|

시장보고서

상품코드

2073141

네트워크 스위치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Network Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

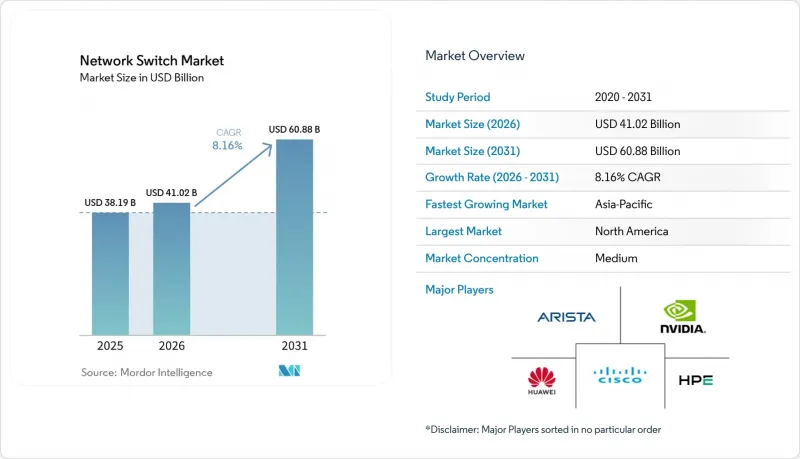

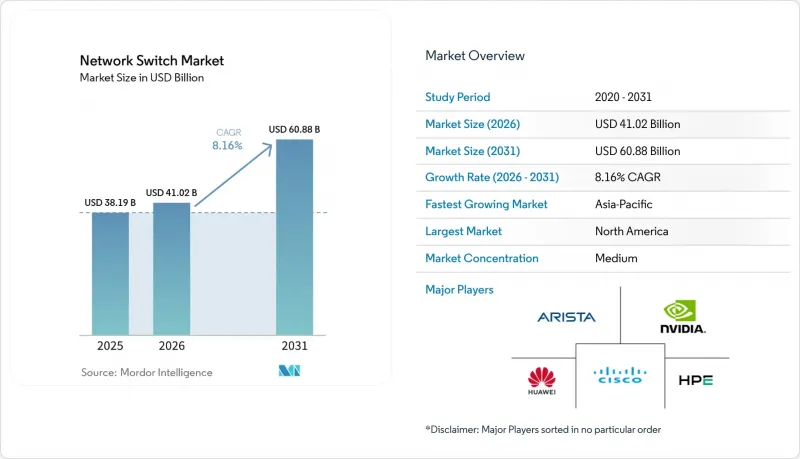

Mordor Intelligence에 의하면, 네트워크 스위치 시장 규모는 2025년 381억 9,000만 달러, 2026년 410억 2,000만 달러에서 2031년까지 608억 8,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.16%를 나타낼 전망입니다.

본 보고서는 스위치 유형(고정 구성 스위치 및 모듈형 스위치), 포트 속도(1 GbE 이하, 2.5/5GbE 멀티기가, 10 GbE, 기타), 전력 공급 능력(비 PoE 스위치, PoE 지원 스위치), 최종 사용자(클라우드 및 데이터센터 제공업체, 기업, 통신 서비스 제공업체, 기타), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 네트워크 스위치 시장 동향과 인사이트

하이퍼스케일 데이터센터의 확장

하이퍼스케일 사업자들은 계속해서 15-20 GW의 용량을 확충하고 있지만, 변압기 부족으로 인해 신규 건설이 규제상 대기 목록에 머물러 있는 상황이라, 사업자들은 와트당 연산 밀도를 높이기 위해 기존 데이터센터 내 네트워크 설비를 과도하게 확충할 수밖에 없는 실정입니다. GPU 수 증가에 따라 비차단형 800 GbE 패브릭이 필요해졌으며, 이로 인해 수년 동안 지속되어 온 포트당 수익의 감소 추세가 주춤하고 있습니다. NVIDIA의 Spectrum-X는 Spectrum-4 스위치와 첨단 혼잡 제어 소프트웨어를 결합하여 xAI Colossus 슈퍼컴퓨터에서 95%의 네트워크 처리량을 달성했습니다. 그 결과, AI 전용 텔레메트리 기능을 갖추지 않은 범용 반도체 공급업체들은 스파인 계층에서 설계 채택 기회를 놓칠 위험에 직면해 있습니다.

더 빠른 포트로의 전환

대규모 언어 모델의 추론을 수행하는 조직이 100 GbE 백본을 넘어설 것으로 예상에 따라, 2025년에는 800 GbE 광 모듈의 전 세계 출하량이 60% 증가했습니다. Arista의 7700R5는 1 랙 유닛에 32개의 800 GbE 포트를 탑재하고 있어, 클라우드 사업자는 3계층 패브릭을 2계층으로 통합하여 지연 시간을 30% 단축할 수 있습니다. NVIDIA가 도입한 코패키지드 옵틱스는 전기-광 변환 과정을 제거함으로써 테라비트당 에너지 소비를 40% 절감할 가능성이 있습니다. 기존 네트워크 OS는 대칭적인 속도를 전제로 하고 있기 때문에 소프트웨어의 복잡성이 증가하고 있으며, 혼합 링크 속도를 추상화하는 인텐트 기반 자동화에 대한 수요가 높아지고 있습니다.

화이트박스 ODM 스위치로 인한 가격 압박

각 하이퍼스케일러 기업들은 Edgecore 및 Celestica의 베어메탈 스위치에 SONiC을 탑재함으로써 20-30%의 비용 절감을 실현하고 있으며, 2025년 11월 출시 버전에서는 800 GbE 지원 기능이 추가되었습니다. 마이크로소프트, 메타, 구글은 이미 100만 대 이상의 화이트박스 기기를 운영 중이며, 이는 브랜드 제조업체들의 매출 총이익률을 압박하고 있습니다. 주니퍼가 2025년에 휴렛 팩커드 엔터프라이즈에 매각된 것은 상품화 추세에 대응하기 위해 AI 네이티브 소프트웨어를 서버와 함께 번들로 제공하는 것을 목적으로 했습니다. SONiC가 역할 기반 접근 제어 등의 엔터프라이즈 기능을 갖추며 성숙해감에 따라, 중견 기업 고객도 이탈하게 되어 프리미엄 제품의 잠재 수익이 축소될 가능성이 있습니다.

부문별 분석

2025년, 고정형 스위치는 네트워크 스위치 시장 점유율의 71.45%를 차지했습니다. 이는 기업들이 여전히 단순성, 도입의 용이성, 그리고 초기 설비 투자 비용 절감을 우선시하고 있기 때문입니다. 이러한 플러그 앤 플레이 특성과 전문적인 관리 노하우가 별로 필요하지 않다는 점 때문에 예측 가능한 워크로드를 가진 캠퍼스나 지사 환경에서 특히 매력적입니다. 한편, 통신 사업자들이 장기적인 투자 보호와 확장성을 점점 더 중요시함에 따라 모듈형 스위치 시장은 연평균 성장률(CAGR) 9.62%로 성장할 것으로 전망됩니다. Arista Networks사의 "7800R4"와 같은 플랫폼에서는 고객이 400 GbE 및 800 GbE 라인 카드를 단계적으로 추가할 수 있으므로, 고비용이 드는 전면 교체를 하지 않고도 용량을 업그레이드할 수 있습니다.

AI 중심의 데이터센터 환경에서는 대역폭 수요가 기하급수적으로 증가하고, 보다 유연한 아키텍처가 요구되기 때문에 상황이 크게 다릅니다. 이러한 시나리오에서 NVIDIA Corporation의 Spectrum-X 레퍼런스 아키텍처는 향후 확장성과 동서 방향 트래픽 증가를 효율적으로 지원하기 위해 모듈형 스파인 스위치를 중시하고 있습니다. 고정형 스위치는 비용 효율성과 컴팩트한 설계 덕분에, 특히 표준화된 랙 환경에서 Top-of-Rack(ToR) 구축 방식의 주류를 여전히 차지하고 있습니다.

2025년 네트워크 스위치 시장 규모 중, 캠퍼스 엔드포인트와 관련된 기존 1 GbE 이하 포트가 32.40%를 차지했습니다. 400 GbE 이상의 포트는 연평균 성장률(CAGR) 10.61%를 기록하며, 네트워크 스위치 시장 전체보다 245 베이시스 포인트 높은 성장세를 보이고 있습니다. 한편, 400 GbE 이상의 포트는 하이퍼스케일 및 AI로 인한 대역폭 요구 사항 증가에 힘입어 연평균 성장률(CAGR) 10.61%로 확대되고 있으며, 이는 시장 전체 성장률을 245 베이시스 포인트 상회하는 수치입니다. 광트랜시버의 비용 감소로 인해 고속화로의 전환이 훨씬 더 경제적으로 가능해지면서, 기업들이 차세대 스위칭 아키텍처를 도입하려는 의지가 높아지고 있습니다.

멀티 기가비트급 2.5/5GbE 업링크는 WiFi 7의 업데이트 주기에 따라 점차 보급되고 있습니다. 이 사이클에서는 고밀도 디바이스 환경과 고도의 용도를 지원하기 위해 높은 처리량과 낮은 지연 시간이 필수적입니다. 이러한 동향은 Cisco Systems, Inc.의 "Catalyst 9000X"와 같은 플랫폼에도 반영되어 있으며, 이 제품은 400 GbE 업링크와 48개의 멀티 기가비트 PoE++ 포트를 통합하여, 지속적으로 발전하는 기업의 액세스 요구 사항을 충족하고 있습니다. 실리콘 수준에서는 브로드컴의 "Tomahawk 6" 등의 혁신적인 기술을 통해, 기존 400 GbE 칩과 동등한 전력 소비 범위를 유지하면서 800 GbE의 성능을 실현하고 있습니다. 이로 인해 저속 스위칭 계층의 노후화가 가속화되면서, 기업들은 더 대용량의 네트워크 인프라로 전환해야 하는 상황에 직면해 있습니다.

지역별 분석

2025년 북미, 버지니아주, 오리건주, 텍사스주 내 하이퍼스케일 시설의 확대 및 인근 노드에서의 광섬유 집약형 스위치를 지원하는 424억 5,000만 달러 규모의 BEAD 프로그램의 뒷받침을 받아, 전 세계 매출의 36.88%를 계속 차지했습니다. 클라우드 사업자들이 컨텐츠 전송 지연을 줄이기 위해 자금 지원을 받은 광섬유 노선 근처에 엣지 시설을 코로케이션함에 따라, 연방 정부의 인센티브가 민간 투자를 뒷받침하고 있습니다. 캐나다에서도 규모는 작지만, 주 정부의 광대역 지원금을 통해 비슷한 추세가 나타나고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 9.72%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도가 계획하고 있는 300억-360억 달러 규모의 투자는 통신탑의 광섬유화율을 70% 가까이 끌어올리는 것을 목표로 하고 있으며, 메트로 링 내 집약 스위치에 대한 수요를 촉진하고 있습니다. 중국에서는 정책은행이 훈련 데이터를 국내에 보관해야 하는 AI 스타트업 기업에 대한 저금리 대출을 확대하고 있어, 내륙 지역의 성에서 데이터센터 건설이 가속화되고 있습니다. 일본과 한국에서는 로봇 공학 분야에 타임 센시티브 네트워킹(TSN)을 도입하고 있으며, 프라이빗 5G 캠퍼스에서는 결정론적 이더넷 패브릭이 필요로 하고 있습니다.

유럽에서는 에코디자인 지침에 따라 Tier 2 에너지 효율 목표를 달성하기 위해 비용이 많이 드는 ASIC 재설계가 의무화되어 있어, 성장세가 둔화되고 있습니다. 독일과 네덜란드에서는 절수형 냉각 솔루션을 우선적으로 채택하고 있으며, 침지 냉각이 가능한 섀시를 갖춘 공급업체를 우대하는 조달 기준이 추가되었습니다. 남유럽의 통신 사업자들은 지방의 광대역 사업에 주력하고 있지만, 거시경제적인 역풍으로 인해 자본 집약도가 억제되고 있습니다. 중동에서는 사우디아라비아와 아랍에미리트가 800 GbE 스파인을 갖춘 AI 전용 캠퍼스를 구축하고 있는 반면, 아프리카에서는 불안정한 전력망과 제한된 광섬유 회선으로 인해 어려움을 겪고 있음에도 불구하고, 모바일 백홀의 4G 및 초기 단계의 5G로의 업그레이드가 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the network switch market size is projected to expand from USD 38.19 billion in 2025 and USD 41.02 billion in 2026 to USD 60.88 billion by 2031, registering a CAGR of 8.16% between 2026 to 2031.

This report is Segmented by Switch Type (Fixed Configuration Switches, and Modular Switches), Port Speed (1 GbE and Below, 2. 5/5 GbE Multi-Gig, 10 GbE, and More), Power Capability (Non-PoE Switches, and PoE-Capable Switches), End-User (Cloud and Data Center Providers, Enterprise, Telecommunication Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Network Switch Market Trends and Insights

Hyperscale Data Center Expansion

Hyperscale operators continue to add 15-20 GW of capacity, yet transformer shortages keep new builds in regulatory queues, prompting operators to over-provision networking in existing halls to raise compute density per watt. Rising GPU counts require non-blocking 800 GbE fabrics, reversing the multi-year decline in revenue per port. NVIDIA's Spectrum-X reached 95% network throughput in the xAI Colossus supercomputer by pairing Spectrum-4 switches with advanced congestion-control software. As a result, merchant-silicon vendors that lack AI-specific telemetry risk design-win losses at the spine layer.

Migration to Higher Port Speeds

Global shipments of 800 GbE optical modules grew 60% in 2025 as organizations running large-language-model inference moved beyond 100 GbE backbones. Arista's 7700R5 packs 32 800 GbE ports in one rack unit, enabling cloud operators to collapse three-tier fabrics into two tiers and cut latency by 30%. Co-packaged optics introduced by NVIDIA eliminate electrical-optical conversion and may cut energy per terabit by 40%. Software complexity rises because legacy network operating systems assume symmetrical speeds, pushing demand for intent-based automation that abstracts mixed link rates.

Price Pressure from White-Box ODM Switches

Hyperscalers save 20-30% by loading SONiC on bare-metal switches from Edgecore or Celestica, and the November 2025 release added 800 GbE support. Microsoft, Meta, and Google already run more than one million white-box devices, eroding gross margins for branded vendors. Juniper's 2025 sale to Hewlett Packard Enterprise aimed to bundle AI-native software with servers to combat commoditization. As SONiC matures with enterprise features like role-based access control, mid-market customers may also defect, compressing addressable revenue for premium products.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI-Optimized Ethernet Fabrics

- Proliferation of Cloud-Managed Networking Platforms

- Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed configuration switches held 71.45% of the network switch market share in 2025, as enterprises continue to prioritize simplicity, ease of deployment, and lower upfront capital expenditure. Their plug-and-play nature and reduced need for specialized management expertise make them especially attractive for campus and branch environments with predictable workloads. Modular switches, however, are projected to expand at a 9.62% CAGR as operators increasingly focus on long-term investment protection and scalability. Platforms such as the 7800R4 from Arista Networks allow customers to incrementally add 400 GbE and 800 GbE line cards, enabling capacity upgrades without costly forklift replacements.

The calculus shifts significantly in AI-driven data center environments, where bandwidth demands grow exponentially, requiring more flexible architectures. In such scenarios, NVIDIA Corporation's Spectrum-X reference architecture emphasizes modular spine switches to efficiently support future scaling and east-west traffic expansion. Fixed-configuration switches still dominate top-of-rack deployments due to their cost efficiency and compact design, particularly in standardized rack environments.

Legacy 1 GbE-and-below accounted for 32.40% of the network switch market size in 2025, tied to campus endpoints. Ports rated 400 GbE and above are growing at a 10.61% CAGR, outpacing the network switch market by 245 basis points. Meanwhile, ports rated 400 GbE and above are expanding at a 10.61% CAGR, outpacing the overall market by 245 basis points, driven by hyperscale and AI-driven bandwidth requirements. The declining cost of optical transceivers has made the transition to higher speeds significantly more economical, accelerating enterprise willingness to adopt next-generation switching architectures.

Multi-gig 2.5/5 GbE uplinks are gaining traction in the WiFi 7 refresh cycle, where higher throughput and low latency are essential for supporting dense device environments and advanced applications. This trend is reflected in platforms like the Catalyst 9000X from Cisco Systems, Inc., which integrates 400 GbE uplinks alongside 48 multi-gig PoE++ ports to address evolving enterprise access needs. At the silicon level, innovations such as the Tomahawk 6 from Broadcom Inc. enable 800 GbE performance while maintaining power envelopes similar to those of earlier 400 GbE chips, thereby accelerating the obsolescence of slower switching tiers and pushing enterprises toward higher-capacity network infrastructure.

Complete Report Scope:

- By Switch Type

- Fixed Configuration Switches

- Modular Switches

- By Port Speed

- 1 GbE and Below

- 2.5/5 GbE Multi-Gig

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE and Above

- By Power Capability

- Non-PoE Switches

- PoE-Capable Switches

- By End-User

- Cloud and Data Center Providers

- Enterprise (Commercial Offices & Campuses)

- Telecommunication Service Providers

- Government and Defense

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America maintained 36.88% of global revenue in 2025, lifted by hyperscale footprints in Virginia, Oregon, and Texas, and by the USD 42.45 billion BEAD program that underwrites fiber aggregation switches at neighborhood nodes. Federal incentives amplify private spending as cloud operators co-locate edge facilities near funded fiber routes to lower content-delivery latency. Canada follows similar patterns through provincial broadband grants, albeit at smaller scale.

Asia-Pacific is the fastest-growing region at a 9.72% CAGR. India's planned USD 30-36 billion investment aims to lift tower fiberization toward 70%, triggering demand for aggregation switches in metro rings. China accelerates data-center construction in inland provinces as policy banks extend low-rate loans to AI start-ups that must keep their training data within national borders. Japan and South Korea deploy Time-Sensitive Networking for robotics, requiring deterministic Ethernet fabrics in private 5G campuses.

Europe is growing more slowly as the EcoDesign Directive forces costly ASIC redesigns to meet Tier 2 energy-efficiency targets. Germany and the Netherlands prioritize water-efficient cooling solutions, adding purchasing criteria that favor vendors with immersion-ready chassis. Southern European carriers focus on rural broadband, but macroeconomic headwinds curb capital intensity. In the Middle East, Saudi Arabia and the United Arab Emirates build AI-focused campuses with 800 GbE spines, while Africa upgrades mobile backhaul to 4G and early 5G, held back by unreliable grids and limited fiber.

- Cisco Systems, Inc.

- Arista Networks, Inc.

- NVIDIA Corporation

- Extreme Networks, Inc.

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- Juniper Networks, Inc.

- Dell Technologies Inc.

- Broadcom Inc.

- D-Link Corporation

- NETGEAR, Inc.

- Ubiquiti Inc.

- Allied Telesis Holdings K.K.

- Edgecore Networks Corporation

- Ruijie Networks Co., Ltd.

- Shandong New H3C Technologies Co., Ltd.

- Zyxel Communications Corporation

- Celestica Inc.

- Buffalo, Inc.

- QNAP Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale Data Center Expansion

- 4.2.2 Migration to Higher Port Speeds

- 4.2.3 Proliferation of Cloud-Managed Networking Platforms

- 4.2.4 Government Broadband Stimulus Funds

- 4.2.5 Integration of AI-Optimized Ethernet Fabrics

- 4.2.6 Rise of Private 5 G Campus Networks Requiring TSN

- 4.3 Market Restraints

- 4.3.1 Price Pressure from White-Box ODM Switches

- 4.3.2 Semiconductor Supply-Chain Volatility

- 4.3.3 Energy-Efficiency Regulations Raising Design Complexity

- 4.3.4 Skills Gap in High-Speed Optical Switching Technologies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Fixed Configuration Switches

- 5.1.2 Modular Switches

- 5.2 By Port Speed

- 5.2.1 1 GbE and Below

- 5.2.2 2.5/5 GbE Multi-Gig

- 5.2.3 10 GbE

- 5.2.4 25/40 GbE

- 5.2.5 100 GbE

- 5.2.6 400 GbE and Above

- 5.3 By Power Capability

- 5.3.1 Non-PoE Switches

- 5.3.2 PoE-Capable Switches

- 5.4 By End-User

- 5.4.1 Cloud and Data Center Providers

- 5.4.2 Enterprise (Commercial Offices & Campuses)

- 5.4.3 Telecommunication Service Providers

- 5.4.4 Government and Defense

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Arista Networks, Inc.

- 6.4.3 NVIDIA Corporation

- 6.4.4 Extreme Networks, Inc.

- 6.4.5 Hewlett Packard Enterprise Development LP

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Juniper Networks, Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Broadcom Inc.

- 6.4.10 D-Link Corporation

- 6.4.11 NETGEAR, Inc.

- 6.4.12 Ubiquiti Inc.

- 6.4.13 Allied Telesis Holdings K.K.

- 6.4.14 Edgecore Networks Corporation

- 6.4.15 Ruijie Networks Co., Ltd.

- 6.4.16 Shandong New H3C Technologies Co., Ltd.

- 6.4.17 Zyxel Communications Corporation

- 6.4.18 Celestica Inc.

- 6.4.19 Buffalo, Inc.

- 6.4.20 QNAP Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment