|

시장보고서

상품코드

2073147

기업용 노트북 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Enterprise Laptop - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

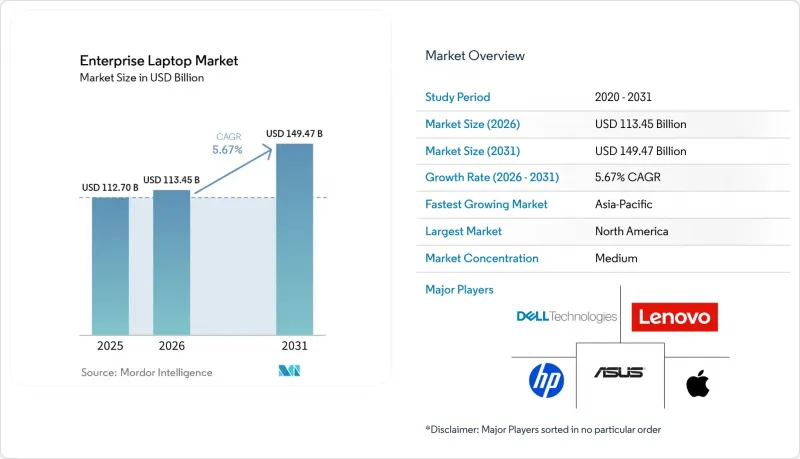

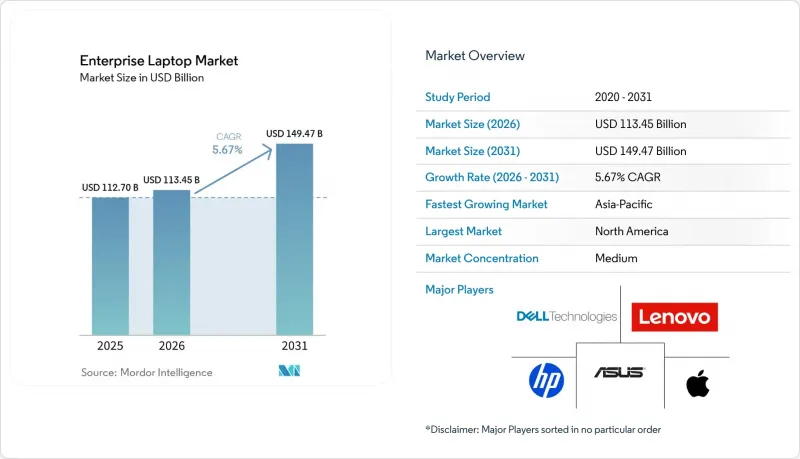

Mordor Intelligence에 의하면, 기업용 노트북 시장 규모는 2025년에 1,127억 달러, 2026년에 1,134억 5,000만 달러되어, 2031년까지 1,494억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.67%로 성장할 전망입니다.

본 보고서는 제품 유형(울트라북, 노트북, 2-in-1 컨버터블, 내충격 노트북, 모바일 워크스테이션 등), 운영 체제(Windows, macOS, Chrome OS 등), 조직 규모(대기업 등), 최종 사용자 산업(정부·공공 부문 등), 화면 크기(12인치 미만 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 기업용 노트북 시장 동향과 인사이트

하이브리드 근무 방식에 따른 업데이트 주기의 가속화

재택근무 직원들이 화상 회의를 장시간 진행할 수 있는 가벼운 하드웨어가 필요했기 때문에 기업은 교체 주기를 4년 이상에서 약 3년으로 단축했습니다. 마이크로소프트의 Windows 10 지원 종료로 인해, 조직들은 Windows 11이 탑재된 기기로의 전환을 피할 수 없게 되었습니다. 이는 연장 보안 업데이트 비용이 3년 차에는 엔드포인트 1대당 427달러에 달하고, 비용 절감의 동기가 되었기 때문입니다. 기존 Windows 10 탑재 PC의 약 40%는 Trusted Platform Module 2.0을 탑재하지 않아 현장에서의 업그레이드가 불가능했기 때문에 장비를 전면적으로 교체하도록 권장되었습니다. 각 벤더사는 Windows 11 지원 기능과 AI 지원 칩을 세트로 판매하고 있으며, 2025년 아시아태평양 기업용 주문의 절반에서 신경망 처리 장치(NPU) 기능이 지정되었습니다. OS 전환, 하이브리드 근무 환경 개선, AI 관련 메시징이 맞물리면서 조달 주기가 18개월로 단축되었습니다. 이로 인해 단기적인 수익은 증가했으나, 본래라면 여러 회계 기간에 분산되었을 수요가 앞당겨져 집중되는 결과가 되었습니다.

임베디드 하드웨어 기반 엔드포인트 보안의 보급 확대

금융 업계에서 랜섬웨어 피해로 인한 평균 배상액은 건당 608만 달러로, 업계 전반의 평균보다 25% 높았습니다. 이에 따라 이사회 차원의 리스크 위원회는 하드웨어 기반의 신뢰 기반(Root of Trust) 도입을 의무화하게 되었습니다. 유럽의 NIS2 및 미국의 CISA 지침에 따르면, 중요 인프라에서 암호 키를 펌웨어에 저장해야 할 의무가 있으며, 이를 충족하는 제품은 커먼 크라이테리아 EAL 4+ 인증을 획득한 노트북뿐입니다. 2025년에 출시된 HP의 “TPM Guard”는 칩이 제거되면 장치를 잠그고, 공급망상의 변조를 방지합니다. 그 결과, 은행, 의료, 공공 부문의 구매 담당자들은 FIPS 140-3 인증을 통과한 모델을 우선적으로 후보 목록에 선정하게 되었으며, 이로 인해 입찰 과정에서 소비자용 SKU의 약 3분의 1이 제외되었습니다. 감사 체계가 강화되고, 사이버 보험의 보험료가 하드웨어 기반 통제를 우대함에 따라, 이 보안 요인은 중기적으로 그 중요성이 더욱 커질 것입니다.

첨단 노드(6nm 이하)에서의 부품 공급 변동

메모리 팹이 수익성이 높은 AI 가속기를 우선시함에 따라 범용 DRAM 및 NAND 생산 라인에 대한 공급이 부족해졌고, 2025년 하반기에는 계약 가격이 10-15% 상승했습니다. OEM 각사는 리드타임이 8-12주로 두 배로 늘어나는 것을 목격하고, 회계 연도의 자금 계획과 맞지 않는 단계적 도입을 선택할 수밖에 없었습니다. 인도의 2026년 출하 전망은 호조인 수요에도 불구하고 공급 부족이 더 크게 작용함에 따라 1,590만 대에서 1,430만 대로 하향 조정되었습니다. 계약에 따른 가격 고정으로 위험의 일부는 헤지되었지만, 경쟁 입찰에서의 가격 인하 유연성은 제한되었습니다. 파운드리 확장 계획은 있지만, 반도체 수출 규제를 둘러싼 지정학적 마찰로 인해 단기적인 불확실성이 지속되고 있습니다.

부문별 분석

모바일 워크스테이션 시장은 2031년까지 연평균 성장률(CAGR) 7.55%를 기록하며 성장할 것으로 예상되며, 이는 기업용 노트북 시장 전체의 성장 속도를 웃도는 수준입니다. 이 플랫폼들은 초당 672 테라오퍼레이션을 처리하는 디스크리트 GPU와 128GB의 DDR5 메모리를 결합하여, 이전에는 사용자를 고정형 타워형 PC에 묶어두었던 엔지니어링 및 의료용 이미지 처리 워크로드를 처리합니다. Lenovo의 “ThinkPad P 시리즈”는 실리콘 음극 배터리를 통해 2kg 미만의 케이스로 1,000 Wh L을 실현함으로써, 성능 밀도 향상은 물론 구동 시간 연장도 달성했음을 보여줍니다. 2025년 시점에서 기존 노트북은 기업용 노트북 시장에서 35.60%의 점유율을 차지하고 있었으나, 통합 그래픽 기능으로 주류 생산성 요구 사항이 충족됨에 따라 상품화가 진행되면서 이익률이 하락하고 있습니다. 울트라북은 1kg 미만의 무게와 15시간의 배터리 사용 시간 덕분에 경영진의 지지를 얻고 있습니다. 한편, 2-in-1 컨버터블은 힌지의 내구성에 대한 논란이 계속되고 있음에도 불구하고, 스타일러스를 활용하는 현장 업무의 요구를 충족시키고 있습니다. 러기드 노트북은 MIL-STD-810H 및 IP65 규격 인증을 위해 30-50%의 추가 비용을 지불하는 것을 마다하지 않는 특정 업계로부터 지속적인 지지를 받고 있으며, 크롬북은 대당 500달러의 비용 절감을 지적한 총경제효과 조사를 통해 정당화된, 비용 최적화된 교육 및 정부 기관에서의 도입 기반을 유지하고 있습니다.

성능에 대한 요구는 더 이상 그래픽 렌더링에만 국한되지 않습니다. Microsoft Copilot+는 신경망 처리 장치(NPU)의 최소 성능 기준을 45 TOPS 정도로 규정하고 있어, 워크스테이션 조달을 AI 지원 칩으로 이끌고 있습니다. 오토데스크와 지멘스가 부여하는 독립 소프트웨어 공급업체(ISV) 인증은 여전히 조달 결정의 주요 요인으로 작용하고 있으며, EPEAT 골드 및 ENERGY STAR 9.0 인증 마크는 경쟁이 치열한 RFP(제안 요청서) 평가 점수에 점점 더 큰 영향을 미치고 있습니다. 점점 더 많은 산업 분야에서 시뮬레이션을 엣지로 이전함에 따라, 모바일 워크스테이션 관련 기업용 노트북 시장 규모는 고가의 부품 비용으로 인한 가격 민감도가 존재함에도 불구하고, 시장 전체의 성장 곡선을 상회하는 속도로 계속 확대될 전망입니다.

Windows는 Active Directory와의 통합 및 레거시 소프트웨어 스택에 힘입어 2025년에도 75.21%의 점유율을 유지했습니다. 한편, Chrome OS는 연평균 성장률(CAGR) 8.15%를 기록하며 성장하고 있습니다. 이는 랜섬웨어 피해 제로라는 실적과, 1대당 500달러의 비용 절감 효과가 최고정보책임자(CIO)들의 공감을 얻고 있기 때문입니다. 포레스터(Forrester)가 3년 동안 208%의 투자 수익률(ROI)을 산출한 데 따라, 대한항공, 웨이페어, 텔러스는 각각 1만 대 이상의 도입 대수를 달성했습니다. Chrome OS Flex는 사용이 중단된 Windows 기기를 안전한 엔드포인트로 전환하여, 자본 지출(Capex) 없이 하드웨어의 수명을 연장합니다. macOS는 M4 칩으로 인한 배터리 사용 시간 향상과 UCLA Health가 보고한 1% 미만의 고장률에 힘입어, 만족도가 높은 틈새 시장으로서의 입지를 유지하고 있습니다. 리눅스는 상용 지원보다 오픈 커널을 중시하는 소프트웨어 공학 및 사이버 보안 연구실에서 여전히 중요한 역할을 하고 있습니다.

데이터 거주지에 관한 규제로 인해, 단일 OS로의 일괄 도입이 복잡해지고 있습니다. 서유럽 CIO의 61%가 2025년에 소버린 클라우드로의 전환을 추진하고 있으며, 이로 인해 현지 관리 인스턴스가 필요해지면서 규정 준수 관련 업무 처리가 증가하고 있습니다. 정책 차이가 확대되는 가운데, 멀티 OS 기반의 엔드포인트 관리는 필수 요건이 되었으며, 기업용 노트북 시장이 다양한 플랫폼의 혁신으로 인한 혜택을 누리는 반면, 관리상의 부담은 미묘하게 증가하고 있습니다.

지역별 분석

아시아태평양이 성장의 견인차 역할을 하고 있으며, 이 지역의 기업용 노트북 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.80%로 확대될 것으로 전망됩니다. 인도에서는 하이브리드 근무 방식이 정착됨에 따라 2025년 노트북 출하 대수가 1,590만 대로 사상 최고치를 기록했으나, 메모리 부족의 영향으로 2026년 전망치는 1,430만 대로 하향 조정되었습니다. 중국의 생산 대수는 내수용 3,500만 대, 수출용 6,700만 대를 넘어, 세계적 브랜드를 뒷받침하는 수탁 제조업체의 규모를 반영하고 있습니다. 베트남과 인도네시아 등 동남아시아 국가들에서는 새로운 제조 거점에 대한 외국인 직접 투자에 힘입어 노트북 출하 대수가 두 자릿수 증가를 기록했습니다.

북미는 2025년, 1인당 IT 예산이 높고, 구매자들이 하드웨어에 내장된 보호 기능을 채택하도록 유도하는 엄격한 보안 규제의 뒷받침을 받아 34.20%의 점유율을 유지했습니다. Windows 10 지원 종료 시한으로 인해 예산 집행이 18개월이라는 촉박한 기간에 집중되게 되었으며, CFO들은 지불 일정을 이용 기간에 맞추기 위해 “PC-as-a-Service”를 채택했습니다. 유럽의 IT 지출은 2026년에 1조 5,000억 유로(1조 5,900억 달러)에 달했으며, 기기 부문은 전년 대비 10.1% 증가했습니다. 이는 소버린 클라우드와 생성형 AI의 도입이 주도한 결과입니다. 그러나 데이터 주권에 관한 법률로 인해 조달 활동이 세분화되어, 컴플라이언스 팀이 국가별 인증을 확인한 후에야 발주를 진행할 수 있었습니다.

남미에서는 2023년에 호조를 보였으나, 통화 약세로 인해 2025년부터 2026년까지 노트북 수입이 복잡해졌습니다. 브라질 정부가 지원하는 AI 탑재 노트북 입찰은 거시경제적 압박에도 불구하고 잠재적 수요가 존재함을 보여주고 있습니다. 중동 및 아프리카의 IT 지출은 2026년에 1,690억 달러에 달할 전망이며, 걸프협력회의(GCC)의 노력이 주권 클라우드 도입을 촉진함에 따라, 그 결과 현지에서 관리되는 노트북의 도입이 필요하게 되었습니다. 전반적으로 지역 간 차이는 경제의 안정성, 규제 정책, 국내 제조업에 대한 우대 조치에 따라 달라지지만, 하이브리드 근무와 AI 도입은 기업의 노트북 교체 주기를 앞당기는 보편적인 요인으로 국경을 넘어 확산되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the enterprise laptop market size is expected to be USD 112.70 billion in 2025, USD 113.45 billion in 2026, and reach USD 149.47 billion by 2031, growing at a CAGR of 5.67% from 2026 to 2031.

This report is Segmented by Product Type (Ultrabook, Notebook, 2-In-1 Convertible, Rugged Laptop, Mobile Workstation, and More), Operating System (Windows, Macos, Chrome OS, and More), Organization Size (Large Enterprises, and More), End-User Industry (Government and Public Sector, and More), Screen Size (Below 12 Inches, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Laptop Market Trends and Insights

Accelerating Hybrid-Work Refresh Cycles

Enterprises compressed replacement intervals from four-plus years to roughly three years as remote employees required lighter hardware with sustained video-conferencing endurance. Microsoft's Windows 10 sunset channeled organizations toward Windows 11 devices because extended security updates reach USD 427 per endpoint by year three, creating a cost-avoidance incentive. Roughly 40% of incumbent Windows 10 PCs lacked Trusted Platform Module 2.0, making in-place upgrades impossible and prompting wholesale fleet swaps. Vendors bundled Windows 11 compliance with AI-ready silicon, and half of Asia-Pacific corporate orders in 2025 specified neural-processing-unit capability. The confluence of operating-system transition, hybrid-work ergonomics, and AI messaging accelerated procurement into an 18-month cycle that lifted near-term revenue but front-loaded demand otherwise spread across multiple fiscal periods.

Growing Adoption of Hardware-Embedded Endpoint Security

Ransomware penalties in finance averaged USD 6.08 million per breach, 25% above the cross-industry mean, moving board-level risk committees to mandate hardware roots of trust.European NIS2 and U.S. CISA directives now require cryptographic key storage in firmware for critical infrastructure, which only Common Criteria EAL 4+ certified laptops supply. HP's TPM Guard, launched in 2025, locks the device if the chip is removed, countering supply-chain tampering. Banking, healthcare, and public-sector buyers therefore shifted shortlists toward models that pass FIPS 140-3 validation, eliminating roughly one-third of consumer-grade SKUs from tender processes. The security driver grows in the medium term as audit frameworks tighten and cyber-insurance premiums favor hardware-based controls.

Component Supply Volatility in Advanced Nodes (<= 6 nm)

Memory fabs prioritized high-margin AI accelerators, starving commodity DRAM and NAND lines and lifting contract prices 10-15% in H2 2025. Original equipment manufacturers watched lead times double to 8-12 weeks, forcing phased rollouts that misaligned with fiscal-year funding. India's 2026 shipment forecast fell from 15.9 million to 14.3 million units as the shortage overrode vibrant demand. Contract-based price locks partially hedged exposure but limited discount flexibility in competitive bids. Although foundry expansions are scheduled, geopolitical friction around semiconductor export controls sustains short-term uncertainty.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Migration to Wi-Fi 6/6E Driving Notebook Upgrades

- Corporate Sustainability Mandates Favoring Energy-Efficient Laptops

- Extended Desktop Lifecycle Policies in Cost-Sensitive SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile workstations are projected to grow at a 7.55% CAGR through 2031, outstripping the broader enterprise laptop market. These platforms pair discrete GPUs pushing 672 tera-operations per second with 128 GB DDR5 memory, addressing engineering and healthcare imaging workloads that previously tethered users to fixed towers. Lenovo's ThinkPad P Series illustrates how silicon-anode batteries now deliver 1,000 Wh L in sub-2 kg chassis, stacking run-time gains atop performance density. Traditional notebooks held 35.60% enterprise laptop market share in 2025, but commoditization erodes margins as integrated-graphics capability meets mainstream productivity needs. Ultrabooks win executive mindshare through sub-1 kg form factors and 15-hour batteries, while two-in-one convertibles capture stylus-oriented field tasks despite ongoing hinge durability debates. Rugged laptops retain loyal verticals willing to pay 30-50% premiums for MIL-STD-810H and IP65 credentials, and Chromebooks hold cost-optimized education and government footprints justified by total economic impact studies that cite USD 500 per-device savings.

Performance needs are no longer limited to graphics rendering. Microsoft Copilot+ specifies neural-processing-unit floors near 45 TOPS, steering workstation procurement toward AI-ready silicon.Independent software vendor certifications from Autodesk and Siemens remain procurement gatekeepers, and EPEAT Gold plus ENERGY STAR 9.0 labels increasingly tip RFP scores in tight races. As more industries push simulation to the edge, the enterprise laptop market size tied to mobile workstations should continue outpacing the aggregate curve, albeit with component-price sensitivity due to premium bill-of-materials inputs.

Windows preserved a 75.21% grip in 2025, anchored by Active Directory integration and legacy software stacks. Yet Chrome OS is expanding at an 8.15% CAGR as zero-ransomware track records and USD 500 per-device cost avoidance resonate with chief information officers. Korean Air, Wayfair, and Telus each scaled fleets above 10,000 units after Forrester calculated a 208% three-year ROI. Chrome OS Flex converts retired Windows boxes into secure endpoints, extending hardware life without capex. macOS remains a high-satisfaction niche, fortified by M4 battery-life gains and sub-1% failure rates reported by UCLA Health. Linux maintains relevance in software engineering and cybersecurity labs that value open kernels over commercial support.

Data-residency rules complicate homogeneous OS rollouts. Sixty-one percent of Western European CIOs pivoted toward sovereign clouds in 2025, requiring local management instances and adding compliance paperwork. As policy divergence grows, multi-OS endpoint management becomes table stakes, subtly lifting management overhead even as the enterprise laptop market benefits from diversified platform innovation.

Complete Report Scope:

- By Product Type

- Ultrabook

- Notebook

- 2-in-1 Convertible

- Rugged Laptop

- Mobile Workstation

- Chromebook

- By Operating System

- Windows

- macOS

- Chrome OS

- Linux

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- Government and Public Sector

- Education

- Healthcare and Life Sciences

- BFSI

- IT and Telecom

- Other End-User Industries

- By Screen Size

- Below 12 Inches

- 12 to 14 Inches

- 14 to 16 Inches

- Above 16 Inches

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific anchors the growth trajectory, with the enterprise laptop market size in the region advancing at a projected 7.80% CAGR through 2031. India set a shipment record of 15.9 million notebooks in 2025 after hybrid work normalized, although memory shortages trimmed the 2026 outlook to 14.3 million units. Chinese production volumes crossed 35 million units for domestic demand and 67 million for export, reflecting contract manufacturer scale that feeds global brands. Southeast Asian countries such as Vietnam and Indonesia posted double-digit notebook growth alongside foreign direct investment in new manufacturing corridors.

North America maintained 34.20% share in 2025, buoyed by high per-capita IT budgets and stringent security rules that nudge buyers toward hardware-embedded protections. The Windows 10 support deadline forced budget pulls into a tight 18-month window, and CFOs embraced PC-as-a-Service to match payments with usage periods. Europe's IT spend hit EUR 1.5 trillion (USD 1.59 trillion) in 2026, devices segment up 10.1% year-over-year, driven by sovereign cloud and generative AI rollouts. Yet data-sovereignty laws fragmented procurement, as compliance teams validated country-specific certifications before releasing purchase orders.

South America experienced a favorable trend in 2023, but currency depreciation complicated 2025-2026 laptop imports. Brazil's government-backed AI notebook tenders illustrate latent demand despite macro strain.Middle East and Africa IT spending climbed to USD 169 billion in 2026, with Gulf Cooperation Council initiatives driving sovereign-cloud deployments that in turn require locally managed laptop fleets. Overall, regional differences hinge on economic stability, regulatory posture, and domestic manufacturing incentives, but hybrid work and AI initiatives cut across borders as universal catalysts for enterprise laptop upgrades.

- Dell Inc.

- HP Inc.

- Lenovo Group Limited

- Apple Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Samsung Electronics Co., Ltd.

- Microsoft Corporation

- LG Electronics Inc.

- Panasonic Holdings Corporation

- Dynabook Inc.

- Fujitsu Limited

- Micro-Star International Co., Ltd.

- Huawei Technologies Co., Ltd.

- Razer Inc.

- Getac Technology Corporation

- Clevo Co., Ltd.

- Tongfang Co., Ltd.

- Chuwi Innovation Limited

- Xiaomi Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Hybrid-Work Refresh Cycles

- 4.2.2 Growing Adoption of Hardware-embedded Endpoint Security

- 4.2.3 Enterprise Migration to Wi-Fi 6/6E Driving Notebook Upgrades

- 4.2.4 Corporate Sustainability Mandates Favoring Energy-Efficient Laptops

- 4.2.5 Expansion of PC-as-a-Service Contracts Among Large Enterprises

- 4.2.6 On-Device AI Acceleration Requirements for Productivity Applications

- 4.3 Market Restraints

- 4.3.1 Component Supply Volatility in Advanced Nodes (?6 nm)

- 4.3.2 Extended Desktop Lifecycle Policies in Cost-Sensitive SMBs

- 4.3.3 Data-Residency Rules Hindering Global Device Fleet Standardization

- 4.3.4 Intensifying Competition From Enterprise Chromebooks and Tablets

- 4.4 Industry Supply Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Ultrabook

- 5.1.2 Notebook

- 5.1.3 2-in-1 Convertible

- 5.1.4 Rugged Laptop

- 5.1.5 Mobile Workstation

- 5.1.6 Chromebook

- 5.2 By Operating System

- 5.2.1 Windows

- 5.2.2 macOS

- 5.2.3 Chrome OS

- 5.2.4 Linux

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 Government and Public Sector

- 5.4.2 Education

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 BFSI

- 5.4.5 IT and Telecom

- 5.4.6 Other End-User Industries

- 5.5 By Screen Size

- 5.5.1 Below 12 Inches

- 5.5.2 12 to 14 Inches

- 5.5.3 14 to 16 Inches

- 5.5.4 Above 16 Inches

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dell Inc.

- 6.4.2 HP Inc.

- 6.4.3 Lenovo Group Limited

- 6.4.4 Apple Inc.

- 6.4.5 ASUSTeK Computer Inc.

- 6.4.6 Acer Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Microsoft Corporation

- 6.4.9 LG Electronics Inc.

- 6.4.10 Panasonic Holdings Corporation

- 6.4.11 Dynabook Inc.

- 6.4.12 Fujitsu Limited

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Huawei Technologies Co., Ltd.

- 6.4.15 Razer Inc.

- 6.4.16 Getac Technology Corporation

- 6.4.17 Clevo Co., Ltd.

- 6.4.18 Tongfang Co., Ltd.

- 6.4.19 Chuwi Innovation Limited

- 6.4.20 Xiaomi Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment