|

시장보고서

상품코드

2073143

산업용 네트워크 스위치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Industrial Network Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

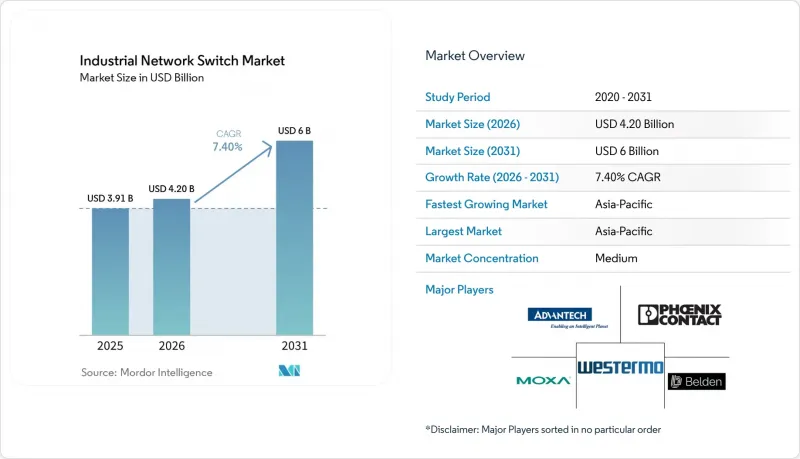

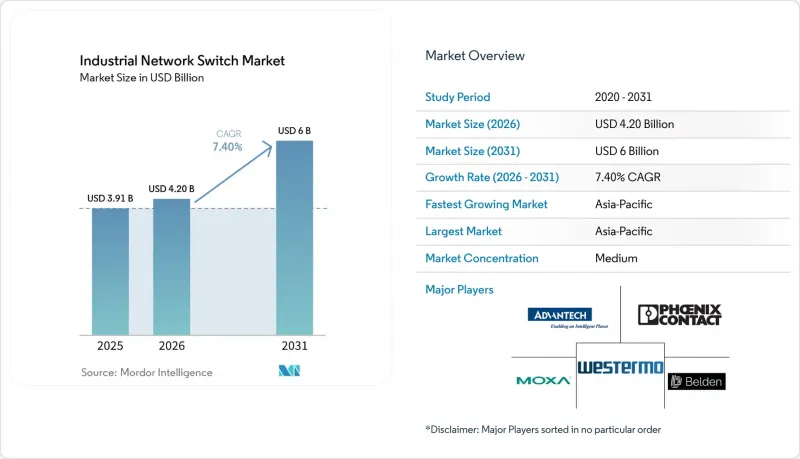

Mordor Intelligence에 의하면, 산업용 네트워크 스위치 시장 규모는 2025년 39억 1,000만 달러에서 2026년에는 42억 달러로 확대되어 2031년까지 60억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 7.4%로 성장할 전망입니다.

본 보고서는 유형별(관리형 스위치, 비관리형 스위치, 스마트/웹 관리형 스위치), 포트 수별(2-8포트, 9-16포트, 17-24포트, 25-48포트, 기타), 포트 속도별(패스트 이더넷 100 Mbps, 기타), PoE 지원 기능(PoE 스위치 및 비 PoE 스위치), 업종(제조업 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 산업용 네트워크 스위치 시장 동향 및 분석

인더스트리 4.0에 따른 자동화의 급속한 확대

공장 운영자들은 기존의 필드버스 아일랜드를 디지털 트윈, AI를 활용한 결함 감지, 그리고 폐쇄 루프 품질 관리를 지원하는 통합 이더넷 패브릭으로 전환하고 있습니다. 2026년 시스코의 조사에 따르면, 제조업체의 61%가 이미 현장에 인공지능을 도입했으며, 97%가 연결 밀도의 향상을 기대하고 있어, 이는 매니지드 스위치 포트에 대한 수요 증가를 뒷받침하고 있습니다. 지멘스는 소프트웨어 정의 생산 셀로 전환한 후, 인도네시아의 시범 생산 라인에서 49%의 생산성 향상을 확인했습니다. 자동차 조립 제조업체에서는 이더넷 기반의 모션 제어가 표준화되고 있으며, 이에 따라 스위치의 리프레시 주기가 빨라지고, 액세스 계층의 대역폭이 패스트 이더넷에서 10기가비트로 향상되고 있습니다. 따라서 산업용 네트워크 스위치 시장은 포트의 고속화와 결정론적 트래픽 스케줄링을 촉진하는 모든 새로운 엣지 AI 워크로드의 혜택을 누리고 있습니다. NETCONF 인터페이스와 VLAN 템플릿을 함께 제공하는 벤더는 공장 관리자가 설정의 복잡성을 극복할 수 있도록 지원함으로써 시운전 기간을 최대 30% 단축하고 있습니다.

결정론적 이더넷을 위한 시간 민감형 네트워킹의 급속한 확산

IEEE 802.1AS에 의한 시간 동기화, 802.1Qbv에 의한 시간 인식형 셰이핑, 그리고 802.1Qbu에 의한 프레임 선점 기능을 결합함으로써, 이더넷은 필드버스 수준의 결정성을 실현할 수 있게 됩니다. 이는 폐쇄 루프 모션 및 안전 셀에 있어 필수적인 요건입니다. 2024년에 발표된 IEC/IEEE 60802 표준에서는 서브 마이크로초 수준의 지터를 요구 사항으로 하는 산업용 TSN 프로파일이 규정되었습니다. 프랑스의 송전망 운영사 RTE는 2025년, 400 kV 변전소에서 다중 벤더 간 TSN 상호운용성을 검증하고, 캐리어급의 견고성을 입증했습니다. 자동차용 이더넷 위원회도 카메라, LiDAR 및 무선 업데이트 스트림을 동시에 전송하기 위한 TSN 스케줄링을 승인했습니다. 그 결과, 산업용 네트워크 스위치 시장에서는 단일 하드웨어 플랫폼에서 TSN과 기존 산업용 프로토콜을 모두 준수하는 장치에 대한 수주가 급증하고 있습니다. IEEE 1588 기반의 클럭 복구 및 핫 스탠바이 경로를 통합한 공급업체는 저가형 시장에 새로 진입한 업체들에 대해 기술적 경쟁 우위를 확보하고 있습니다.

운영 기술(OT) 네트워크의 사이버 보안 취약점

IT와 OT가 융합된 토폴로지에서는 패치가 적용되지 않은 펌웨어나 기본 인증 정보를 악용하는 랜섬웨어에 대해 기존의 PLC나 HMI가 노출되어 있습니다. CISA는 2025년, 원격 코드 실행을 가능하게 하는 스위치의 취약점을 해결하기 위해 47건의 권고문을 발표했습니다. 2026년 초 현재, 이미 도입된 산업용 스위치 중 IEC 62443-4-2의 보안 수준을 충족하는 제품은 30% 미만입니다. Dragos사의 보고서에 따르면, 2025년에는 산업 조직의 68%가 적어도 한 건의 사이버 사고를 기록했으며, 그중 42%의 사례에서 이더넷 장치가 첫 번째 침입 경로가 되었습니다. 피닉스 콘택트사의 “"FL Switch 2000" 는 2025년 12월에 IEC 62443-4-2 인증을 취득했으며, 규정 준수는 가능하지만 비용이 많이 든다는 사실이 입증되었습니다. 세분화되지 않은 네트워크에 대한 보험료의 급등은 단기적인 구매 결정을 더욱 위축시키고 있습니다.

부문별 분석

2025년, 매니지드 스위치는 산업용 네트워크 스위치 시장의 65.8%를 차지하고, 인더스트리 4.0 생산 분야에서 VLAN 세분화, QoS 큐잉 및 원격 진단이 필수 요소로 대두됨에 따라 2031년까지 연평균 성장률(CAGR) 10.3%로 성장할 것으로 전망됩니다. 디지털 변전소를 도입하는 전력 회사는 10밀리초 미만의 장애 전환을 요구하고 있지만, 이는 비관리형 모델에서는 제공할 수 없습니다. 스마트형이나 웹 관리형 모델은 CLI의 복잡함 없이 브라우저 기반 GUI를 제공함으로써 소규모 공장에서 선호되고 있습니다. 사이버 보안 인증을 획득한 매니지드 스위치는 현재 25-40%의 가격 프리미엄이 붙고 있지만, 중요 인프라 구매자에게 있어 규정 준수는 절대 양보할 수 없는 요건입니다.

대조적으로, 비관리형 스위치는 단일 장비가 독립적으로 설치된 환경에서는 여전히 유용하지만, 안전 관련 트래픽에 결정론적인 우선순위 지정이 필요한 상황에서는 역풍을 맞고 있습니다. 따라서 각 벤더사는 고객이 나중에 관리 기능을 활성화할 수 있는 펌웨어 업그레이드 기능에 투자함으로써, 보급형 하드웨어의 미래 가치를 확보하고 있습니다. 산업용 네트워크 스위치 시장이 성숙해짐에 따라, 분석가들은 2020년대 중반까지 매니지드 스위치 시장 점유율이 70%를 넘어설 것으로 예측하고 있으며, 이에 따라 일원적으로 오케스트레이션되고 API 기반의 패브릭으로의 전환이 더욱 가속화될 것으로 보입니다.

2-8포트급 스위치는 2025년에 35.6%의 시장 점유율을 차지하며, 소형 머신 셀에 대응하고 있습니다. 한편, 48포트 이상의 스위치는 자동차, 전자, 반도체 팹 분야에서 엣지 캐비닛을 집약 계층의 랙에 통합하는 추세가 확대됨에 따라, 2031년까지 연평균 성장률(CAGR) 9.3%를 나타낼 것으로 전망됩니다. 자동차 생산 라인에서는 초당 수천 프레임의 비전 데이터를 처리하기 위해, 10G 업링크를 제공하는 48포트의 기가비트 액세스 블록이 도입되어 있습니다. 포트 밀도가 높을수록 포트당 비용은 절감되지만, 이중화된 PSU나 핫스왑이 가능한 팬 트레이를 채택하지 않는 한 단일 고장 지점이 발생할 가능성이 있습니다.

그 때문에 제어실에서는 모듈식 PSU 베이를 갖춘 견고한 19인치 섀시가 DIN 레일식 박스를 점차 대체하고 있습니다. 또한, 각 벤더사는 소프트웨어 정의 프로비저닝을 추진하고 있으며, 이를 통해 엔지니어는 수동으로 패치를 적용할 필요 없이 미사용 포트를 재사용할 수 있게 됩니다. 가상화가 보급됨에 따라 48포트 이상의 산업용 네트워크 스위치 시장 규모는 꾸준히 확대될 전망이며, 특히 케이블 감축을 목표로 하는 기존 플랜트(브라운필드)에서 이러한 경향이 두드러집니다.

지역별 분석

아시아태평양은 2025년에 산업용 네트워크 스위치 시장의 37.2%를 차지하고, 2031년까지 연평균 성장률(CAGR) 9.7%로 성장할 것으로 전망됩니다. 중국의 '중국 제조 2025' 계획, 인도의 "생산 연계형 인센티브(PLI)", 그리고 동남아시아의 스마트 팩토리 지원금이 더해져, 수년에 걸친 설비 투자 주기를 뒷받침하고 있습니다. 지멘스는 인도네시아에서 진행한 시범 사업에서 49%의 생산성 향상이 확인되었다는 점을 근거로, 2030년까지 공장 자동화에 대한 지출이 1,258억 4,000만 달러에 달할 가능성이 있다고 추산하고 있습니다. 일본과 한국의 반도체 공장에서는 5nm 리소그래피의 동기화를 위해 TSN 스위치가 필요한 반면, 인도의 태양광 발전 단지에서는 재생에너지의 간헐성을 보완하기 위해 IEC 61850 규격을 지원하는 장비가 도입되고 있습니다. 대만과 중국의 국내 공급업체들은 가격 면에서 기존 기업들보다 저렴하지만, 1차 자동차 및 항공우주 OEM 업체들은 여전히 24시간 지원 체제를 갖춘 세계 공급업체를 선호하고 있습니다.

북미에서는 527억 달러 규모의 “CHIPS and Science Act”의 혜택을 받고 있으며, 이 법은 인텔의 애리조나주 팹(200억 달러), TSMC의 피닉스 캠퍼스(400억 달러), 마이크론의 뉴욕 생산 라인(200억 달러), 삼성의 텍사스주 시설(170억 달러)에 대한 자금 지원을 보장하고 있습니다. 각 팹에서는 리소그래피, 계측 및 자동 소재 이송을 동기화하기 위해 TSN을 지원하는 10G 및 100G 패브릭이 채택되고 있습니다. 미국 및 캐나다 전역의 전력 회사들은 NERC CIP를 준수하기 위해 변전소의 현대화를 추진하고 있으며, 이에 따라 IEC 62443을 준수하는 스위치에 대한 수요가 증가하고 있습니다. 멕시코에서 니어쇼어링의 확산에 힘입어, 자동차 클러스터가 미국의 라인 아키텍처를 모방함에 따라 해당 지역의 매출은 더욱 확대되고 있습니다.

유럽 시장은 스마트 그리드 구축, 자동차의 전기화, 그리고 NIS2 사이버 보안 규정에 따라 영향을 받습니다. RTE가 400 kV 사이트 전역에 걸쳐 다중 공급업체 TSN을 도입한 것은 상업적 실현 가능성을 입증했으며, 다른 송전망 사업자들에게 선례가 되고 있습니다. 독일의 자동차 제조업체들은 현재 카메라 및 LiDAR 스트림을 관리하기 위해 이더넷 백본을 도입하고 있으며, 이로 인해 저지연 스위치에 대한 현지 수요가 증가하고 있습니다. EU의 '디지털 디케이드' 계획에 따르면, 2030년까지 기업의 클라우드 및 빅데이터 도입률을 80%로 높이는 것을 목표로 하고 있으며, 이에 따라 제조업체들은 기존 필드버스 네트워크를 이더넷 패브릭으로 업그레이드하도록 권장받고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the industrial network switch market size is expected to increase from USD 3.91 billion in 2025 to USD 4.20 billion in 2026 and reach USD 6.00 billion by 2031, growing at a CAGR of 7.4% over 2026-2031.

This report is Segmented by Type (Managed Switches, Unmanaged Switches, and Smart/Web-Managed Switches), Port Count (2-8 Ports, 9-16 Ports, 17-24 Ports, 25-48 Ports, and More), Port Speed (Fast Ethernet 100 Mbps, and More), Poe Capability (PoE Switches, and Non-PoE Switches), Industry Vertical (Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Network Switch Market Trends and Insights

Surge in Industry 4.0 Automation

Factory operators are converting legacy fieldbus islands into unified Ethernet fabrics that support digital twins, AI-driven defect detection, and closed-loop quality control. A 2026 Cisco survey found that 61% of manufacturers are already deploying artificial intelligence on the shop floor and 97% anticipate higher connectivity density, underscoring rising demand for managed switch ports.Siemens observed productivity gains of 49% in Indonesian pilot lines after migrating to software-defined production cells. Automotive assemblers are standardizing on Ethernet-based motion control, which accelerates switch refresh cycles and lifts access-layer bandwidth from Fast Ethernet to 10 Gigabit. The industrial network switch market therefore benefits from every new edge AI workload that pushes ports toward higher speeds and deterministic traffic scheduling. Vendors that bundle NETCONF interfaces and VLAN templates help plant managers overcome configuration complexity, shortening commissioning windows by up to 30%.

Rapid Adoption of Time-Sensitive Networking for Deterministic Ethernet

IEEE 802.1AS time synchronization, 802.1Qbv time-aware shaping, and 802.1Qbu frame pre-emption together let Ethernet match fieldbus-level determinism, a prerequisite for closed-loop motion and safety cells. IEC/IEEE 60802 published in 2024 codified industrial TSN profiles that require sub-microsecond jitter. France's grid operator RTE validated multi-vendor TSN interoperability across 400 kV substations in 2025, demonstrating carrier-grade robustness. Automotive Ethernet committees have also ratified TSN scheduling to carry camera, LiDAR, and over-the-air update streams simultaneously. Consequently, the industrial network switch market sees surging orders for devices that certify to both TSN and legacy industrial protocols on a single hardware platform. Suppliers that embed IEEE 1588-based clock recovery and hot-standby paths secure a technical moat against low-end entrants.

Cybersecurity Vulnerabilities in Operational Technology Networks

Converged IT-OT topologies expose legacy PLCs and HMIs to ransomware that exploits unpatched firmware and default credentials. CISA issued 47 advisories in 2025 addressing switch vulnerabilities that allowed remote code execution. Less than 30% of installed industrial switches meet IEC 62443-4-2 security levels as of early 2026. Dragos reported that 68% of industrial organizations logged at least one cyber incident in 2025, with Ethernet devices as the initial access vector in 42% of cases. Phoenix Contact's FL Switch 2000 achieved IEC 62443-4-2 certification in December 2025, proving compliance is feasible but costly. Rising insurance premiums for non-segmented networks further restrain short-run purchasing decisions.

Other drivers and restraints analyzed in the detailed report include:

- Growing Deployment of Industrial PoE Cameras and Sensors

- Expansion of Smart Grids and Digital Substations

- Shortage of Industrial Networking Skill Sets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed switches captured 65.8% of the industrial network switch market in 2025 and are forecast to deliver a 10.3% CAGR through 2031, as VLAN segmentation, QoS queuing, and remote diagnostics become essential in Industry 4.0 production zones. Utilities deploying digital substations demand sub-10-millisecond failover, which unmanaged models cannot provide. Smart or web-managed variants appeal to small plants by offering browser GUIs without the full CLI complexity. Cybersecurity-certified managed switches now command 25-40% price premiums, yet critical-infrastructure buyers consider compliance non-negotiable.

In contrast, unmanaged switches remain viable for single-machine islands but face headwinds where safety traffic needs deterministic prioritization. Vendors are therefore investing in firmware upgradability that lets customers unlock management features later, future-proofing entry-level hardware. As the industrial network switch market matures, analysts expect the managed tier to exceed 70% share by mid-decade, reinforcing the shift toward centrally orchestrated, API-driven fabrics.

The 2-8-port class held 35.6% share in 2025, serving compact machine cells, while switches above 48 ports are projected to post a 9.3% CAGR through 2031 as automotive, electronics, and semiconductor fabs consolidate edge cabinets into aggregation-layer racks. Automotive lines deploy 48-port Gigabit access blocks feeding 10 G uplinks to handle thousands of vision frames per second. High port density trims per-port costs, yet it introduces single points of failure unless redundant PSUs and hot-swap fan trays are adopted.

Ruggedized 19-inch chassis with modular PSU bays are therefore supplanting DIN-rail boxes in control rooms. Vendors also push software-defined provisioning so engineers can repurpose idle ports without manual patching. As virtualization spreads, the industrial network switch market size for the above-48-port bracket is set to climb steadily, particularly inside brownfield plants seeking cable reduction.

Complete Report Scope:

- By Switch Type

- Managed Switches

- Unmanaged Switches

- Smart / Web-Managed Switches

- By Port Count

- 2-8 Ports

- 9-16 Ports

- 17-24 Ports

- 25-48 Ports

- Above 48 Ports

- By Port Speed

- Fast Ethernet (100 Mbps)

- Gigabit Ethernet (1G)

- 10 Gigabit Ethernet (10G)

- Above 10G (25G / 40G / 100G)

- By PoE Capability

- PoE Switches

- Non-PoE Switches

- By Industry Vertical

- Manufacturing

- Energy and Power (Electric Utilities / Smart Grid)

- Oil and Gas

- Transportation (Rail, Ports, Intelligent Transport Systems)

- Automotive

- Aerospace and Defense

- Mining and Metals

- Others Industry Verticals

- By Geography

- North America

- South America

- Europe

- Asia-Pacific

- Middle East

- Africa

Geography Analysis

Asia-Pacific commanded 37.2% of the industrial network switch market in 2025 and is forecast to expand at a 9.7% CAGR through 2031. China's Made in China 2025 plan, India's Production-Linked Incentives, and Southeast Asian smart-factory grants jointly sustain multi-year capex cycles. Siemens estimated factory-automation outlays could climb to USD 125.84 billion by 2030, citing 49% productivity gains in Indonesian pilots. Japanese and South Korean fabs require TSN switches for 5 nm lithography sync, while India's solar parks install IEC 61850 gear to balance renewable intermittency. Domestic Taiwanese and Chinese vendors undercut incumbents on price, but Tier-1 automotive and aerospace OEMs still prefer global suppliers with 24-hour support.

North America benefits from the USD 52.7 billion CHIPS and Science Act, which underwrites Intel's USD 20 billion Arizona fabs, TSMC's USD 40 billion Phoenix campus, Micron's USD 20 billion New York line, and Samsung's USD 17 billion Texas facility. Each fab specifies TSN-capable 10 G and 100 G fabrics to synchronize lithography, metrology, and automated material handling. Utilities across the United States and Canada modernize substations to meet NERC CIP, which accelerates demand for IEC 62443-compliant switches. Mexico's nearshoring wave further expands regional sales as automotive clusters replicate U.S. line architectures.

Europe's market hinges on smart-grid roll-outs, automotive electrification, and NIS2 cybersecurity rules. RTE's multi-vendor TSN deployment across 400 kV sites validated commercial viability and sets a precedent for other grid operators. German automakers now embed Ethernet backbones to manage camera and LiDAR streams, lifting local demand for low-latency switches. The EU Digital Decade targets 80% enterprise cloud and big-data adoption by 2030, nudging manufacturers to upgrade legacy fieldbus networks to Ethernet fabrics.

- Moxa Inc.

- Advantech Co., Ltd.

- Belden Inc.

- Phoenix Contact GmbH & Co. KG

- Antaira Technologies, LLC

- Westermo Network Technologies AB

- Beijer Electronics Group AB

- Hirschmann Automation and Control GmbH

- Red Lion Controls, Inc.

- RuggedCom Inc.

- PLANET Technology Corporation

- TRENDnet, Inc.

- Allied Telesis Holdings K.K.

- Lantronix, Inc.

- ORing Industrial Networking Corporation

- Korenix Technology Co., Ltd.

- EtherWAN Systems, Inc.

- Weidmuller Interface GmbH & Co. KG

- Patton Electronics Co.

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Industry 4.0 Automation

- 4.2.2 Rapid Adoption of Time-Sensitive Networking for Deterministic Ethernet

- 4.2.3 Growing Deployment of Industrial PoE Cameras and Sensors

- 4.2.4 Expansion of Smart Grids and Digital Substations

- 4.2.5 Edge Computing Requirements in Harsh Environments

- 4.2.6 Government-Led Reshoring of Critical Manufacturing

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Vulnerabilities in Operational Technology Networks

- 4.3.2 Shortage of Industrial Networking Skill Sets

- 4.3.3 Volatility in Industrial Semiconductor Supply Chains

- 4.3.4 Higher Total Cost of Ownership versus Commercial-Grade Switches

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Managed Switches

- 5.1.2 Unmanaged Switches

- 5.1.3 Smart / Web-Managed Switches

- 5.2 By Port Count

- 5.2.1 2-8 Ports

- 5.2.2 9-16 Ports

- 5.2.3 17-24 Ports

- 5.2.4 25-48 Ports

- 5.2.5 Above 48 Ports

- 5.3 By Port Speed

- 5.3.1 Fast Ethernet (100 Mbps)

- 5.3.2 Gigabit Ethernet (1G)

- 5.3.3 10 Gigabit Ethernet (10G)

- 5.3.4 Above 10G (25G / 40G / 100G)

- 5.4 By PoE Capability

- 5.4.1 PoE Switches

- 5.4.2 Non-PoE Switches

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Energy and Power (Electric Utilities / Smart Grid)

- 5.5.3 Oil and Gas

- 5.5.4 Transportation (Rail, Ports, Intelligent Transport Systems)

- 5.5.5 Automotive

- 5.5.6 Aerospace and Defense

- 5.5.7 Mining and Metals

- 5.5.8 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.2 South America

- 5.6.3 Europe

- 5.6.4 Asia-Pacific

- 5.6.5 Middle East

- 5.6.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Moxa Inc.

- 6.4.2 Advantech Co., Ltd.

- 6.4.3 Belden Inc.

- 6.4.4 Phoenix Contact GmbH & Co. KG

- 6.4.5 Antaira Technologies, LLC

- 6.4.6 Westermo Network Technologies AB

- 6.4.7 Beijer Electronics Group AB

- 6.4.8 Hirschmann Automation and Control GmbH

- 6.4.9 Red Lion Controls, Inc.

- 6.4.10 RuggedCom Inc.

- 6.4.11 PLANET Technology Corporation

- 6.4.12 TRENDnet, Inc.

- 6.4.13 Allied Telesis Holdings K.K.

- 6.4.14 Lantronix, Inc.

- 6.4.15 ORing Industrial Networking Corporation

- 6.4.16 Korenix Technology Co., Ltd.

- 6.4.17 EtherWAN Systems, Inc.

- 6.4.18 Weidmuller Interface GmbH & Co. KG

- 6.4.19 Patton Electronics Co.

- 6.4.20 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment