|

시장보고서

상품코드

2073192

흉부외과 기기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thoracic Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

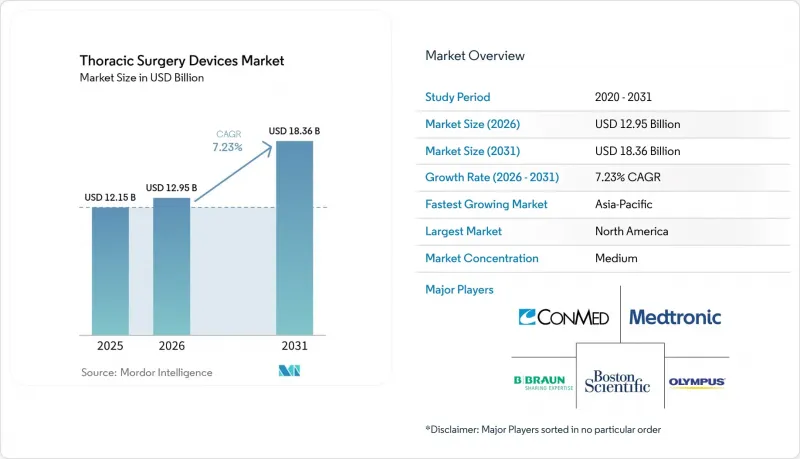

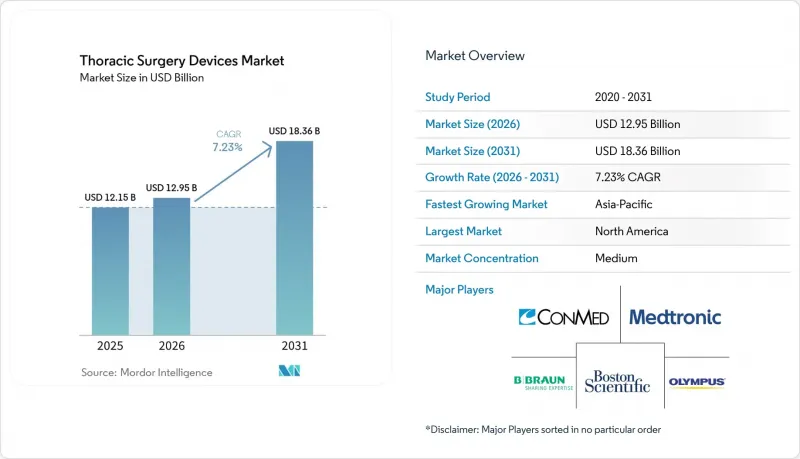

Mordor Intelligence에 의하면, 흉부외과 기기 시장 규모는 2025년에 121억 5,000만 달러, 2026년에 129억 5,000만 달러되어, 2031년까지 183억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 7.23%로 성장할 전망입니다.

본 보고서는 수술 유형(개흉 수술, VATS, 로봇 보조 수술, 내시경 수술), 제품 유형(수술 기구, 내시경/영상 진단 장치, 에너지/스테이플링 장치, 로봇 플랫폼), 적응증(폐암, 식도암, 기흉, 종격동 종양, 다한증), 최종 사용자(병원 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 흉부외과 기기 시장 동향 및 인사이트

폐암 검진 확대 및 조기 수술 의뢰 증가

폐암 검진 프로그램의 확대에 따라 조기 진단 사례가 증가하고 있으며, 이는 흉부외과 기기 시장에서 외과적 치료 경로를 선택하는 환자 수 증가로 직접적으로 이어지고 있습니다. OSF HealthCare에서는 AI를 활용한 다단계 선별 검사 프로그램을 도입한 결과, 해당 기관의 선별 검사 실시율이 2020년 18.2%에서 2025년까지 42.8%로 상승했으며, 같은 기간 동안 1기 진단율은 30.9%에서 44.6%로 증가했습니다. 영국 NHS 폐암 검진 프로그램에 따르면, 2025년 3월까지 검진을 통해 진단된 폐암은 7,193건에 달했으며, 이 중 63.1%가 1기였습니다. 이는 선별 검사를 통해 환자 구성에 변화가 생겨, 보다 조기에 외과적 개입으로 전환될 수 있음을 보여줍니다. 조기 발견으로 인해 병기 분류 검사, 영상 유도 하 기관지경 검사, 내비게이션 기관지경 검사의 건수도 증가함에 따라, 흉부외과 기기 시장의 상업적 이익은 단순한 절제 수술에만 그치지 않습니다. 이러한 광범위한 검사 및 치료 과정 덕분에, 병원이 체계적인 흉부 진료 경로를 통해 더 많은 결절과 조기 병변을 관리하게 됨에 따라 내시경 시스템, 영상 진단 기기 및 접근 장치 수요가 증가하고 있습니다.

ERAS 도입 확대 및 당일 퇴원 프로토콜

조기 회복 프로토콜(ERAS)의 보급에 따라, 흉부외과 기기 시장에서는 특정 수술이 외래 수술이나 당일 퇴원 방식으로 전환되고 있습니다. 『JTCVS Open』지에 게재된 체계적 문헌고찰 및 메타분석에 따르면, 19건의 연구와 8,447명의 환자를 대상으로 한 조사에서 흉부외과 수술 후 조기 회복 프로토콜(ERAS)을 적용한 결과, 입원 기간이 3일 단축되고 수술 후 합병증의 전반적인 발생률이 감소한 것으로 밝혀졌습니다. 2015년부터 2024년까지 44개국에서 발표된 617편의 논문을 대상으로 한 문헌계량학적 조사에 따르면, 흉부 ERAS에 관한 연구는 현재 연간 100편을 넘어서는 것으로 나타났습니다. 이 중 중국이 214편, 미국이 155편을 차지하고 있는데, 이는 단순한 단편적인 도입이 아니라 프로토콜에 대한 지속적인 개선이 진행되고 있음을 시사합니다. 2024년에 실시된 폐 결절 절제를 위한 VATS 당일 수술에 관한 실제 임상 연구에서는 수술 전 재활, 소구경 배액관, 그리고 다각적인 통증 관리를 통해 표준 치료에 비해 조기 퇴원이 가능해졌음이 밝혀졌습니다. 이러한 치료 경로를 표준화하는 의료기관이 늘어남에 따라, 흉부외과 기기 시장은 모든 사례를 기존의 입원 의뢰 경로로만 제한할 필요 없이, 저비용 환경에서 수요가 더욱 확대될 것으로 전망됩니다. 이러한 변화는 회복 기간을 단축하고 수술 후 관리를 간소화하는 플랫폼 및 기기의 보급을 촉진할 것입니다.

고도화된 흉부 수술 플랫폼에서 외과의사의 학습 곡선이 가파른 점

흉강경 수술(VATS)의 기존 기술에 비해 로봇 수술을 숙달하는 데 훨씬 더 오랜 시간이 소요되기 때문에 흉부외과 기기 시장은 여전히 보급이 정체된 상황에 직면해 있습니다. 한국의 28개 병원을 대상으로 한 전국 규모의 집단 기반 연구에 따르면, 학습 곡선의 임계값 중앙값은 110건이었으며, 2019년부터 2022년까지의 연구 기간 동안 그 수준에 도달한 병원은 28개 병원 중 고작 8개 병원에 그쳤습니다. 노르웨이의 한 의료기관에서 시행된 200건의 로봇 보조 폐엽 절제술에 관한 연구에서 2단계 학습 곡선이 확인되었습니다. 수술 시간은 117번째 사례를 넘어서도 계속해서 단축되고 있으며, 합병증 발생률은 94번째 사례 무렵에야 비로소 안정되었습니다. 이로 인해 흉부외과 기기 시장에서 경제적 딜레마가 발생하고 있습니다. 왜냐하면 병원은 외과 의사가 프로그램 도입을 정당화할 수 있을 만큼의 효율성에 도달하기도 전에 종종 설비 투자를 단행해 버리기 때문입니다. 이 문제는 지도 체계, 펠로우십 양성 체계, 체계적인 로봇 수술 훈련이 충분히 갖춰지지 않은 2차 병원이나 신흥 시장에서 더욱 심각합니다. 이러한 지원 체계가 확대되기 전까지는 흉부외과 기기 시장에서 로봇 수술의 보급이 병원 유형에 따라 고르지 않은 양상을 보일 것으로 보입니다.

부문별 분석

2025년, 비디오 보조 흉강경 수술(VATS)은 흉부외과 기기 시장 점유율의 49.21%를 차지하며, 해당 시장에서 가장 큰 수술 방식 부문이 되었습니다. 이 지위는 장기간에 걸친 임상적 근거, 확립된 수련 과정, 그리고 폐절제술 분야에서 신뢰할 수 있는 종양학적 치료 성과를 반영하고 있습니다. 북미와 유럽의 주요 학술 의료 센터에서는 이미 보편화되어 있지만, 더 얇은 트로카, 4K 영상, 저압 공기 주입 기술의 도입으로 인해 지역 병원에서도 보급이 확대되고 있습니다. 로봇 보조 흉강경 수술은 종격동 및 기관 분지 하부 림프절 부위로의 접근성을 개선하는 관절식 기구, 손떨림 보정 기능, 3D 광학 시스템에 힘입어 2031년까지 연평균 성장률(CAGR) 8.23%로 성장할 것으로 전망됩니다.

2026년 다기관 공동 코호트 연구에 따르면, 로봇 보조 폐엽 절제술은 VATS(영상 보조 흉강경 수술)에 비해 개흉 수술로의 전환율이 낮고, 수술 후 입원 기간도 짧은 것으로 보고되었으며, 이는 보다 복잡한 수술에서 로봇을 활용하는 근거를 강화해 줍니다. 개흉 흉강 수술은 재수술 사례, 혈관 침윤, 외상 등 최소 침습적 접근법이 여전히 제한적인 분야에서 흉강 수술용 의료기기 시장에서 여전히 중요한 위치를 차지하고 있습니다. 내시경 흉부 수술 시장 규모는 여전히 작지만, 내비게이션 기관지경 검사의 보급에 따라 생검 및 국소 절제술의 선택지가 확대되고, 기존에는 절제술로 넘어갔을 가능성이 있는 주변 병변의 치료가 가능해짐에 따라 해당 시장은 성장하고 있습니다. 일본에서는 2018년에 로봇 보조 폐엽 절제술, 2020년에 로봇 보조 폐분절 절제술이 보험 적용 대상이 됨에 따라, 로봇 보조 흉부 수술은 폐암 수술 전체의 1% 미만에서 2025년까지 15% 이상으로 확대되었습니다. 이는 아시아태평양의 VATS 시장 상한선이 현재 점유율이 시사하는 것보다 낮을 가능성이 있음을 시사합니다. 이 순서가 중요한 이유는 흉부외과 기기 시장에서는 플랫폼의 보급이 정착되기 전에 보험 적용 확대가 선행되는 경우가 많기 때문입니다.

2025년, 로봇 플랫폼은 제품 유형별 매출의 31.83%를 차지하며 흉부외과 기기 시장에서 가장 큰 제품 부문이 되었습니다. 이 부문은 이미 도입된 장비의 효과와 핵심 하드웨어, 보조 기기 및 관련 소프트웨어에 더해진 부가가치를 반영하고 있습니다. 내시경 및 영상 진단 시스템은 2031년까지 연평균 성장률(CAGR) 7.28%를 나타낼 것으로 예측되며, 흉부외과 기기 시장에서 가장 빠르게 성장하는 제품 카테고리가 될 것입니다. 이러한 성장은 4K 형광 가이드를 통한 시각화, 분절 평면 매핑을 위한 인디시안 그린 관류 이미징, 그리고 현재 독립형 시스템과 로봇 타워 모두에 탑재되고 있는 AI 강화 오버레이 도구 덕분입니다.

수술 기구 및 부속품은 로봇 시스템의 도입 대수가 늘어날 때마다 수요가 확대되고 있습니다. 이는 각 수술마다 교체용이나 일회용 제품의 사용이 반복되기 때문입니다. 에너지 장치 및 스테이플링 장치는 표준 구성에서 더 큰 압력을 받지만, 폐문부 해부학적 구조나 고밀도 식도 조직에 사용되는 특수 두꺼운 조직용 리로드 카트리지는 여전히 프리미엄급 위치를 유지하고 있습니다. 또한, 흉부외과 분야에서는 과거 기계식 스테이플러로만 수행되던 특정 폐엽 절제술 및 폐분절 절제술 과정에서 초음파 에너지 플랫폼으로의 전환이 점차 진행되고 있습니다. 따라서 제품 구성의 균형 측면에서 볼 때, 핵심 자본 설비와 반복 사용이 가능한 액세서리 및 영상 진단 기능의 업그레이드를 결합할 수 있는 공급업체가 유리합니다. 이러한 추세로 인해 흉부외과 기기 시장은 폭넓은 제품 포트폴리오, 탄탄한 서비스 체계, 그리고 시각화, 접근성, 로봇 워크플로우의 통합을 실현하고 있는 공급업체에게 유리한 상황이 지속되고 있습니다.

지역별 분석

2025년, 북미는 흉부외과 기기 시장 점유율의 38.23%를 차지하며, 해당 시장에서 가장 규모가 큰 지역 부문이 되었습니다. 이러한 위상은 로봇 시스템 도입 대수가 많고, ERAS(조기 회복 수술 후 관리) 도입이 성숙 단계에 이르렀으며, 병원 시스템 전반에 걸쳐 복잡한 흉부 수술을 지속적으로 지원하는 보상 체계에 의해 뒷받침되고 있습니다. 2026년 CMS(미국 의료보험서비스센터)의 정책 문서에 따르면, 코드 163-165에 해당하는 복잡한 흉부 수술에 대한 DRG(진단 관련군) 기반의 보상액은 복잡도에 따라 1건당 1만 3,929달러에서 3만 2,613달러 사이입니다. 미국은 수술 건수가 많을 뿐만 아니라 로봇 및 첨단 내시경 플랫폼에 대한 폭넓은 접근성이 더해져, 이 지역의 주요 수술 거점으로 자리매김하고 있습니다. 한편, 2026년 1월 1일부터 시행되는 심장·흉부외과 분야의 비시간 기반 작업 RVU 2.5% 삭감은 단기적인 이익률에 압박 요인이 될 것이며, 각 프로그램이 단순히 수술 건수를 줄이는 대신 시간 효율이 높은 치료 경로나 특정 시설로의 전환을 우선시하는 방향으로 나아갈 가능성이 있습니다.

유럽은 독일과 영국을 필두로, 흉부외과 기기 시장에서 지역별 2위의 규모를 차지하고 있습니다. 이 지역은 강력한 흉부외과 센터 네트워크라는 강점을 가지고 있지만, 의료기기 도입에 있어서는 EU 의료기기 규정(MDR)에 따른 더욱 엄격한 규정 준수 환경의 영향을 지속적으로 받고 있습니다. 2025년, 가이즈 앤 세인트 토마스 NHS 재단 트러스트는 NHS 공급망 체계를 통해 인튜이티브 서지컬과 7년간의 로봇 흉강경 수술에 관한 직접 계약을 체결했습니다. 이는 규정 준수상의 장벽이 해소된다면, 공공 조달을 통해 공급업체와 장기적인 관계를 구축할 수 있음을 보여줍니다. 프랑스, 이탈리아, 스페인, 폴란드, 네덜란드 및 스칸디나비아 국가들에서는 각국의 의료 제도적 제약 속에서 VATS(흉강경 수술) 및 ERAS(수술 후 조기 회복)의 활용이 지속적으로 확대되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.92%를 나타낼 것으로 예측되며, 흉부외과 기기 시장에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 일본에서는 보험 적용 범위 확대에 따라, 로봇 보조 흉부 수술이 폐암 수술에서 차지하는 비중이 2017년 1% 미만에서 2025년에는 15% 이상으로 증가하는 등, 보험 급여가 수술 구성을 어떻게 변화시키는지를 이미 보여주고 있습니다. 중국은 2025년에 국내 로봇 브랜드가 공립 병원 입찰의 50% 이상을 수주하고, 상하이 폐병원이 단일 기관으로서 국내 로봇 보조 흉강 수술 건수가 1,000건을 돌파함에 따라, 흉부외과 기기 시장에서 구조적으로 가장 중요한 성장 동력으로 부상하고 있습니다. 인도, 한국, 호주에서도 보험 적용 범위 확대와 대규모 종양 센터를 통해, 저침습 및 로봇 보조 흉강 수술의 수용 능력이 확대되고 있습니다. 한편, 중동 및 아프리카 및 남미는 규모는 작지만, 사립 병원의 성장과 의료 관광 인프라 확충에 힘입어 투자처로서 부상하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the thoracic surgery devices market size is projected to be USD 12.15 billion in 2025, USD 12.95 billion in 2026, and reach USD 18.36 billion by 2031, growing at a CAGR of 7.23% from 2026 to 2031.

This report is Segmented by Procedure Type (Open, VATS, Robotic-Assisted, Endoscopic), Product Type (Instruments, Endoscopes/Imaging, Energy/Stapling, Robotic Platforms), Indication (Lung Cancer, Esophageal Cancer, Pneumothorax, Mediastinal Tumors, Hyperhidrosis), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Thoracic Surgery Devices Market Trends and Insights

Rising Lung Cancer Screening and Earlier Surgical Referral

Expanded lung cancer screening programs are producing more early-stage diagnoses, and that directly raises the number of patients who move into surgical pathways in the thoracic surgery device market. At OSF HealthCare, an AI-assisted multistep screening program increased the institutional screening rate from 18.2% in 2020 to 42.8% by 2025, while stage I diagnoses rose from 30.9% to 44.6% over the same period. The UK NHS Lung Cancer Screening Programme reported 7,193 lung cancers diagnosed through screening by March 2025, and 63.1% of those cases were stage 1, which shows how screening can shift case mix toward earlier surgical intervention. Earlier detection also expands the volume of staging procedures, image-guided bronchoscopy, and navigational bronchoscopy, so the commercial benefit in the thoracic surgery device market extends beyond formal resection alone. That broader procedural funnel supports demand for endoscopy systems, imaging tools, and access devices as hospitals manage more nodules and more early lesions through organized thoracic pathways.

Increasing ERAS Adoption and Same-Day Recovery Pathways

Enhanced recovery pathways are helping the thoracic surgery device market move selected procedures into ambulatory and same-day discharge settings. A systematic review and meta-analysis in JTCVS Open found that Enhanced Recovery After Thoracic Surgery protocols reduced hospital length of stay by 3 days and lowered overall postoperative complications across 19 studies and 8,447 patients. A bibliometric study covering 617 publications from 2015 to 2024 across 44 countries showed that thoracic ERAS research now exceeds 100 papers annually, with China contributing 214 publications and the United States 155, which points to ongoing protocol refinement rather than isolated adoption. A 2024 real-world study on VATS day surgery for pulmonary nodule resection showed that prehabilitation, small-diameter drainage tubes, and multimodal pain management enabled faster discharge than standard care. As more centers standardize these pathways, the thoracic surgery device market gains additional volume in lower-cost settings without requiring every case to remain inside traditional inpatient referral channels. This shift also favors platforms and instruments that shorten recovery and simplify postoperative management.

Steep Surgeon Learning Curve for Advanced Thoracic Platforms

The thoracic surgery device market still faces an adoption ceiling because robotic proficiency takes much longer to build than conventional VATS capability. A nationwide population-based study across 28 Korean hospitals found a median learning curve threshold of 110 procedures, and only 8 of the 28 hospitals reached that level during the 2019 to 2022 study period. A Norwegian single-center study of 200 robotic pulmonary lobectomies found a bi-phasic learning curve, with operative time still improving after the 117th procedure and complication rates stabilizing only around the 94th case. This creates an economic trap inside the thoracic surgery device market because hospitals often commit capital before surgeons reach the efficiency needed to justify the program. The problem is sharper in Tier 2 hospitals and emerging markets where proctoring systems, fellowship pipelines, and structured robotic training are less developed. Until those support systems widen, robotic diffusion in the thoracic surgery device market will remain uneven across hospital tiers.

Other drivers and restraints analyzed in the detailed report include:

- AI-Guided Imaging and Workflow Integration

- Aging Population and Complex Comorbidity Burden

- High Capital Expenditure and Case-Volume Threshold Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video-assisted thoracoscopic surgery held 49.21% of the thoracic surgery device market share in 2025, making it the largest procedure segment in the thoracic surgery device market. Its position reflects long-term clinical evidence, established training pathways, and reliable oncologic outcomes in lung resection. Penetration has already become deep in major academic centers across North America and Europe, but expansion continues in community hospitals through narrower trocars, 4K visualization, and low-pressure insufflation. Robotic-Assisted Thoracic Surgery is projected to grow at 8.23% CAGR through 2031, supported by articulated instruments, tremor filtration, and 3D optics that improve access in mediastinal and subcarinal lymph node territories.

A 2026 multicenter cohort study reported that robotic lobectomy delivered lower conversion-to-open rates and shorter postoperative stays than VATS, which strengthens the case for robotic use in higher-complexity procedures. Open Thoracic Surgery still retains a meaningful place in the thoracic surgery device market for re-operative cases, vascular invasion, and trauma, where minimally invasive access remains limited. Endoscopic Thoracic Surgery remains smaller, but it is growing as navigational bronchoscopy expands biopsy and focal ablation options for peripheral lesions that might otherwise move to resection. In Japan, reimbursement inclusion of robotic lobectomy in 2018 and segmentectomy in 2020 helped robotic thoracic surgery move from less than 1% of lung cancer procedures to more than 15% by 2025, which suggests the regional ceiling for VATS may be lower in Asia-Pacific than current shares indicate. That sequencing matters because the thoracic surgery device market often follows reimbursement expansion before broader platform adoption takes hold.

Robotic platforms held 31.83% of product type revenue in 2025, which made them the largest product segment in the thoracic surgery device market. The segment reflects the installed base effect and the premium value attached to core hardware, supporting instruments, and related software. Endoscopes and imaging systems are projected to grow at 7.28% CAGR through 2031, which makes them the fastest-moving product category in the thoracic surgery device market. Growth comes from 4K fluorescence-guided visualization, indocyanine green perfusion imaging for segmental plane mapping, and AI-enhanced overlay tools that now appear in both standalone systems and robotic towers.

Surgical instruments and accessories rise with every expansion in the robotic installed base because replacement and disposable use recur with each procedure. Energy and Stapling Devices face more pressure in standard configurations, but specialized thick-tissue reloads for hilar anatomy and dense esophageal tissue still support premium positioning. The thoracic surgery industry also shows a gradual shift toward ultrasonic energy platforms for selected lobectomy and segmentectomy steps that were once reserved for mechanical staplers. The segment mix, therefore, favors vendors that can pair core capital equipment with repeat-use accessories and imaging upgrades. That pattern keeps the thoracic surgery device market tilted toward vendors with broad portfolios, strong service coverage, and integration across visualization, access, and robotic workflows.

Complete Report Scope:

- By Procedure Type

- Open Thoracic Surgery

- Video-Assisted Thoracoscopic Surgery

- Robotic-Assisted Thoracic Surgery

- Endoscopic Thoracic Surgery

- By Product Type

- Surgical Instruments and Accessories

- Endoscopes and Imaging Systems

- Energy and Stapling Devices

- Robotic Platforms

- By Indication

- Lung Cancer

- Esophageal Cancer

- Pneumothorax

- Mediastinal Tumors

- Hyperhidrosis

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Thoracic Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.23% of thoracic surgery device market share in 2025, which made it the largest regional segment in the thoracic surgery device market. This position is supported by a dense robotic installed base, mature ERAS adoption, and a reimbursement structure that still supports complex thoracic procedures across hospital systems. CMS policy documentation for 2026 shows DRG-based reimbursement for complex thoracic procedures under codes 163 to 165 ranging from USD 13,929 to USD 32,613 per case depending on complexity. The United States remains the main volume center in the region because it combines high procedural intensity with broad access to robotic and advanced endoscopic platforms. At the same time, the 2.5% reduction in non-time-based work RVUs for cardiothoracic surgery effective January 1, 2026 creates a near-term margin headwind that could push programs to favor time-efficient pathways and selected site migration rather than reduce procedure volumes outright.

Europe held the second-largest regional position in the thoracic surgery device market, led by Germany and the United Kingdom. The region benefits from strong thoracic center networks, but device adoption remains shaped by a more demanding compliance environment under the EU Medical Device Regulation. In 2025, Guy's and St Thomas' NHS Foundation Trust awarded a 7-year direct robotic thoracic surgery contract to Intuitive Surgical through the NHS Supply Chain framework, which shows how public procurement can lock in long-duration vendor relationships once compliance barriers are cleared. France, Italy, Spain, Poland, the Netherlands, and the Scandinavian countries continue to expand VATS and ERAS use within national health system constraints.

Asia-Pacific is projected to grow at 8.92% CAGR through 2031, which makes it the fastest-growing regional segment in the thoracic surgery device market. Japan has already shown how reimbursement can reshape procedure mix, with robotic-assisted thoracic surgery moving from less than 1% of lung cancer procedures in 2017 to more than 15% by 2025 after insurance inclusion widened. China is becoming the most structurally important growth engine in the thoracic surgery device market because domestic robotic brands won more than 50% of public hospital tenders in 2025, while Shanghai Pulmonary Hospital surpassed 1,000 domestic robot-assisted thoracic cases at a single center. India, South Korea, and Australia are also extending minimally invasive and robotic thoracic capacity through reimbursement expansion and high-volume oncology centers, while the Middle East and Africa and South America remain smaller but emerging destinations for investment through private hospital growth and medical tourism infrastructure.

- Applied Medical Resources

- Asensus Surgical

- B. Braun

- Boston Scientific

- CMR Surgical

- Conmed

- Danaher

- FUJIFILM

- Getinge

- Intuitive Surgical

- Johnson & Johnson

- Karl Storz SE and Co. KG

- Medtronic

- MicroPort

- Olympus

- Richard Wolf

- Mindray

- Smiths Group

- Stryker

- Teleflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Lung Cancer Screening and Earlier Surgical Referral

- 4.2.2 Increasing ERAS Adoption and Same-Day Recovery Pathways

- 4.2.3 AI-Guided Imaging and Workflow Integration

- 4.2.4 Reimbursement Expansion for Robotic Thoracic Surgery

- 4.2.5 Subscription-Based Robotic Service Bundling

- 4.2.6 Aging Population and Complex Comorbidity Burden

- 4.3 Market Restraints

- 4.3.1 Steep Surgeon Learning Curve for Advanced Thoracic Platforms

- 4.3.2 High Capital Expenditure and Case-Volume Threshold Risk

- 4.3.3 Regulatory Evidence Burden for New Robotic and Energy Devices

- 4.3.4 Supply Chain Exposure to Specialized Components and Tariff Pressure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Procedure Type

- 5.1.1 Open Thoracic Surgery

- 5.1.2 Video-Assisted Thoracoscopic Surgery

- 5.1.3 Robotic-Assisted Thoracic Surgery

- 5.1.4 Endoscopic Thoracic Surgery

- 5.2 By Product Type

- 5.2.1 Surgical Instruments and Accessories

- 5.2.2 Endoscopes and Imaging Systems

- 5.2.3 Energy and Stapling Devices

- 5.2.4 Robotic Platforms

- 5.3 By Indication

- 5.3.1 Lung Cancer

- 5.3.2 Esophageal Cancer

- 5.3.3 Pneumothorax

- 5.3.4 Mediastinal Tumors

- 5.3.5 Hyperhidrosis

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Thoracic Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Applied Medical Resources Corporation

- 6.3.2 Asensus Surgical

- 6.3.3 B. Braun Melsungen AG

- 6.3.4 Boston Scientific Corporation

- 6.3.5 CMR Surgical

- 6.3.6 CONMED Corporation

- 6.3.7 Danaher Corporation

- 6.3.8 Fujifilm Holdings Corporation

- 6.3.9 Getinge AB

- 6.3.10 Intuitive Surgical

- 6.3.11 Johnson and Johnson

- 6.3.12 Karl Storz SE and Co. KG

- 6.3.13 Medtronic

- 6.3.14 MicroPort Scientific Corporation

- 6.3.15 Olympus Corporation

- 6.3.16 Richard Wolf GmbH

- 6.3.17 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.18 Smith and Nephew plc

- 6.3.19 Stryker Corporation

- 6.3.20 Teleflex Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment