|

시장보고서

상품코드

2073055

흉부외과 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thoracic Surgery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

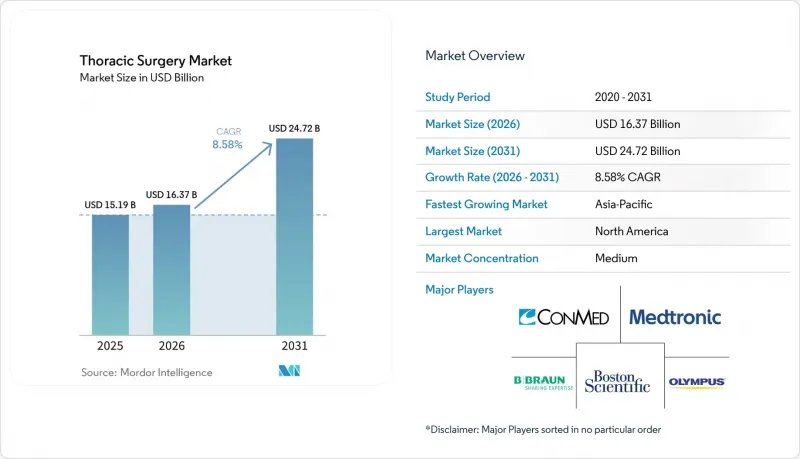

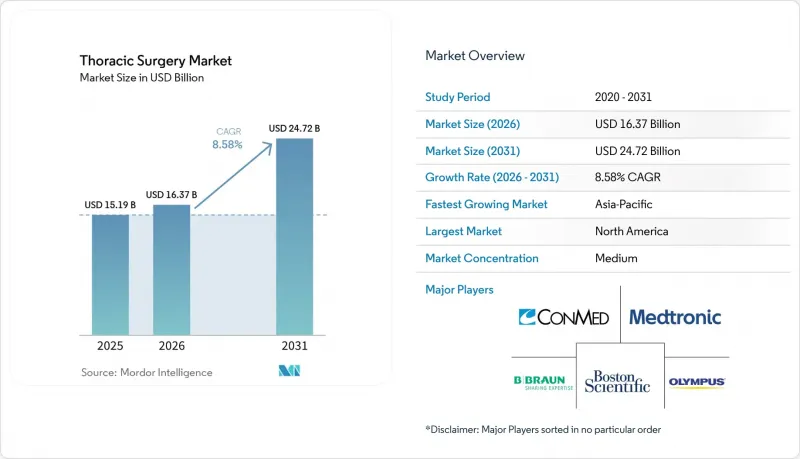

Mordor Intelligence에 의하면, 흉부외과 시장 규모는 2025년 151억 9,000만 달러에서 2026년에는 163억 7,000만 달러로 확대되어 2026-2031년까지 CAGR 8.58%로 성장을 지속하여, 2031년에는 247억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 및 서비스(수술 기구, 기타), 수술 유형(개흉술, 기타), 수술 유형(폐엽 절제술, 기타), 질환(폐암, 기타), 환자 유형(입원 환자, 외래 환자), 수술 접근법(저침습 수술, 기타), 수술 범위, 최종 사용자, 지역(북미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 흉부외과 시장 동향 및 인사이트

증가하는 흉부 질환의 부담

흉부외과 시장은 암 치료, 응급 의료, 병원에서 이루어지는 복잡한 치료에 걸쳐 지속적으로 수요를 창출하는 질환 구성에 힘입어 성장하고 있습니다. 2025년에 발표된 GLOBOCAN 조사 결과에 따르면, 2022년에는 기관·기관지·폐암의 신규 환자가 248만 건, 사망자 수가 182만 명에 달했으며, 이로 인해 폐절제술 건수는 치료 경로에서 여전히 중심적인 위치를 차지하고 있습니다. 이 조사에 따르면, 남성의 폐암 신규 환자 수는 2050년까지 160만 건에서 295만 건으로 증가할 것으로 예상되는 반면, 여성의 환자 수는 같은 기간 동안 83.3% 증가할 것으로 예측됩니다. 식도암 역시 수요를 더욱 끌어올리는 요인이 되고 있습니다. 2022년에는 전 세계적으로 51만 1,054건의 신규 확진자와 44만 5,391명의 사망자가 기록되었으며, 그 중 75%가 아시아에 집중되어 있었기 때문입니다. 또한, 흉부외과 시장은 기흉, 농흉, 종격동 질환 등의 영향도 지속적으로 받고 있으며, 이로 인해 종양학 부문뿐만 아니라 수술 수요도 활발하게 유지되고 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 병원은 단일한 성장 요인에 대응하는 것이 아니라, 모두 수술실 시간, 기구, 영상 진단 지원, 숙련된 팀이 필요한 여러 질환 분야에 대응하고 있는 셈입니다.

저침습 흉부외과 수술로의 전환

흉부외과 시장은 대규모 의료기관에서 임상 실무가 더 이상 개흉술에만 국한되지 않음에 따라, 저침습 치료로 더욱 전환되고 있습니다. 30만 1,123건의 종양성 폐절제술을 대상으로 한 전미 암 데이터베이스 분석에 따르면, 미국에서는 2019년까지 RATS(로봇 보조 흉강경 수술)의 사례 수가 VATS(영상 보조 흉강경 수술)를 넘어섰으며, 2021년까지 RATS는 최소 침습 수술 전체의 65.4%를 차지하게 되었습니다. 이러한 변화가 중요한 이유는 외과의사들이 단순히 로봇 수술 도구를 시험해 보는 데 그치지 않고, 주요 의료 시장에서 일상적인 환자 선정 과정의 일환으로 이를 도입하고 있음을 보여주기 때문입니다. 대학 부속 병원은 지역 병원보다 도입을 더 빠르게 추진하고 있으며, 대도시의 병원은 지방 병원보다 도입을 더 빠르게 추진하고 있는데, 이는 가격 및 연수와 관련된 장벽이 완화됨에 따라 이러한 보급 양상이 지속될 수 있음을 시사합니다. 밀라노의 ATS가 2026년에 실시한 다기관 공동 코호트 연구에 따르면, RATS는 회복이나 수술 방법 변경과 같은 수술 전후 결과 측면에서 VATS보다 우수한 것으로 밝혀졌습니다. 이로 인해 주요 교육 병원 이외의 곳에서도 도입이 더욱 촉진되고 있습니다. 따라서 흉부외과 시장이 변화하고 있는 것은 단순히 기기가 새로워졌기 때문만이 아니라, 병원 측이 더 광범위한 사용을 뒷받침하는 임상적 근거를 무시하기 어려워지고 있기 때문이기도 합니다.

고도 흉부 수술 시스템의 높은 비용

흉부외과 시장은 여전히 도입에 있어 큰 장벽에 직면해 있습니다. 그 이유는 첨단 로봇 시스템에는 많은 병원이 쉽게 감당하기 어려운 수준의 설비 투자가 필요하기 때문입니다. 플랫폼 도입 비용은 시스템당 150만-300만 달러로 변함없으며, 연간 유지보수비와 소모품비가 운영 비용에 추가로 15만-30만 달러가 더해지고 있습니다. 『Annals of Esophagus』 저널의 2024년 총설에 따르면, 로봇 보조 저침습 식도 절제술의 직접적인 수술 비용은 로봇을 사용하지 않는 기존 방식에 비해 9% 더 높은 것으로 밝혀졌습니다. 해당 리뷰에서는 현재의 보상 제도 하에서 외래 환자 대상 로봇 수술이 경제적으로 불리하다는 점도 지적하고 있으며, 이것이 소규모 의료기관들이 여전히 플랫폼 소유를 정당화하는 데 어려움을 겪고 있는 이유를 보여줍니다. 이로 인해 수술 건수가 많은 대학병원은 발전하는 반면, 수술 건수가 적은 의료기관은 비용 문제로 인해 VATS나 개흉 수술에 계속 의존하게 되는 ‘ 양극화”라는 경향이 나타나고 있습니다. 가격 책정 모델, 임대 계약 또는 플랫폼 공유를 통해 중규모 병원의 부담이 줄어들지 않는 한, 이러한 상황에서는 흉부외과 시장이 서서히만 확대될 것으로 보입니다.

부문별 분석

2025년에는 제품이 매출의 68.13%를 차지했는데, 이는 흉부외과 시장이 여전히 단일 서비스 분야가 아니라 의료기기, 수술 기구, 수술용 소모품에서 가치의 대부분을 창출하고 있음을 보여줍니다. 개흉 수술과 최소 침습 수술 모두에서 흉부 절제술 시 스테이플러, 에너지 장치, 글라스파, 견인 기구를 반복적으로 사용해야 하므로, 수술 기구와 부속품이 이러한 상황을 뒷받침하고 있습니다. 에너지 장치와 스테이플러는 표준 폐엽 절제술의 경우에도 한 번의 수술 중에 여러 차례의 연속적인 발사 및 밀봉 과정을 수반할 수 있기 때문에 여전히 특히 중요한 역할을 하고 있습니다. 또한, 4K 영상, 형광 보조, 영상 유도 기반 식별 기능이 수술 계획 및 수술 수행에 점점 더 통합됨에 따라 내시경 및 영상 시스템의 가치도 높아지고 있습니다. 2025년 4월, 인튜이티브 서지컬은 싱글포트 로봇 수술용으로 설계된 완전 가동식 스테이플러 ‘SP SureForm 45”가 FDA 승인을 획득함에 따라, 이 제품 분야의 전략을 한층 더 확대했습니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 8.78%를 나타낼 것으로 예측되며, 흉부외과 시장 규모 내에서 가장 빠르게 확대되고 있는 부문입니다. 이러한 추세는 수술 전 계획, 수술 중 내비게이션, 수술 후 모니터링, 원격 상담, 체계적인 교육 지원으로의 착실한 전환을 반영하고 있습니다. 병원 측은 치료의 편차를 줄이고, 수술실 회전율을 높이며, 외과 의사가 업무 혼란을 최소화하면서 첨단 업무 흐름을 도입할 수 있도록 지원하는 서비스에 대해 보다 적극적으로 비용을 지불하려는 태도를 보이고 있습니다. 이러한 변화에서 훈련은 특히 중요한 요소입니다. 왜냐하면 로봇 수술의 새로운 적응증이 추가될 때마다, 본격적인 도입에 앞서 자격 인증, 시뮬레이션, 시술 지원에 대한 상업적 수요가 발생하기 때문입니다. 따라서 흉부외과 분야에서는 서비스 수익이 기존 비즈니스 모델의 범위를 벗어나기보다는 의료기기 판매에 가까워지는 경향이 나타나고 있습니다. 시간이 지남에 따라, 이로 인해 과거에는 주로 장비 설치나 소모품 사용에 의존하던 공급업체들에게 지속적인 지원 수익의 중요성이 커지고 있습니다.

2025년 현재, VATS(흉강경 수술)는 흉부외과 시장 점유율의 49.21%를 차지하고 있으며, 이는 흉부외과 시장이 여전히 광범위한 외과의사층으로부터 지지를 받고 있는 확립된 저침습 수술법에 크게 의존하고 있음을 뒷받침합니다. 이러한 우위는 대중에게 친숙하다는 점, 확고한 임상적 근거, 그리고 아직 첨단 로봇 수술 기능을 갖추지 않은 수술실과의 호환성에 의해 뒷받침되고 있습니다. 유착이 심한 사례, 해부학적 구조가 불안정한 사례, 또는 응급으로 병변을 제어해야 하는 사례 등 특정 경우에는 여전히 개흉 수술이 필요하지만, 한편 내시경 흉부 수술은 기관지경 검사를 통한 진단 및 병변의 조기 검체를 채취하는 데 계속해서 기여하고 있습니다. 이러한 경향은 수술법 선택이 단일한 보편적 기준에 따르는 것이 아니라, 여전히 증례의 복잡성, 인력 구성, 인프라, 예산에 좌우되고 있음을 보여줍니다. 수술 계획의 초점은 이미 바뀌기 시작했습니다.

RATS는 2031년까지 연평균 성장률(CAGR) 10.42%를 나타낼 것으로 예측되며, 이 수술 부문에서 가장 강력한 성장 동력으로 자리매김하고 있습니다. 미국 암 데이터베이스(NCDB)의 연구에 따르면, RATS는 2019년까지 미국 내 시술 건수에서 VATS를 추월했으며, 2021년까지 최소 침습 폐 종양 절제술의 65.4%를 차지하게 되었습니다. 또한, 2026년 밀라노에서 실시된 다기관 공동 연구에서도 회복 및 수술법 변경과 같은 결과 측면에서 RATS가 VATS보다 수술 전후 관리에 있어 이점이 있는 것으로 밝혀졌습니다. 병원들은 특히 복잡한 절제술의 경우, 로봇 수술 도입 확대를 임상적·경제적 판단으로 간주하게 되면서, 흉부외과 시장은 이러한 근거에 반응하고 있습니다. 따라서 흉부외과 분야에서는 VATS가 여전히 수술 건수의 기반을 이루고 있는 반면, RATS는 수술비 지출 측면에서 고성장 및 고부가가치 방향을 형성하는 단계에 접어들고 있습니다.

2025년에는 폐엽 절제술이 수익의 61.16%를 차지하며, 이 수술 구성에서 주도적인 위치를 차지할 뿐만 아니라 흉부외과 시장 규모의 주요 축이 되고 있습니다. 1기 및 2기 비소세포폐암의 대부분에서 폐엽절제술이 여전히 표준 치료법으로 자리 잡고 있기 때문에 이 부문은 지배적인 위치를 유지하고 있습니다. 2024년 『Journal of CardIoThoracic Surgery』지에 게재된 연구에 따르면, 폐엽 절제술에서 VATS는 RATS와 동등한 장기 생존율을 보이는 것으로 밝혀졌으며, 이는 확립된 흉강경 수술 프로토콜을 통해 수술 건수가 계속해서 높은 수준을 유지하고 있음을 뒷받침합니다. 쐐기형 절제술과 분절 절제술은 조기 병변이나 선택적 해부학적 보존에 있어 여전히 중요하며, 한편 흉막 절제술은 흉막 질환이나 재발성 기흉에서 여전히 중요한 역할을 하고 있습니다. 이는 가장 규모가 큰 수술 유형이 널리 보급되어 있을 뿐만 아니라, 병원 진료 현장에 이미 확고하게 자리 잡은 임상 프로토콜과 밀접한 관련이 있음을 의미합니다.

폐전적출술은 절대적인 사례 수는 폐엽절제술이나 쐐기형 절제술보다 적지만, 2031년까지 연평균 성장률(CAGR) 9.83%로 증가할 것으로 예측됩니다. 이러한 성장률은 보다 소규모의 절제술이 불가능한 상황에서 여전히 복잡하고 국소 진행성 질환이 존재한다는 사실을 반영하고 있습니다. 2024년 연구에 따르면, 저침습 폐전절제술은 해당 의료기관 전체 사례의 27%를 차지했으며, 그중 19%는 VATS(흉강경 하 폐전절제술), 8%는 RATS(경항문적 흉강경 하 폐전절제술)로 시행되었습니다. 이는 매우 복잡한 절제술조차도 침습성이 적은 방식으로 전환되기 시작하고 있음을 보여줍니다. 또한, 이러한 수술에서는 주요 혈관의 절단이나 광범위한 스테이플링이 일반적이기 때문에 사례당 의료기기 사용량도 많아지고 있습니다. 따라서 흉부외과 시장에서 폐절제술은 수술 건수에 비해 불균형할 정도로 큰 수익 기여를 하고 있습니다. 이는 수술의 복잡성이 높아질수록 기구의 사용 빈도와 플랫폼의 가치가 모두 높아지기 때문입니다.

지역별 분석

2025년, 북미는 흉부외과 시장 점유율의 39.03%를 차지하며, 매출 측면에서 계속해서 가장 규모가 큰 지역별 기여 요인으로 자리매김했습니다. 이 지역은 성숙한 보험 환급 제도, 학술적 흉부외과 센터의 밀집, 로봇 수술 및 흉강경 수술 인프라에 대한 폭넓은 접근성이라는 장점을 갖추고 있습니다. 또한, 폐 질환 및 식도 질환에 대한 체계화된 치료 모델에서 진단, 수술, 수술 후 경과 관리를 연계하는 측면에서도 다른 지역보다 앞서 있습니다. 이는 이 지역의 성장이 단순히 질병 발생률 증가라기보다는 수술 기법의 고도화와 의료 제공 환경의 변화에 의해 형성되고 있음을 의미합니다. 북미의 흉부외과 시장이 여전히 중요한 이유는 신기술이 다른 대부분의 지역보다 더 빨리 상업적 규모에 도달하는 경향이 있기 때문입니다.

유럽은 여전히 2위 지역 블록이며, 사용자가 제출한 초안에서는 독일, 영국, 프랑스가 주도적인 역할을 하고 있습니다. 독일에서는 로봇 흉강경 수술이 지속적으로 확대되고 있으며, 하이델베르크 대학병원은 전국적인 폐암 검진 준비의 일환으로 2025년 3월부터 로봇 보조 기관지 내시경 검사를 시작했습니다. 프랑스 PMSI 행정 데이터베이스의 2026년 조사에 따르면, 2021년부터 2022년까지 로봇 수술로 인한 입원 건수는 전년 대비 15.6% 증가했으며, 흉부 외과 수술은 전국 로봇 수술 전체의 7%를 차지하고 있습니다. EU의 MDR 2017/745에 따른 규제 준수 요건은 이미 강력한 인증 역량과 시판 후 지원 체계를 갖추고 있는 기업들에게 계속해서 유리하게 작용하고 있습니다. 따라서 유럽의 흉부외과 시장은 기술 도입이 순조롭게 진행되고 있는 반면, 소규모 신규 진출기업의 진출을 지연시킬 가능성이 있는 규제 환경이 공존하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.92%를 기록하며 성장할 것으로 예상되며, 흉부외과 시장 규모 측면에서 가장 빠른 지역적 확장이 전망됩니다. 중국은 주요 성장 동력이 되고 있습니다. 사용자가 제공한 초안에 따르면, 외과용 로봇의 조달액은 2025년 1분기에 6억 9,100만 위안(9,500만 달러 상당)에 달했으며, 이는 전년 동기 대비 43% 증가한 수치입니다. 국내 제조업체들은 수입품 가격의 50-70% 수준에 시스템을 제공함으로써 시장 점유율을 확대하고 있으며, 이로 인해 사용자 제공 초안에서 주요 도시의 병원 이외의 곳에서도 시스템 도입이 촉진되고 있습니다. 인도에서는 사용자가 제출한 초안에서 의료보험의 적용 범위가 확대됨에 따라, 암 수술 건수가 증가할 여지가 커지고 있습니다. 한편, 일본에서는 사용자가 제출한 초안에서 로봇 보조 폐엽 절제술에 대한 보험 급여 지원이 확대되었습니다. 남미, 중동 및 아프리카는 여전히 소규모 시장이지만, 브라질, 사우디아라비아, 아랍에미리트의 민간 병원 그룹들은 차별화 전략의 일환으로 흉부 로봇 수술을 도입하고 있습니다. 한편, 아프리카 일부 지역에서는 인력 부족이 지속되면서 대상 수술 건수의 확대를 계속해서 제한하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the thoracic surgery market size is expected to grow from USD 15.19 billion in 2025 to USD 16.37 billion in 2026 and is forecast to reach USD 24.72 billion by 2031 at 8.58% CAGR over 2026-2031.

This report is Segmented by Product and Services (Surgical Instruments, and More), Procedure Type (Open, and More), Surgery Type (Lobectomy, and More), Medical Condition (Lung Cancer, and More), Patient Type (Inpatients, Outpatients), Surgical Approach (Minimally Invasive, and More), Surgical Scope, End User, and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Thoracic Surgery Market Trends and Insights

Rising Thoracic Disease Burden

The thoracic surgery market is being supported by a disease mix that continues to generate demand across cancer care, emergency care, and complex hospital-based treatment. GLOBOCAN findings published in 2025 reported 2.48 million incident tracheal, bronchial, and lung cancer cases and 1.82 million deaths in 2022, which keeps lung resection volumes central to the care pathway. The same study showed that male incident lung cancer cases are projected to rise from 1.6 million to 2.95 million by 2050, while female cases are projected to increase 83.3% over the same period. Esophageal cancer adds another layer of demand because 511,054 new cases and 445,391 deaths were recorded globally in 2022, and 75% of cases were concentrated in Asia. The thoracic surgery market also remains exposed to pneumothorax, empyema, and mediastinal disease, which keeps surgical workloads active beyond oncology alone. This combination means hospitals are not dealing with a single source of growth, but with several disease pathways that all require operating room time, instruments, imaging support, and trained teams.

Shift Toward Minimally Invasive Thoracic Surgery

The thoracic surgery market is moving further toward minimally invasive care because clinical practice is no longer centered only on open thoracotomy in large referral centers. A National Cancer Database analysis covering 301,123 oncologic lung resections showed that RATS exceeded VATS case volume in the United States by 2019, and by 2021 RATS represented 65.4% of all minimally invasive cases. That change matters because it shows surgeons are not only trying robotic tools, but are making them part of routine case selection in a major care market. Academic programs have moved faster than community centers, and metropolitan hospitals have moved faster than rural hospitals, which points to a diffusion pattern that can continue as pricing and training barriers ease. A 2026 multicenter cohort study from the ATS of Milan found that RATS delivered perioperative advantages over VATS in recovery and conversion outcomes, which strengthens adoption beyond flagship teaching hospitals. The thoracic surgery market is therefore shifting not only because the tools are newer, but because the clinical case for broader use has become harder for hospitals to ignore.

High Cost of Advanced Thoracic Systems

The thoracic surgery market still faces a major adoption ceiling because advanced robotic systems demand a capital outlay that many hospitals cannot absorb easily. Platform acquisition costs remain at USD 1.5-3 million per system, and annual maintenance plus consumables add another USD 150,000-300,000 to the operating burden. A 2024 review in the Annals of Esophagus found that robotic-assisted minimally invasive esophagectomy carried 9% higher direct surgical costs than non-robotic alternatives. The same review noted that outpatient robotic procedures were financially unfavorable under current reimbursement structures, which shows why smaller providers still struggle to justify platform ownership. This creates a two-speed pattern where high-volume academic hospitals move ahead, while lower-volume centers continue to rely on VATS or open surgery for cost reasons. The thoracic surgery market can widen only gradually under these conditions, unless pricing models, leasing arrangements, or shared platform access reduce the burden on mid-tier hospitals.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Robotics and Image Guidance

- Expansion of Ambulatory Thoracic Care Pathways

- Shortage of Skilled Thoracic Surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Product held 68.13% of revenue in 2025, which shows that the thoracic surgery market still draws most of its value from equipment, instruments, and procedural consumables rather than stand-alone service lines. Surgical instruments and accessories support this position because thoracic resections require repeated use of staplers, energy devices, graspers, and retraction tools across open and minimally invasive cases. Energy and stapling devices remain especially important because even a standard lobectomy can involve several sequential firing and sealing steps in one operation. Endoscopes and imaging systems are also moving higher in value as 4K visualization, fluorescence support, and image-led identification features become more integrated into operative planning and execution. In April 2025, Intuitive Surgical expanded this product-side logic through FDA clearance of the SP SureForm 45, a fully wristed stapler built for single-port robotic surgery.

Services are projected to grow at 8.78% CAGR through 2031, which makes this the fastest-moving side of the thoracic surgery market size within this segmentation. That pace reflects a steady shift toward preoperative planning, intraoperative navigation, postoperative monitoring, teleconsultation, and structured training support. Hospitals are showing more willingness to pay for services that reduce variation, shorten room turnover, and help surgeons adopt advanced workflows with fewer disruptions. Training is a notable part of that change because each new robotic indication creates a commercial need for credentialing, simulation, and procedural support before full-scale rollout. The thoracic surgery industry is therefore seeing service revenue move closer to the device sale, rather than sitting outside the commercial model. Over time, this makes recurring support income more important to vendors that once depended mainly on capital placement and disposable usage.

VATS held 49.21% of the thoracic surgery market share in 2025, which confirms that the thoracic surgery market still relies heavily on an established minimally invasive technique with a broad surgeon base. Its lead is supported by familiarity, a strong clinical evidence base, and compatibility with operating rooms that do not yet have advanced robotic capacity. Open surgery remains necessary in selected cases with dense adhesions, unstable anatomy, or urgent control requirements, while endoscopic thoracic surgery continues to support bronchoscopy-driven diagnosis and early lesion sampling. These patterns show that procedure choice still depends on case complexity, staffing, infrastructure, and budget rather than a single universal standard. Even so, the center of gravity in procedure planning has started to move.

RATS is forecast to grow at 10.42% CAGR through 2031, which makes it the strongest growth engine in this procedure mix. A National Cancer Database study showed that RATS overtook VATS in U.S. case count by 2019, and by 2021 it represented 65.4% of minimally invasive oncologic lung resections. A 2026 multicenter study from Milan also found perioperative advantages for RATS over VATS in recovery and conversion outcomes. The thoracic surgery market is reacting to this evidence because hospitals can now frame robotic expansion as both a clinical and economic decision, especially in complex resections. The thoracic surgery industry is therefore entering a period where VATS remains the volume base, but RATS shapes the higher-growth and higher-value direction of procedural spending.

Lobectomy held 61.16% of revenue in 2025, which gives it the leading position in this surgery mix and makes it a major anchor of the thoracic surgery market size. The segment stays dominant because lobar resection remains standard care for a large share of stage I and II non-small cell lung cancer. A 2024 study in the Journal of Cardiothoracic Surgery found that VATS can deliver long-term survival outcomes comparable to RATS in lobectomy, which supports continued high procedural volume through established thoracoscopic pathways. Wedge resection and segmental resection remain important for earlier lesions and selective anatomical preservation, while pleurectomy stays relevant in pleural disease and recurrent pneumothorax. This means the largest surgery type is not only widespread, but also linked to clinical pathways that are already well embedded in hospital practice.

Pneumonectomy is projected to grow at 9.83% CAGR through 2031, even though absolute case volume remains lower than lobectomy and wedge procedures. Its growth rate reflects the fact that complex and locally advanced disease still presents in settings where lesser resections are not possible. A 2024 study reported that minimally invasive pneumonectomy reached 27% of institutional cases, including 19% by VATS and 8% by RATS, which shows that even highly complex resections are starting to shift into less invasive formats. Device use per case is also high because major vascular division and extensive stapling are common in these operations. The thoracic surgery market therefore receives a disproportionate revenue contribution from pneumonectomy relative to its volume because complexity raises both instrument intensity and platform value.

Complete Report Scope:

- By Product And Services

- Product

- Surgical Instruments and Accessories

- Endoscopes and Imaging Systems

- Energy and Stapling Devices

- Robotic Platforms

- Services

- Preoperative Planning Services

- Intraoperative Navigation Services

- Postoperative Monitoring And Follow-Up Services

- Teleconsultation Services

- Surgical Training And Support Services

- Product

- By Procedure Type

- Open Thoracic Surgery

- Video-Assisted Thoracoscopic Surgery

- Robotic-Assisted Thoracic Surgery

- Endoscopic Thoracic Surgery

- Other Thoracic Procedures

- By Surgery Type

- Lobectomy

- Wedge Resection

- Pneumonectomy

- Pleurectomy

- Segmental Resection

- Other Surgery Types

- By Medical Condition

- Lung Cancer

- Esophageal Cancer

- Mediastinal Tumors

- Pneumothorax

- Empyema

- Other Thoracic Conditions

- By Patient Type

- Inpatients

- Outpatients

- By Surgical Approach

- Minimally Invasive Approach

- Standard Open Approach

- By Surgical Scope

- Diagnostic

- Therapeutic

- Emergency

- By End User

- Hospitals

- Ambulatory Surgical Centers/Outpatient Centre

- Specialty Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 39.03% of the thoracic surgery market share in 2025, which kept it as the largest regional contributor by revenue. The region benefits from mature reimbursement systems, a dense concentration of academic thoracic centers, and broad access to robotic and thoracoscopic infrastructure. It is also further along in linking diagnosis, surgery, and postoperative pathway management into structured care models for lung and esophageal disease. This means regional growth is being shaped more by procedural upgrading and care setting shifts than by a simple rise in disease incidence. The thoracic surgery market in North America remains important because new technologies tend to reach commercial scale here earlier than in most other regions.

Europe remained the second-largest regional block, led by Germany, the United Kingdom, and France in the user-supplied draft. Germany has continued to expand robotic thoracic activity, and the University Hospital of Heidelberg initiated robotic-assisted bronchoscopy in March 2025 as part of preparation for national lung cancer screening. A 2026 study based on France's PMSI administrative database found a 15.6% year-over-year rise in robotic hospital stays between 2021 and 2022, with thoracic surgery accounting for 7% of all robotic procedures nationally. Regulatory compliance under EU MDR 2017/745 continues to favor companies that already have strong certification capacity and post-market support structures. The thoracic surgery market in Europe, therefore, combines healthy technology adoption with a regulatory environment that can slow smaller entrants.

Asia-Pacific is projected to grow at 8.92% CAGR through 2031, giving it the fastest regional expansion in the thoracic surgery market size. China is a major driver because surgical robot procurement reached CNY 691 million in Q1 2025, equal to USD 95 million, after a 43% year-over-year increase in the user-supplied draft. Domestic manufacturers are widening access by pricing systems at 50-70% of imported alternatives, which supports adoption beyond top-tier city hospitals in the user-supplied draft. India is opening more room for cancer surgery volumes through broader health coverage in the user-supplied draft, while Japan has expanded reimbursement support for robotic-assisted lobectomy in the user-supplied draft. South America, the Middle East, and Africa remain smaller markets, but private hospital groups in Brazil, Saudi Arabia, and the United Arab Emirates are using thoracic robotics as a differentiation tool, while workforce shortages across parts of Africa continue to limit addressable volume.

- Product Manufacturer

- Service Provider

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Thoracic Disease Burden

- 4.2.2 Shift Toward Minimally Invasive Thoracic Surgery

- 4.2.3 Adoption of Robotics And Image Guidance

- 4.2.4 Expansion of Ambulatory Thoracic Care Pathways

- 4.2.5 OR Throughput Pressure From Reprocessing And Turnover Constraints

- 4.2.6 Reimbursement Lag For New Thoracic Platforms

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Thoracic Systems

- 4.3.2 Shortage of Skilled Thoracic Surgeons

- 4.3.3 Regulatory And Evidence Burden For New Devices

- 4.3.4 Capital Budget Prioritization Versus Competing Surgical Specialties

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product And Services

- 5.1.1 Product

- 5.1.1.1 Surgical Instruments and Accessories

- 5.1.1.2 Endoscopes and Imaging Systems

- 5.1.1.3 Energy and Stapling Devices

- 5.1.1.4 Robotic Platforms

- 5.1.2 Services

- 5.1.2.1 Preoperative Planning Services

- 5.1.2.2 Intraoperative Navigation Services

- 5.1.2.3 Postoperative Monitoring And Follow-Up Services

- 5.1.2.4 Teleconsultation Services

- 5.1.2.5 Surgical Training And Support Services

- 5.1.1 Product

- 5.2 By Procedure Type

- 5.2.1 Open Thoracic Surgery

- 5.2.2 Video-Assisted Thoracoscopic Surgery

- 5.2.3 Robotic-Assisted Thoracic Surgery

- 5.2.4 Endoscopic Thoracic Surgery

- 5.2.5 Other Thoracic Procedures

- 5.3 By Surgery Type

- 5.3.1 Lobectomy

- 5.3.2 Wedge Resection

- 5.3.3 Pneumonectomy

- 5.3.4 Pleurectomy

- 5.3.5 Segmental Resection

- 5.3.6 Other Surgery Types

- 5.4 By Medical Condition

- 5.4.1 Lung Cancer

- 5.4.2 Esophageal Cancer

- 5.4.3 Mediastinal Tumors

- 5.4.4 Pneumothorax

- 5.4.5 Empyema

- 5.4.6 Other Thoracic Conditions

- 5.5 By Patient Type

- 5.5.1 Inpatients

- 5.5.2 Outpatients

- 5.6 By Surgical Approach

- 5.6.1 Minimally Invasive Approach

- 5.6.2 Standard Open Approach

- 5.7 By Surgical Scope

- 5.7.1 Diagnostic

- 5.7.2 Therapeutic

- 5.7.3 Emergency

- 5.8 By End User

- 5.8.1 Hospitals

- 5.8.2 Ambulatory Surgical Centers/Outpatient Centre

- 5.8.3 Specialty Clinics

- 5.8.4 Other End Users

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Mexico

- 5.9.2 Europe

- 5.9.2.1 Germany

- 5.9.2.2 United Kingdom

- 5.9.2.3 France

- 5.9.2.4 Italy

- 5.9.2.5 Spain

- 5.9.2.6 Rest of Europe

- 5.9.3 Asia-Pacific

- 5.9.3.1 China

- 5.9.3.2 Japan

- 5.9.3.3 India

- 5.9.3.4 Australia

- 5.9.3.5 South Korea

- 5.9.3.6 Rest of Asia-Pacific

- 5.9.4 Middle East & Africa

- 5.9.4.1 GCC

- 5.9.4.2 South Africa

- 5.9.4.3 Rest of Middle East & Africa

- 5.9.5 South America

- 5.9.5.1 Brazil

- 5.9.5.2 Argentina

- 5.9.5.3 Rest of South America

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Product Manufacturer

- 6.3.1.1 B. Braun Melsungen AG

- 6.3.1.2 Boston Scientific Corporation

- 6.3.1.3 CONMED Corporation

- 6.3.1.4 Cook Medical LLC

- 6.3.1.5 Fujifilm Holdings Corporation

- 6.3.1.6 Getinge AB

- 6.3.1.7 Intuitive Surgical, Inc.

- 6.3.1.8 Johnson and Johnson

- 6.3.1.9 Medtronic plc

- 6.3.1.10 Olympus Corporation

- 6.3.1.11 Smith and Nephew plc

- 6.3.1.12 Stryker Corporation

- 6.3.1.13 Teleflex Incorporated

- 6.3.1.14 Terumo Corporation

- 6.3.2 Service Provider

- 6.3.2.1 Mayo Clinic

- 6.3.2.2 Cleveland Clinic

- 6.3.2.3 Massachusetts General Hospital

- 6.3.2.4 Johns Hopkins Hospital

- 6.3.2.5 Memorial Sloan Kettering Cancer Center

- 6.3.2.6 University of Texas MD Anderson Cancer Center

- 6.3.2.7 Toronto General Hospital

- 6.3.2.8 National University Hospital, Singapore

- 6.3.2.9 Apollo Hospitals

- 6.3.1 Product Manufacturer

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment