|

시장보고서

상품코드

2072963

영국의 펜스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

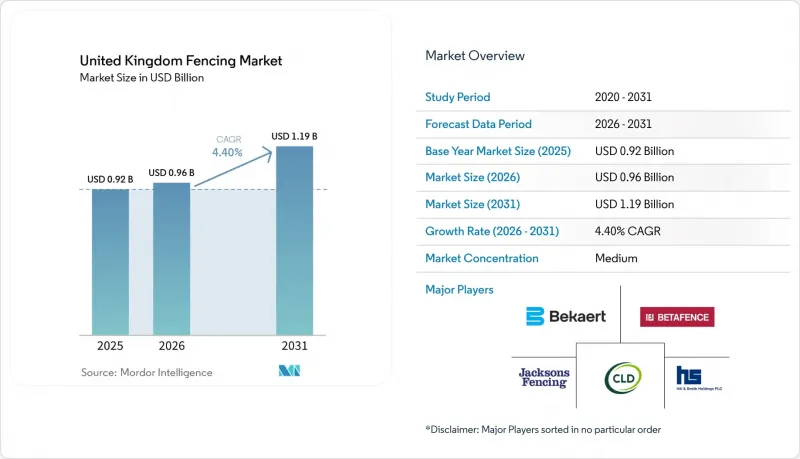

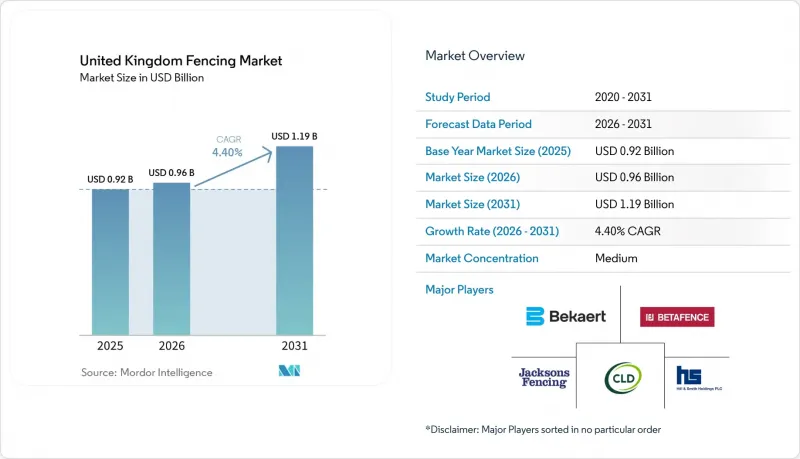

Mordor Intelligence에 의하면, 영국 펜스 시장 규모는 2025년 9억 2,000만 달러에서 2026년에는 9억 6,000만 달러로 확대되어 2031년까지 11억 9,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 4.40%로 성장할 전망입니다.

본 보고서는 소재별(금속, 목재, 플라스틱·복합재, 콘크리트, 기타 소재), 최종 사용자별(주택, 농업, 기타), 설치 유형별(고정식/영구 펜스, 가설식/이동식 펜스), 설치 채널별(전문 업체, 기타) 및 지역별(잉글랜드, 스코틀랜드, 웨일스, 북아일랜드)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국 펜스 시장 동향과 인사이트

정부 자금을 통한 주변 보안 강화가 중요 인프라 시설의 펜스 수요를 끌어올리고 있습니다.

'2025년도 지출 재검토'에 따라 통합 안보 기금을 통해 2028-2029 회계연도까지 연간 최소 1억 파운드(1억 2,700만 달러)를 출연하기로 약속하고, 방위 자본 예산을 2025-2026 회계연도의 232억 파운드(295억 달러)에서 2029-2030 회계연도에는 332억 파운드(422억 달러)로 증액하는 한편, 군용 숙소 개보수에만 70억 파운드(89억 달러)가 배정되었습니다. 이러한 지출 기반은 영국 펜스 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 주변 경비 시스템은 단순히 펜스 교체 주기에만 의존하는 것이 아니라, 국방, 교정, 교통, 중요 인프라 분야의 각 예산에 포함되어 있기 때문입니다. 또한, 해당 보고서에서는 2031년까지 수용 인원을 1만 4,000명 늘리기 위해 70억 파운드(89억 달러)가 배정되었으며, 이는 수용 시설 주변의 고사양 펜스 및 출입 통제 시스템에 대한 다년간 수요를 뒷받침할 것입니다. 2025년 6월의 '국가안보전략'에 따라 국가 중요 인프라 보호가 공식적인 우선 과제로 자리 잡았으며, 이에 따라 조달 동향은 저가형 주변 보안 제품에서 규격 인증을 받은 시스템으로 전환되고 있습니다. 힐 앤 스미스(Hill & Smith)사는 2025년도 연간 실적 발표에서 데이터센터 수요가 주변 보안 매출의 주요 견인 역할을 하고 있다고 밝혔으며, 이는 디지털 인프라가 고부가가치 펜스 시스템의 주요 구매자로 부상하고 있음을 보여줍니다. 이로 인해 영국 펜스 시장 전반에 걸쳐 사양 수준이 높아지고 있으며, 시험을 통과한 제품과 인증된 설치 역량을 바탕으로 프리미엄 보안 기준을 충족할 수 있는 공급업체로 가치가 이동하고 있습니다.

팬데믹 이후 주택 개조 활동이 활발해지면서 주택용 펜스 설치가 증가하고 있습니다.

2025년 한 해 동안 민간 주택의 보수 및 유지 관리 활동이 활발해졌으며, 2026년에도 이러한 추세가 이어지면서 영국 펜스 시장의 주택 부문에서 경계 제품의 교체 및 업그레이드 수요를 지속적으로 뒷받침하고 있습니다. 해당 국가에는 규모가 크고 노후화된 주택 재고가 존재하기 때문에 주택 수요는 여전히 크며, 신축 주택 착공이 주춤하는 시기에도 펜스의 정기적인 교체 수요가 발생하고 있습니다. 수요 증가는 설치 활동뿐만 아니라, 주택 소유자들이 기본적인 보급형 펜스 솔루션보다 품질이 더 우수하고 보증 기간이 긴 제품을 선호하는 추세가 강화되고 있는 점에도 영향을 받고 있습니다. 이러한 추세는 공급업체의 전략에도 반영되어, 각 제조업체들은 2024년과 2025년에 지속적인 업그레이드 수요를 흡수하기 위해 수명이 긴 목재 및 하이브리드 복합재 제품 라인업을 도입했습니다. 그 결과, 영국의 펜스 시장에서는 설치 건수의 전반적인 증가세가 완만한 수준에 그치더라도, 프로젝트당 수익은 증가할 가능성이 있습니다. 또한, 공공시설의 보안 및 인프라 관련 펜스 프로젝트에 대한 관심이 높아지고 있음에도 불구하고, 주택 부문의 중요성이 여전히 크다는 점은 경쟁적 입지를 결정하는 데 있어 그 역할을 부각시키고 있습니다.

철강·목재 가격 변동이 펜스 시공업체의 이익률을 압박하고 있습니다.

많은 프로젝트가 고정가격 계약으로 발주되는 반면, 자재 비용은 시공 기간 동안 변동할 가능성이 있으므로, 투입 비용의 변동은 2026년 영국 펜스 시장에서 계속해서 주요 제약 요인으로 작용할 것입니다. 2025년, Timber Development UK(TDUK)는 목재 가격의 큰 변동을 보고했습니다. 이 단체의 목재 가격 지수는 2025년 초 107에서 2025년 중반에는 130까지 상승했으나, 이후 2025년 3분기에는 125로 안정되었고, 공급 상황의 개선에 따라 2025년 4분기에는 5% 추가 하락을 기록했습니다. 2025년 말 무렵 목재 가격은 안정세를 보였으나, 연중 내내 나타난 가격 변동은 2026년의 구매 및 입찰 결정에 계속해서 영향을 미치고 있습니다. 이러한 문제는 영국의 펜스 시장에서 특히 두드러지며, 향후 자재 비용이 불투명한 상황에서는 중소규모의 도급업체들이 공공 입찰 참여를 주저할 가능성이 있습니다. 그 결과, 입찰 경쟁이 약화되어 계약 체결이 지연될 우려가 있습니다. 또한, 비용 변동은 공급망을 관리하고 재고를 유지하며, 목재, 철강, 복합재 펜스 제품에 위험을 분산할 수 있는 통합형 제조업체에 유리하게 작용합니다. 장기적으로는 2026년의 전반적인 수요 상황이 견조한 추세를 보일 것으로 예상되는 가운데, 이러한 동향이 대형 사업자들 시장 점유율 확대를 뒷받침할 가능성이 있습니다.

부문별 분석

2025년, 금속은 매출의 46%를 차지하며 영국 펜스 시장에서 가장 큰 소재 부문이 되었습니다. 이러한 선도적 지위는 보안, 경계 보호, 교통, 유틸리티, 그리고 규격에 부합하는 메쉬, 강철 펜스, 내구성이 뛰어난 경계 시스템이 표준 요건으로 요구되는 기타 용도 분야에서 확고한 입지를 바탕으로 뒷받침되었습니다. 금속 시장에서는 철강이 큰 점유율을 차지하고 있었으나, 알루미늄은 내식성과 수명 주기 전반에 걸친 낮은 유지 관리 비용을 모두 갖추고 있어 주택 및 상업시설 분야에서 점유율을 확대했습니다. 또한, 금속은 외관 디자인보다 검증된 보안 성능과 구조적 내구성이 중시되는 프로젝트에서도 뚜렷한 우위를 유지했습니다. 그런 의미에서 다른 소재의 매력이 부각되고 있는 상황에서도 금속은 여전히 영국 펜스 시장의 핵심을 지탱하고 있습니다.

플라스틱 및 복합재료는 2031년까지 연평균 성장률(CAGR) 5.5%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 재료 그룹이 될 전망입니다. 이 부문은 지속가능성에 대한 요구 사항이 강화되고, 주택 및 상업 프로젝트에서 지속적인 유지보수 부담을 줄여주는 제품에 대한 수요가 증가함에 따라 혜택을 보고 있습니다. 2025년 공급업체 자료에 따르면, 15년에서 25년의 보증이 적용되는 재생재를 포함한 복합재 시스템이 등장했으며, 제품 수명 전반에 걸친 비용 측면에서 방부 처리 목재와의 차이가 더욱 두드러지고 있습니다. 목재는 여전히 주택용 및 농업용 펜스 분야에서 중요한 위치를 차지하고 있지만, 유지보수 부담이 크고 내구성이 더 뛰어난 대체재에 대한 고객의 관심이 높아짐에 따라 그 입지가 위협받고 있습니다. 콘크리트는 경계벽이나 방음벽 용도로, 특히 보수 공사가 진행 중인 도로나 철도 연선 부근에서 중요한 역할을 하고 있습니다. “건설 분야 목재 활용을 위한 산림 연구 로드맵”이는 보다 광범위한 건축 분야에서 목재에 대한 정책적·조달적 지원을 지속적으로 시사하고 있으며, 지역별 규정이 여전히 목재에 유리한 지역에서는 목재 펜스의 판매량 증가에 기여할 가능성이 있습니다. 그렇긴 하지만, 영국의 펜스 시장에서는 유지 관리에 드는 수고가 적고, 지속가능성 측면에서 우위를 차지하는 제품으로 소재의 성장 추세가 점차 바뀌고 있습니다.

2025년에는 주택 부문이 매출의 38%를 차지하며, 영국 펜스 시장에서 가장 큰 최종 사용자 부문이 되었습니다. 이러한 규모는 해당 국가의 광범위한 주택 기반과 기존 주택의 펜스 교체, 수리 및 정원 개조에 대한 지속적인 수요를 반영하고 있습니다. 수요가 4개 구성국 모두에 걸쳐 있기 때문에 이 부문은 특정 자본 지출 클러스터나 단일 기관 예산 주기에 얽매이지 않습니다. 농촌 지역의 토지 관리와 가축 펜스 설치에는 지속적인 정기적인 경계선 유지 관리가 필요하기 때문에 농업 분야 수요 역시 영국 펜스 시장의 주요 견인력 중 하나로 자리 잡고 있습니다. 또한, 공공 지출 프로그램을 통해 교도소, 군사 시설 및 기타 공공시설의 경계선 개보수 작업이 진행됨에 따라 군사, 국방 및 정부 관련 수요도 가속화되었습니다.

에너지 및 전력 분야는 2031년까지 연평균 성장률(CAGR) 6.2%를 나타낼 것으로 예측되며, 이에 따라 영국 펜스 시장에서 가장 빠르게 성장하는 최종 사용자 부문이 될 것입니다. 주요 견인 요인은 신규 기존 방식 발전소의 건설이 아니라, 재생에너지, 특히 대규모 태양광 발전입니다. 사용자 입력 예시로 제시된 클리브 힐 태양광 발전소 사례는 단일 대형 프로젝트의 경우 수 킬로미터에 달하는 주변 펜스가 필요할 수 있으며, 이러한 시설에서는 일반적인 농업 용도보다 더 높은 사양이 요구된다는 점을 보여줍니다. 광업, 석유, 화학 분야 수요는 신규 시설 건설 붐이라기보다는 기존 자산의 유지 관리에 의존하고 있기 때문에 비교적 안정적입니다. 판매량 증가세가 완만하더라도, 위험한 환경이나 높은 수준의 보안이 요구되는 환경에서는 사업자가 통합형 접근 제어 기능을 갖춘 인증된 주변 펜스 솔루션을 필요로 하기 때문에 여전히 그 가치가 유지되고 있습니다. 이는 영국 펜스 업계에서 단순한 판매량보다 기술적 규정 준수가 더 중요하게 여겨지는 분야에서 가장 강력한 가치 확대가 나타나고 있음을 의미합니다. 또한, 영국 펜스 업계가 설치 업체에게 제품 지식과 더욱 엄격한 프로젝트 실행 기준을 모두 요구하는 용도로 나아가고 있음을 보여주고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united kingdom fencing market size is expected to increase from USD 0.92 billion in 2025 to USD 0.96 billion in 2026 and reach USD 1.19 billion by 2031, growing at a CAGR of 4.40% over 2026-2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, and Other Materials), End-User (Residential, Agricultural, and More), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (England, Scotland, Wales, and Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Fencing Market Trends and Insights

Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites

The Spending Review 2025 committed at least GBP 100 million (USD 127 million) per year by 2028-2029 through the Integrated Security Fund and raised defense capital budgets from GBP 23.2 billion (USD 29.5 billion) in 2025-2026 to GBP 33.2 billion (USD 42.2 billion) by 2029-2030, while military accommodation renewal alone received GBP 7 billion (USD 8.9 billion). That spending base matters for the United Kingdom's fencing market because perimeter systems sit within defense, prison, transport, and critical infrastructure budgets rather than relying solely on stand-alone fence replacement cycles. The same review also allocated GBP 7 billion (USD 8.9 billion) for 14,000 new prison places by 2031, which supports multi-year demand for high-specification perimeter fencing and access control around custodial sites. The June 2025 National Security Strategy made protection of critical national infrastructure a formal priority, and that is pushing procurement toward rated systems rather than lower-end perimeter products. Hill & Smith stated in its 2025 full-year results that data center demand was an important driver of perimeter security revenue, which shows that digital infrastructure is becoming a major buyer of higher-value fencing systems. This is raising specification levels across the United Kingdom fencing market and shifting value toward suppliers that can meet premium security standards with tested products and approved installation capabilities.

Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations

Private housing repair and maintenance activity strengthened during 2025 and continues to support demand in 2026, sustaining replacement and upgrade requirements for boundary products within the residential segment of the United Kingdom fencing market. Residential demand remains significant due to the country's large and aging housing stock, which drives recurring fence replacement needs even during periods of slower new housing construction. Demand growth is influenced not only by installation activity but also by homeowners increasingly favoring higher-quality, longer-warranty products over basic entry-level fencing solutions. This trend is reflected in supplier strategies, as manufacturers introduced extended-life timber and hybrid-composite product ranges during 2024 and 2025 to capture ongoing upgrade spending. As a result, revenue generated per project in the United Kingdom fencing market can increase even when overall installation volumes grow at a more moderate pace. The continued importance of the residential segment also underscores its role in shaping competitive positioning, despite the growing attention to institutional security and infrastructure-related fencing projects.

Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins

Input-cost volatility remains a key restraint for the United Kingdom fencing market in 2026, as many projects are awarded under fixed-price contracts while material costs can fluctuate throughout the delivery period. During 2025, Timber Development UK (TDUK) reported significant timber price movements, with its timber price index rising from 107 at the beginning of 2025 to 130 by mid-2025, before easing to 125 in the third quarter of 2025 and recording a further 5% correction during the fourth quarter of 2025 as supply conditions improved. Although timber prices moderated toward the end of 2025, the volatility experienced throughout the year continues to influence purchasing and bidding decisions in 2026. This challenge is particularly relevant in the United Kingdom fencing market, where smaller contractors may be reluctant to participate in public tenders when future material costs are uncertain, reducing bidding depth and potentially delaying contract awards. Cost fluctuations also favor integrated manufacturers that can manage supply chains, maintain inventory, or diversify exposure across timber, steel, and composite fencing products. Over time, this dynamic may support market-share gains for larger operators, even as overall demand conditions remain healthy in 2026.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems

- Expansion of Solar Farms Increases Utility-Scale Fencing Installations

- Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal accounted for 46% of revenue in 2025, making it the largest material category in the United Kingdom fencing market. That leadership rested on its strong position in security, perimeter protection, transport, utilities, and other applications where rated mesh, steel palisade, and durable boundary systems are standard requirements. Steel held the larger share of the metal market, while aluminum gained ground in residential and commercial settings because it combines corrosion resistance with lower lifetime maintenance costs. Metal also retained a clear edge in projects where tested security performance and structural durability mattered more than visual style. In that sense, metal continued to anchor the core of the United Kingdom fencing market, even as other materials gained in appeal.

Plastics & composites are forecast to grow at a 5.5% CAGR through 2031, making it the fastest-growing material group. The segment is benefiting from stronger sustainability requirements and from demand for products that reduce ongoing maintenance in residential and commercial projects. Supplier documentation in 2025 showed recycled-content composite systems with 15- to 25-year warranties, sharpening the cost comparison with treated timber over the product life. Wood still holds an important place in residential and agricultural fencing, but it is under pressure from higher maintenance requirements and customer interest in longer-lasting alternatives. Concrete also plays a role in boundary walls and noise-barrier applications, especially near road and rail corridors undergoing refurbishment. The Forest Research Timber in Construction Roadmap still points to policy and procurement support for wood in broader building applications, which could help wood fencing volumes where local specifications remain favorable. Even so, the United Kingdom fencing market is seeing a material growth shift toward products that offer lower upkeep and stronger sustainability positioning.

Residential accounted for 38% of revenue in 2025, making it the largest end-user segment in the United Kingdom fencing market. That scale reflects the country's broad housing base and the continued need for fence replacement, repair, and garden upgrades across existing homes. Demand is spread across all 4 nations, so the segment is not tied to one capital spending cluster or a single institutional budget cycle. Agricultural demand remained another major driver of the United Kingdom fencing market, as rural land management and livestock containment continue to require regular boundary maintenance. Military, defense, and government demand also accelerated as public spending programs lifted perimeter upgrades at prisons, military sites, and other institutional locations.

Energy & power is projected to grow at a 6.2% CAGR through 2031, which makes it the fastest-growing end-user segment in the United Kingdom fencing market. The main driver is renewable energy, especially utility-scale solar, rather than new conventional power build-out. The Cleve Hill Solar Farm example in the user input showed that a single large project can require several kilometers of perimeter fencing, and that such a site requires a higher specification than standard agricultural use. Mining, petroleum, and chemicals demand remains steadier because it depends more on existing asset maintenance than on a wave of new sites. Even when volume growth is modest, hazardous and high-security environments still support value because operators need rated perimeter solutions with integrated access control. This means the United Kingdom fencing industry is seeing some of its strongest value expansion where technical compliance matters more than simple volume. It also means the United Kingdom fencing industry is being pulled toward applications where installers need both product knowledge and tighter project execution standards.

Complete Report Scope:

- By Material

- Metal

- Steel

- Aluminium

- Wood

- Plastic & Composite

- Concrete

- Other Materials

- Metal

- By End-User

- Residential

- Agricultural

- Military & Defense

- Government

- Mining

- Petroleum & Chemicals

- Energy & Power

- Other End-Users

- By Installation Type

- Fixed / Permanent Fencing

- Temporary / Mobile Fencing

- By Installation Channel

- Professional Contractor

- Others - Fabricators, DIY / Modular Kits

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

List of Companies Covered in this Report:

- Bekaert

- Betafence

- Jacksons Fencing

- CLD Fencing Systems

- Hill & Smith Holdings

- IAE Fencing

- Zaun Limited

- Heras UK

- Fence Group

- Barkers Fencing

- Steelway Fensecure

- Alpha Rail

- Borderland Fencing

- Hadley Group

- Quickfencer

- KDM Timber

- Timber Focus

- Dura Composites

- Fencewise

- Gripple Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations

- 4.2.2 Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites

- 4.2.3 Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems

- 4.2.4 Demand for Eco-Friendly Composite Fencing Rises Across Residential and Commercial Sectors

- 4.2.5 Expansion of Solar Farms Increases Utility-Scale Fencing Installations

- 4.2.6 Smart Sensor-Integrated Fencing Adoption Grows for Advanced Security Monitoring Applications

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins

- 4.3.2 Strict Planning Permissions in Heritage and Conservation Zones Delay Fencing Projects

- 4.3.3 Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity

- 4.3.4 High Upfront Costs of Smart Fencing Limit Adoption Among SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By Geography

- 5.5.1 England

- 5.5.2 Scotland

- 5.5.3 Wales

- 5.5.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Betafence

- 6.4.3 Jacksons Fencing

- 6.4.4 CLD Fencing Systems

- 6.4.5 Hill & Smith Holdings

- 6.4.6 IAE Fencing

- 6.4.7 Zaun Limited

- 6.4.8 Heras UK

- 6.4.9 Fence Group

- 6.4.10 Barkers Fencing

- 6.4.11 Steelway Fensecure

- 6.4.12 Alpha Rail

- 6.4.13 Borderland Fencing

- 6.4.14 Hadley Group

- 6.4.15 Quickfencer

- 6.4.16 KDM Timber

- 6.4.17 Timber Focus

- 6.4.18 Dura Composites

- 6.4.19 Fencewise

- 6.4.20 Gripple Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment