|

시장보고서

상품코드

2072876

미국의 펜스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

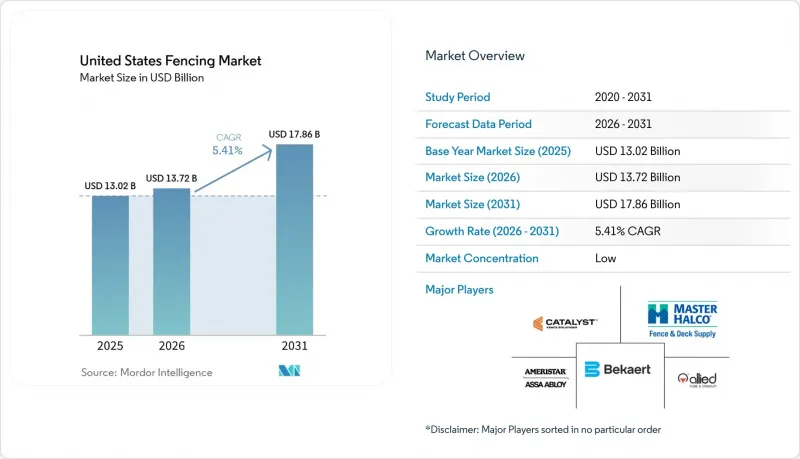

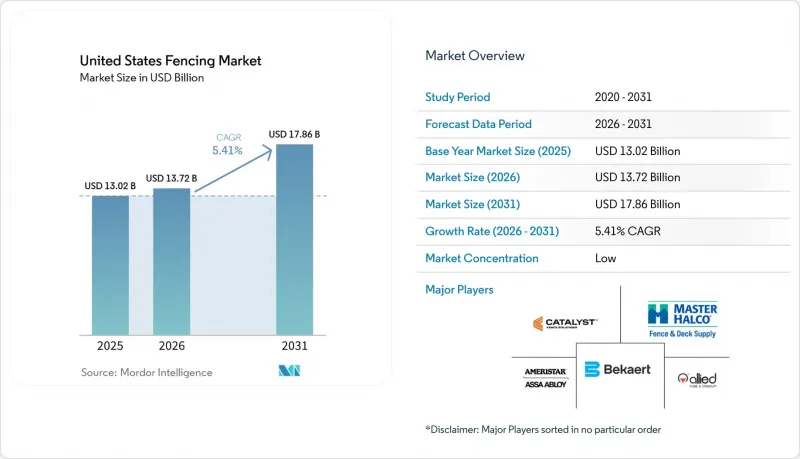

Mordor Intelligence에 의하면, 미국 펜스 시장 규모는 2025년 130억 2,000만 달러에서 2026년에는 137억 2,000만 달러로 확대되어 2026-2031년까지 CAGR 5.41%로 성장을 지속하여, 2031년에는 178억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 소재별(금속, 목재, 플라스틱·복합재, 콘크리트, 기타), 최종 사용자별(주택, 농업, 군 및 방위, 기타), 설치 유형별(고정·영구형, 일시적·이동형), 설치 채널별(전문 업체, 제조업체·DIY), 주별(텍사스주, 캘리포니아주, 플로리다주, 뉴욕주, 일리노이주, 미국 기타 지역)로 분류되어 있습니다. 예측값은 금액(달러)으로 표시되어 있습니다.

미국 펜스 시장 동향과 인사이트

교외 주택 개발 지역에서 주거용 사생활 보호 및 보안용 펜스에 대한 수요가 증가하고 있습니다.

선벨트 지역 주들의 교외 지역이 성장함에 따라, 미국에서는 주택용 펜스에 대한 견고한 수요 기반이 형성되고 있습니다. 댈러스-포트워스, 피닉스, 탬파 등의 지역에 위치한 신규 단독주택 단지에서는 펜스가 선택 사양이 아닌, 주택의 기본 사양으로 포함되는 경우가 많아지고 있습니다. 또한, 하이브리드 근무 방식의 확산으로 뒷마당 활용에 대한 관심이 높아지고 있으며, 이는 기존 주택가에서 신규 설치 수요와 교체 수요를 모두 뒷받침하고 있습니다. 많은 프로젝트에서 초기 구매 가격보다 장기적인 유지 관리가 더 중요시됨에 따라, 주택 소유자들은 비닐, 복합 소재, 분체 도장 알루미늄 제품으로 전환하고 있습니다. 또한, 급성장 중인 커뮤니티 내 주택 소유자 협회의 규정에 따라 구매자들은 승인된 디자인이나 인증된 공급업체를 선택하도록 유도되고 있으며, 이는 고부가가치 시공과 안정적인 이익률을 뒷받침하고 있습니다.

상업 및 산업 건설 분야의 성장이 주변 보안 펜스 도입을 주도하고 있습니다.

미국 펜스 시장에서 2026년에 들어서도 상업 및 산업 건설 분야의 수주 전망이 주변 보안 수요를 지속적으로 뒷받침하고 있습니다. 물류 시설, 데이터센터, 에너지 관련 자산, 제조 시설은 모두 일반적인 주거용 시스템보다 더 높은 보안 기준을 충족할 수 있는 펜스가 필요합니다. 이에 따라 비주거용 프로젝트 전반에 걸쳐 등반 방지용 강철 패널, 용접 메쉬, 충돌 방지 장벽, 통합형 게이트 시스템에 대한 수요가 증가하고 있습니다. 태양광 발전소, 배터리 저장 시설, 전기차 충전소는 특히 소유주가 물리적 보호와 접근 통제를 모두 요구하는 경우, 부지 고유의 주변 보안 요구 사항에 또 다른 차원을 더하고 있습니다. 프로젝트의 범위가 점점 더 복잡해짐에 따라, 펜스 공급업체들은 장벽, 출입 통제 지점, 감시 기능을 결합한 번들 제품을 제공해야 하는 상황에 직면하고 있습니다.

높은 인건비와 설치 비용이 펜스 프로젝트 전체 비용을 끌어올리고 있습니다.

미국 전역의 펜스 시장에서 인력 확보는 여전히 큰 운영상의 과제로 남아 있습니다. 펜스 설치, 특히 영구적인 시스템의 경우, 기둥 설치, 위치 조정, 출입구 설치, 마무리 작업 등에서 숙련된 작업자의 역할이 매우 중요합니다. 숙련된 작업 인력이 부족한 경우, 시공업체는 납기일을 연장하거나 더 높은 인건비로 입찰하게 되며, 그 결과 주택, 상업, 농업 각 분야의 프로젝트 총비용이 상승하고 있습니다. 이러한 비용 압박으로 인해, 현장에서의 작업 시간을 단축할 수 있는 모듈식 패널이나 조립이 완료된 게이트 유닛에 대한 관심이 높아지고 있습니다. 또한, 이는 업계 재편을 촉진하고 있어, 더 많은 인력을 확보할 수 있는 대형 도급업체들이 소규모 지역 기업들이 인력 확보에 어려움을 겪는 프로젝트를 수주할 수 있게 되었습니다.

부문별 분석

2025년, 금속 펜스는 미국 펜스 시장 점유율의 45.1%를 차지하며, 전체 소재 부문에서 1위를 유지했습니다. 이러한 우위는 장식적 가치보다 강도, 등반 방지 성능, 내충격성이 중시되는 산업용 경계, 군사 및 정부 관련 분야에서 나타나는 활발한 수요를 반영하고 있습니다. 농업 및 산업 분야에서는 여전히 강철이 주요 소재로 사용되고 있지만, 유지보수가 간편하고 더욱 세련된 마감이 요구되는 주택이나 소규모 상업 프로젝트에서는 알루미늄이 더 널리 사용되고 있습니다. 플라스틱 및 복합재로 제작된 펜스는 가장 빠르게 성장하고 있는 소재 부문으로, 수명 주기 전반에 걸친 유지보수 비용이 낮은 소재로 전환하는 구매자가 늘어남에 따라 2031년까지 연평균 성장률(CAGR)이 6.21%를 나타낼 것으로 전망됩니다.

