|

시장보고서

상품코드

2072846

동물성 소화물 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Animal Digest - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

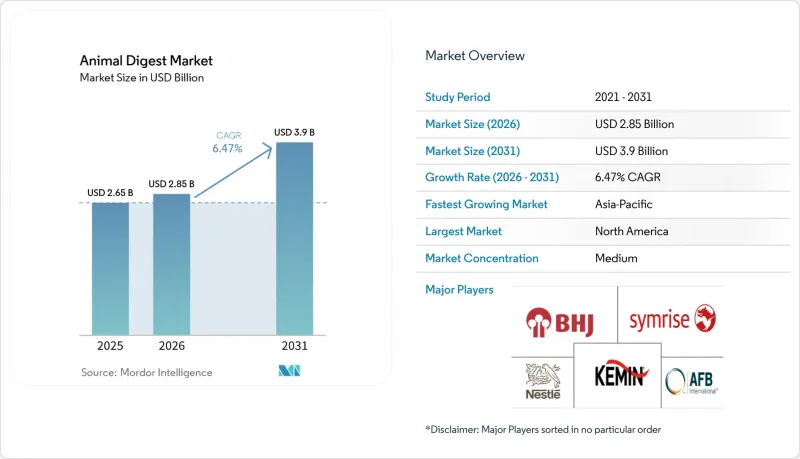

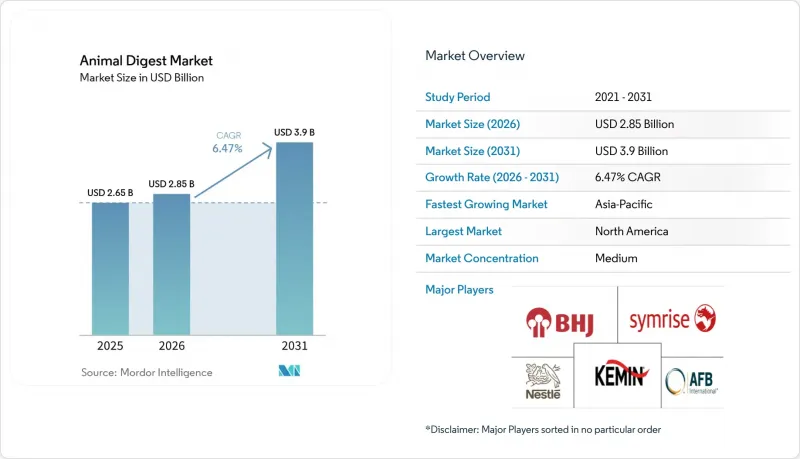

Mordor Intelligence에 의하면, 동물성 소화물 시장 규모는 2025년 26억 5,000만 달러로 평가되었고, 2026년 28억 5,000만 달러로 추정되고, 2031년까지 39억 달러로 확대될 전망이며, 2026-2031년 CAGR 6.47%를 나타낼 것으로 예측됩니다.

본 보고서는 원료별(가금류, 돼지, 소, 어류, 기타), 형태별(분말, 액체, 페이스트 및 슬러리), 용도별(반려동물사료, 수산 양식용 사료, 가축용 사료, 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 동물성 소화물 시장 동향 및 분석

프리미엄 반려동물 사료 시장의 성장에 따라, 동물성 소화물이 기호성 향상제로 자리매김하고 있습니다.

2025년 이후, 소비자들이 맛에 대해 지불할 의향이 더욱 강해지고 있는 만큼, 반려동물 사료 제조업체들은 동물성 부산물을 단순한 충전재에서 기능성 풍미 향상제로 재정의하기 위해 레시피를 재검토하고 있습니다. 네슬레 퓨리나 펫케어 컴퍼니(Nestle S.A.)는 영국 위스벡에 위치한 공장의 현대화에 1억 5,000만 유로(약 2억 달러) 이상을 투자하고 있습니다. 2025년 초까지 완료될 예정인 이 프로젝트는 생산 라인의 현대화, 자동화 추진, 에너지 효율 향상 및 이산화탄소 배출량 감축을 목표로 하고 있습니다. AFB 인터내셔널(The Ensign-Bickford Industries, Inc.)은 2024년 조지아주 콜럼버스에 7,900만 달러를 투자하여 아시아태평양의 프리미엄 시장에 대응하기 위해 2024년 태국에 허브를 개설했습니다. 성분 데이터에 따르면, 프리미엄 건식 사료에는 현재 2%-4%의 소화물(다이제스트)이 포함되어 있는 반면, 이코노미 사료에는 0.5%-1.5%에 그치고 있습니다. 이로 인해 1Kg당 원자재 비용은 0.15-0.30달러 상승했으나, 기호성이 브랜드 충성도를 높이는 경우 제조업체는 높은 투입 비용을 상쇄할 수 있음이 입증되었습니다.

수산물 양식용 사료로의 적용이 급속히 확대되고 있습니다.

새우나 어류의 양식업자들은 대두나 곤충 사료의 배합 비율 증가로 인한 악취를 해소하기 위해 동물성 소화물을 배합하고 있습니다. Symrise AG사는 집약형 양식장에서의 사료 섭취율을 향상시키는 'Actipal' 등의 어류 및 갑각류 가수분해물을 판매하고 있습니다. 2026년 미국 곡물 및 바이오 제품 협의회가 검증한 태평양 흰새우를 대상으로 한 실험에서 어류 단백질 소화물을 2% 배합한 사료가 대조군 사료에 비해 섭식량을 8%, 체중 증가율을 5% 향상시킨 것으로 나타났습니다. 베트남의 VNF사와 프랑스의 Adisseo사도 유사한 효과를 목적으로 한 새우 유래 펩타이드를 공급하고 있는 반면, Kemin사는 2025년에 이탈리아에 본사를 설립하여 수산 사료의 연구 개발을 강화했습니다. 현재 아시아태평양은 전 세계 양식 생산량의 85% 이상을 차지하고 있으며, 사료 배합에 대한 수요가 앞으로도 계속 증가할 것으로 확실시되고 있습니다.

유럽 및 북미의 엄격한 렌더링 제품별 규제

유럽연합(EU) 규정 1069/2009는 추적성, 열처리 및 검사를 강화하는 카테고리 3의 관리를 의무화하고 있으며, 이로 인해 규정 준수 비용이 1kg당 0.05-0.12달러 증가하고 있습니다. 유럽식품안전청(EFSA)은 2024-2025년 발표된 여러 건의 의견서에서 미생물학적 기준을 강화하고 감사 빈도를 높일 것을 요구하고 있습니다. 캐나다 식품검사청은 2024년 7월, 개정된 RG-4 지침을 도입하여 문서화 요건을 강화했습니다. 이는 소규모 렌더링 사업자에게 감가상각이 어려운 부담이 되고 있습니다. 2025년 1월, 미국 식품의약국(FDA)은 '동물용 식품 원료 요람'을 발행하고, 제조 공정의 심사를 확대하는 한편, 품질 관리 시스템에 대한 설비 투자를 늘렸습니다. 이러한 중복된 규제로 인해 대규모 사업자의 영향력이 강화되어, 고정적인 규정 준수 투자 비용을 더 많은 처리량에 분산시킬 수 있게 되었습니다.

부문별 분석

2025년에는 전 세계 육계 생산량이 471억 파운드(2,355만 메트릭톤)에 달한 것으로 평가되었고, 가금류 부산물이 동물성 부산물 시장의 46.0%를 차지할 것으로 전망됩니다. 미국 농무부(USDA) 경제조업체국(ERS)에 따르면, 이를 통해 제품별 안정적인 공급이 확보될 전망입니다. 돼지 유래 소화물은 아미노산 구성과 개에 대한 높은 수용성 덕분에 2위를 차지하고 있지만, 아프리카 돼지열병으로 인해 주기적인 공급 부족이 발생하고 있습니다. 소 유래 소화물 추출물은 특정 펩타이드 범위를 중시하는 틈새 시장용 저알레르기 사료나 특정 수산 양식용 배합 사료에 이용되고 있습니다. 어류 유래 소화물은 오메가-3 함량과 감칠맛 덕분에 기호성을 높여주므로, 해양성 고양이 사료나 고성능 새우 사료에 필수적입니다. 곤충 유래 소화물은 현재 규모가 작지만, 유럽 및 아시아 규제 당국이 검은파리나 밀웜의 가수분해물을 승인하고 신규 공장에 대한 자금 유입이 재개됨에 따라 연평균 성장률(CAGR) 10.9%를 기록하며 가장 빠르게 성장하는 부문이 될 것으로 전망됩니다.

동물성 소화물 시장에서 가금류가 지배적인 위치를 차지하고 있는 것은 내장이나 폐계(폐사 닭)를 비용 경쟁력이 있는 가수분해물로 전환하는 통합적인 렌더링 네트워크가 존재하기 때문입니다. 미국의 렌더링 업체는 국내 및 수출용 미생물학적 기준을 모두 충족하는 자동 온도 및 시간 제어 시스템을 도입하여 일관된 품질을 보장하고 있습니다. 반면, 곤충 생산 업체들은 전용 가수분해 라인을 구축하고 다운스트림 공정의 분무 건조기에 투자해야 하기 때문에 기존 원료와의 비용 경쟁력 확보가 더디게 진행되고 있습니다. 2025년 6월에 출원된 곤충 단백질 가수분해물에 관한 특허 출원은 기술적 진보를 보여주고 있지만, 상용화를 위해서는 생산량 확대와 안정적인 자금 조달이 필요합니다. '클린 라벨' 및 '새로운 단백질'을 내세우는 브랜드는 이미 곤충 유래 소화물을 0.5%에서 1%의 배합 비율로 제품에 첨가하고 있으며, 생산 능력이 확대되면 이 부문은 비약적인 성장을 이룰 것으로 전망됩니다.

지역별 분석

북미는 2025년, 다국적 반려동물사료 기업의 본사, 첨단 렌더링 사업, 그리고 높은 반려동물 사육률에 힘입어 동물성 부산물 시장의 38.0%를 차지했습니다. 미국 농무부의 추산에 따르면, 2024년 소·송아지 및 돼지의 생산량은 3,922만 메트르톤에 달하며, 이는 소화물 원료의 안정적인 공급원이 되고 있습니다. 네슬레 퓨리나 펫케어(네슬레 S.A.), 마스 펫케어, J.M. 스마커는 각각 부지 내에 기호성 향상제 분무 라인을 갖춘 여러 공장을 운영하며, 지역 수요를 뒷받침하고 있습니다. 질병 발생은 여전히 위험 요인으로 작용하고 있으며, 예를 들어 조류 인플루엔자로 인한 가금류 전두 살처분이나 카리브해 지역에서 유입된 아프리카 돼지열병의 위협 등을 들 수 있습니다. 후자에 대해서는 2026년에 돼지의 이동을 제한하는 연방 명령이 발령되었습니다. 북미에서는 프리미엄화 추세, 치료용 사료 수요 증가, 그리고 단일 단백질 원료를 내세우는 제품의 보급이 성장을 견인하여 시장의 성숙화를 상쇄할 것으로 예측됩니다.

아시아태평양은 중국과 인도의 반려동물 사육 마릿수 증가와 동남아시아의 수산 양식 산업 성장이 맞물리면서, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.8%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 중국의 닭고기 생산량은 2026년에 1,730만 메트르톤에 달하고, 수출량은 140만 메트르톤이 될 것으로 예상되며, 이에 따라 렌더링 원료공급량도 확대될 것입니다. AFB International(The Ensign-Bickford Industries, Inc.)은 2024년에 태국에 본사를 설립하고 현지에서 향료 생산을 시작했습니다. 한편, Symrise AG는 해당 지역의 새우 양식업자들을 대상으로 'ActITuna Oil' 및 'Actipal'을 판매하고 있습니다. 인도는 시장 규모는 작지만, 도시 지역 소비자들이 음식물 쓰레기에서 시판되는 반려동물사료로 전환하고 있어, 이에 따라 반려동물사료에 대한 수요가 증가하고 있습니다. 한국과 태국에서는 곤충 단백질에 관한 규제가 명확해지고 있어, 검은 군파리 가공업체로부터 향후 소화물 공급의 길이 열리고 있습니다.

유럽은 독일, 프랑스, 영국의 대규모 반려동물사료 산업 클러스터에 힘입어 여전히 주요 소비 시장으로 자리 잡고 있습니다. 그러나 규정 1069/2009로 인해 추가 비용이 발생하고, 소규모 시장 진출기업들이 진입을 가로막히고 있어 성장이 제약을 받고 있습니다. 켈리 그룹의 2024년 매출액은 기호성 향상제를 공급하는 '테이스트 앤 뉴트리션' 부문의 지속적인 성장을 반영한 것이었습니다. 2024년부터 2025년에 걸쳐 유럽식품안전청(EFSA)은 검은살파리와 밀웜의 가수분해물에 대한 안전성을 확인하는 여러 가지 견해를 발표함으로써, 곤충 유래 제품 시장 출시를 촉진했습니다. 그럼에도 불구하고, 동유럽 돼지고기 시장의 변동이나 카테고리 3 관련 서류 요건의 강화로 인해 단기적인 공급 유연성에 차질이 생길 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the animal digest market size is projected to expand from USD 2.65 billion in 2025 and USD 2.85 billion in 2026 to USD 3.90 billion by 2031, registering a 6.47% CAGR over 2026-2031.

This report is Segmented by Source (Poultry, Porcine, Bovine, Fish, and Others), by Form (Powder, Liquid, and Paste/Slurry), by Application (Pet Food, Aquaculture Feed, Livestock Feed, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Animal Digest Market Trends and Insights

Growth in Premium Pet Food, Positioning Animal Digest as a Palatability Enhancer

Pet food manufacturers are redesigning recipes to elevate animal digest from a filler to a functional flavor driver, because consumer willingness to pay for taste has intensified since 2025. Nestle Purina PetCare Company (Nestle S.A.) is investing over EURO 150 million (approximately USD 200 million) to upgrade its Wisbech, United Kingdom, plant. Scheduled for completion by early 2025, the project aims to modernize production lines, enhance automation, improve energy efficiency, and reduce carbon emissions. AFB International (The Ensign-Bickford Industries, Inc.) deployed USD 79 million in Columbus, Georgia, in 2024 and opened a Thailand hub in 2024 to serve Asia-Pacific premium tiers. Formulation data show premium dry dog food now contains 2% - 4% digest, versus 0.5% - 1.5% in economy kibble, lifting raw-material costs per kilogram by USD 0.15-0.30 and proving manufacturers can absorb higher input costs when palatability drives brand loyalty.

Rapid Expansion of Aquaculture Feed Applications

Shrimp and finfish farmers are blending animal digest to overcome off-flavors associated with higher soy or insect meal inclusion rates. Symrise AG markets fish and crustacean hydrolysates such as Actipal that improve acceptance rates in intensive ponds. A 2026 US Grains and Bioproducts Council-reviewed trial on Pacific white shrimp showed 2% fish protein digest raised feed intake 8% and weight gain 5% versus a control diet. Vietnam's VNF and France's Adisseo supply shrimp-derived peptides that target the same outcome, while Kemin opened an Italy headquarters in 2025 to deepen aquafeed research and development. Asia-Pacific now delivers more than 85% of global aquaculture output, guaranteeing persistent demand tailwinds for digest inclusion.

Stringent Rendering By-product Regulations in Europe and North America

European Union Regulation 1069/2009 mandates Category 3 controls that heighten traceability, heat treatment, and testing, thereby lifting compliance costs by USD 0.05-0.12 per kilogram. The European Food Safety Authority tightened microbiological criteria in several 2024-2025 opinions, compelling more frequent audits. Canada's Food Inspection Agency introduced updated RG-4 guidance in July 2024 that intensified documentation requirements, a burden that smaller renderers find difficult to amortize. In January 2025 the United States Food and Drug Administration issued its Animal Food Ingredient Compendium, expanding process scrutiny and increasing capital outlays for quality systems. These overlapping rules consolidate power among scale operators, enabling them to spread fixed compliance investments across larger volumes.

Other drivers and restraints analyzed in the detailed report include:

- Cost Advantage Over Synthetic Flavor Alternatives

- Surge in Single-Protein Diets for Companion Animals

- Volatility in Poultry and Porcine By-product Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poultry digest is projected to account for 46.0% of the animal digest market in 2025, driven by global broiler production reaching 47.1 billion pounds (23.55 million metric tons) that year. This ensures a stable supply of by-products, according to the United States Department of Agriculture (USDA) Economic Research Service (ERS). Porcine digest ranks second because of its amino-acid profile and high canine acceptance, although African swine fever causes periodic shortages. Bovine digest serves niche hypoallergenic diets and certain aquaculture formulations that value specific peptide ranges. Fish digest is essential in marine cat food and high-performance shrimp feed, where omega-3 content and umami flavor boost palatability. Insect digest, while small today, is forecast to be the fastest-growing segment, with a 10.9% CAGR, as European and Asian regulators approve black soldier fly and mealworm hydrolysates and capital flows resume into new plants.

Poultry's dominance within the animal digest market size reflects integrated rendering networks that convert offal and spent hens into cost-competitive hydrolysates. United States renderers rely on automated temperature-time systems that meet both domestic and export microbiological standards, which supports consistent quality. In contrast, insect producers must build specialized hydrolysis lines and invest in downstream spray dryers, delaying cost parity with traditional sources. Patent activity filed in June 2025 for an insect protein hydrolysate demonstrates technical advances, yet commercialization awaits higher production volumes and stable financing. Brands focused on clean-label or novel-protein claims already formulate with insect digest at inclusion levels of 0.5% to 1%, positioning the segment for outsized growth once capacity expands.

Complete Report Scope:

- By Source

- Poultry

- Porcine

- Bovine

- Fish

- Others

- By Form

- Powder

- Liquid

- Paste/Slurry

- By Application

- Pet Food

- Aquaculture Feed

- Livestock Feed

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America captured 38.0% of the animal digest market in 2025, driven by multinational pet food headquarters, sophisticated rendering operations, and high pet ownership rates. The United States Department of Agriculture measured cattle and calf plus hog and pig output at 39.22 million metric tons in 2024, a stable feedstock base for digests. Nestle Purina PetCare Company (Nestle S.A.), Mars Petcare, and The J.M. Smucker Company each operate multiple plants with on-site palatant spray lines, reinforcing regional demand. Disease outbreaks continue to pose risks, such as avian influenza leading to poultry depopulations and African swine fever threats from the Caribbean, which resulted in a 2026 Federal Order restricting hog movement. Growth in North America is expected, driven by increasing premiumization, therapeutic diets, and single-protein claims, which help counterbalance market maturity.

Asia-Pacific is projected to be the fastest-growing region at a 7.8% CAGR during 2026-2031, driven by rising pet adoption in China and India, and by converging aquaculture growth in Southeast Asia. China's chicken production is set to hit 17,300 thousand metric tons in 2026, with exports at 1,400 thousand metric tons, expanding rendering inputs. AFB International (The Ensign-Bickford Industries, Inc.) opened a Thailand headquarters in 2024 for local palatant production, while Symrise AG markets ActITuna Oil and Actipal to shrimp growers across the region. India, though smaller, is seeing urban consumers migrate from table scraps to commercial kibble, lifting digest demand. Regulatory clarity on insect proteins is advancing in South Korea and Thailand, opening the way for future digest supply from black soldier fly processors.

Europe remains a key consumer market, driven by large pet food clusters in Germany, France, and the United Kingdom. However, growth is constrained by Regulation 1069/2009, which imposes additional costs and discourages smaller market entrants. Kerry Group's 2024 revenue reflected continued growth in its Taste and Nutrition unit, which supplies palatants. In 2024-2025, the European Food Safety Authority issued several opinions confirming the safety of black soldier fly and mealworm hydrolysates, facilitating the introduction of insect digest products. Despite this, short-term supply flexibility may be affected by volatility in the pork market in Eastern Europe and by stricter Category 3 documentation requirements.

- Kemin Industries, Inc.

- AFB International

- Symrise AG

- Nestle Purina PetCare Company

- BHJ A/S

- Darling Ingredients Inc.

- Nutriad International NV

- Alltech, Inc.

- Kerry Group plc

- Charoen Pokphand Foods Public Company Limited

- Olam Food Ingredients Holdings Pte. Ltd.

- Biorigin Solucoes em Ingredientes Naturais Ltda.

- Bioiberica S.A.U.

- Wilbur-Ellis Nutrition, LLC

- Protix B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in premium pet food, positioning animal digest as a palatability enhancer

- 4.2.2 Rapid expansion of aquaculture feed applications

- 4.2.3 Cost advantage over synthetic flavor alternatives

- 4.2.4 Surge in single-protein diets for companion animals

- 4.2.5 Emerging insect-based animal digest production technologies

- 4.2.6 Upcycling waste streams from cultured-meat production

- 4.3 Market Restraints

- 4.3.1 Stringent rendering by-product regulations in Europe and North America

- 4.3.2 Volatility in poultry and porcine by-product supply

- 4.3.3 Negative consumer perception of "digest" labeling

- 4.3.4 Competition from clean-label plant hydrolysates

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source

- 5.1.1 Poultry

- 5.1.2 Porcine

- 5.1.3 Bovine

- 5.1.4 Fish

- 5.1.5 Others

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.2.3 Paste/Slurry

- 5.3 By Application

- 5.3.1 Pet Food

- 5.3.2 Aquaculture Feed

- 5.3.3 Livestock Feed

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Kenya

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Kemin Industries, Inc.

- 6.4.2 AFB International

- 6.4.3 Symrise AG

- 6.4.4 Nestle Purina PetCare Company

- 6.4.5 BHJ A/S

- 6.4.6 Darling Ingredients Inc.

- 6.4.7 Nutriad International NV

- 6.4.8 Alltech, Inc.

- 6.4.9 Kerry Group plc

- 6.4.10 Charoen Pokphand Foods Public Company Limited

- 6.4.11 Olam Food Ingredients Holdings Pte. Ltd.

- 6.4.12 Biorigin Solucoes em Ingredientes Naturais Ltda.

- 6.4.13 Bioiberica S.A.U.

- 6.4.14 Wilbur-Ellis Nutrition, LLC

- 6.4.15 Protix B.V.