|

시장보고서

상품코드

2073113

오픈 기어 윤활유 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Open Gear Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

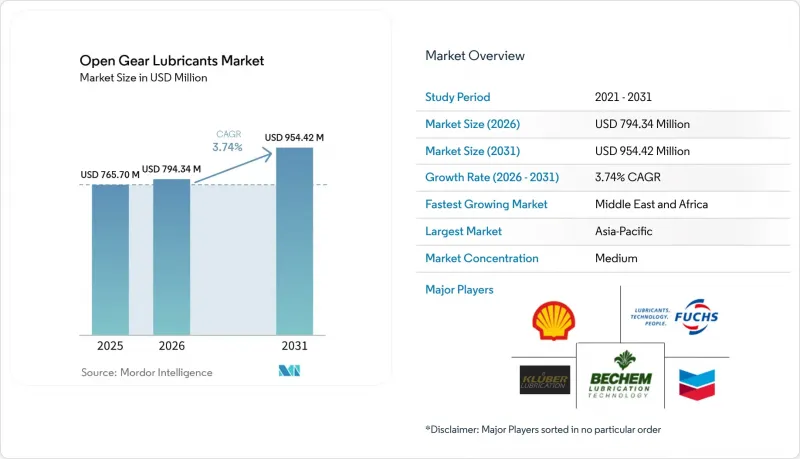

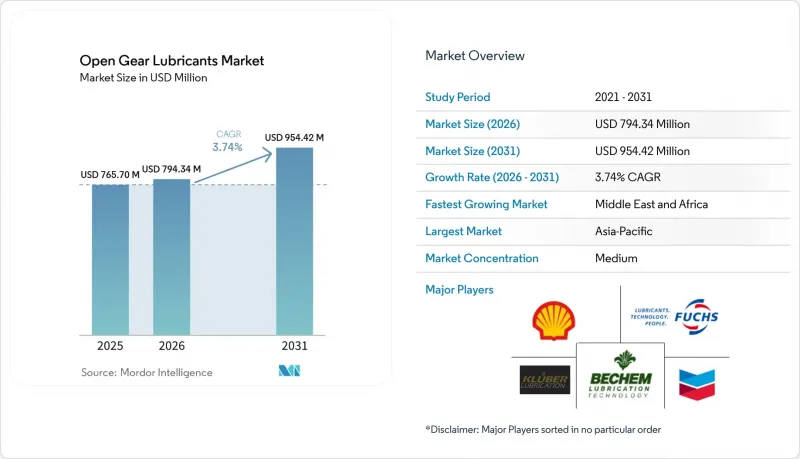

Mordor Intelligence에 의하면, 오픈 기어 윤활유 시장 규모는 2025년 7억 6,570만 달러에서 2026년에는 7억 9,434만 달러로 확대되어 2031년까지 9억 5,442만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 3.74%로 성장할 전망입니다.

본 보고서는 기유(광물유, 합성유, 바이오유), 최종 사용 산업(광업, 시멘트, 건설, 발전, 석유 및 가스, 선박, 기타) 및 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계 오픈 기어 윤활유 시장 동향 및 인사이트

광업 및 시멘트 산업의 확장에 따른 수요 증가

칠레, 페루, 인도네시아의 구리광산 및 철광산 확장뿐만 아니라 사우디아라비아에서의 신규 소성로 도입이 더해지면서 연간 윤활유 소비량이 증가하고 있습니다. 이러한 윤활유는 연속 가동을 하는 분쇄기나 로터리 킬른에 필수적입니다. 가마의 기어에 결함이 발생하면 생산이 중단되고 막대한 비용이 발생할 가능성이 있으므로, 조달 부서는 현재 윤활유의 초기 가격보다 팀켄(Timken) 정격에 따른 고부하 내구성을 우선시하고 있습니다. 크루버사의 합성 오픈 기어용 제품은 윤활유 소비량을 줄이고 작동 온도를 낮춤으로써 가동 시간을 현저히 향상시켰습니다. 또한, 집중식 스프레이 시스템을 통해 기어가 회전할 때마다 윤활유를 정확하게 공급함으로써 낭비를 최소화하고 있습니다. 그 결과, 주목의 초점은 리터당 가격에서 전체 수명 주기 비용으로 옮겨가고 있습니다.

바이오 윤활유의 사용 확대

미국 환경보호청(EPA)의 “선박 부수적 배출법(Vessel Incidental Discharge Act)” 규정에 따르면, 대형 선박의 경우 기름과 바다가 접촉하는 부위에서 환경 친화적인 윤활유를 사용해야 합니다. 이러한 요건으로 인해, 소정의 기간 내에 분해되는 생분해성 제품에 대한 수요가 확대될 것으로 예측됩니다. PAS 2060 인증을 획득한 캐스트롤의 탄소 중립 제품 ‘BioTac OG”는 바이오 그리스의 진화를 구현하고 있으며, 높은 생분해성을 실현함과 동시에 4볼 극압 시험에서 뛰어난 접착점을 보여주고 있습니다. 유출 사고에 따른 법적 책임에 대응하고 기업의 지속가능성 목표를 달성하기 위해, 해상 풍력 발전소와 연안 시멘트 터미널에서는 바이오에스테르로의 전환이 가속화되고 있습니다. 이러한 전환은 유럽의 OSPAR 협약과 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질(PFAS)에 대한 금지 조치가 임박한 점도 뒷받침하고 있어, 북해의 선단 사이에서 급속히 도입되고 있습니다. 바이오 배합에 대해 OEM(주문자 상표 제조) 승인을 받은 공급업체는 입찰 평가에서 우선적으로 고려되는 공급업체로 부상하고 있습니다. 경영진 사이에서 라이프사이클 탄소 회계의 중요성이 인식되는 가운데, 바이오 오픈 기어 윤활유 시장의 제품들은 기존 광물유보다 가격이 비싸더라도 장기 계약을 확보할 수 있는 체제가 갖춰져 있습니다.

지정학적 요인으로 인한 공급망의 불안정화

유럽의 그룹 II 기초유의 상당 부분이 통과하는 호르무즈 해협에서 혼란이 발생하면, 단기간 내에 블렌딩 비용이 크게 상승할 가능성이 있습니다. 홍해를 우회함으로써 리드타임이 대폭 연장됨에 따라, 저스트-인-타임 방식을 채택하고 있는 시멘트 공장은 비용이 증가할 수밖에 없었으며, 비상용 광물유 재고에 의존할 수밖에 없게 되었습니다. 북미의 블렌딩 업체들은 헤지 전략의 일환으로 국내산 폴리아알파올레핀으로 조달처를 전환하고 있지만, 합성 베이스 오일로 전환하기 위해서는 실험실 시험 및 OEM 제조업체의 재승인을 포함한 광범위한 절차가 필요합니다. 그룹 II 오일의 현물 가격이 크게 상승하면서 독립 블렌더들의 이익률을 압박하고 있습니다.

부문별 분석

2025년, 광물유는 오픈 기어 윤활유 시장 점유율의 43.56%를 차지했습니다. 이는 비용을 중시하는 아시아의 시멘트 가마에서 확고히 자리 잡은 사용 실적이 뒷받침된 것으로, 이 지역의 구매자들은 여전히 설비의 수명에 따른 결과가 아닌 드럼 단위로 구매하고 있습니다. 이 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 3.68%로 성장할 것으로 전망됩니다. 인도나 인도네시아에서 기존 설비가 가동을 시작함에 따라, 합성 윤활유가 이러한 우위를 유지하는 데 어려움을 겪고 있습니다. 국제전기표준회의(IEC)가 풍력 터빈용 기어박스에 대한 규제를 도입한 것을 배경으로, 폴리알파올레핀 및 그룹 III 블렌드는 현재 북미 시장에서 판매량의 상당 부분을 차지하고 있습니다. 시멘트 분야에서는 클루버(Kluber)사의 현장 데이터에 따르면, 합성 윤활유가 소비량과 작동 온도를 낮추는 것으로 밝혀졌으며, 이에 따라 다국적 기업들이 프리미엄 등급을 표준으로 채택하도록 장려하고 있습니다. 바이오 유래 에스테르는 현재 시장 점유율은 작지만, 특히 갑판 기계와 같이 VIDA 준수가 필수적인 분야에서 눈에 띄는 성장을 보이고 있습니다. 온도 범위를 확대하기 위해 바이오에스테르와 폴리아알파올레핀을 혼합하는 제조업체는 아시아 선박 분야에서 새로운 수익원을 개척할 가능성이 있습니다. 기술적 우위와 규제상의 인센티브를 고려할 때, 소비량 증가세가 둔화되고 있음에도 불구하고 합성 윤활유는 향후 10년이 끝나기 훨씬 전에 금액 기준으로 광물유를 추월할 것으로 전망됩니다.

오픈 기어 윤활유 분야의 합성유 시장은 크게 확대될 것으로 예상되며, 전체 시장에서 가장 빠르게 성장하고 있는 부문입니다. 가마나 제분소의 기어박스에서 OEM이 권장하는 나노 첨가제가 보편화됨에 따라, 광물유는 틈새 시장과 가격 주도형 용도로만 제한될 것이라는 위협에 직면해 있습니다. 이에 대응하여 각 공급업체들은 높은 수익률을 자랑하는 합성유와 디지털 모니터링 서비스를 결합하여 시장 점유율을 지키고, 장기적인 서비스 계약을 체결하는 것을 목표로 하고 있습니다. 동시에, 유럽 내 그룹 I 광물유의 생산 능력이 감소함에 따라 공급이 부족해지면서 그룹 III와의 가격 차이가 줄어들고 있습니다. 이러한 변화는 조달 부서가 단순한 청구 가격 대신 총소유비용(TCO)을 우선시하게 된 이유를 여실히 보여주고 있으며, 업계의 합성유로의 전환을 가속화하고 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 35.40%를 차지했습니다. 중국의 견고한 중공업 기반과 인도의 시멘트 산업 확대가 맞물려, 이 지역의 산업 동향을 주도하고 있습니다. 중국석유화학(Sinopec)의 톈진 확장 사업은 내습성 오픈 기어 제품공급을 촉진할 것으로 예상되며, 이는 인도네시아의 니켈 및 구리 제련소 가동 개시와 시기가 맞물립니다. 이 지역의 높은 기술력은 일본과 한국의 지식이 국제전기표준회의(IEC)의 기어박스 규격을 형성하고, OEM 제조업체들이 저온용 폴리아알파올레핀 블렌드의 채택을 추진하도록 이끌고 있다는 점에서도 분명합니다. 호주의 철광석 채굴 기업들은 필바라 외딴 지역의 인력 부족 문제를 해결하기 위해 자동 분사 시스템 도입을 추진하고 있으며, 이는 업계의 통합 솔루션으로의 전환을 더욱 두드러지게 하고 있습니다.

중동 및 아프리카는 2026년부터 2031년까지 연평균 성장률(CAGR) 3.82%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. “사우디 비전 2030”의 인프라 프로젝트가 시멘트 생산의 지속적인 확대를 뒷받침하고 있습니다. 리야드에서는 가마가 극한의 주변 온도와 연마성이 강한 모래에 노출되어 있어, 씻겨 나가기 어려운 고점도 합성 윤활유에 대한 수요가 증가하고 있습니다. 남아프리카의 백금 산업 부흥 역시 이와 유사한 고농도 분진 환경이라는 과제에 직면해 있지만, 집중 윤활 시스템이 지하 갱도에서 예기치 못한 가동 중단 시간을 대폭 줄이는 데 효과적임이 입증되었습니다. 이집트의 새로운 지중해 항구가 주도하는 북아프리카 해운 허브에서는 국제해사기구(IMO)의 오염 방지 규정을 준수하기 위해 부두 크레인에 바이오 그리스가 채택되고 있습니다. 그러나 지역 정세의 불안으로 인해 수입 베이스 오일의 운송비 프리미엄이 때때로 급등함에 따라, 구매자들은 현지에서 충전된 합성 윤활유로 눈을 돌리고 있습니다.

북미와 유럽은 전반적인 성장률 면에서는 뒤처지고 있지만, 주로 엄격한 환경 규제로 인해 화학제품의 동향에 큰 영향력을 행사하고 있습니다. 유럽의 오픈 기어 윤활유 시장은 완만한 성장이 예상되지만, 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질의 사용 금지 조치로 인해 제품 라인업을 대폭 재검토해야 할 상황에 직면해 있습니다. 미국에서는 해양 사업자들이 선미 파이프를 통한 광물유 사용을 단계적으로 폐지하고 있으며, 이는 “선박 부수적 배출법(Vessel Incidental Discharge Act)”의 규제 하에서 시추 허가를 확보하기 위한 조치이며, 그 결과 폴리아알파올레핀이나 에스테르계 등 친환경 윤활유 수요가 확대되고 있습니다. 영국 기어 협회(British Gear Association)가 국제전기기술위원회(IEC) 규격을 승인함에 따라, 영국 및 북유럽의 풍력 발전 부문 수요가 더욱 확대되고 있습니다. 한편, 남미, 특히 칠레와 페루에서는 구리 생산 확대에 힘입어 판매량이 꾸준히 증가하고 있습니다. 그러나 안데스 산맥의 광산에서 발생하는 물류상의 문제로 인해 집중 윤활 시스템의 가격이 상승하고 있으며, 이러한 시스템은 대개 미국이나 유럽에서 항공으로 운송되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the open gear lubricants market size is expected to increase from USD 765.70 million in 2025 to USD 794.34 million in 2026 and reach USD 954.42 million by 2031, growing at a CAGR of 3.74% over 2026-2031.

This report is Segmented by Base Oil (Mineral Oil, Synthetic Oil, and Bio-Based Oil), End-User Industry (Mining, Cement, Construction, Power Generation, Oil And Gas, Marine, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East, and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Open Gear Lubricants Market Trends and Insights

Rising Demand from Mining and Cement Expansion

Expansions of copper and iron-ore mines in Chile, Peru, and Indonesia, coupled with the introduction of new kilns in Saudi Arabia, are driving up annual lubricant consumption. These lubricants are essential for grinding mills and rotary kilns that operate continuously. Given that failures in kiln gears can halt production and incur substantial costs, procurement teams are now prioritizing high-load Timken ratings over the initial price of lubricants. Synthetic open-gear products from Kluber have reduced lubricant consumption and lowered operating temperatures, leading to noticeable improvements in operational uptime. Additionally, centralized spray systems are minimizing waste by precisely dosing lubricant with each gear rotation. As a result, the focus has shifted from the price per liter to the overall life-cycle cost.

Growth in Bio-Based Lubricants Adoption

The Environmental Protection Agency Vessel Incidental Discharge Act rule mandates that large vessels use environmentally acceptable lubricants at oil-to-sea interfaces. This requirement is expected to drive the demand for biodegradable products that break down within a specified timeframe. Castrol's carbon-neutral BioTac OG, certified to PAS 2060, showcases the evolution of bio-based greases, achieving high biodegradability alongside strong Four-Ball Extreme Pressure weld points. To address spill liabilities and meet corporate sustainability goals, offshore wind farms and coastal cement terminals are increasingly turning to bio-esters. This transition is further bolstered by Europe's OSPAR convention and impending bans on per- and polyfluoroalkyl substances, spurring swift adoption among North Sea marine fleets. Suppliers boasting original equipment manufacturer approvals for bio-based formulations are emerging as preferred vendors in bid assessments. With life-cycle carbon accounting gaining traction in boardrooms, offerings in the bio-based open gear lubricants market are poised to secure long-term contracts, even with a price premium over traditional mineral oils.

Geopolitical Supply-Chain Instability

Disruptions in the Strait of Hormuz, through which a significant portion of Europe's Group II base stocks transit, can lead to a substantial increase in blending costs within a short period. A diversion to the Red Sea extended lead times considerably, compelling just-in-time cement plants to rely on emergency mineral-oil inventories at a higher cost. While North American blenders have turned to domestic sourcing of polyalphaolefin as a hedge, the transition to synthetic stocks requires an extensive process involving laboratory testing and original equipment manufacturer reapproval. Spot prices for Group II oils have risen significantly, squeezing profit margins for independent blenders.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Uptake of Synthetic Base Oils

- AI-Enabled Predictive Maintenance Lowering Lubricant Wastage

- Emerging PFAS Restrictions Affect Legacy Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oils captured 43.56% of the open gear lubricants market share in 2025, thanks to entrenched use in cost-sensitive Asian cement kilns, where buyers still purchase by the drum rather than by equipment life results. The segment is projected to expand at a 3.68% CAGR during 2026-2031. As legacy assets in India and Indonesia come online, synthetics are challenging this dominance. Polyalphaolefin and Group III blends now account for a significant portion of North American sales, driven by the International Electrotechnical Commission mandate for wind-turbine gearboxes. In the cement sector, Kluber's field data reveals that synthetics reduce consumption and operating temperatures, persuading multinationals to adopt premium grades as the standard. While bio-based esters currently hold a small market share, they are witnessing substantial growth, especially where VIDA compliance is essential for deck machinery. Blenders merging bio-esters with polyalphaolefin to expand the temperature range could tap into new revenue streams in Asia's marine sector. Given the technical advantages and regulatory incentives, synthetics are poised to surpass mineral oils in value terms long before the end of the decade, even if their volumes remain subdued due to lower consumption rates.

The market for synthetic oils in open gear lubricants is projected to expand significantly, marking it as the most rapidly advancing segment in the larger market. With original equipment manufacturer-endorsed nano-additives becoming commonplace in kiln and mill gearboxes, mineral oils face the threat of being confined to niche, price-driven applications. In response, suppliers are pairing high-margin synthetics with digital monitoring services, aiming to safeguard their market share and establish enduring service contracts. Concurrently, as Group I mineral capacities dwindle in Europe, supply tightens, and the price gap to Group III narrows. This shift highlights why procurement teams are now prioritizing total cost of ownership over mere invoice price, hastening the industry's pivot towards synthetics.

Complete Report Scope:

- By Base Oil

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

- By End-user Industry

- Mining

- Cement

- Construction

- Power Generation

- Oil and Gas

- Marine

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific generated 35.40% of global revenue in 2025. China's robust heavy-industry foundation, coupled with India's cement expansion, is steering the region's industrial narrative. Sinopec's expansion in Tianjin is set to boost the supply of humidity-resistant open-gear products, coinciding with the launch of nickel and copper smelters in Indonesia. The region's technical prowess is evident as Japanese and South Korean inputs shape International Electrotechnical Commission gearbox standards, guiding original equipment manufacturers towards adopting low-temperature polyalphaolefin blends. In a bid to address labor shortages at its remote Pilbara sites, Australian iron-ore miners are turning to automatic spray systems, further emphasizing the industry's shift towards synthetic solutions.

The Middle East and Africa is the fastest-growing territory at 3.82% CAGR during 2026-2031. Saudi Vision 2030's infrastructure projects are fueling continuous cement production. In Riyadh, kilns face extreme ambient temperatures and abrasive sand, increasing the demand for high-viscosity synthetics that resist wash-off. South Africa's platinum revival encounters similar high-dust challenges; however, centralized lubrication systems have proven effective in significantly reducing unplanned downtime in underground shafts. North African marine hubs, with Egypt's new Mediterranean ports leading the charge, are adopting bio-based greases for dockside cranes, aligning with International Maritime Organization pollution protocols. Yet, regional political volatility occasionally inflates freight premiums for imported base oils, steering buyers towards locally packaged synthetics.

While North America and Europe may lag in overall growth, they wield significant influence over chemistry trends, largely due to stringent environmental regulations. Europe's open gear lubricants market is expected to grow modestly, but the prohibition of per- and polyfluoroalkyl substances threatens to overhaul product lineups. In the United States, offshore operators are phasing out mineral oils in stern tubes, a move aimed at securing drilling permits under Vessel Incidental Discharge Act regulations, subsequently boosting demand for polyalphaolefin and ester environmentally acceptable lubricants. The British Gear Association's endorsement of International Electrotechnical Commission standards is further propelling wind-sector demand in the United Kingdom and Nordic regions. Meanwhile, South America, particularly Chile and Peru, is witnessing robust volume growth driven by copper expansion. However, logistical challenges in the Andes mines are inflating prices for centralized lubrication systems, which are often flown in from the United States or Europe.

- Bel-Ray Company LLC

- BP p.l.c.

- Carl Bechem GmbH

- Castrol Limited

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil Lubricants

- Idemitsu Kosan Co. Ltd.

- Kluber Lubrication

- Lubrication Engineers Inc.

- Lubriplate Lubricants Company

- Petro-Canada Lubricants

- Petron Corporation

- Phillips 66 Lubricants

- Shell plc

- Sinopec Lubricants

- Specialty Lubricants Corporation

- TotalEnergies

- Valvoline Inc.

- Whitmore Manufacturing LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from mining and cement expansion

- 4.2.2 Growth in bio-based lubricants adoption

- 4.2.3 Increasing uptake of synthetic base oils

- 4.2.4 AI-enabled predictive maintenance lowering lubricant wastage

- 4.2.5 OEM-approved nano-additive packages extending gear life

- 4.2.6 Shift toward centralized spray systems in high-altitude mines

- 4.3 Market Restraints

- 4.3.1 Geopolitical supply-chain instability

- 4.3.2 Application difficulties with large-diameter open gears

- 4.3.3 Emerging PFAS restrictions affecting legacy chemistries

- 4.3.4 Skill shortage for advanced lubrication audits in developing regions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Base Oil

- 5.1.1 Mineral Oil

- 5.1.2 Synthetic Oil

- 5.1.3 Bio-based Oil

- 5.2 By End-user Industry

- 5.2.1 Mining

- 5.2.2 Cement

- 5.2.3 Construction

- 5.2.4 Power Generation

- 5.2.5 Oil and Gas

- 5.2.6 Marine

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordic Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Bel-Ray Company LLC

- 6.4.2 BP p.l.c.

- 6.4.3 Carl Bechem GmbH

- 6.4.4 Castrol Limited

- 6.4.5 Chevron Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Gulf Oil Lubricants

- 6.4.9 Idemitsu Kosan Co. Ltd.

- 6.4.10 Kluber Lubrication

- 6.4.11 Lubrication Engineers Inc.

- 6.4.12 Lubriplate Lubricants Company

- 6.4.13 Petro-Canada Lubricants

- 6.4.14 Petron Corporation

- 6.4.15 Phillips 66 Lubricants

- 6.4.16 Shell plc

- 6.4.17 Sinopec Lubricants

- 6.4.18 Specialty Lubricants Corporation

- 6.4.19 TotalEnergies

- 6.4.20 Valvoline Inc.

- 6.4.21 Whitmore Manufacturing LLC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Subsidised Cool Roofs for Low-income Urban Housing