복합재 공급업체들은 제품의 내구성과 프리미엄 포지셔닝을 무기로, 미국 펜스 업계에서 입지를 확대되고 있습니다. Trex는 2026년 International Builders' Show에서 아웃도어 리빙용 제품 라인업을 강조하는 한편, 복합 소재 제품의 긴 수명이라는 특징을 다시 한번 부각시켰습니다. 이는 고부가가치 주택 프로젝트에서 복합재 펜스의 매력을 입증하는 것입니다. 목재는 초기 비용을 비교적 낮게 유지할 수 있고, 또한 많은 주택 소유자가 비교적 간단한 설치 작업을 직접 수행할 수 있기 때문에 저예산 주택이나 지방에서의 설치에 있어 여전히 일정한 위치를 차지하고 있습니다. 콘크리트는 방음벽이나 높은 수준의 보안이 요구되는 경계 펜스 등의 용도에서 여전히 틈새 시장에서의 선택지로 남아 있습니다. 반면, 재생 폴리머 메쉬나 대나무와 같은 다른 소재들은 지속가능성을 중시하는 소규모 시장에 국한된 상태입니다. 이 부문에서 나타나는 주요 변화는 금속의 소멸이 아니라, 오히려 코팅 제품, 복합재료 및 수명이 긴 제품으로의 프리미엄 지향성이 꾸준히 전환되고 있다는 점에 있습니다.

2025년, 미국 펜스 시장에서 주택 최종 소비자가 38.7%를 차지하며, 주택 관련 수요가 가장 큰 최종 용도 부문이 되었습니다. 이러한 상황은 단독주택 매매, 교외 지역에서의 건축, 사생활 보호를 위한 개조, 그리고 뒷마당 정비에 대한 지출과 직접적인 관련이 있음을 반영하고 있습니다. 많은 신규 주택 소유자들은 주택을 구입한 직후 펜스를 설치하는 반면, 기존 주택 소유자들은 야외 리모델링 계획의 일환으로 노후된 펜스를 계속해서 교체하고 있습니다. 농업용 펜스는 보전 관련 설치 지원과 광대한 목축 경영에서의 스마트 전기 펜스 보급에 힘입어, 2031년까지 연평균 성장률(CAGR)이 6.34%에 달하며 가장 빠르게 성장하고 있는 최종 용도 부문입니다.

농업 분야 수요 증가가 중요한 이유는 이를 통해 미국의 펜스 시장이 소비자 주도형 수요의 범위를 넘어 확대되기 때문입니다. 미국 농무부의 보고서에 따르면, 2024년 소 사육 두수는 9,440만 마리이며, 이는 축산 시설 전반에 걸쳐 펜스가 광범위하게 설치되어 있고, 수리 및 교체를 위한 지속적인 수요가 있음을 보여줍니다. 군 및 방위 분야의 사용자들은 충격에 강한 장벽, 더 높은 등반 방지 패널, 통합 감시 시스템을 필요로 하기 때문에 여전히 중요한 프리미엄층 구매자로 남아 있습니다. 정부, 광업, 석유·화학, 에너지 및 전력 분야의 사용자들도 이러한 환경에서 펜스가 외관이 아니라 안전성과 자산 보호에 직결되기 때문에 비재량적 수요의 또 다른 층을 형성하고 있습니다. 이처럼 최종 사용자층이 폭넓다는 점은 단일 건설 분야에 의존하는 시장에 비해 미국 펜스 업계가 더 큰 회복력을 유지하는 데 도움이 되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 동향과 분석

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states fencing market size is expected to grow from USD 13.02 billion in 2025 to USD 13.72 billion in 2026 and is forecast to reach USD 17.86 billion by 2031 at 5.41% CAGR over 2026-2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Others), by End-User (Residential, Agricultural, Military & Defense, and More), by Installation Type (Fixed/Permanent, Temporary/Mobile), by Installation Channel (Professional Contractor, Fabricators/DIY), and by State (Texas, California, Florida, New York, Illinois, Rest of US). Forecasts are in Value (USD)

United States Fencing Market Trends and Insights

Increasing Demand for Residential Privacy and Security Fencing Across Suburban Housing Developments

Suburban growth across Sun Belt states has created a durable base of demand for residential fencing in the United States. New single-family communities in areas such as Dallas-Fort Worth, Phoenix, and Tampa often include fencing as standard with the property rather than an optional add-on. Hybrid work patterns have also kept attention on backyard use, which supports both first-time installations and replacement demand in established neighborhoods. Homeowners are moving toward vinyl, composite, and powder-coated aluminum because long-term upkeep matters more than initial purchase price in many projects. Homeowner association rules in fast-growing communities also steer buyers toward approved designs and certified suppliers, which supports higher-value installations and steadier margins.

Growth in Commercial and Industrial Construction Driving Perimeter Security Fencing Adoption

Commercial and industrial construction pipelines continued to support perimeter security demand entering 2026 in the United States fencing market. Logistics sites, data centers, energy assets, and manufacturing facilities all require fencing that can handle higher security standards than standard residential systems. This is lifting demand for anti-climb steel panels, welded mesh, crash-rated barriers, and integrated gate systems across nonresidential projects. Solar farms, battery storage locations, and electric vehicle charging sites are adding another layer of site-specific perimeter demand, especially where owners want both physical protection and controlled access. As project scopes become more complex, fencing suppliers are being pushed toward bundled products that combine barriers, access points, and monitoring features.

High Labor and Installation Costs Increasing Overall Fencing Project Expenses

Labor availability remains a major operating challenge across the United States fencing market. Fence installation still depends heavily on skilled crews for post setting, alignment, gate placement, and finish work, especially in permanent systems. When trained crews are scarce, installers can extend lead times and bid at higher labor rates, which pushes up total project costs across residential, commercial, and agricultural jobs. That cost pressure is encouraging more interest in modular panels and pre-assembled gate units that reduce on-site work time. It also supports consolidation, as larger contractors with better crew access can take on projects that smaller local firms may struggle to staff.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Automated and Smart Fencing Systems in High-Security Applications

- Increasing Cross-Border Migration from Neighboring Countries Driving Demand for Border Security Fencing Infrastructure

- Fluctuating Prices of Raw Materials Such as Steel, Aluminum, and Wood Impacting Product Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fencing held 45.1% of the United States fencing market share in 2025, maintaining its leading position across material categories. That lead reflects strong demand from industrial perimeter, military, and government applications where strength, anti-climb performance, and crash resistance carry more weight than decorative value. Steel remains the primary material for agricultural and industrial work, while aluminum is more commonly used in residential and light commercial projects that require lower maintenance and cleaner finishes. Plastic and composite fencing is the fastest-growing material segment, with a projected 6.21% CAGR through 2031, as more buyers move away from wood toward materials with lower lifecycle maintenance costs.

Composite suppliers are using product longevity and premium positioning to widen their role in the United States fencing industry. Trex highlighted its outdoor living portfolio and reinforced the long-life positioning of composite products at the 2026 International Builders' Show, which supports the appeal of composite fencing in higher-value residential projects. Wood still holds a place in budget residential and rural installations because its upfront cost stays lower, and many homeowners can handle simpler installation work themselves. Concrete remains a niche option for applications such as noise barriers and high-security perimeters. In contrast, other materials, such as recycled polymer mesh and bamboo, remain limited to small, sustainability-focused pockets. The main change in this segment is not the disappearance of metal, but rather the steady shift in premium toward coated, composite, and longer-life products.

Residential end users accounted for 38.7% of the United States fencing market in 2025, making housing-related demand the largest end-use segment. This position reflects the direct link between single-family housing turnover, suburban construction, privacy upgrades, and backyard improvement spending. Many new homeowners install fencing soon after purchase, while established households continue to replace aging systems as part of outdoor renovation programs. Agricultural fencing is the fastest-growing end-use segment, with a 6.34% CAGR through 2031, supported by conservation-linked installation support and by wider use of smart electric fencing across large-acreage livestock operations.

The agricultural push matters because it broadens the United States fencing market beyond consumer-led demand. The U.S. Department of Agriculture reported a cattle inventory of 94.4 million head in 2024, indicating a large installed base of fencing across livestock operations and a recurring need for repair and replacement. Military and defense users remain important premium buyers because they require crash-rated barriers, taller anti-climb panels, and integrated monitoring systems. Government, mining, petroleum and chemicals, and energy and power users add another layer of non-discretionary demand because fencing in those settings is tied to safety and asset protection rather than appearance. This spread of end users helps the United States fencing industry remain more resilient than markets tied to a single construction category.

Complete Report Scope:

- By Material

- Metal

- Steel

- Aluminium

- Wood

- Plastic & Composite

- Concrete

- Other Materials

- Metal

- By End-User

- Residential

- Agricultural

- Military & Defense

- Government

- Mining

- Petroleum & Chemicals

- Energy & Power

- Other End-Users

- By Installation Type

- Fixed / Permanent Fencing

- Temporary / Mobile Fencing

- By Installation Channel

- Professional Contractor

- Others - Fabricators, DIY / Modular Kits

- By State

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

List of Companies Covered in this Report:

- Catalyst Fence Solutions

- Master Halco

- Ameristar Perimeter Security

- Bekaert Fencing

- Allied Tube & Conduit

- Fortress Building Products

- Merchants Metals

- Gregory Industries

- Eastern Wholesale Fence

- SpecRail

- Long Fence

- Stephens Pipe & Steel

- Ultra Aluminum Mfg.

- Jamieson Fence Supply

- Jerith Manufacturing LLC

- Ametco Manufacturing

- Pexco LLC (PDS Fence Products)

- Wheatland Tube

- Sharon Fence

- Ply Gem Residential Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for residential privacy and security fencing across suburban housing developments

- 4.2.2 Growth in commercial and industrial construction driving perimeter security fencing adoption

- 4.2.3 Rising demand for automated and smart fencing systems in high-security applications

- 4.2.4 Increasing cross-border migration from neighboring countries driving demand for border security fencing infrastructure

- 4.2.5 Growing agricultural fencing needs for livestock management and land protection

- 4.2.6 Increasing focus on wildlife conservation and highway safety driving installation of wildlife fencing

- 4.3 Market Restraints

- 4.3.1 High labor and installation costs increasing overall fencing project expenses

- 4.3.2 Fluctuating prices of raw materials such as steel, aluminum, and wood impacting product costs

- 4.3.3 Strict zoning laws and local regulations limiting fencing installations in certain areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By State

- 5.5.1 Texas

- 5.5.2 California

- 5.5.3 Florida

- 5.5.4 New York

- 5.5.5 Illinois

- 5.5.6 Rest of US

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Catalyst Fence Solutions

- 6.4.2 Master Halco

- 6.4.3 Ameristar Perimeter Security

- 6.4.4 Bekaert Fencing

- 6.4.5 Allied Tube & Conduit

- 6.4.6 Fortress Building Products

- 6.4.7 Merchants Metals

- 6.4.8 Gregory Industries

- 6.4.9 Eastern Wholesale Fence

- 6.4.10 SpecRail

- 6.4.11 Long Fence

- 6.4.12 Stephens Pipe & Steel

- 6.4.13 Ultra Aluminum Mfg.

- 6.4.14 Jamieson Fence Supply

- 6.4.15 Jerith Manufacturing LLC

- 6.4.16 Ametco Manufacturing

- 6.4.17 Pexco LLC (PDS Fence Products)

- 6.4.18 Wheatland Tube

- 6.4.19 Sharon Fence

- 6.4.20 Ply Gem Residential Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment