|

시장보고서

상품코드

2073136

캠퍼스 스위치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Campus Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

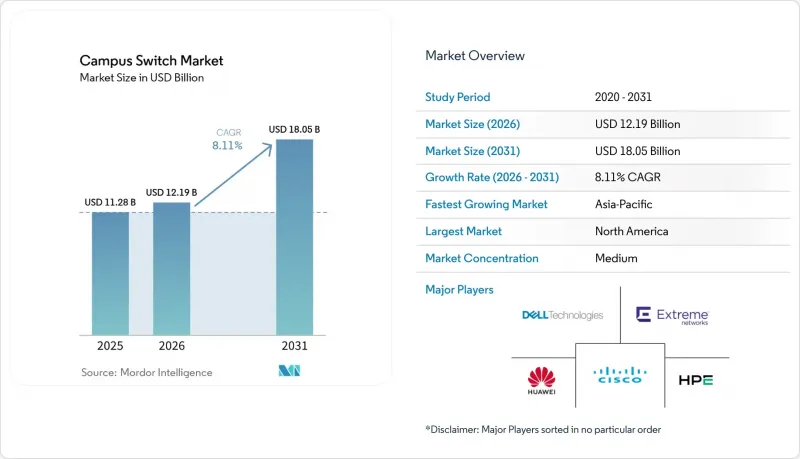

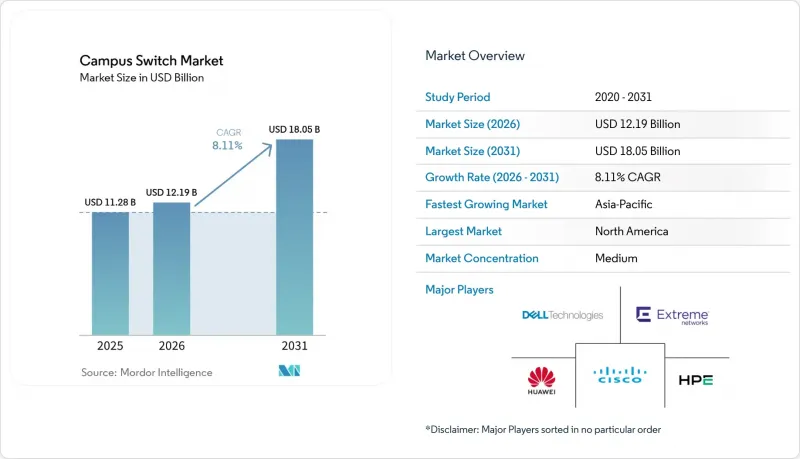

Mordor Intelligence에 의하면, 캠퍼스 스위치 시장 규모는 2025년 112억 8,000만 달러에서 2026년에는 121억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.1%로 성장을 지속하여, 2031년에는 180억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 스위치 유형(고정 구성 스위치 및 모듈형 스위치), 포트 속도(1 GbE 이하, 2.5/5GbE 멀티기가, 10 GbE, 기타), 최종 사용자 기업 규모(대기업, 중소기업), 최종 사용자 산업 분야(교육 기관, 기업·법인 캠퍼스, 정부·공공 부문 캠퍼스, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 캠퍼스 스위치 시장 동향 및 인사이트

Wi-Fi 6/6E 및 Wi-Fi 7의 도입 확대

Wi-Fi 7의 320 MHz 채널은 40 Gbps를 초과하는 최대 처리량을 실현하며, 구형 기가비트 스위칭이 여전히 남아 있는 곳에서는 액세스 계층의 병목 현상을 드러내고 있습니다. 조지타운 대학교는 이러한 병목 현상을 해소하기 위해 2025년에 2.5/5GbE 포트를 갖춘 Catalyst 9000 스위치로 업그레이드했습니다. Hewlett Packard Enterprise의 보고서에 따르면, 신형 Aruba 730 시리즈 액세스 포인트의 60%가 현재 멀티 기가비트 스위치와 세트로 출하되고 있으며, 이로 인해 유선 백홀이 무선 용량을 따라잡아야 할 필요성이 부각되고 있습니다. 화웨이가 2025년 후베이 대학에서 실시한 ‘사무실 광섬유 연결(FTOO)”프로젝트에서는 Wi-Fi 7 무선 모듈과 XGS-PON Pro+를 결합하여 10 Gbps의 엣지 대역폭을 실현했습니다. 이러한 사례를 따르는 캠퍼스가 늘어남에 따라, 액세스 계층의 멀티 기가비트 포트부터 수백 개의 고속 업링크를 집약하는 400 Gbps 스파인에 이르기까지 수요가 연쇄적으로 확대되고 있습니다. 따라서 캠퍼스 스위치 시장은 당초 예상되었던 Wi-Fi 7 도입 주기를 훨씬 뛰어넘어 지속될 견실한 성장 동력을 확보하게 될 것입니다.

스마트 캠퍼스 및 에드테크에 대한 투자 확대

생성형 AI, 몰입형 학습, 통합형 빌딩 제어는 모두 서비스 품질(QoS)을 보장하고 kW 단위의 PoE 전력 공급이 가능한 유선 인프라에 의존하고 있습니다. 2024년에 콜로라도 대학교 볼더 캠퍼스가 “ChatGPT Edu”를 도입한 결과, 코어 네트워크 전체의 일일 피크 트래픽이 10 Tb에 달하고, 400 Gbps 스파인으로의 긴급 업그레이드를 단행할 수밖에 없었습니다. 버밍엄 시티 대학교의 디지털 전환 프로그램에서는 모든 강의실에 설치된 고해상도 카메라와 IoT 센서를 작동시키기 위해 PoE++가 필요했으며, 이를 통해 현대 교육 방식이 스위칭 기능과 밀접하게 연결되어 있음이 부각되었습니다. 아델피 대학의 2025년 멀티기가 네트워크 개편은 캠퍼스 내 학생과 원격지 학생에게 4K 동영상을 전송하는 하이브리드 학습 모델을 지원하기 위한 것입니다. 이러한 프로젝트들에는 네트워크 패브릭의 품질이 학생들의 학습 경험과 교육 기관의 경쟁력에 점점 더 큰 영향을 미칩니다는 공통된 인식이 있으며, 그 결과 재정적으로 신중한 환경 속에서도 스위치에 대한 투자가 점차 확대되고 있습니다.

공립 교육 기관의 예산상 제약

OECD 자료에 따르면, 2023년부터 2024년까지 학생 1인당 실질 고등교육 지출은 3% 감소했으며, IT 시스템 업그레이드를 위한 재량 예산이 압박을 받고 있습니다. 캘리포니아주는 2025-2026 회계연도에 커뮤니티 칼리지에 대한 예산을 5억 달러 삭감함에 따라, 각 학군은 멀티 기가비트 플랫폼 도입을 보류하고, 10년 동안 사용해 온 스위치의 수명을 연장할 수밖에 없는 상황에 처해 있습니다. 세계은행의 통계에 따르면, 저소득 국가에서는 현재 교육 지출 중 디지털 인프라에 할당되는 비중이 10% 미만인 것으로 나타났습니다. 그 결과, 양극화가 발생하고 있습니다. 재정력이 탄탄한 사립대학들은 교체 주기를 앞당기고 있는 반면, 공립 기관들은 교체를 미루고 있어, 이미 도입된 장비가 노후화되었음에도 불구하고 출하 대수는 정체되어 있습니다.

부문별 분석

2025년, 고정형 스위치는 캠퍼스 스위치 시장 점유율의 84.16%를 차지했습니다. K-12(유치원부터 고등학교까지) 및 지사에서는 랙당 48포트를 초과하는 경우가 거의 없기 때문에 2031년까지 고정 구성 스위치가 액세스 클로젯 시장을 계속 독점할 것으로 보입니다. Cisco Catalyst 9300 등의 스태킹 기능을 통해 최대 8대의 장치를 논리적으로 통합할 수 있어, 섀시의 복잡성을 수반하지 않으면서도 일정한 확장성을 실현할 수 있습니다. 그러나 스태킹 케이블은 모듈형 백플레인에서는 피할 수 있는 단일 고장 지점을 도입하게 되며, 이러한 미묘한 차이는 기술 평가에서 점점 더 주목받고 있습니다. 그 결과, 주요 대학의 조달 팀은 배포 계층 및 코어 계층에는 섀시형 제품을 지정하는 한편, 에지 계층에서는 고정형 모델을 유지하는 하이브리드 방식을 채택하고 있습니다. 이러한 접근 방식을 통해 절대적인 대체는 억제되면서도 모듈식 성장의 기세는 유지되고 있습니다.

모듈형 스위치는 2025년에는 매출의 극히 일부에 그쳤으나, 2031년까지 연평균 9.72%의 성장률이 예상되며, 캠퍼스 스위치 시장 전체를 상회하는 성장률을 보일 것으로 전망됩니다. 수만 개의 엔드포인트를 보유한 교육 기관에서는 일부만 장착된 섀시를 도입하고, 학생 수 증가나 IoT 밀도 상승에 맞추어 라인 카드를 확장함으로써 투자 자본 수익률(ROIC)을 향상시킬 수 있습니다. Juniper의 QFX5250은 16슬롯 프레임으로 102.4 Tbps의 처리 능력을 제공하지만, 관리자가 필요한 포트만 활성화할 수 있으므로 초기 투자 비용을 절감할 수 있습니다. Extreme Networks의 7830 역시 마찬가지로, 섀시를 교체할 필요 없이 향후 출시될 800 Gbps 광 모듈을 지원합니다. 반면, 슬롯의 유연성보다는 단순성과 신속한 도입이 중시되는 중소기업에서는 고정 구성 모델이 여전히 인기를 끌고 있습니다.

2025년에는 1 GbE 및 그보다 속도가 낮은 포트가 출하 대수의 44.82%를 차지했으나, Wi-Fi 6E 및 Wi-Fi 7로 인해 기가비트 업링크가 포화 상태에 이르면서 그 점유율은 감소하고 있습니다. 2.5/5GbE 멀티기가 계층은 모든 속도 등급 중에서 가장 빠른 연평균 12.48%의 성장률을 보일 것으로 예상되며, 액세스 계층 하드웨어 분야의 캠퍼스 스위치 시장 전체 규모를 끌어올릴 것으로 전망됩니다. Juniper의 EX4000은 모든 포트에서 멀티기가 및 PoE++를 지원하므로, 교육 기관은 클로젯에서 코어에 이르기까지 단일 SKU로 표준화할 수 있습니다. Juniper의 팬리스 모델 710XP는 소음에 민감한 도서관이나 소규모 교실에 적합하며, 멀티기가가 더 이상 프리미엄 기능이 아님을 보여줍니다.

10기가비트 포트는 서버의 업링크에서 여전히 중요한 역할을 하고 있지만, 25/40 GbE는 주로 데이터센터의 리프 계층에서 그 역할이 제한되어 있습니다. 스파인은 수백 개의 멀티기가비트 플로우를 업스트림으로 집계해야 하기 때문에 100/400 Gbps 집계 기능에 대한 수요는 절대적인 수치로 증가하고 있지만, 캠퍼스 스위치 시장에서의 점유율은 여전히 낮은 수준입니다. 2028년까지 기가비트 포트는 음성 전화기나 구형 센서에 사용될 전망이지만, 한편으로 멀티 기가비트 포트는 신축 및 대규모 개보수 공사에서 표준이 되어, 공급업체가 목표로 삼아야 할 전력 예산, 냉각 요건, 가격대 구성에 변화를 가져올 것입니다.

지역별 분석

아시아태평양은 광섬유가 풍부하게 구축된 캠퍼스 백본에 자금을 지원하는 각국의 AI 전략에 힘입어, 연평균 성장률(CAGR) 9.68%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 일본의 SINET6에서 400 Gbps로 업그레이드함에 따라, 네트워크 전반에 걸쳐 수요가 확산되면서 100 Gbps 분배 스위치의 일괄 구매가 촉진되고 있습니다. 중국에서는 학생 기숙사에서 XGS-PON Pro+로의 급속한 전환으로 인해 구리선으로 인한 제약이 해소되면서 멀티 기가비트 도입이 가속화되고 있습니다. 한편, 인도에서는 AirTrunk가 Lumina CloudInfra를 12억 달러 규모로 인수한 데 이어 데이터센터 확장이 진행됨에 따라, 컴퓨팅 클러스터와 스토리지 클러스터를 통합하기 위한 400 Gbps 스파인이 필요해지고 있습니다.

북미는 Wi-Fi 7의 조기 도입과 적극적인 PoE 확대를 배경으로 2025년 매출의 37.82%를 차지했습니다. 그러나 도입 기반이 성숙해지고 갱신 주기가 길어짐에 따라 성장세는 둔화되고 있습니다. 디지털 형평성과 관련된 연방 정부의 경기 부양책이 단기적인 지출을 뒷받침하고 있지만, 주 및 지방 정부 차원의 재정적 압박으로 인해 특히 커뮤니티 칼리지와 K-12 학군에서의 확장이 제약을 받고 있습니다. 유럽은 여전히 중요한 시장이지만, 긴축 재정으로 인해 제약을 받고 있습니다.

영국과 독일의 교육 기관은 “디지털 우선”의 교육 과정을 추진하고 있지만, 국경을 넘는 조달 프로세스의 복잡성으로 인해 도입 속도가 더딘 상황입니다. 남미 지역의 지출은 브라질과 아르헨티나에 집중되어 있지만, 거시경제의 변동이 수년에 걸친 프로젝트의 진전을 저해하고 있습니다. 중동에서는 다각화 자금을 새로운 스마트 캠퍼스에 투자하고 있으며, 최신 스위칭 기술이 선호되고 있습니다. 아프리카에서는 도입이 아직 초기 단계에 불과하지만, 남아프리카공화국과 나이지리아에 집중되어 있으며, 전력 공급의 신뢰성 문제와 통화 약세로 인해 기부국들의 자금 지원에 맞추어 신중하게 추진되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the campus switch market size is projected to grow from USD 11.28 billion in 2025 to USD 12.19 billion in 2026 and is forecast to reach USD 18.05 billion by 2031 at a CAGR of 8.1% from 2026 to 2031.

This report is Segmented by Switch Type (Fixed Configuration Switches, and Modular Switches), Port Speed (1 GbE and Below, 2. 5/5 GbE Multi-Gig, 10 GbE, and More), End-User Enterprise Size (Large Enterprises, and SMEs), End-User Industry (Education, Enterprise and Corporate Campuses, Government and Public Sector Campuses, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Campus Switch Market Trends and Insights

Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption

Wi-Fi 7's 320 MHz channels deliver headline throughput above 40 Gbps, exposing access-layer bottlenecks wherever legacy gigabit switching persists. Georgetown University upgraded to Catalyst 9000 switches with 2.5/5 GbE ports in 2025 to remove that choke point. Hewlett Packard Enterprise reports that 60% of new Aruba 730 series access points now ship with multi-gig switches, underscoring that the wired backhaul must keep pace with wireless capacity. Huawei's 2025 fiber-to-the-office project at Hubei University pairs Wi-Fi 7 radios with XGS-PON Pro+ to deliver 10 Gbps of edge bandwidth. As more campuses emulate these examples, demand cascades from access-layer multi-gig ports to 400 Gbps spines that aggregate hundreds of high-speed uplinks. The campus switch market, therefore, gains a durable growth engine that extends well beyond the initial Wi-Fi 7 refresh cycle.

Growth in Smart Campus and EdTech Investments

Generative AI, immersive learning, and converged building controls all ride on wired infrastructure that can enforce quality of service and deliver PoE power budgets measured in kilowatts. University of Colorado Boulder's ChatGPT Edu launch in 2024 drove daily peak traffic to 10 Tb across the core, forcing emergency upgrades to 400 Gbps spines. Birmingham City University's digital-transformation program required PoE++ to run high-definition cameras and IoT sensors in every classroom, highlighting that modern pedagogy intertwines with switching capabilities. Adelphi University's 2025 multi-gig refresh aligns with hybrid learning models that stream 4K video to on-campus and remote students. These projects share the thesis that network fabric quality increasingly influences student experience and institutional competitiveness, which, in turn, fuels incremental switch spending even in fiscally cautious environments.

Budgetary Constraints in Public Educational Institutions

OECD data show that real per-student tertiary spending fell 3% between 2023 and 2024, squeezing discretionary budgets for IT upgrades. California cut community-college funding by USD 500 million for fiscal 2025-2026, prompting districts to extend the service life of decade-old switches rather than adopt multi-gig platforms. World Bank figures indicate that lower-income countries now devote under 10% of education outlays to digital infrastructure. The result is a bifurcation: well-endowed private universities advance refresh cycles, while public institutions defer, dampening unit shipments even as the installed base ages.

Other drivers and restraints analyzed in the detailed report include:

- Rising Data Traffic per Student and Staff Device

- Surge in PoE-Powered IoT Edge Devices on Campuses

- Lengthy Cap-Ex Refresh Cycles (7-10 Years)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed Configuration Switches held 84.16% of the campus switch market share in 2025. Fixed configuration switches will still dominate access closets through 2031 because K-12 and branch offices rarely exceed 48 ports per rack. Stacking options, such as Cisco Catalyst 9300, allow logical aggregation of up to 8 units, offering some scale without chassis complexity. However, stacking cables introduces single-point failure domains that modular backplanes avoid, a nuance increasingly acknowledged in technical evaluations. Consequently, procurement teams at flagship universities specify chassis for distribution and core layers while retaining fixed models at the edge, a hybrid approach that tempers absolute displacement but sustains modular growth momentum.

Modular switches captured a modest slice of revenue in 2025 but are forecast to grow 9.72% annually through 2031, outstripping the broader campus switch market. Institutions with tens of thousands of endpoints can install a partially populated chassis and scale line cards as enrollment or IoT density increases, thereby improving return on invested capital. Juniper's QFX5250 delivers 102.4 Tbps in a 16-slot frame, yet administrators can light only the ports they need, reducing upfront cash outlay. Extreme Networks' 7830 likewise supports future 800 Gbps optics without requiring a chassis replacement. In contrast, fixed configuration models remain popular in SMEs, where simplicity and rapid deployment matter more than slot flexibility.

In 2025, 1 GbE and slower ports held 44.82% of shipments, but their share is sliding as Wi-Fi 6E and Wi-Fi 7 saturate gigabit uplinks. The 2.5/5 GbE multi-gig tier is projected to expand 12.48% annually, the fastest of any speed class, lifting the overall campus switch market size for access-layer hardware. Juniper's EX4000 delivers multi-gig and PoE++ across every port, enabling institutions to standardize on a single SKU from the closet to the core. Arista's fanless 710XP caters to noise-sensitive libraries and small classrooms, underscoring that multi-gig is no longer a premium feature.

Ten-gigabit ports remain relevant for server uplinks, while 25/40 GbE remain mostly confined to data-center leaf roles. Demand for 100/400 Gbps aggregation climbs in absolute terms because spines must funnel hundreds of multi-gig flows upstream, but their share within the campus switch market remains modest. By 2028, gigabit ports are expected to serve voice handsets and legacy sensors, whereas multi-gigabit becomes the default across new construction and major renovations, changing the mix of power budgets, cooling requirements, and price bands that vendors must target.

Complete Report Scope:

- By Switch Type

- Fixed Configuration Switches

- Modular Switches

- By Port Speed

- 1 GbE and Below

- 2.5/5 GbE Multi-Gig

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE and Above

- By End-user Enterprise Size

- Large Enterprises

- SMEs

- By End-User

- Education (K-12 and Higher Education)

- Enterprise and Corporate Campuses

- Government and Public Sector Campuses

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific is the fastest-growing region at a projected 9.68% CAGR, fueled by national AI strategies that bankroll fiber-rich campus backbones. Japan's SINET6 400 Gbps upgrade cascades demand across the network, prompting bulk purchases of 100 Gbps distribution switches. China's leapfrog to XGS-PON Pro+ in student housing eliminates copper limitations and accelerates multi-gig adoption, while India's data-center build-out following AirTrunk's USD 1.2 billion acquisition of Lumina CloudInfra requires 400 Gbps spines to marry compute and storage clusters.

North America held 37.82% of 2025 revenue on the strength of early Wi-Fi 7 deployments and aggressive PoE rollouts. Growth, however, decelerates as the installed base matures and refresh cycles lengthen. Federal stimulus tied to digital equity sustains near-term spending, but fiscal pressure at state and local levels tempers expansion, especially in community colleges and K-12 districts. Europe remains significant yet constrained by austerity budgets.

Institutions in the United Kingdom and Germany pursue digital-first curricula, but cross-border procurement complexity slows velocity. South America's spending centers on Brazil and Argentina, but macroeconomic volatility hampers multi-year projects. The Middle East channels diversification funds into greenfield smart campuses, favoring the latest switching technology. Africa's nascent adoption concentrates in South Africa and Nigeria, where power reliability and currency depreciation dictate cautious rollouts aligned with donor financing.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Dell Technologies Inc.

- Alcatel-Lucent Enterprise International SAS

- Extreme Networks, Inc.

- Fortinet, Inc.

- NETGEAR, Inc.

- TP-Link Technologies Co., Ltd.

- D-Link Corporation

- Ubiquiti Inc.

- Edgecore Networks Corporation

- Allied Telesis Holdings Corporation

- Ruijie Networks Co., Ltd.

- Nokia Corporation

- Cambium Networks

- Ruckus Networks

- Byezzy Tech

- Zyxel Communications Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTON

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption

- 4.2.2 Growth in Smart Campus and EdTech Investments

- 4.2.3 Rising Data Traffic per Student and Staff Device

- 4.2.4 Surge in PoE-Powered IoT Edge Devices on Campuses

- 4.2.5 Increasing Campus Cyber-Resilience Requirements

- 4.2.6 Vendor Neutral Open-Networking Push (SONiC, NOS Disaggregation)

- 4.3 Market Restraints

- 4.3.1 Budgetary Constraints in Public Educational Institutions

- 4.3.2 Lengthy Cap-Ex Refresh Cycles (7-10 Years)

- 4.3.3 Skills Shortage in Network Automation and SDN

- 4.3.4 Supply-Chain Volatility for ASICs and Optics

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Fixed Configuration Switches

- 5.1.2 Modular Switches

- 5.2 By Port Speed

- 5.2.1 1 GbE and Below

- 5.2.2 2.5/5 GbE Multi-Gig

- 5.2.3 10 GbE

- 5.2.4 25/40 GbE

- 5.2.5 100 GbE

- 5.2.6 400 GbE and Above

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By End-User

- 5.4.1 Education (K-12 and Higher Education)

- 5.4.2 Enterprise and Corporate Campuses

- 5.4.3 Government and Public Sector Campuses

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Arista Networks, Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Alcatel-Lucent Enterprise International SAS

- 6.4.7 Extreme Networks, Inc.

- 6.4.8 Fortinet, Inc.

- 6.4.9 NETGEAR, Inc.

- 6.4.10 TP-Link Technologies Co., Ltd.

- 6.4.11 D-Link Corporation

- 6.4.12 Ubiquiti Inc.

- 6.4.13 Edgecore Networks Corporation

- 6.4.14 Allied Telesis Holdings Corporation

- 6.4.15 Ruijie Networks Co., Ltd.

- 6.4.16 Nokia Corporation

- 6.4.17 Cambium Networks

- 6.4.18 Ruckus Networks

- 6.4.19 Byezzy Tech

- 6.4.20 Zyxel Communications Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment