|

시장보고서

상품코드

2073148

교육용 노트북 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Education Laptop - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

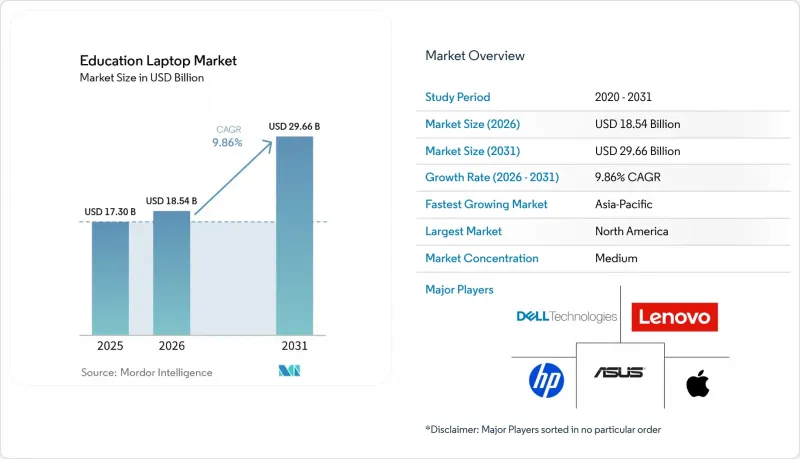

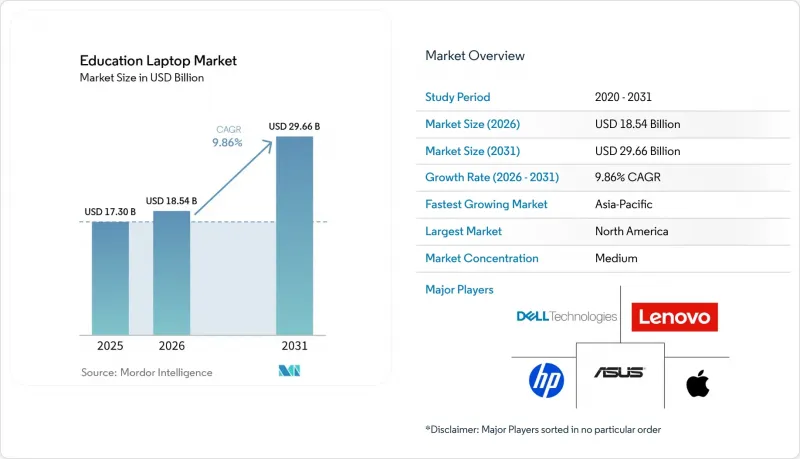

Mordor Intelligence에 의하면, 교육용 노트북 시장 규모는 2025년에 173억 달러, 2026년에 185억 4,000만 달러되어, 2031년까지 296억 6,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 9.86%로 성장할 전망입니다.

본 보고서는 제품 유형(기존 클램쉘형 노트북, 2-in-1 컨버터블형 노트북, 크롬북, 내충격형 노트북, 기타 제품 유형), 운영 체제(Windows, Chrome OS, macOS, Linux, 기타 운영 체제), 최종 사용자(K-12 학교 등), 유통 채널(온라인 소매 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 교육용 노트북 시장 동향과 인사이트

정부의 디지털 학습 이니셔티브

수년에 걸친 공공 부문의 자금 지원 덕분에 하드웨어와 연결 환경이 보편적 권리로 자리매김하게 되었으며, 예측 가능한 구매 주기가 가능해졌습니다. 일본의 “Next GIGA”업그레이드 계획에 따르면, 800만 대의 기기를 업그레이드하는 데 자금이 배정되었으며, 행정 부담을 줄이기 위해 발주량의 60%가 Chrome OS에 할당되었습니다. 독일의 “디지털 협정 2.0”에서는 2030년까지 50억 유로(56억 5,000만 달러)를 투자하고, 적응형 학습 연구에 2억 5,000만 유로(2억 8,250만 달러)를 특정 목적 자금으로 확보하고 있습니다. 인도의 “Free Laptop Yojana”는 2,000 카롤 루피(2억 4,000만 달러)의 예산 범위 내에서 타밀나두 주에 100만 대 이상의 노트북을 배포했습니다. 나이지리아의 ‘Digital Literacy Network”는 4,700만 대를 도입할 계획이며, 수입 관세를 피하기 위해 현지 조립 거점을 건설하고 있습니다. 이러한 프로그램을 통해 간헐적인 구매가 공급업체가 확신을 가지고 예측할 수 있는 지속적인 연간 배분으로 전환됩니다.

K-12 학교에서의 1대1 기기 프로그램 확대

조사에 따르면, 미국 학군의 93%가 2025년에 크롬북을 구매할 계획이며, 이에 따라 전 세계 도입 대수는 3,800만 대를 넘어설 것으로 전망됩니다. 뉴욕시는 초등학교 3학년부터 고등학교 3학년까지의 모든 학생에게 개인용 단말기를 확실히 제공하기 위해 35만 대를 배포했습니다. 도쿄도의 공동 조달에는 23개 구가 참여했으며, 물류 통합을 통해 80억 6,000만 엔(5,450만 달러)의 비용 절감을 실현했습니다. 이러한 도입으로 인해 학생 1인당 단말기 보유율이 표준화되었으며, 경쟁의 초점은 보증 기간, 예비 단말기 비축, 재활용 제도로 옮겨가고 있습니다.

개발도상국 학군의 예산 제약

재정적 한도로 인해 단말기 도입은 경상 예산이 아닌 보조금이나 기부자의 지원에 의존할 수밖에 없습니다. 레소토는 2025년에 아랍에미리트(UAE)의 자금 지원으로 노트북 400대를 지원받았으나, 이는 외부 자금에 대한 의존도를 여실히 드러내고 있습니다. 환율 변동과 관세 분쟁으로 인해 나이지리아로의 저비용 수입이 최대 9개월 지연되고 있습니다. 2026년부터 2028년까지 3,800만 대의 크롬북이 수명을 다하게 되는 가운데, 신제품보다 40-50% 저렴한 가격의 리퍼브 제품이 주목을 받고 있습니다. 이 지역을 타겟으로 하는 공급업체들은 ‘리스 투 오너(Lease-to-Own)’ 모델을 채택하여 판매량을 확보하기 위해 이익률 하락을 감수하고 있습니다.

부문별 분석

2-in-1 컨버터블형 시장은 교사가 인터랙티브 화이트보드에서 스타일러스를 이용한 주석을 자주 사용함에 따라 2031년까지 연평균 성장률(CAGR) 16.71%로 성장세가 가속화되었습니다. 2025년에도 교육용 노트북 시장의 출하 대수 중 31.66%는 여전히 기존 클램쉘형이 차지하고 있으며, 그 주된 이유는 비터치 패널의 조달 비용이 여전히 저렴하기 때문입니다. 저가형 클램쉘형 노트북 시장에서는 크롬북이 주류를 이루고 있는 반면, MIL-STD-810H 규격을 준수하는 러기드 노트북은 먼지나 낙하 등 가혹한 환경에 노출되는 직업 훈련 과정에서 활용되고 있습니다. Dell의 “Pro Education 11” 및 “Pro Education 14”는 경첩을 강화하여 3만 회의 개폐 주기를 견딜 수 있도록 설계되었으며, K-12(유치원부터 고등학교) 기기군에서 일반적으로 나타나는 연간 5-7%의 고장률을 해결하고 있습니다.

컨버터블 유형은 터치 조작, 펜 입력, 360도 힌지를 하나의 구성으로 통합하여, 필기나 그룹 작업 모두에 적합한 모델로 점점 더 널리 보급되고 있습니다. ASUS의 “BR” 및 “CR" Chromebook 시리즈는 핫스왑이 가능한 키보드와 도구 없이 교체할 수 있는 배터리 모듈을 채택하여 서비스 데스크의 처리 시간을 단축하고 있습니다." Framework의 “Laptop 12”는 수리 용이성 측면에서 만점을 받았지만, 1,199달러라는 도입 가격 때문에 그 도입은 지속가능성 시범 프로젝트로 한정되어 있습니다. 예측 기간 동안, 교육과정 개발자가 “펜 우선”의 활동이 확대됨에 따라, 교육용 노트북 시장에서 컨버터블형 모델은 클램쉘형 모델을 앞지르는 성장세를 이어갈 것으로 전망됩니다. 한편, 견고한 설계는 프리미엄 가격을 정당화하는 틈새 워크로드를 계속해서 뒷받침할 것입니다.

Chrome OS는 2025년에 교육용 노트북 시장에서 38.11%의 점유율을 차지하고, 제로 터치 등록을 통해 IT 인건비가 대폭 절감됨에 따라 연평균 성장률(CAGR) 17.00%로 성장하고 있습니다. Windows는 AutoCAD, Adobe 및 정식 버전의 Office 제품군이 필요한 교육 기관에서 여전히 사용되고 있지만, 클라우드 기반의 대체 솔루션이 동등한 기능을 제공하게 됨에 따라 그 점유율은 감소하고 있습니다. macOS는 예술 계열 학과에서 충성도 높은 사용자층을 유지하고 있는 반면, 리눅스는 코딩 부트캠프 수요를 충족시키고 있습니다. 도쿄도의 집계 데이터에 따르면, Chrome OS는 Windows에 비해 관리 비용을 40% 절감하여 80억 6,000만 엔(5,450만 달러)을 다른 우선 과제에 할당할 수 있게 되었습니다.

Chrome OS와 관련된 교육용 노트북 시장 규모는 보급형 하드웨어의 범위를 넘어 확대될 전망입니다. Lenovo의 “Chromebook Plus 14”는 50 TOPS의 성능을 지닌 MediaTek Kompanio Ultra 910 NPU를 탑재하여, 기존에는 Windows 기기가 필요했던 온디바이스 추론을 가능하게 합니다. 이에 대해 마이크로소프트는 Windows 11 Education SKU에 Copilot을 기본 제공하며, AI를 활용한 수업 계획 및 실시간 속기 기능을 강조하고 있습니다. 따라서 OS 선정은 총소유비용(TCO), 보안 체계, AI 지원 수준을 반영하는 지표가 됩니다.

지역별 분석

북미는 2025년 매출의 36.27%를 차지했으며, 접속 환경 및 단말기에 대해 71억 7,000만 달러를 지원한 ‘긴급 연결 기금(Emergency Connectivity Fund)” 및 “E-Rate”의 연장 조치 덕분에 가능했습니다. 현재 대부분의 학군에서 1인 1단말기 배치가 완료됨에 따라, 기기 교체 주기가 길어지고 있으며, 예산은 사이버 보안 소프트웨어 및 교사의 전문성 개발로 전환되고 있습니다. 따라서 해당 지역의 교육용 노트북 시장 규모는 단순히 대수가 늘어나는 것이 아니라, 리퍼브 제품이나 AI 지원 기기로의 교체 추세에 따라 좌우될 것입니다.

아시아태평양은 연평균 성장률(CAGR) 16.21%로 가장 빠르게 성장하고 있습니다. 일본의 “Next GIGA”에 의한 업데이트, 인도의 여러 주에 걸친 “무료 노트북 계획(Free Laptop Yojanas)”, 그리고 중국의 직업 훈련 의무화 조치가 더해지면서 수백만 대 규모 수요가 예상됩니다. 도쿄도의 통합 입찰을 통해 물류 공동화를 통해 80억 6,000만 엔(5,450만 달러)을 절감함으로써, 행정 개혁을 통해 고사양 모델에 대한 투자 자금을 확보할 수 있음을 보여주었습니다.

유럽에서는 독일의 50억 유로(56억 5,000만 달러) 규모의 ‘디지털 팩트 2.0”, 영국의 3억 2,500만 파운드(4억 1,200만 달러) 규모의 “커넥트 더 클래스룸”, 벨기에의 1억 7,600만 유로(1억 9,900만 달러) 규모의 “디지플랜”를 배경으로 시장이 확대되고 있습니다. GDPR(EU 개인정보보호규정) 준수로 인해 라이프사이클 비용이 10-15% 증가함에 따라, 수요는 암호화 스토리지 및 데이터 처리 계약을 제공하는 벤더로 쏠리고 있습니다.

남미와 아프리카는 1인당 지출액 면에서는 뒤처져 있지만, 자금이 확보되면 대규모 수주가 이루어질 것입니다. 나이지리아의 4,700만 대 도입 계획과 UAE의 4만 6,888대 보급은 석유 수입과 개발 자금이 디지털 형평성을 얼마나 신속하게 추진할 수 있는지를 여실히 보여주고 있습니다. 2026년 하반기에 개장할 예정인 사우디아라비아의 20억 달러 규모 레노버-알라트 공장은 연간 50만 대의 현지 생산을 목표로 하고 있으며, 수입 관세 인하를 추진하고 있습니다. 따라서 이 지역의 성장은 가계의 구매력보다 정책적 의지에 달려 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the education laptop market size is expected to be USD 17.30 billion in 2025, USD 18.54 billion in 2026, and reach USD 29.66 billion by 2031, growing at a CAGR of 9.86% from 2026 to 2031.

This report is Segmented by Product Type (Traditional Clamshell Laptops, 2-In-1 Convertible Laptops, Chromebooks, Rugged Laptops, and Other Product Types), Operating System (Windows, Chrome OS, Macos, Linux, and Other Operating Systems), End User (K-12 Schools, and More), Distribution Channel (Online Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Education Laptop Market Trends and Insights

Government Digital Learning Initiatives

Multi-year public-sector funding frames hardware and connectivity as universal rights, enabling predictable purchase cycles. Japan's Next GIGA refresh funds 8 million replacements and channels 60% of orders toward Chrome OS to cut administrative labor. Germany's Digital Pact 2.0 commits EUR 5 billion (USD 5.65 billion) through 2030 and rings-fences EUR 250 million (USD 282.5 million) for adaptive-learning research. India's Free Laptop Yojana distributed more than 1 million laptops in Tamil Nadu under a INR 2,000 crore (USD 240 million) line item. Nigeria's Digital Literacy Network schedules 47 million units and builds local assembly hubs to bypass import tariffs. Such programs convert episodic buying into rolling annual allocations that vendors can forecast with confidence.

Expanding 1:1 Device Programs in K-12 Schools

Surveys show 93% of United States districts planned Chromebook purchases in 2025, pushing the global installed base beyond 38 million. New York City issued 350,000 units to guarantee every grade 3-12 student a personal device. Tokyo's joint tender pooled 23 wards, saving ¥8.06 billion (USD 54.5 million) through consolidated logistics. These deployments normalize device-per-student ratios and shift competition toward warranty length, spare-device pools, and recycling schemes.

Budget Constraints in Developing-World School Districts

Fiscal ceilings anchor device rollouts to grants or donor aid rather than recurring budgets. Lesotho accepted 400 UAE-funded laptops in 2025, underscoring dependence on external finance. Currency swings and tariff disputes delay Nigeria's low-cost imports by up to nine months. Refurbished fleets, priced 40-50% below new, gain traction as 38 million Chromebooks approach end-of-life between 2026 and 2028. Vendors courting these regions adopt lease-to-own models and accept thinner margins to secure volume.

Other drivers and restraints analyzed in the detailed report include:

- Rising Availability of Low-Cost Chromebooks

- Surge in Hybrid and Distance-Learning Models

- Component Supply-Chain Volatility and Price Spikes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

2-in-1 convertibles accelerated at a 16.71% CAGR through 2031 as teachers lean on stylus annotation for interactive whiteboarding. In 2025, traditional clamshells still accounted for 31.66% of shipments within the education laptop market, mainly because non-touch panels remain cheaper to procure. Chromebooks dominate the low-cost clamshell tier, while rugged laptops with MIL-STD-810H ratings serve vocational courses that expose devices to dust and drops. Dell's Pro Education 11 and 14 reinforced hinges to survive 30,000 open-close cycles, tackling the 5-7% yearly breakage common in K-12 fleets.

Convertibles increasingly blend touch, pen, and 360-degree hinges into a single configuration that suits both note-taking and group work. ASUS's BR and CR Chromebook lines launch hot-swap keyboards and tool-less battery modules, cutting service desk wait times. Framework's Laptop 12 scored a perfect repairability rating but its USD 1,199 entry price limits adoption to sustainability pilots. Over the forecast horizon, the education laptop market size for convertibles is projected to keep outpacing clamshells as curriculum developers embed pen-first activities, while ruggedized builds defend niche workloads that justify premium pricing.

Chrome OS held 38.11% share of the education laptop market in 2025, expanding at a 17.00% CAGR because zero-touch enrollment slashes IT labor. Windows persists in institutes that need AutoCAD, Adobe, and full Office suites, yet its share erodes as cloud alternatives gain parity. macOS maintains a loyal base in creative arts faculties, while Linux caters to coding bootcamps. Tokyo's aggregated order showed a 40% administration cost reduction for Chrome OS versus Windows, freeing JPY 8.06 billion (USD 54.5 million) for other priorities.

The education laptop market size tied to Chrome OS is poised to move beyond entry-level hardware. Lenovo's Chromebook Plus 14 integrates a MediaTek Kompanio Ultra 910 NPU rated at 50 TOPS, enabling on-device inference that historically demanded Windows devices.Microsoft counters by bundling Copilot with Windows 11 Education SKUs, pitching AI lesson planning and real-time transcription. Operating-system preference is therefore shorthand for total cost of ownership, security posture, and AI readiness.

Complete Report Scope:

- By Product Type

- Traditional Clamshell Laptops

- 2-in-1 Convertible Laptops

- Chromebooks

- Rugged Laptops

- Other Product Types

- By Operating System

- Windows

- Chrome OS

- macOS

- Linux

- Other Operating Systems

- By End User

- K-12 Schools

- Higher Education Institutions

- Vocational and Technical Institutes

- Corporate Training Centers

- Government Educational Programs

- Other End Users

- By Distribution Channel

- Online Retail

- Offline Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America contributed 36.27% of 2025 revenue, buoyed by the Emergency Connectivity Fund and E-Rate extensions that reimbursed USD 7.17 billion in connectivity and devices. Replacement cycles are now lengthening because most districts achieved 1:1 parity, pivoting budgets toward cybersecurity software and teacher professional development. The education laptop market size in the region therefore tracks refurbishment and AI-ready refreshes rather than raw unit expansion.

Asia-Pacific is the fastest growing at a 16.21% CAGR. Japan's Next GIGA refresh, India's multi-state Free Laptop Yojanas, and China's vocational-training mandates combine into multi-million-unit pipelines. Tokyo's consolidated tender saved ¥8.06 billion (USD 54.5 million) through joint logistics, demonstrating that administrative reforms can free capital for higher-spec models.

Europe advances on the back of Germany's EUR 5 billion (USD 5.65 billion) Digital Pact 2.0, the United Kingdom's GBP 325 million (USD 412 million) Connect the Classroom, and Belgium's EUR 176 million (USD 199 million) Digiplan. GDPR compliance adds 10-15% to lifecycle cost, channeling demand toward vendors offering encrypted storage and data-processing agreements.

South America and Africa lag on per-capita spend yet stage blockbuster orders when funding aligns. Nigeria's 47-million-device roadmap and the UAE's 46,888-unit rollout highlight how oil revenues and development loans can fast-track digital equity. Saudi Arabia's USD 2 billion Lenovo-Alat plant, opening late 2026, aims to localize 500,000 units a year and trim import duties. Regional growth therefore hinges on policy resolve more than household purchasing power.

- HP Inc.

- Lenovo Group Limited

- Dell Technologies Inc.

- Apple Inc.

- Acer Inc.

- ASUSTeK Computer Inc.

- Samsung Electronics Co., Ltd.

- Microsoft Corporation

- Huawei Technologies Co., Ltd.

- Dynabook Inc.

- LG Electronics Inc.

- Fujitsu Limited

- Micro-Star International Co., Ltd.

- Beijing Chuwi Innovation Technology Co., Ltd.

- Haier Smart Home Co., Ltd.

- Panasonic Holdings Corporation

- Getac Technology Corporation

- Razer Inc.

- CTL Corporation

- Nexstgo Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Digital Learning Initiatives

- 4.2.2 Expanding 1:1 Device Programs in K-12 Schools

- 4.2.3 Rising Availability of Low-Cost Chromebooks

- 4.2.4 Surge in Hybrid and Distance-Learning Models

- 4.2.5 Growing Demand for AI-Ready Edge Computing Laptops

- 4.2.6 Procurement Preferences for Repairable Modular Designs

- 4.3 Market Restraints

- 4.3.1 Budget Constraints in Developing-World School Districts

- 4.3.2 Component Supply-Chain Volatility and Price Spikes

- 4.3.3 Device Saturation in Mature Education Markets

- 4.3.4 Data-Privacy Compliance Costs for Student Devices

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Traditional Clamshell Laptops

- 5.1.2 2-in-1 Convertible Laptops

- 5.1.3 Chromebooks

- 5.1.4 Rugged Laptops

- 5.1.5 Other Product Types

- 5.2 By Operating System

- 5.2.1 Windows

- 5.2.2 Chrome OS

- 5.2.3 macOS

- 5.2.4 Linux

- 5.2.5 Other Operating Systems

- 5.3 By End User

- 5.3.1 K-12 Schools

- 5.3.2 Higher Education Institutions

- 5.3.3 Vocational and Technical Institutes

- 5.3.4 Corporate Training Centers

- 5.3.5 Government Educational Programs

- 5.3.6 Other End Users

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Lenovo Group Limited

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Apple Inc.

- 6.4.5 Acer Inc.

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Microsoft Corporation

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Dynabook Inc.

- 6.4.11 LG Electronics Inc.

- 6.4.12 Fujitsu Limited

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Beijing Chuwi Innovation Technology Co., Ltd.

- 6.4.15 Haier Smart Home Co., Ltd.

- 6.4.16 Panasonic Holdings Corporation

- 6.4.17 Getac Technology Corporation

- 6.4.18 Razer Inc.

- 6.4.19 CTL Corporation

- 6.4.20 Nexstgo Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment