|

시장보고서

상품코드

2073087

만성질환 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chronic Care Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

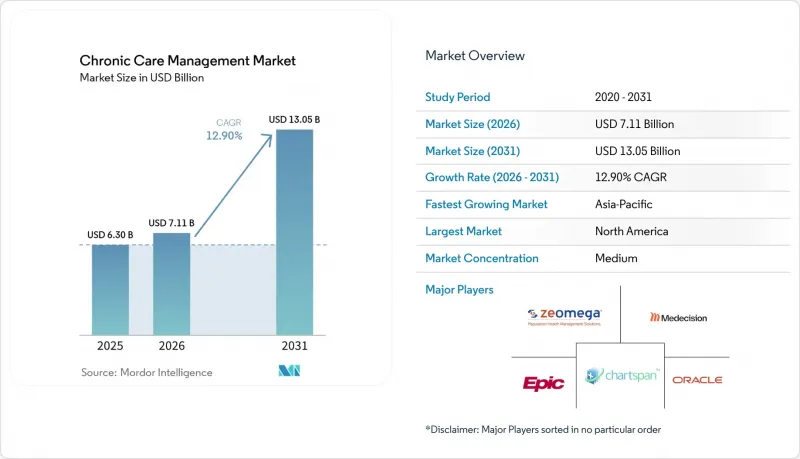

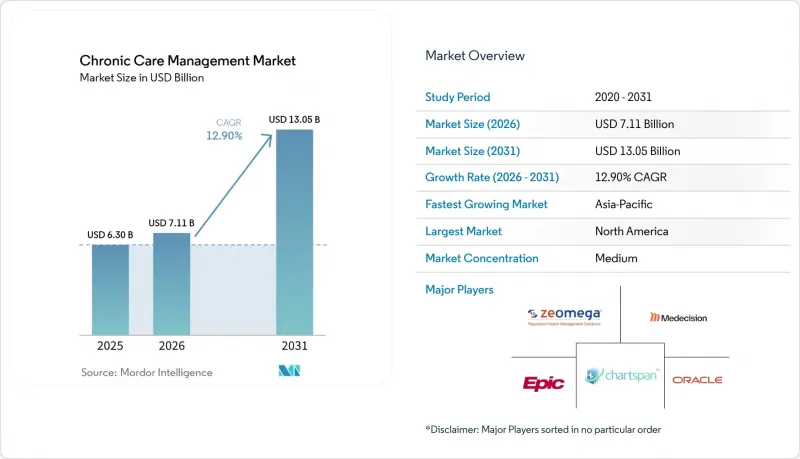

Mordor Intelligence에 의하면, 만성질환 관리 시장 규모는 2025년 63억 달러, 2026년 71억 1,000만 달러에서 2031년까지 130억 5,000만 달러로 확대한다고 예측되고 있어 2026-2031년까지 연평균 복합 성장률(CAGR)은 12.90%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어, 서비스), 도입 형태(클라우드 기반, On-Premise형), 최종 사용자(의료 제공업체, 보험사, 기타 최종 사용자), 질환 범주(당뇨병, 심혈관 질환, 만성 호흡기 질환, 암, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 만성질환 관리 시장 동향 및 인사이트

메디케어 확대와 가치 기반 의료의 도입 확대가 플랫폼 도입을 가속화하고 있습니다.

메디케어의 결제 개혁으로 인해 만성질환 관리의 양상이 크게 변화하고 있습니다. 의료 제공업체들은 현재 단순한 월별 활동 추적보다는 보고, 연계, 측정 가능한 성과를 중시하는 시스템을 우선시하고 있습니다. CMS(미국 의료보험 및 의료보조 서비스 센터)가 책임의료(Accountable Care)에 대한 보다 적극적인 참여를 장려하고, 2025년 APCM(Account Payer Care Model)으로의 전환 계획에 힘입어, 만성질환 관리 시장에서는 체계화된 1차 진료 관리와 가치 기반 보상 체계로의 전환이 진행되고 있습니다. 2026년 요금표에서는 CCM 상환율이 인상되고, 규정 준수 요건을 충족하는 프로그램을 확대할 수 있는 의료 제공업체의 투자 수익률(ROI)이 개선됨에 따라 이러한 추세가 더욱 가속화되었습니다. 이러한 변화는 매우 중요합니다. 적시에 데이터를 수집하고, 검증된 케어 플랜을 수립하며, 일관된 사후 관리를 통해 보험금 지급이 이루어질 경우, 수작업에 의존하는 업무 흐름으로는 이에 대응하기 어려워지기 때문입니다. 그 결과, 임상 처치, 문서화, 청구 처리를 원활하게 통합하는 소프트웨어에 대한 수요가 급증하고 있습니다.

AI를 활용한 케어 갭 감지가 개입까지 소요되는 시간에 대한 경제성을 재정의합니다.

AI를 활용한 치료 격차 감지는 문제 파악부터 임상적 개입에 이르기까지의 속도를 가속화함으로써 만성질환 관리 시장에 혁명을 일으키고 있습니다. Cadence는 2025년 7월 1일, AI를 핵심으로 하는 ‘Proactive Care Engine”를 발표했습니다. 이 시스템은 최소 90일간 모니터링을 받은 환자에서 치료 공백 해소율이 30%에 육박한다는 점을 자랑합니다. 이는 후속 조치의 성과 향상에 있어 자동 모니터링이 가져다주는 구체적인 이점을 입증하는 것입니다. 경쟁 환경은 변화하고 있으며, 초점은 인력 규모에서 데이터의 질, 워크플로우 자동화, 실시간 액션 트리거로 옮겨가고 있습니다. 예측에 따르면, 2026년까지 자율형 AI가 아시아태평양의 의료 IT 예산에서 상당한 비중을 차지하게 될 것이며, 만성질환 관리가 주요 투자 분야로 부상할 전망입니다. 지속적인 AI 모니터링을 활용하는 조직은 신속하게 대응하고, 더 많은 치료 격차를 해소하며, 인건비를 비례적으로 늘리지 않고도 더 대규모의 환자 집단을 관리할 수 있게 됩니다.

EHR과 RPM 플랫폼 간의 상호운용성 분절화가 규모 확대를 저해하고 있습니다.

세분화된 상호운용성은 여전히 만성질환 관리 시장의 발전을 저해하고 있습니다. 왜냐하면 효과적인 업무 흐름에는 여러 시스템에서 제공되는 완전하고 시의적절한 환자 기록이 필요하기 때문입니다. 2025년 ONC 조사에 따르면, 미국 의료 시스템의 60%가 세분화되고 구조화되지 않은 데이터를 의료 서비스의 격차를 효과적으로 관리하는 데 있어 장애물로 꼽고 있습니다. 휴마나가 2026년에 b.well Connected Health와 제휴를 계획하고 있는 것은 의료 제공업체, 보험 플랜, 약국, 용도의 데이터를 실시간으로 통합함으로써 이러한 과제를 해결하기 위함입니다. 그러나 소규모 공급업체나 의료 제공업체 그룹의 경우, 이러한 고도의 데이터 통합을 수행할 자원이 부족한 경우가 많아, 시장이 균등하게 성장할 수 있는 능력을 제한하고 있으며, 치료 계획의 질, 환자 식별, 청구 정확성에 영향을 미치고 있습니다.

부문별 분석

2025년, 이 서비스는 만성질환 관리 시장의 57.18%를 차지하고 있으며, 시장 초기 단계에서 외부 위탁을 통한 케어 조정 모델에 대한 의존도가 높았음이 드러났습니다. 의료 제공업체들은 임상 인력 배치, 아웃리치, 청구 지원 분야에서 대개 제3자 기관에 의존해 왔습니다. 이는 이러한 서비스들이 사내 디지털 워크플로우보다 도입하기가 더 쉬웠기 때문입니다. 복잡한 만성 질환 환자 집단을 관리하는 데에는 여전히 인적 개입이 필수적이지만, 시장은 플랫폼 주도의 자동화로 전환되고 있으며, 노동 집약적인 서비스 제공 방식에 대한 의존도는 낮아지고 있습니다.

소프트웨어 시장은 2031년까지 연평균 성장률(CAGR) 15.90%를 기록하며 성장할 것으로 전망됩니다. 이는 AI 시스템이 인력을 비례적으로 늘리지 않고도 신규 환자 접수, 문서 작성, 치료 계획 수립, 일상적인 환자 소통과 같은 업무를 자동화하기 때문인 것으로 보입니다. CCS는 2026년 4월, AI 도입을 통해 2026년 말까지 월간 10만 건을 넘는 신규 접수 문서의 70%-80%를 처리하고, 연간 비용을 30% 이상 절감하는 것을 목표로 한다고 발표했습니다. eClinicalWorks는 2026년 4월, “healow CCM Specialist Service”를 시작하며, 소프트웨어 및 서비스가 융합되는 하이브리드 모델로의 추세를 반영하고 있습니다. 산업계는 반복적이고 대량의 업무 흐름을 소프트웨어에 맡기는 한편, 복잡한 업무에 대해서는 AI를 활용한 인간과의 상호작용으로 전환해 가고 있습니다.

2025년에는 확장성, 상호 운용성, 대용량 데이터 처리 능력을 바탕으로 클라우드 기반 도입이 만성질환 관리 시장의 71.22%를 차지했습니다. 클라우드 환경은 원격 환자 모니터링, 통합 분석, 분산형 진료팀, 지속적인 업데이트를 지원하며, 신속한 도입과 시스템 전반에 걸친 가시성을 추구하는 조직에 최적의 선택지가 되고 있습니다. 주요 벤더들은 제품 로드맵을 클라우드 네이티브 AI 기능과 연계함으로써 이러한 추세를 더욱 강화하고 있습니다.

Oracle은 2025년 8월, 외래 진료 제공업체를 위한 AI 기반 전자건강기록(EHR)을 출시하며, 음성 중심의 임상 인텔리전스와 대화형 워크플로를 강조했습니다. 에픽은 2026년 3월에 “Agent Factory”를 도입하여, 임상 워크플로우 전반에 걸쳐 AI 에이전트를 활용할 수 있게 되었습니다. 거버넌스를 중시하는 계약에서 데이터 주권 및 저장 위치에 관한 요건이 여전히 중요하게 여겨지고 있는 만큼, On-Premise 구축은 2031년까지 연평균 성장률(CAGR) 14.25%로 확대될 것으로 예측됩니다. 솔루션 도입 규모 면에서는 클라우드가 주류를 이루고 있지만, 규제가 엄격한 시장에서는 On-Premise 시스템도 여전히 중요한 역할을 하고 있습니다.

지역별 분석

2025년, 북미는 만성질환 관리 시장의 41.55%를 차지하며, 현재 매출 측면에서 가장 규모가 큰 지역 기여 요인으로서의 입지를 확고히 했습니다. 이러한 선도적 지위는 메디케어의 CCM 청구 제도의 성숙, 보험사의 디지털화 진전, 만성질환 관리용 소프트웨어 및 서비스에 대한 막대한 투자에 힘입어 유지되고 있습니다. 2026년도의 의사 보수 일정에 따르면, CCM에 대한 상환액이 10% 인상되어 의료 제공업체들의 도입 확대가 촉진되었으며, 프로그램의 경제성도 향상되었습니다. 또한 미국 시장에서는 보험사와 의료 제공업체가 통합된 플랫폼과 중소규모 클리닉을 지원하는 전문 벤더 사이에서 양극화가 진행되고 있습니다.

유럽은 여전히 만성질환 관리 시장에서 2위의 규모를 자랑하며, 독일과 영국이 도입을 주도하고 있습니다. 독일의 DiGA 프레임워크는 디지털 헬스케어에 대한 보험 급여를 촉진하고, 인증된 만성질환 관리 용도를 위한 효율적인 도입 경로를 구축하고 있습니다. 영국에서는 디지털 만성질환 관리가 발전하고 있으며, 공적 보험 제도 하에서 고령자용 원격 모니터링 시스템의 비용 대비 효과를 강조하는 연구 결과가 보고되고 있습니다. 프랑스, 이탈리아, 스페인 등에서도 인구 동향에 따른 압박이 커지고, 상환 제도가 성숙해짐에 따라 시장이 서서히 확대되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 16.45%를 나타낼 것으로 예측되며, 만성질환 관리 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 만성 질환의 부담 증가, 디지털 헬스 정책에 대한 투자, 세분화된 의료 시스템에서 체계적인 치료 제공의 필요성에 의해 주도되고 있습니다. 인도, 중국, 일본, 한국, 호주 등의 국가들은 국가 차원의 디지털 헬스 프로그램, 예방을 목적으로 한 AI 전략, 임상 주도형 의사결정 지원 모델 등 다양한 노력을 통해 발전해 나가고 있습니다. 중동 및 아프리카와 남미는 여전히 초기 단계에 있으며, 수요는 전국적인 보급이라기보다는 도시 현대화 프로젝트나 선택적인 의료 시스템의 디지털화에 집중되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the chronic care management market size is projected to expand from USD 6.30 billion in 2025 and USD 7.11 billion in 2026 to USD 13.05 billion by 2031, registering a CAGR of 12.90% between 2026 to 2031.

This report is Segmented by Component (Software, Services), Deployment (Cloud-Based, On-Premise), End User (Providers, Payers, Other End Users), Disease Category (Diabetes, Cardiovascular Diseases, Chronic Respiratory Diseases, Cancer, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Chronic Care Management Market Trends and Insights

Rising Medicare and Value-Based Care Adoption Accelerates Platform Deployment

Medicare's payment reforms are reshaping the landscape of chronic care management. Providers are now prioritizing systems that emphasize reporting, coordination, and measurable outcomes over mere monthly activity tracking. Benefiting from CMS's push for deeper accountable care participation and the 2025 APCM pathway, the chronic care management market is witnessing a shift towards structured primary care management and value-based reimbursement. The 2026 fee schedule further fueled this momentum by boosting CCM reimbursement rates, enhancing ROI for providers who can scale compliant programs. This shift is pivotal; manual workflows falter when timely data capture, validated care plans, and consistent follow-ups are tied to reimbursement. Consequently, there's a surging demand for software that seamlessly integrates clinical actions, documentation, and payment readiness.

AI-Enabled Care Gap Detection Redefines Time-to-Intervention Economics

AI-driven care gap detection is revolutionizing the chronic care management market by accelerating the pace from problem identification to clinical intervention. Cadence unveiled its AI-centric Proactive Care Engine on July 1, 2025, boasting a nearly 30% closure rate for care gaps in patients monitored for a minimum of 90 days. This underscores the tangible benefits of automated surveillance in enhancing follow-up performance. The competitive landscape is shifting, with a focus moving from staffing scale to the quality of data, workflow automation, and real-time action triggers. Projections indicate that by 2026, agentic AI will carve out a significant portion of healthcare IT budgets in the Asia-Pacific, with chronic disease management emerging as a prime investment area. Organizations leveraging persistent AI monitoring can act swiftly, bridge more care gaps, and manage larger patient groups without a proportional increase in labor.

Fragmented Interoperability Across EHR and RPM Platforms Constrains Scale

Fragmented interoperability continues to hinder the chronic care management market, as effective workflows require complete and timely patient records from multiple systems. A 2025 ONC survey revealed that 60% of U.S. health systems identified fragmented and unstructured data as a barrier to managing care gaps effectively. Humana's planned 2026 partnership with b.well Connected Health aims to address this by integrating provider, plan, pharmacy, and application data in real time. However, smaller vendors and provider groups often lack the resources for such advanced data integration, limiting the market's ability to scale evenly and affecting care plan quality, patient identification, and billing accuracy.

Other drivers and restraints analyzed in the detailed report include:

- Under-Diagnosed Multimorbidity in Aging Populations Creates Latent Demand

- Remote Patient Monitoring Partnerships Extend the Data Perimeter for Chronic Care

- Clinical Documentation Burden Creates Adoption Drag and Compliance Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, services accounted for 57.18% of the chronic care management market, highlighting the reliance on outsourced care coordination models during the market's early stages. Providers often depended on third-party organizations for clinical staffing, outreach, and billing support, as these services were easier to implement than internal digital workflows. While human intervention remains critical for managing complex chronic populations, the market is shifting toward platform-led automation, reducing reliance on labor-intensive delivery methods.

Software is projected to grow at a 15.90% CAGR through 2031, driven by AI systems automating tasks like intake, documentation, care plan generation, and routine patient engagement without proportional headcount increases. CCS announced in April 2026 that its AI deployment aims to process 70%-80% of over 100,000 monthly intake documents by year-end 2026, delivering over 30% in annual cost savings. eClinicalWorks launched the healow CCM Specialist Service in April 2026, reflecting a trend toward hybrid models where software and services converge. The industry is moving toward AI-augmented human interaction for complex tasks, while software handles repetitive, high-volume workflows.

Cloud-based deployment held 71.22% of the chronic care management market in 2025, driven by its scalability, interoperability, and ability to handle large data volumes. Cloud environments support remote patient monitoring, centralized analytics, distributed care teams, and continuous updates, making them the preferred choice for organizations seeking fast implementation and system-wide visibility. Major vendors are aligning product roadmaps with cloud-native AI functionalities, reinforcing this trend.

Oracle launched an AI-driven EHR for ambulatory providers in August 2025, emphasizing voice-first clinical intelligence and conversational workflows. Epic introduced Agent Factory in March 2026, enabling AI agent deployment across clinical workflows. On-premise deployment is expected to grow at a 14.25% CAGR through 2031, as data sovereignty and residency requirements remain critical in governance-heavy contracts. While cloud solutions dominate by volume, on-premise systems retain relevance in markets with stricter regulatory controls.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- By End User

- Providers

- Payers

- Other End Users

- By Disease Category

- Diabetes

- Cardiovascular Diseases

- Chronic Respiratory Diseases

- Cancer

- Other Chronic Diseases

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 41.55% of the chronic care management market, establishing itself as the largest regional contributor to current revenues. This leadership is driven by the maturity of Medicare's CCM billing, increased payer digitization, and significant investments in chronic care software and services. The CY 2026 Physician Fee Schedule introduced a 10% reimbursement increase for CCM, encouraging broader provider adoption and improving program economics. The U.S. market is also becoming polarized between integrated payer-delivery platforms and specialist vendors supporting smaller and mid-sized practices.

Europe remains the second-largest region in the chronic care management market, with Germany and the U.K. leading adoption. Germany's DiGA framework facilitates digital health reimbursements, creating a streamlined pathway for certified chronic disease management applications. The U.K. is advancing in digital chronic care, with studies highlighting the cost-effectiveness of remote monitoring systems for older adults under public insurance frameworks. Other countries like France, Italy, and Spain are expanding gradually as demographic pressures rise and reimbursement structures mature.

Asia-Pacific is projected to grow at a 16.45% CAGR through 2031, making it the fastest-growing region in the chronic care management market. Growth is driven by the rising chronic disease burden, investments in digital health policies, and the need for structured care delivery in fragmented health systems. Countries like India, China, Japan, South Korea, and Australia are advancing through diverse initiatives, including national digital health programs, preventive AI strategies, and clinically governed decision support models. The Middle East, Africa, and South America remain in early stages, with demand focused on urban modernization projects and selective health system digitization rather than widespread national adoption.

- ChartSpan Medical Technologies, Inc.

- CVS Health

- eClinicalWorks LLC

- Elevance Health, Inc.

- Epic Systems

- EXLService Holdings, Inc.

- HealthSnap, Inc.

- Humana Inc.

- Koninklijke Philips

- Mckesson

- Medecision, Inc.

- Medtronic

- NextGen Healthcare

- Oracle

- Prevounce Health, LLC

- Siemens Healthineers

- The Cigna Group

- United Health Group

- Veradigm Inc.

- ZeOmega, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Medicare and Value-Based Care Adoption

- 4.2.2 Expansion of Remote Patient Monitoring Paired with Chronic Care Workflows

- 4.2.3 Under-Diagnosed Multimorbidity in Aging Populations

- 4.2.4 Provider Need to Reduce Avoidable Readmissions and Total Cost of Care

- 4.2.5 Reimbursement Friction for Documentation-Heavy CCM Workflows

- 4.2.6 AI-Enabled Care Gap Detection and Time Capture

- 4.3 Market Restraints

- 4.3.1 Clinical Documentation Burden and Billing Complexity

- 4.3.2 Fragmented Interoperability Across EHR, RPM, and Billing Systems

- 4.3.3 Care Team Staffing Constraints and Patient Non-Adherence

- 4.3.4 Narrow Margin Pressure in Small Practices Due to Reimbursement Dependence

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By End User

- 5.3.1 Providers

- 5.3.2 Payers

- 5.3.3 Other End Users

- 5.4 By Disease Category

- 5.4.1 Diabetes

- 5.4.2 Cardiovascular Diseases

- 5.4.3 Chronic Respiratory Diseases

- 5.4.4 Cancer

- 5.4.5 Other Chronic Diseases

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 ChartSpan Medical Technologies, Inc.

- 6.3.2 CVS Health Corporation

- 6.3.3 eClinicalWorks LLC

- 6.3.4 Elevance Health, Inc.

- 6.3.5 Epic Systems Corporation

- 6.3.6 EXLService Holdings, Inc.

- 6.3.7 HealthSnap, Inc.

- 6.3.8 Humana Inc.

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 McKesson Corporation

- 6.3.11 Medecision, Inc.

- 6.3.12 Medtronic plc

- 6.3.13 NextGen Healthcare, Inc.

- 6.3.14 Oracle Corporation

- 6.3.15 Prevounce Health, LLC

- 6.3.16 Siemens Healthineers AG

- 6.3.17 The Cigna Group

- 6.3.18 UnitedHealth Group Incorporated

- 6.3.19 Veradigm Inc.

- 6.3.20 ZeOmega, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment