|

시장보고서

상품코드

2073150

의료 분야 증강현실 및 가상현실 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Augmented and Virtual Reality In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

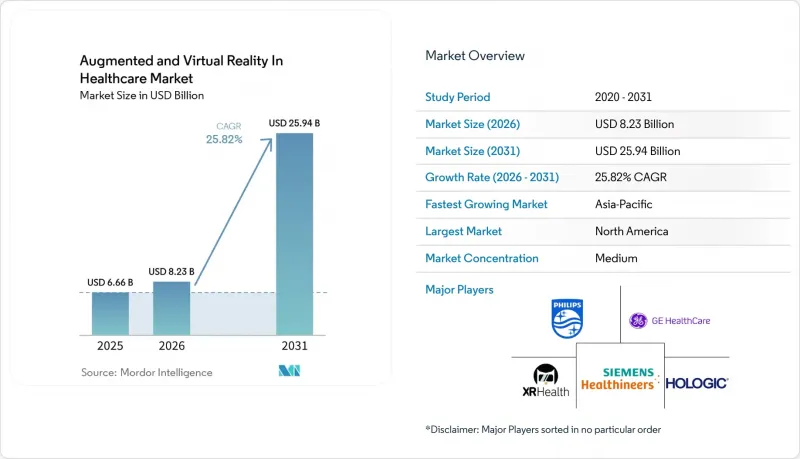

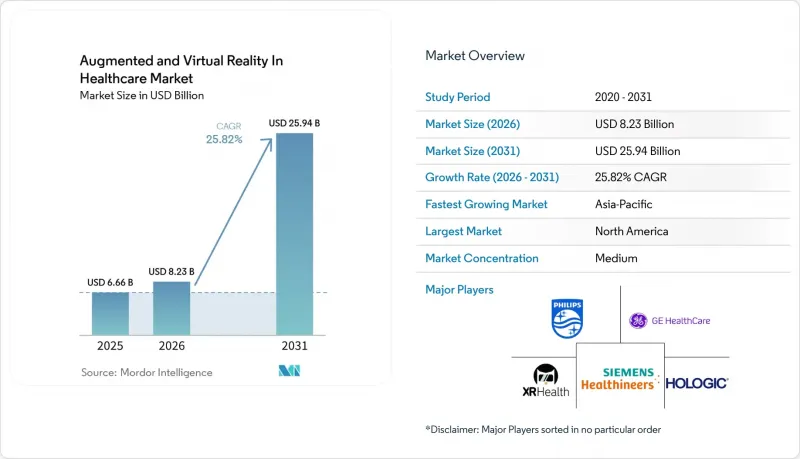

Mordor Intelligence에 의하면, 의료 분야 증강현실 및 가상현실 시장 규모는 2025년 66억 6,000만 달러에서 2026년에는 82억 3,000만 달러로 확대되어 2031년까지 259억 4,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 25.82%로 성장할 전망입니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 기술(증강현실, 가상현실), 용도(외과 수술, 의료 연수, 환자 관리, 행동 치료, 의료 영상 진단), 최종 사용자(병원, 학술 기관 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

의료 분야 증강현실 및 가상현실 세계 시장 동향 및 인사이트

위험이 없는 임상 연수에 대한 수요 증가

임상 교육은 수련 시간이 부족하여 실제 증례에 접할 기회를 확대하기 어려워지고 있어, 구조적인 부족에 직면해 있습니다. 2026년 『JMIR Medical Education』에 게재된, 7개 외과 전문 분야에 걸친 11건의 무작위 전향적 연구를 포괄한 총설에 따르면, 증강현실(AR)을 활용한 훈련은 기술적 실수를 측정한 5건의 연구 모두에서 그 발생률을 감소시켰으며, 초보 수련의의 학습 곡선을 단축시키는 것으로 밝혀졌습니다. 이 총설에서는 경험이 풍부한 외과의사의 경우 그 효과가 비교적 미미한 것으로 밝혀졌는데, 이는 가장 큰 상업적 수요가 전문가를 위한 기술 재교육 프로그램이 아니라 초기 단계의 훈련에 집중되어 있음을 의미합니다. 2026년 5월 『JMIR Perioperative Medicine』에 게재된 연구에서도, 단 한 번의 가상현실(VR) 세션을 통해 정형외과 외상 관련 과제의 완료 시간과 자기 평가에 따른 숙련도가 향상되었으며, 참가자들은 이 방식이 자원이 제한된 환경에서 유용하다고 평가한 것으로 밝혀졌습니다. 의료 분야 증강현실 및 가상현실 시장에서 이러한 수요 추세는 레지던트 프로그램, 다수의 수련의를 보유한 병원 시스템, 그리고 실제 환자에게 위험을 초래하지 않으면서 반복적인 연습이 필요한 교육 네트워크에 유리하게 작용합니다.

원격 돌봄, 원격 의료 및 원격 멘토링의 확대

증강현실을 활용한 오버레이 기술 덕분에 시술 중 지도자가 수련생을 지도하는 방식이 개선됨에 따라, 원격 임상 지원의 실용성이 높아지고 있습니다. 2026년 3월 『JMIR Human Factors』에 발표된 사용성 연구에 따르면, 동적 증강현실(AR)을 활용한 단서는 제스처나 포인터를 이용한 지도에 비해 인지적 부하를 증가시키지 않으면서도, 수련생이 원격 지시에 따를 때 발생하는 실수를 줄이는 데 도움이 되는 것으로 나타났습니다. 또한, 미국외과학회(American College of Surgeons)도 2026년 4월, 고해상도 영상, 저지연 지도 도구, 그리고 안전한 시청각 플랫폼을 기반으로 한 안전하고 확장성이 뛰어난 원격 지도 체계를 설명하는 프로토콜을 발표했습니다. 2025년 『Journal of Robotic Surgery』에 실린 총설에서는 새롭게 등장한 5G와 XR의 결합이 저지연 외과 훈련 시스템에 있어 중요하다고 지적하고 있습니다. 이는 원격지를 아우르며 실시간 지도가 필요한 환경에서 가장 중요한 요소가 됩니다. 의료 분야 증강현실 및 가상현실 시장에서 한국, 일본, 중국 등 5G 구축이 진행 중인 국가들은 네트워크 인프라가 미비한 시장에 비해 원격 AR 지원을 통한 치료 및 훈련을 보다 신속하게 도입할 수 있는 입장에 있습니다.

초기 통합 및 컨텐츠 제작에 드는 막대한 비용

비용은 특히 지역 병원이나 소규모 의료 시스템의 경우, 여전히 가장 뚜렷한 단기적 장벽으로 남아 있습니다. 2025년 ITIF의 검토 보고서에 따르면, 많은 미국 병원들이 여전히 이익률 압박에 직면해 있으며, 몰입형 훈련을 통해 장기적인 비용을 절감할 수 있는 경우에도 재량적인 기술 투자가 제한되고 있는 것으로 지적되었습니다. 초기 비용에는 헤드셋, 소프트웨어 라이선스, 도입 지원, 워크플로우 설정, 특정 전문 분야를 위한 맞춤형 컨텐츠 제작 등이 포함됩니다. 2025년 『Scientific Reports』에 발표된 연구에 따르면, 하이브리드형 가상현실 모델은 유용한 훈련의 충실도를 유지하면서 고가의 물리적 시뮬레이터에 대한 의존도를 낮춤으로써 비용 대비 효과를 높일 수 있는 것으로 밝혀졌습니다. 의료 분야 증강현실 및 가상현실 시장에서 서비스가 하드웨어보다 빠르게 성장하고 있는 이유 중 하나는 구독 방식 덕분에 컨텐츠 및 지원 비용이 더 광범위한 사용자층에 분산되기 때문입니다.

부문별 분석

2025년, 의료 분야 증강현실 및 가상현실 시장에서 하드웨어가 64.31%의 점유율을 차지했습니다. 이는 병원이 소프트웨어 및 서비스 예산을 확대하기 전에, 우선 헤드마운트 디스플레이, AR 헤드셋, 햅틱 주변 기기에 대한 투자를 진행했기 때문입니다. 이러한 경향은 임상 현장이 컨텐츠, 분석, 워크플로 도구를 확장하기 전에 물리적 장치 기반을 구축해야 하는 초기 도입 단계를 반영하고 있습니다. 또한, 이는 현재의 하드웨어 도입이 향후 수년에 걸쳐 지속적인 수익의 기반을 마련하고 있음을 의미합니다. 의료 분야 증강현실 및 가상현실 시장에서 이러한 도입 기반은 일회성 구매에서 장기적인 계약 관계로의 광범위한 전환을 이끌고 있습니다.

의료 시스템이 컨텐츠 자체 개발보다 구독형 컨텐츠 라이브러리나 관리형 교육 계약을 점점 더 선호하는 추세에 따라, 서비스 분야는 2031년까지 연평균 성장률(CAGR) 26.33%를 기록하며 성장할 것으로 전망됩니다. 이러한 변화는 의료 분야 증강현실 및 가상현실 산업이 단순한 기기 판매보다는 의료 소프트웨어 플랫폼에 가까운 모델로 전환되고 있음을 보여줍니다. 병원이 이미 몰입형 기술 도입을 결정한 후에는 온보딩, 컨텐츠 업데이트, 이용 현황 분석을 관리하는 공급업체가 더 큰 가치를 창출할 가능성이 높을 것입니다. 시장 점유율 측면에서 소프트웨어는 여전히 중간층을 차지하고 있으며, 컨텐츠 라이브러리가 더 많은 전문 분야를 아우르고 적응형 학습 도구가 상용화로 전환됨에 따라 그 역할은 확대되고 있습니다.

2025년에는 증강현실(AR)이 57.68%의 점유율을 차지했습니다. 이는 외과 의사가 수술 중 안내나 내비게이션을 수행할 때 환자를 계속해서 직접 확인해야 하기 때문입니다. 따라서 AR은 오버레이가 시야를 가리지 않으면서 시술을 지원하는 척추, 정형외과 및 영상 유도 워크플로우에 적합합니다. 또한, AR의 선도적 위상은 이미 높은 가치와 엄격한 문서화 기준이 요구되는 시술과의 임상적 일관성이 높다는 점도 반영하고 있습니다. 따라서 의료 분야 증강현실 및 가상현실 시장에서 AR은 정확도, 워크플로우와의 적합성, 그리고 수술실에서의 수용성이 중시되는 이용 사례에서 가장 큰 혜택을 보고 있습니다.

한편, 가상현실(VR)은 훈련, 재활, 행동 치료, 통증 관리 등 각 분야에서 인프라 요건이 비교적 적은 상태에서 도입할 수 있기 때문에 2031년까지 연평균 성장률(CAGR) 28.36%를 나타낼 것으로 예측됩니다. 2025년 『npj Digital Medicine』에 게재된 연구에 따르면, 원격의료에서 VR을 활용함으로써 만성 통증 환자의 통증 강도, 불안, 수면장애가 완화된 것으로 밝혀졌으며, 이는 병원 밖에서의 보다 광범위한 활용을 뒷받침하는 결과입니다. 또한, 독립형 VR 시스템은 AR을 활용한 임상 시스템과 같이 공간 매핑이 필요하지 않기 때문에 교실, 시뮬레이션 실습실, 가정 환경에서도 쉽게 활용할 수 있습니다. 의료 업계의 증강현실 및 가상현실 분야에서는 이를 통해 두 가지 명확한 상업적 방향이 제시되고 있습니다. 하나는 고도의 시술 지원과 관련이 있고, 다른 하나는 확장성이 뛰어난 교육 및 치료 제공과 관련이 있습니다.

지역별 분석

2025년, 북미는 의료 분야 증강현실 및 가상현실 시장에서 42.64%를 차지했습니다. 이는 FDA의 성숙한 승인 절차와 병원 및 학술 기관 내 초기 도입자들의 탄탄한 기반에 힘입은 결과입니다. 이 지역 시장 점유율의 대부분은 미국이 차지하고 있는데, 그 배경에는 벤처 캐피털 투자를 받은 전문 기업, 대규모 의료 시스템, 그리고 디지털 치료제에 대해 점차 개방적인 태도를 보이고 있는 보험 급여 환경이 복합적으로 작용하고 있기 때문입니다. MindMaze Therapeutics는 2025년에 재택형 디지털 신경 재활에 대해 CMS 카테고리 III 보상 코드를 획득했다고 보고했으며, 이는 미국에서 재택 VR 치료의 보험 적용을 향한 중요한 한 걸음이 되었습니다. 캐나다 역시 연구 주도형 AR 수술 지침 개발을 통해 기여하고 있으며, 지역 혁신 기반에 깊이를 더하고 있습니다.

유럽은 여전히 두 번째로 큰 규모를 자랑하는 지역이며, 독일, 영국, 프랑스가 기관 차원의 도입을 주도하고 있습니다. 독일에서는 2025년, 할레-비텐베르크의 마르틴 루터 대학교에서 AR 시나리오가 정규 의학 교육 과정에 도입되었습니다. 이는 몰입형 훈련이 단발성 시범 사업에 그치지 않고, 체계적인 교육 과정에 점차 통합되고 있음을 보여줍니다. 또한, T-Systems와 본 대학병원은 AI 기반 환자 아바타를 탑재한 VR 간호사 교육 플랫폼을 개발하여, 직원 교육에 있어 지리적 장벽을 낮췄습니다. 프랑스에서는 AR 가이드를 활용한 정형외과 수술과 혼합현실(MR)을 이용한 어깨 수술을 통해 실용화가 가속화되고 있으며, 이는 도입이 연구센터뿐만 아니라 실제 병원에서의 활용을 통해 점차 확대되고 있음을 보여줍니다.

아시아태평양은 의료 분야 증강현실 및 가상현실 시장 규모 측면에서 가장 빠르게 성장하고 있는 지역이며, 2031년까지의 연평균 성장률(CAGR)은 27.92%로 전망됩니다. 이 지역의 성장은 중국과 인도의 의료 현대화, 한국의 5G에 대한 높은 대응 능력, 그리고 확장 가능한 시뮬레이션을 더욱 매력적으로 만드는 대규모 의대생층에 의해 주도되고 있습니다. 2025년에 실시된 전 세계적인 혼합 방식 조사에서는 선전시 룽강구 병원에서 진행된 실무 중심의 디지털 전환 워크숍이 소개되었으며, 인프라 환경이 서로 다른 의료 현장에서도 몰입형 도구를 통합할 수 있음이 입증되었습니다. 남미, 중동 및 아프리카 시장 규모는 현재로서는 작지만, 아르헨티나의 공립 병원에서는 이미 증강현실(AR)을 활용한 수술이 이루어지고 있으며, 걸프 지역 국가들의 의료 시스템에서도 스마트 병원 프로그램에 몰입형 도구가 지속적으로 도입되고 있는 만큼, 구조적으로는 여전히 중요한 위치를 차지하고 있습니다. 의료 분야 증강현실 및 가상현실 시장에서 이들 지역은 현재 시장 규모라는 관점보다는 검증된 모델을 새로운 디지털 헬스 프로그램에 신속하게 도입할 수 있다는 점에서 중요하게 여겨지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the augmented and virtual reality in healthcare market size is expected to increase from USD 6.66 billion in 2025 to USD 8.23 billion in 2026 and reach USD 25.94 billion by 2031, growing at a CAGR of 25.82% over 2026-2031.

This report is Segmented by Component (Hardware, Software, Services), Technology (Augmented Reality, Virtual Reality), Application (Surgery, Medical Training, Patient Care, Behavioral Therapy, Medical Imaging), End User (Hospitals, Academic Institutes, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Value (USD).

Global Augmented and Virtual Reality In Healthcare Market Trends and Insights

Rising Need for Risk-Free Clinical Training

Clinical education is facing a structural shortfall because training time is tighter, and real case exposure is harder to scale. A 2026 JMIR Medical Education review covering 11 randomized and prospective studies across 7 surgical specialties found that augmented reality training reduced technical errors in all 5 studies that measured them and shortened learning curves for novice trainees. The same review found weaker gains for experienced surgeons, which means the strongest commercial demand is concentrated in early-stage training rather than expert refresh programs. A May 2026 JMIR Perioperative Medicine study also found that a single virtual reality session improved orthopedic trauma task completion time and self-rated competence, and participants viewed the format as useful in low-resource settings. In the augmented and virtual reality in healthcare market, this demand pattern favors residency programs, hospital systems with large trainee cohorts, and education networks that need more repetitions without adding live patient risk.

Expansion of Remote Care, Telemedicine, and Telementoring

Remote clinical support is becoming more practical because augmented overlays now improve how mentors guide trainees during procedures. A March 2026 usability study in JMIR Human Factors showed that dynamic augmented reality cues helped trainees follow remote instructions with fewer errors than gesture-based or pointer-based guidance, without raising cognitive load. The American College of Surgeons also published protocols in April 2026 that described safe and scalable telementoring frameworks built around high-definition video, low-latency guidance tools, and secure audiovisual platforms. A 2025 Journal of Robotic Surgery review noted that emerging 5G and XR combinations are important for low-latency surgical training systems, which matters most in settings that need real-time guidance across distance. In the augmented and virtual reality in healthcare market, countries with advanced 5G rollouts, such as South Korea, Japan, and China, are positioned to adopt remote AR-assisted care and training faster than markets with weaker network readiness.

High Upfront Integration and Content Creation Costs

Cost remains the clearest short-term barrier, especially for community hospitals and smaller systems. A 2025 ITIF review noted that many U.S. hospitals were still operating under margin pressure, which limited discretionary technology spending even when immersive training could lower long-run costs. The upfront burden includes headsets, software licenses, onboarding, workflow setup, and custom content creation for specific specialties. A 2025 Scientific Reports study found that hybrid virtual reality models can improve cost effectiveness by reducing reliance on expensive physical simulators while preserving useful training fidelity. In the augmented and virtual reality in healthcare market, this is one reason services are growing faster than hardware, because subscriptions spread content and support costs across a wider user base.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use in Surgical Visualization and Procedure Guidance

- AI-Enabled Scenario Analytics and Adaptive Learning

- Regulatory Uncertainty Across Clinical Use Cases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 64.31% of the augmented and virtual reality in healthcare market share in 2025 because hospitals first spent on head-mounted displays, AR headsets, and haptic peripherals before they expanded software and service budgets. This pattern reflects an early deployment phase where clinical sites need the physical device layer in place before they can scale content, analytics, and workflow tools. It also means that current hardware installations create a base for recurring revenue over the next several years. In the augmented and virtual reality in healthcare market, this installed base is shaping a broader transition from one-time purchases toward longer contractual relationships.

Services are projected to grow at 26.33% CAGR through 2031 because health systems increasingly prefer subscription-based content libraries and managed training contracts over building content alone. This shift shows that the augmented and virtual reality in healthcare industry is moving toward a model closer to healthcare software platforms than pure device sales. Vendors that manage onboarding, content refresh, and usage analytics are likely to capture more value once a hospital has already committed to immersive deployment. Software remains the middle layer by share, and its role is expanding as content libraries cover more specialties and as adaptive learning tools move into commercial use.

Augmented reality held 57.68% share in 2025 because surgeons need to keep direct visibility of the patient during intraoperative guidance and navigation. That made AR the better fit for spine, orthopedic, and image-guided workflows where overlays support action without blocking the field of view. Its lead also reflects stronger clinical alignment with procedures that already carry high value and high documentation standards. In the augmented and virtual reality in healthcare market, AR therefore benefits most from procedural use cases that reward precision, workflow fit, and operating room acceptance.

Virtual reality is projected to grow at 28.36% CAGR through 2031 because it can be deployed with fewer infrastructure demands across training, rehabilitation, behavioral therapy, and pain management. A 2025 study in npj Digital Medicine found that telehealth virtual reality reduced pain intensity, anxiety, and sleep disturbance in patients with chronic pain conditions, which supports wider use beyond hospital walls. Standalone VR systems are also easier to use in classrooms, simulation labs, and home settings because they do not depend on the same spatial mapping needs as AR-guided clinical systems. Within the augmented and virtual reality in healthcare industry, this creates two distinct commercial paths, one tied to high-acuity procedure support and the other tied to scalable education and therapy delivery.

Complete Report Scope:

- By Component

- Hardware

- Software

- Services

- By Technology

- Augmented Reality

- Virtual Reality

- By Application

- Surgery

- Medical Training and Education

- Patient Care Management

- Fitness Management

- Behavioral Therapy

- Medical Imaging

- By End User

- Hospitals

- Academic and Research Institutes

- Surgical Centers

- Clinics and Diagnostic Centers

- Pharma and Life Sciences Companies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 42.64% of the augmented and virtual reality in healthcare market share in 2025, supported by a mature FDA pathway and a strong base of hospital and academic early adopters. The United States accounts for most of this regional weight because it combines venture-backed specialist firms, large health systems, and a reimbursement environment that is slowly becoming more open to digital therapeutics. MindMaze Therapeutics reported that it achieved a CMS Category III reimbursement code in 2025 for home-based digital neurorehabilitation, which marked an important step for home VR therapy coverage in the U.S. Canada is also contributing through research-led AR surgical guidance development, which adds depth to the regional innovation base.

Europe remains the second-largest region, with Germany, the UK, and France leading institutional adoption. Germany embedded AR scenarios into formal medical education at Martin Luther University Halle-Wittenberg in 2025, which showed that immersive training is entering structured curricula rather than staying in isolated pilots. T-Systems and Universitatsklinikum Bonn also developed a VR nurse training platform with AI-driven patient avatars, which reduced geographic barriers in staff training. France has added procedural momentum through AR-guided orthopedic surgery and mixed-reality shoulder procedures, which signals that adoption is spreading through real hospital use rather than only through research centers.

Asia-Pacific is the fastest-growing part of the augmented and virtual reality in healthcare market size, with a projected 27.92% CAGR through 2031. Regional growth is being driven by healthcare modernization in China and India, strong 5G readiness in South Korea, and a large medical student base that makes scalable simulation more attractive. A 2025 global mixed-methods study highlighted practical digital transformation workshops at Shenzhen's Longgang District Hospital, which showed that immersive tools can be integrated across healthcare settings with different infrastructure conditions. South America and the Middle East and Africa are smaller today, but they remain structurally important because public hospitals in Argentina have already used AR-assisted surgery and Gulf health systems continue to include immersive tools in smart hospital programs. In the augmented and virtual reality in healthcare market, these regions matter less for present scale and more for the speed at which validated models can be transferred into newer digital health programs.

- Augmedics, Inc.

- CAE Healthcare

- EchoPixel, Inc.

- EON Reality, Inc.

- FundamentalVR Limited

- GE Healthcare

- Hologic

- ImmersiveTouch, Inc.

- Intuitive Surgical Operations, Inc.

- Koninklijke Philips

- Medivis, Inc.

- MindMaze Group

- Osso VR, Inc.

- Penumbra

- Siemens Healthineers

- Surgical Theater, Inc.

- TheraSim, Inc.

- Vuzix

- WorldViz, Inc.

- XRHealth

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need For Risk-Free Clinical Training

- 4.2.2 Expansion Of Remote Care, Telemedicine, and Telementoring

- 4.2.3 Rising Use In Surgical Visualization and Procedure Guidance

- 4.2.4 Increasing Adoption In Pain Distraction and Behavioral Therapy

- 4.2.5 AI-Enabled Scenario Analytics And Adaptive Learning

- 4.2.6 Falling Device Costs And Faster Enterprise Procurement Cycles

- 4.3 Market Restraints

- 4.3.1 High Upfront Integration and Content Creation Costs

- 4.3.2 Regulatory Uncertainty Across Clinical Use Cases

- 4.3.3 Limited Clinical Workflow Integration and Staff Readiness

- 4.3.4 Data Privacy, Security, and Patient Consent Complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Augmented Reality

- 5.2.2 Virtual Reality

- 5.3 By Application

- 5.3.1 Surgery

- 5.3.2 Medical Training and Education

- 5.3.3 Patient Care Management

- 5.3.4 Fitness Management

- 5.3.5 Behavioral Therapy

- 5.3.6 Medical Imaging

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Academic and Research Institutes

- 5.4.3 Surgical Centers

- 5.4.4 Clinics and Diagnostic Centers

- 5.4.5 Pharma and Life Sciences Companies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Augmedics, Inc.

- 6.3.2 CAE Healthcare

- 6.3.3 EchoPixel, Inc.

- 6.3.4 EON Reality, Inc.

- 6.3.5 FundamentalVR Limited

- 6.3.6 GE HealthCare

- 6.3.7 Hologic, Inc.

- 6.3.8 ImmersiveTouch, Inc.

- 6.3.9 Intuitive Surgical Operations, Inc.

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Medivis, Inc.

- 6.3.12 MindMaze Group

- 6.3.13 Osso VR, Inc.

- 6.3.14 Penumbra, Inc.

- 6.3.15 Siemens Healthineers

- 6.3.16 Surgical Theater, Inc.

- 6.3.17 TheraSim, Inc.

- 6.3.18 Vuzix Corporation

- 6.3.19 WorldViz, Inc.

- 6.3.20 XRHealth

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment