow at a 9.56% CAGR from 2026 to 2031, making them the fastest-growing treatment category. Voclosporin has revitalized this class with its modern profile and broader regulatory approvals, including its 2024 launch in Japan. Mycophenolate mofetil and tacrolimus are increasingly used in combination regimens under steroid-minimization guidelines. Antimalarial drugs remain foundational in SLE care, while antihypertensives manage cardiovascular complications. Corticosteroid reliance is gradually decreasing as the market shifts toward safer long-term options.

Complete Report Scope:

- By Disease Type

- Systemic Lupus Erythematosus

- Cutaneous Lupus Erythematosus

- Others

- By Treatment Type

- Corticosteroids

- Immunosuppressive Drugs

- Biologic Drugs

- Antimalarial Drugs

- Antihypertensive Drugs

- Other Treatment Types

- By Diagnosis

- Laboratory Tests

- Biopsy

- Imaging Tests

- Other Diagnostic Methods

- By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

- Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America led the lupus market with a 39.25% share, driven by a high density of rheumatology and nephrology specialists, early access to new therapies, and broader reimbursement options compared to other markets. The 2025 ACR guideline and Medicare Part D reform expanded access to biologics, reducing out-of-pocket costs for patients. The U.S. approval of the Saphnelo Pen in April 2026 reduced dependence on infusion centers and improved adherence in community rheumatology settings. In Canada, reimbursement support for obinutuzumab in active lupus nephritis enhanced access to advanced therapies.

Europe remained the second-largest regional contributor to the lupus market, with Germany, the UK, and France generating the highest revenue. The approval of subcutaneous anifrolumab in December 2025 strengthened competition by addressing delivery disadvantages compared to other biologics. The region is also set to benefit from obinutuzumab expansion as regulatory reviews progress, supported by strong late-stage nephritis and broader SLE data. Western Europe leads in biologic access, while Central and Eastern Europe face slower adoption due to inconsistent reimbursement systems.

Asia-Pacific is the fastest-growing region in the lupus market, projected to grow at an 11.20% CAGR from 2026 to 2031. China and Japan drive growth with large patient populations, faster regulatory approvals, and improved specialty access. Japan's approval and launch of voclosporin for lupus nephritis set a precedent for premium therapy adoption. China's 2025 treatment guideline update supports broader biologic use and formalized prescribing in major hospitals. India, South Korea, and Australia contribute to growth, while South America and the Middle East and Africa remain early-stage markets, limited by infrastructure and high out-of-pocket costs.

- Abbvie

- Amgen

- AstraZeneca

- Aurobindo Pharma

- Biogen

- Bristol-Myers Squibb

- Dr. Reddy's Laboratories

- Eli Lilly and Company

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Johnson & Johnson

- Lupin

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- UCB

- Zydus Lifesciences Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence and Earlier Lupus Detection

- 4.2.2 Shift Toward Targeted Biologics and Steroid-Sparing Treatment

- 4.2.3 Reimbursement Expansion for Specialty Lupus Diagnostics and Therapies

- 4.2.4 Rising Demand for Home-Based Administration and Self-Injection

- 4.2.5 Biomarker-Driven Flare Prediction and Precision Monitoring

- 4.2.6 Pipeline Expansion in Lupus Nephritis and Refractory SLE

- 4.3 Market Restraints

- 4.3.1 High Lifetime Treatment Cost and Access Barriers

- 4.3.2 Diagnostic Heterogeneity and Delayed Disease Confirmation

- 4.3.3 Infection Risk and Long-Term Safety Concerns With Immunosuppression

- 4.3.4 Slow Clinical Translation and Narrow Trial Success Rates

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Disease Type

- 5.1.1 Systemic Lupus Erythematosus

- 5.1.2 Cutaneous Lupus Erythematosus

- 5.1.3 Others

- 5.2 By Treatment Type

- 5.2.1 Corticosteroids

- 5.2.2 Immunosuppressive Drugs

- 5.2.3 Biologic Drugs

- 5.2.4 Antimalarial Drugs

- 5.2.5 Antihypertensive Drugs

- 5.2.6 Other Treatment Types

- 5.3 By Diagnosis

- 5.3.1 Laboratory Tests

- 5.3.2 Biopsy

- 5.3.3 Imaging Tests

- 5.3.4 Other Diagnostic Methods

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Homecare Settings

- 5.4.4 Diagnostic Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Aurobindo Pharma Limited

- 6.3.5 Biogen Inc.

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 Dr. Reddy's Laboratories Ltd.

- 6.3.8 Eli Lilly and Company

- 6.3.9 GSK plc

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 Johnson and Johnson

- 6.3.12 Lupin Limited

- 6.3.13 Novartis AG

- 6.3.14 Pfizer Inc.

- 6.3.15 Sanofi S.A.

- 6.3.16 Sun Pharmaceutical Industries Limited

- 6.3.17 Teva Pharmaceutical Industries Limited

- 6.3.18 UCB S.A.

- 6.3.19 Zydus Lifesciences Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment