|

시장보고서

상품코드

2072989

울혈성 심부제 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Congestive Heart Failure Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

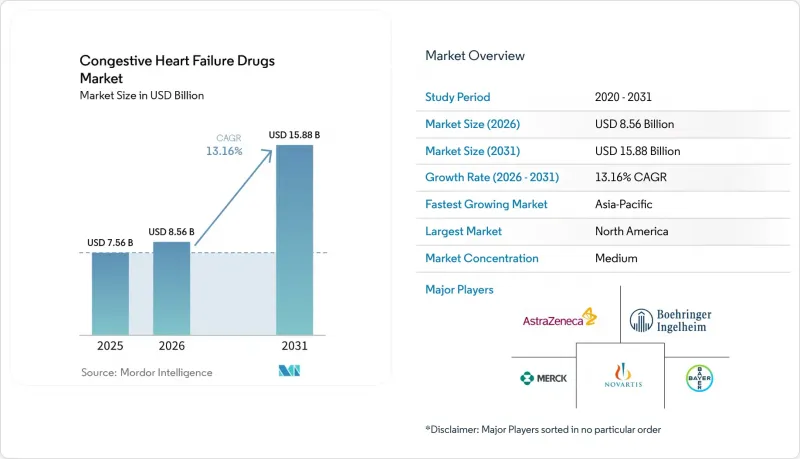

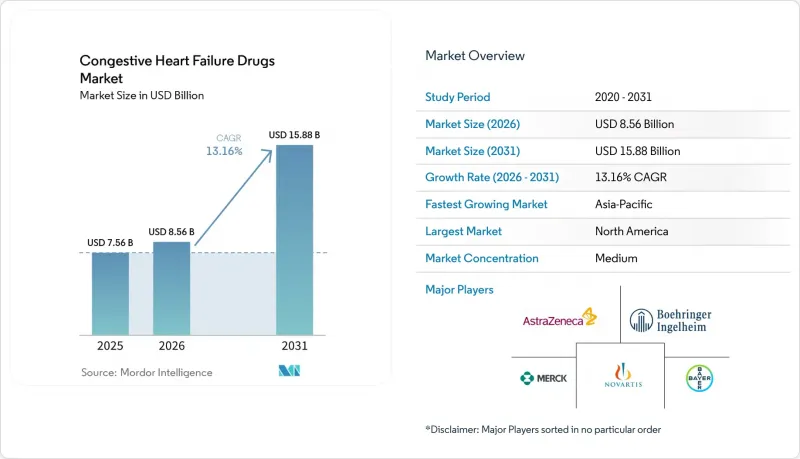

Mordor Intelligence에 의하면, 울혈성 심부제 치료제 시장 규모는 2025년에 75억 6,000만 달러로 평가되었고 2026년 85억 6,000만 달러에서 2031년까지 158억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 13.16%를 나타낼 전망입니다.

본 보고서는 약물 분류별(ACE 억제제, ARB, β-차단제, 이뇨제, 알도스테론 길항제, SGLT2 억제제, ARNI, 강심제, 기타), 투여 경로(경구, 주사제, 기타), 유통 채널(병원, 소매, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 울혈성 심부전 치료제 시장 동향 및 인사이트

심부전의 각 표현형에 대한 지침에 기반한 치료의 보급 확대

울혈성 심부전 치료제 시장은 치료 경로의 초기 단계에서 핵심적인 치료를 시작하는 치료 모델의 혜택을 받고 있습니다. 의료진은 현재 증상이 악화됨에 따라 약물을 하나씩 추가하는 방식이 아니라, 프로토콜에 기반한 병용 요법을 시행하고 있습니다. 2025년 ESC Focus Update에서는 다파글리플로진과 엠파글리플로진에 대해 HFmrEF 및 HFpEF에서 클래스 IA 지위가 인정됨에 따라, 그동안 충분한 치료를 받지 못했던 환자군의 치료 선택지가 확대되었습니다. 마찬가지로, 중국의 전문가 지침에서는 당뇨병 유무와 관계없이 증상이 있는 HFrEF 환자에게 SGLT2 억제제 사용을 권장하고 있으며, 이는 치료 접근 방식에 있어 전 세계적인 변화를 반영하고 있습니다. 이로 인해 기존의 HFrEF 환자층을 넘어 적격 환자 기반이 확대되면서 시장 성장을 주도하고 있습니다.

비만, 당뇨병, 고령화로 인한 심부전 유병률 증가

울혈성 심부전 치료제 시장은 모든 연령대 및 위험군에서 질병 부담이 증가함에 따라 확대되고 있습니다. 2024년, 전 세계적으로 8억 7,800만 명의 성인이 비만 상태이며, 높은 BMI는 심혈관 질환으로 인한 사망의 10% 가까이를 차지하고 있습니다. 2025년까지 20-79세 성인의 11.1%가 당뇨병의 영향을 받을 것으로 예상되지만, 그중 40% 이상이 진단받지 못한 상태이며, 이로 인해 치료가 지연되거나 약물 의존도가 높아지고 있습니다. 2024년 전 세계 심부전 환자 수는 5,550만 명에 달하며, 1990년 이후 2배 이상 증가했고, 특히 젊은 성인층에서 그 증가세가 두드러집니다. 발병 연령이 낮아짐에 따라 치료 기간이 길어지고, 만성적인 치료 수요가 증가하고 있어 이러한 추세가 시장 성장을 뒷받침하고 있습니다.

성숙한 의약품 군에 대한 제네릭 의약품 및 입찰에 따른 가격 압박

성숙한 치료법이 주류를 이루는 울혈성 심부전 치료제 시장은 큰 가격 압박에 직면해 있습니다. ACE 억제제, β-차단제, ARNI 계열과 같은 확립된 약물군은 제네릭 의약품과의 경쟁이 심화되면서, 환자 수는 안정적임에도 불구하고 처방 1건당 수익이 감소하고 있습니다. 이 부문의 주력 브랜드 제품인 "엔트레스트"는 2025년 3분기에 미국에서 제네릭 의약품이 시장에 출시되었습니다. 노바티스는 2026년 1분기 매출이 전년 동기 대비 42% 감소한 13억 달러를 기록했다고 보고했으며, 이로 인해 독점권 상실에 따른 급격한 매출 감소가 여실히 드러났습니다. 수량 기준 조달 시스템으로 인해 가격은 더욱 압박을 받고 있으며, 수요는 저비용 공급업체로 이동하고 있습니다. 그 결과, 기존 약물군은 대규모 환자 기반을 유지하고 있음에도 매출 성장에 기여하는 정도는 최소한에 그치는 반면, 브랜드 의약품의 성장은 신제품에 의존하는 양극화가 나타나고 있습니다.

부문별 분석

2025년, ACE 억제제는 매출의 28.60%를 차지했으며, 합리적인 가격, 폭넓은 접근성, 그리고 심부전 치료에서 확립된 역할 덕분에 주요 약물 군으로서의 위상을 유지했습니다. 이러한 우위는 가격 책정이 안정된 상황임에도 불구하고, 각국의 의약품 목록 및 임상 지침에서 오랫동안 1순위 치료제로 사용되어 온 사실을 반영하고 있습니다. ARB는 ACE 억제제에 내성이 있는 환자를 위한 대체 약물로 작용하는 반면, β-차단제는 HFrEF 치료 지침에 따른 치료에서 여전히 필수적인 역할을 하고 있습니다. 이뇨제의 처방량은 여전히 높은 수준을 유지하고 있지만, 그 가치를 높이기 위한 새로운 제형이 등장하고 있습니다. 피네레논은 미국, 유럽, 영국에서의 승인을 거쳐 적응증을 HFmrEF 및 HFpEF까지 확대함으로써, 알도스테론 길항제 범주의 정의를 새롭게 쓰고 있습니다.

울혈성 심부전 치료제 중 SGLT2 억제제 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.99%를 나타낼 것으로 예측되며, 이 기간 동안 가장 빠르게 성장하는 약물 군이 될 전망입니다. 이러한 성장은 배출률에 관한 지침에 대한 전폭적인 지지에 더해, 이미 전 세계적으로 막대한 매출을 창출하고 있는 '자디안스', 그리고 '팔키시가'의 상업적 성공에 힘입어 성장하고 있습니다. 메타분석을 통해 HFpEF 환자에서 이러한 약물의 임상적 가치가 입증되었으며, 입원 위험 감소 및 환자 예후 개선이 확인됨에 따라, 이 약물의 더 광범위한 사용이 촉진되고 있습니다.

지역별 분석

2025년, 북미는 울혈성 심부전 치료제 시장 매출의 39.52%를 차지하며 가장 큰 시장 점유율을 확보했습니다. 미국은 높은 의약품 지출, 선진적인 심혈관 의료 인프라, 그리고 주요 의료 시스템 전반에 걸친 최신 지침의 신속한 도입을 통해 이러한 우위를 주도하고 있습니다. 또한, 북미는 2025년과 2026년에 KERENDIA, AMVUTTRA, Lasix ONYU, ENBUMYST와 같은 주요 의약품을 최초로 승인한 시장이기도 합니다. 미국에서는 사큐비트릴/발살탄 제네릭 의약품 시장 진입으로 인해 브랜드 ARNI의 매출은 감소하고 있으나, 가격에 민감한 지불 주체들에 대한 접근성이 확대되면서 폭넓은 치료 보장률이 유지되고 있습니다.

유럽은 ESC(유럽심장학회)의 지침 체계와 전문의의 처방 기준에 힘입어, 울혈성 심부전 치료제 시장에서 여전히 2위의 규모를 자랑하고 있습니다. 독일과 영국은 영향력 있는 심사 제도를 통해 새로운 치료법이 승인 단계에서 보험 적용 치료로 전환되도록 촉진하고 있으므로, 도입 과정에서 주도적인 역할을 수행하고 있습니다. 2026년 3월, 영국 의약품규제청(MHRA)과 유럽집행위원회는 심부전을 앓고 있으며 좌심실 박출률(LVEF)이 40% 이상인 성인에 대한 피네레논의 승인을 결정함으로써, 비스테로이드성 MRA 계열의 성장 가능성을 높였습니다. 그러나 의료기술평가(HTA) 절차로 인해 고가 제품 시장 출시가 지연되고 있으며, 미국에 비해 보다 신중한 접근 경로가 형성되어 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 15.26%를 나타낼 것으로 예측되며, 울혈성 심부전 치료제 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 중국은 치료받지 않은 환자 수가 많고, 가격 주도형 조달 전략을 채택하고 있어 이러한 성장을 주도하고 있습니다. 이로 인해 브랜드 의약품의 가격 압박이 있음에도 불구하고, 성숙한 심혈관계 치료제에 대한 접근성이 향상되고 있습니다. 인도는 고령화, 당뇨병, 고혈압과 관련된 환자 수 증가에 기여하고 있으며, 한국은 전문 의료 네트워크를 통해 고품질 치료법의 도입을 뒷받침하고 있습니다. 일본은 꾸준한 성장세를 보이고 있으며, 남미, 중동 및 아프리카는 도시 지역의 고령화, 심혈관 센터의 확대, 그리고 보험 지급 체계 개선의 혜택을 받는 신흥 시장으로 부상하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the congestive heart failure drugs market size was valued at USD 7.56 billion in 2025 and is estimated to grow from USD 8.56 billion in 2026 to reach USD 15.88 billion by 2031, at a CAGR of 13.16% during the forecast period (2026-2031).

This report is Segmented by Drug Class (ACE Inhibitors, Arbs, Beta Blockers, Diuretics, Aldosterone Antagonists, SGLT2 Inhibitors, Arnis, Inotropes, Others), Route of Administration (Oral, Injectable, Others), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Congestive Heart Failure Drugs Market Trends and Insights

Expanding Guideline-Directed Therapy Adoption Across HF Phenotypes

The market for congestive heart failure drugs is benefiting from a treatment model that initiates core therapies earlier in the care pathway. Care teams now implement protocol-led combinations instead of adding medications one at a time as symptoms worsen. The 2025 ESC Focus Update granted dapagliflozin and empagliflozin Class IA status for HFmrEF and HFpEF, broadening treatment options for previously underserved patient groups. Similarly, Chinese expert guidance endorsed SGLT2 inhibitors for symptomatic HFrEF patients regardless of diabetes status, reflecting a global shift in treatment approaches. This has expanded the eligible patient base beyond the traditional HFrEF population, driving market growth.

Rising Heart Failure Prevalence Driven By Obesity, Diabetes, and Aging

The congestive heart failure drugs market is growing due to an increasing disease burden across age groups and risk profiles. In 2024, global obesity affected 878 million adults, with high BMI contributing to nearly 10% of cardiovascular deaths. By 2025, diabetes impacted 11.1% of adults aged 20-79, with over 40% of cases undiagnosed, leading to delayed treatment and higher drug dependency. Global heart failure prevalence reached 55.50 million cases in 2024, more than doubling since 1990, with a notable rise among younger adults. This trend supports market growth as earlier disease onset extends treatment duration and chronic therapy needs.

Generic And Tender Pressure On Mature Drug Classes

The congestive heart failure drugs market, dominated by mature therapies, faces significant pricing pressures. Established classes like ACE inhibitors, beta blockers, and the ARNI class are under growing generic competition, reducing revenue per prescription despite stable patient volumes. Entresto, the leading branded product in this segment, experienced U.S. generic entry in Q3 2025. Novartis reported a 42% year-on-year revenue decline to USD 1.3 billion in Q1 2026, highlighting the rapid revenue erosion following the loss of exclusivity. Volume-based procurement systems further compress prices and shift demand to low-cost suppliers, creating a divide where older drug classes retain large patient bases but contribute minimally to revenue growth, while branded growth relies on newer products.

Other drivers and restraints analyzed in the detailed report include:

- Approval Momentum For New Indications In HFmrEF And HFpEF

- Growth Of Home-Based And Outpatient Congestion Management

- Reimbursement Friction For Newer Therapies In Value-Based Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ACE inhibitors accounted for 28.60% of revenue, maintaining their position as the leading drug class due to their affordability, widespread availability, and established role in heart failure care. Their dominance reflects long-standing first-line use in national formularies and clinical guidelines, despite mature pricing. ARBs serve as alternatives for patients intolerant to ACE inhibitors, while beta blockers remain essential in guideline-directed therapy for HFrEF. Diuretics continue to see high prescription volumes, though newer delivery formats aim to enhance their value. Finerenone is redefining the aldosterone antagonist category by extending its use to HFmrEF and HFpEF after approvals in the U.S., Europe, and the UK.

The SGLT2 inhibitors market for congestive heart failure drugs is projected to grow at a 14.99% CAGR from 2026 to 2031, making it the fastest-growing drug class during this period. Growth is driven by full guideline support for ejection fraction and the commercial success of Jardiance and Farxiga, which already generate significant global revenues. A meta-analysis reinforced their clinical value in HFpEF, showing reduced hospitalization risks and improved patient outcomes, supporting broader adoption.

Complete Report Scope:

- By Drug Class

- ACE Inhibitors

- Angiotensin 2 Receptor Blockers

- Beta Blockers

- Diuretics

- Aldosterone Antagonists

- SGLT2 Inhibitors

- Angiotensin Receptor-Neprilysin Inhibitors

- Inotropes

- Other Drug Classes

- By Route of Administration

- Oral

- Injectable

- Other Routes of Administration

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 39.52% of the congestive heart failure drugs market revenue, securing the largest market share. The U.S. drives this dominance with high drug spending, advanced cardiology infrastructure, and rapid adoption of updated guidelines across major healthcare systems. It was also the first market to approve key drugs in 2025 and 2026, including KERENDIA, AMVUTTRA, Lasix ONYU, and ENBUMYST. While generic sacubitril/valsartan entry in the U.S. is reducing branded ARNI revenue, it is expanding access for price-sensitive payers, maintaining broad treatment coverage.

Europe remains the second-largest region in the congestive heart failure drugs market, supported by the ESC guideline framework and specialist prescribing standards. Germany and the UK lead in adoption due to their influential review systems, which facilitate the transition of new therapies from approval to reimbursed care. In March 2026, the UK MHRA and the European Commission approved finerenone for adults with heart failure and LVEF of 40% or more, boosting the growth potential of the nonsteroidal MRA class. However, health technology assessment processes slow the rollout of premium products, creating a more measured access path compared to the U.S.

Asia-Pacific is projected to grow at a 15.26% CAGR from 2026 to 2031, making it the fastest-growing region in the congestive heart failure drugs market. China drives this growth with its large untreated population and price-led procurement strategies, which enhance access to mature cardiovascular drugs despite branded price pressures. India contributes with a growing patient base linked to aging, diabetes, and hypertension, while South Korea supports premium therapy adoption through its specialist care network. Japan shows steady growth, while South America, the Middle East, and Africa are emerging markets benefiting from urban aging, expanding cardiovascular centers, and improved reimbursement frameworks.

- Abbott Laboratories

- Alnylam Pharmaceuticals

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Eli Lilly and Company

- GlaxoSmithKline

- Johnson & Johnson

- Lexicon Pharmaceuticals, Inc.

- Merck

- Novartis

- Novo Nordisk

- Otsuka

- Pfizer

- Sanofi

- SQ Innovation, Inc.

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Guideline-Directed Therapy Adoption Across Ejection-Fraction Segments

- 4.2.2 Rising Heart Failure Prevalence Driven by Obesity, Diabetes, and Chronic Kidney Disease

- 4.2.3 Earlier Diagnosis and Longer Treatment Duration in Chronic Heart Failure

- 4.2.4 Approval Momentum for New Indications in HFmrEF And HFpEF

- 4.2.5 Shift Toward Multi-Drug, Long-Term Maintenance Regimens

- 4.2.6 Growth of Home-Based and Outpatient Congestion Management Therapies

- 4.3 Market Restraints

- 4.3.1 Generic and Tender Pressure on Mature Drug Classes

- 4.3.2 Safety Concerns, Tolerability Limits, and Dose-Optimization Complexity

- 4.3.3 High Monitoring Burden for Patients With Multi-Morbidity

- 4.3.4 Reimbursement Friction for Newer Therapies in Value-Constrained Markets

- 4.4 Value/ Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Drug Class

- 5.1.1 ACE Inhibitors

- 5.1.2 Angiotensin 2 Receptor Blockers

- 5.1.3 Beta Blockers

- 5.1.4 Diuretics

- 5.1.5 Aldosterone Antagonists

- 5.1.6 SGLT2 Inhibitors

- 5.1.7 Angiotensin Receptor-Neprilysin Inhibitors

- 5.1.8 Inotropes

- 5.1.9 Other Drug Classes

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.2.3 Other Routes of Administration

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Alnylam Pharmaceuticals, Inc.

- 6.3.3 Amgen Inc.

- 6.3.4 AstraZeneca PLC

- 6.3.5 Bayer AG

- 6.3.6 Boehringer Ingelheim International GmbH

- 6.3.7 Bristol-Myers Squibb Company

- 6.3.8 Eli Lilly and Company

- 6.3.9 GSK plc

- 6.3.10 Johnson and Johnson

- 6.3.11 Lexicon Pharmaceuticals, Inc.

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Novartis AG

- 6.3.14 Novo Nordisk A/S

- 6.3.15 Otsuka Pharmaceutical Co., Ltd.

- 6.3.16 Pfizer Inc.

- 6.3.17 Sanofi S.A.

- 6.3.18 SQ Innovation, Inc.

- 6.3.19 Teva Pharmaceutical Industries Ltd.

- 6.3.20 Viatris Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment