|

시장보고서

상품코드

2073169

중국발 유럽행 국경간 전자상거레 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China To Europe Cross-Border E-commerce Logistics Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

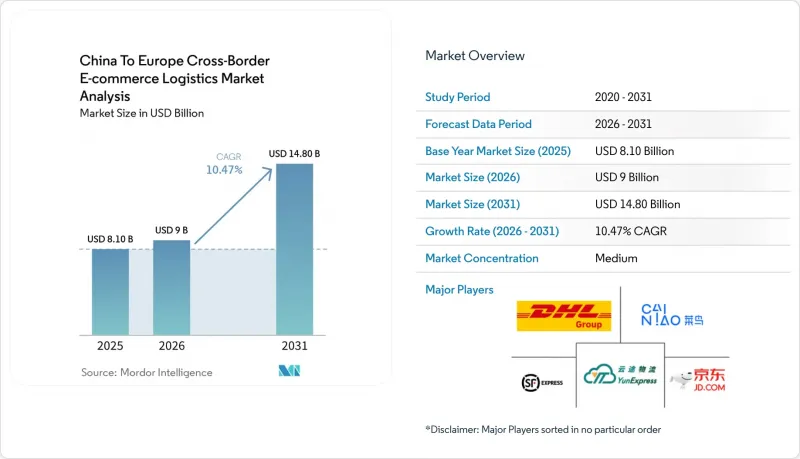

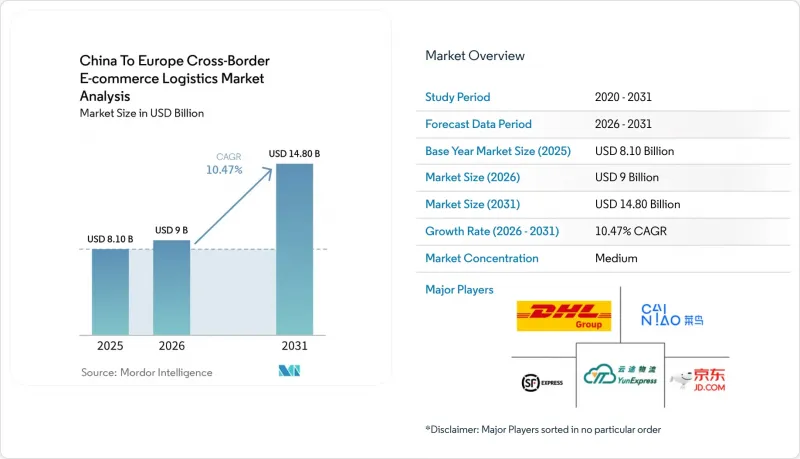

Mordor Intelligence에 의하면, 중국발 유럽행 국경간 전자상거레 물류 시장 규모는 2025년에 81억 달러로 평가되었고 2026년에는 90억 달러, 2031년까지 148억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 10.47%로 성장할 전망입니다.

본 보고서는 제품 카테고리(패션·라이프스타일, 퍼스널케어·가정용품, 기타), 물류 기능(운송, 창고·배송, 부가가치 서비스), 비즈니스 모델(B2C, B2B, C2C), 배송 속도(특급, 일반), 그리고 목적지 국가(서유럽, 동유럽, 북유럽)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국발 유럽행 국경 간 전자상거래 물류 시장 분석 : 인사이트 및 동향

중국 플랫폼 주도로 인한 유럽행 소포 처리량 급증

중국의 패스트커머스 플랫폼은 중국과 유럽 간 물류 노선에서 소포 처리량의 판도를 완전히 바꿔 놓았습니다. 2025년, EU에는 59억 개의 저가 소포가 도착했으며, 유럽연합 집행위원회에 따르면 그중 90% 가까이가 중국에서 온 것이었습니다고 합니다. 이러한 처리량 증가는 중국발 유럽행 국경 간 전자상거래 물류 시장 전반에 걸쳐 세관의 데이터 처리, 국경 통과 시스템, 그리고 라스트 마일 배송업체의 운송 능력에 추가적인 부담을 주고 있습니다. 또한, 통관 지연으로 인한 소포 처리 능력 저하를 방지하기 위해 물류 사업자들은 자동화된 신고 도구 및 도착 전 데이터 처리 체계 강화에 대한 투자를 서둘러야 하는 상황에 놓여 있습니다. 2026년에는 중국의 각 플랫폼 기업들도 EU 내 창고로 더 많은 재고를 이전하고 있으며, 이로 인해 대량으로 취급되는 SKU(재고 관리 단위)에 대한 소량 소포의 직접 발송 의존도가 낮아지고 있습니다. 이로 인해, 단순히 소포를 운송하는 업체와 동일한 운영 모델 내에서 소비자 대상 소포의 직접 배송과 창고로의 대량 보충을 모두 관리할 수 있는 업체 간의 격차가 확대되고 있습니다.

IOSS 지원 결제 절차를 통한 세무 투명성 및 원활한 통관

“수입 원스톱 숍(IOSS)”의 도입으로 인해, EU로 제품을 수출하는 많은 대량 판매업체들의 통관 관련 마찰이 완화되었습니다. 2025년 5월, 유럽연합 이사회는 수입품에 대한 세금 징수를 간소화하기 위한 조치에 대한 입장을 합의했으며, 유럽집행위원회는 이 새로운 접근 방식이 전자상거래를 통한 수입 분야에서 무역 및 규정 준수를 개선하는 것을 목표로 한다고 밝혔습니다. 중국발 유럽행 국경 간 전자상거래 물류 시장에서 이는 중요한 의미를 지닙니다. 왜냐하면, 결제 시 부가가치세(VAT)를 징수하는 판매자는 국경에서의 불확실성을 줄이면서 상품을 운송할 수 있기 때문입니다. 이와 같은 규정 준수 접근 방식은 현재 ICS2로도 확대되고 있으며, 데이터 품질 향상을 통해 등록 사업자의 검사 위험을 줄이고 처리 속도를 높일 수 있습니다. 독자적인 통관 게이트웨이를 보유한 운송업체는 세무 처리, 통관 신고, 통관 절차를 하나의 서비스로 통합할 수 있으므로 더 유리한 입장에 있습니다. EU가 보다 통합된 통관 데이터 모델로 전환해 나가는 가운데, 표준화된 데이터 파이프라인에 대한 조기 투자는 단순한 규정 준수 비용에 그치지 않고 실질적인 서비스 경쟁력으로 자리 잡고 있습니다.

EU의 저가 품목 관세 면제 및 소포 수수료 폐지

EU에서 150유로(162달러)에 대한 관세 면제 조치의 폐지는 이 운송 경로에 영향을 미치는 가장 중요한 단기적 규제 변경 사항입니다. 2025년 12월, 유럽 이사회는 2026년 7월 1일부터 소액 소포에 관세를 부과하기로 합의했으며, 이 개혁에 따라 150유로(173.59달러) 미만의 소포에 대해 관세 분류별로 일률적으로 3유로(3.2달러)의 요금이 도입되었습니다. 이 규정에 따라 판매자가 계속해서 중국에서 직접 소포 발송을 이용할 경우, 매우 저렴한 상품 구성의 매력은 떨어지게 됩니다. 또한, 플랫폼은 인기 상품을 유럽 창고 보관 프로그램으로 전환하고, 저가 소포를 반복적으로 수입하는 대신 일괄 수입을 통해 관세 리스크를 관리해야할 것입니다. 그렇다고 해서, 이로 인해 중국발 유럽행 국경 간 전자상거래 물류 시장의 물류 수요가 사라지는 것은 아닙니다. 그렇긴 하지만, 수익 기반의 일부는 해상 운송, 철도 운송, 창고 보관 및 유럽 내 배송으로 전환될 것입니다. 따라서 직접 소포 물류와 현지 보충 물류를 모두 처리할 수 있는 공급업체는 규제 모델이 변화하는 상황에서도 수익을 확보하기 쉬운 입장에 있습니다.

부문별 분석

2025년, 중국발 유럽행 국경 간 전자상거래 물류 시장 점유율 중 패션·라이프스타일 부문이 31.47%를 차지하고, 퍼스널케어·가정용품 부문은 2031년까지 연평균 성장률(CAGR) 11.45%로 성장할 것으로 전망됩니다. Shein과 Temu가 유럽 전역에서 의류, 신발, 액세서리 주문량을 크게 늘린 덕분에 패션 분야가 1위를 유지했습니다. 그렇긴 하지만, 중국 판매업체들이 재구매를 유도하고, 일반 의류보다 반품률이 낮은 스킨케어, 웰니스, 가정용품 라인을 확대하고 있는 만큼, 카테고리 구성은 변화하고 있습니다. 또한 Anker, Xiaomi, DJI 등의 브랜드가 보다 안전한 운송, 더 우수한 포장, 더욱 엄격하게 관리되는 보관 조건에 대한 수요를 창출하고 있기 때문에 가전제품 및 가정용 전자제품도 전략적으로 중요한 위치를 계속 차지하고 있습니다.

식품 및 음료 및 가구는 중국발 유럽행 국경 간 전자상거래 물류 업계에서 여전히 비교적 작은 비중을 차지하고 있지만, 두 카테고리 모두 취급하기 까다로운 요건을 수반하고 있습니다. 식품 및 음료의 경우, 유럽 내에서 더욱 엄격한 온도 관리가 요구되며, 식품 규제와 관련된 서류 제출 기준도 더욱 엄격해집니다. 가구는 무게가 무겁고 출하 빈도가 낮은 특징이 있어, 주문당 물류 비용이 고객 가치를 급격히 저하시킬 가능성이 있습니다. SF 인터내셔널에 따르면, 2025년 상반기 중국발 유럽행 국경 간 전자상거래 물류 매출액은 전년 동기 대비 2배로 증가했으며, 그 구성에서 의류와 전자기기가 중요한 비중을 차지했습니다. 이러한 매출 추이는 중국발 유럽행 전자상거래 물류 시장이 주문 건수 증가뿐만 아니라, 건당 주문 처리 수익을 높이는 카테고리에서도 가치를 창출하고 있음을 시사합니다.

2025년 중국발 유럽행 국경 간 전자상거래 물류 시장 규모 중 운송이 71.20%를 차지하고 있으며, 부가가치 서비스 및 기타 부문은 2031년까지 연평균 성장률(CAGR) 15.64%로 성장할 것으로 전망됩니다. 항공, 해상, 철도, 육로 등 각 운송 수단은 이 노선에서 발생하는 다양한 긴급 상황과 비용 요구 사항에 지속적으로 대응하고 있으며, 그 결과 운송은 여전히 최대의 수익원입니다. 한편, 성장이 가속화되고 있는 분야로는 반품 처리, 규정 준수 라벨 부착, IOSS(국제 온라인 판매 서비스) 관리, 통관 지원 및 키팅이 있습니다. 또한, 배송 기간을 단축하기 위해 유럽에 상품을 재고로 보관하는 중국 판매업체가 늘어남에 따라, 창고 보관, 배송, 재고 관리의 중요성도 점점 더 커지고 있습니다.

항공 부문은 긴급성이 높은 주문이나 고가 주문에 대해 여전히 구조적인 프리미엄을 유지하고 있으며, SF 에어라인즈는 그 역량을 강화하기 위해 2026년 4월부터 에저우 화후와 파리 샤를 드 골 간을 주 2회 운항하는 B747-400F 노선의 운항을 시작했습니다. 철도 운송은 중요한 중간적 위치를 차지하고 있습니다. 2026년 1분기, “중국·유럽 철도 특급”는 5,460편을 운항하고 54만 TEU를 운송하여, 전년 동기 대비 각각 29%, 22% 증가했습니다. 해상 운송 경로의 불안정성으로 인해 중저가 대의 보충 화물에 있어 철도 운송의 매력이 높아지고 있는 만큼, 이러한 실적은 중요합니다. 장기적으로는 이러한 전환을 통해 창고 보관 및 유럽 내 물류 수요를 실질적으로 줄이지 않으면서도, 일부 보충 화물을 해상 운송에서 철도 운송으로 전환하는 것이 가능해질 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 및 수량, 2020-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the china-to-Europe cross-border e-commerce logistics market size was valued at USD 8.10 billion in 2025 and is projected to be USD 9 billion in 2026 and USD 14.80 billion by 2031, growing at a CAGR of 10.47% from 2026 to 2031.

This report is Segmented by Product Category (Fashion and Lifestyle, Personal and Household Care, and More), by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Business Model (B2C, B2B, C2C), by Delivery Speed (Express, Standard), and by Destination Country (Western, Eastern, Northern Europe). The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of China To Europe Cross-Border E-commerce Logistics Market Analysis

Chinese Platform-Led Parcel Volume Surge into Europe

Chinese fast-commerce platforms have changed the volume base on the China-Europe corridor. The EU received 5.9 billion low-value parcels in 2025, and the European Commission said close to 90% of those parcels came from China. That volume is putting more pressure on customs data processing, border release systems, and final-mile carrier capacity across the China-to-Europe cross-border e-commerce logistics market. It is also pushing logistics providers to invest in automated declaration tools and stronger pre-arrival data handling to prevent clearance delays from disrupting parcel throughput. In 2026, Chinese platforms are also moving more inventory into EU warehouses, which reduces reliance on direct small-parcel shipping for high-volume stock-keeping units. This is widening the gap between providers that only move parcels and providers that can manage direct consumer parcels and bulk warehouse replenishment within the same operating model.

IOSS-Enabled Checkout Tax Transparency and Smoother Clearance

The Import One-Stop Shop has reduced customs friction for many high-volume sellers shipping into the EU. In May 2025, the Council of the European Union agreed on its position on measures designed to simplify tax collection for imports, and the European Commission stated that the new approach was intended to improve trade and compliance for e-commerce imports. In the China-to-Europe cross-border e-commerce logistics market, this matters because sellers who collect VAT at checkout can move goods with less border uncertainty. The same compliance logic now extends into ICS2, where better data quality can reduce inspection risk and improve processing speed for registered operators. Carriers with their own customs gateways are in a stronger position because they can package tax handling, customs filing, and border release into one service. As the EU moves toward a more centralized customs data model, early investment in standardized data pipelines is becoming a practical service advantage rather than only a compliance expense.

End of EU Low-Value Duty Relief and Parcel Fees

The removal of the EU's EUR 150 (USD 162) customs duty exemption is the most important near-term regulatory change affecting this corridor. In December 2025, the Council agreed to levy customs duty on small parcels from July 1, 2026, and this reform introduced a flat EUR 3 (USD 3.2) charge per tariff heading on sub-EUR 150 (USD 173.59) parcels. The rule makes very low-ticket baskets less attractive when sellers continue to use direct parcel shipping from China. It also pushes platforms to shift popular items into European storage programs so duty exposure is managed through bulk imports rather than repeated low-value parcel entries. That does not remove logistics demand from the China-to-Europe cross-border e-commerce logistics market. Still, it does shift part of the revenue base toward ocean, rail, warehousing, and domestic European distribution. Providers that can handle both direct parcel flows and localized replenishment flows are therefore better placed to protect revenue as the regulatory model changes.

Other drivers and restraints analyzed in the detailed report include:

- EU Warehousing Localization by China-Linked Sellers

- Parcel-Locker and Out-Of-Home Density Lowers Last-Mile Friction

- GPSR and ICS2 Data-Compliance Burden on Non-EU Sellers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fashion and lifestyle accounted for 31.47% of the China-to-Europe cross-border e-commerce logistics market share in 2025, while personal and household care is forecast to grow at a 11.45% CAGR through 2031. Fashion kept the lead because Shein and Temu built very high order volumes in apparel, footwear, and accessories across Europe. Even so, the category mix is changing as Chinese sellers add more skincare, wellness, and household care lines that encourage repeat purchases and usually face lower return rates than apparel. Consumer electronics and household appliances also remain strategically important because brands such as Anker, Xiaomi, and DJI create demand for safer transport, better packaging, and more controlled storage conditions.

Foods and beverages and furniture remain smaller parts of the China-to-Europe cross-border e-commerce logistics industry, but both categories pose difficult handling requirements. Foods and beverages require stronger temperature control and tighter food compliance documentation inside Europe. Furniture creates high-weight, low-frequency shipments, where logistics costs per order can quickly erode the customer value proposition. SF International said its cross-border e-commerce logistics revenue from China to Europe doubled year on year in H1 2025, and apparel and electronics were important parts of that mix. That revenue pattern suggests the China-to-Europe e-commerce logistics market is gaining value not only from more orders, but also from categories that support higher fulfillment revenue per shipment.

Transportation accounted for 71.20% of the China to Europe cross-border e-commerce logistics market size in 2025, while value-added services and others are projected to grow at 15.64% CAGR through 2031. Air, ocean, rail, and road continue to serve different urgency and cost needs on the corridor, so transport remains the largest revenue pool. At the same time, the faster-growing opportunity is moving toward returns handling, compliance labeling, IOSS administration, customs support, and kitting. Warehousing, distribution, and inventory management are also becoming increasingly important as more chinese sellers stock goods in Europe to shorten delivery windows.

The air segment still carries a structural premium for urgent or higher-value orders, and SF Airlines launched a twice-weekly B747-400F service between Ezhou Huahu and Paris-Charles de Gaulle in April 2026 to strengthen that capability. Rail is holding a valuable middle position because the China-Europe Railway Express handled 5,460 train trips and 546,000 TEUs in Q1 2026, up 29% and 22% year on year. That performance matters because route instability in maritime corridors has made rail more attractive for mid-value replenishment cargo. Over time, that shift can move some replenishment freight from ocean to rail without materially reducing the need for warehousing and domestic European distribution.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Destination Country

- Western Europe

- Germany

- France

- United Kingdom

- BENELUX

- Spain

- Italy

- Rest of Western Europe

- Eastern Europe

- Poland

- Czech Republic

- Hungary

- Romania

- Rest of Eastern Europe

- Northern Europe (Nordics & Baltic Countries)

- Western Europe

List of Companies Covered in this Report:

- DHL Group

- Cainiao Group

- JD Logistics

- SF Express / SF International

- YunExpress

- 4PX Express

- Yanwen Express

- J&T Express International

- ZTO Express Global

- YTO International Express and Supply Chain Technology

- ECMS Express

- Asendia

- CEVA Logistics (CMA CGM)

- DSV (including DB schenker)

- Kuehne+Nagel

- GEODIS

- FedEx Cross Border

- UPS

- C.H. Robinson

- Meest China-Europe Logistics

- CIRRO E-Commerce

- RongExpress

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Chinese Platform-Led Parcel Volume Surge into Europe

- 4.6.2 IOSS-Enabled Checkout Tax Transparency and Smoother Clearance

- 4.6.3 EU Warehousing Localization By China-Linked Sellers

- 4.6.4 Value-Seeking European Consumers Favor China-Origin Assortments

- 4.6.5 Parcel-Locker and Out-Of-Home Density Lowers Last-Mile Friction

- 4.6.6 Rail-Sea-Air Mode Shifting for Mid-Value Replenishment SKUs

- 4.7 Market Restraints

- 4.7.1 End of EU Low-Value Duty Relief and Parcel Fees

- 4.7.2 GPSR and ICS2 Data-Compliance Burden on Non-EU Sellers

- 4.7.3 Reverse-Logistics Economics Weaken Low-Ticket Bulky Baskets

- 4.7.4 Route-Risk Migration from Red Sea and Eurasian Rail Volatility

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value and Volume, 2020-2031)

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Destination Country

- 5.5.1 Western Europe

- 5.5.1.1 Germany

- 5.5.1.2 France

- 5.5.1.3 United Kingdom

- 5.5.1.4 BENELUX

- 5.5.1.5 Spain

- 5.5.1.6 Italy

- 5.5.1.7 Rest of Western Europe

- 5.5.2 Eastern Europe

- 5.5.2.1 Poland

- 5.5.2.2 Czech Republic

- 5.5.2.3 Hungary

- 5.5.2.4 Romania

- 5.5.2.5 Rest of Eastern Europe

- 5.5.3 Northern Europe (Nordics & Baltic Countries)

- 5.5.1 Western Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Cainiao Group

- 6.4.3 JD Logistics

- 6.4.4 SF Express / SF International

- 6.4.5 YunExpress

- 6.4.6 4PX Express

- 6.4.7 Yanwen Express

- 6.4.8 J&T Express International

- 6.4.9 ZTO Express Global

- 6.4.10 YTO International Express and Supply Chain Technology

- 6.4.11 ECMS Express

- 6.4.12 Asendia

- 6.4.13 CEVA Logistics (CMA CGM)

- 6.4.14 DSV (including DB schenker)

- 6.4.15 Kuehne+Nagel

- 6.4.16 GEODIS

- 6.4.17 FedEx Cross Border

- 6.4.18 UPS

- 6.4.19 C.H. Robinson

- 6.4.20 Meest China-Europe Logistics

- 6.4.21 CIRRO E-Commerce

- 6.4.22 RongExpress

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment