|

시장보고서

상품코드

2073209

독일의 완성 차량 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Finished Vehicle Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

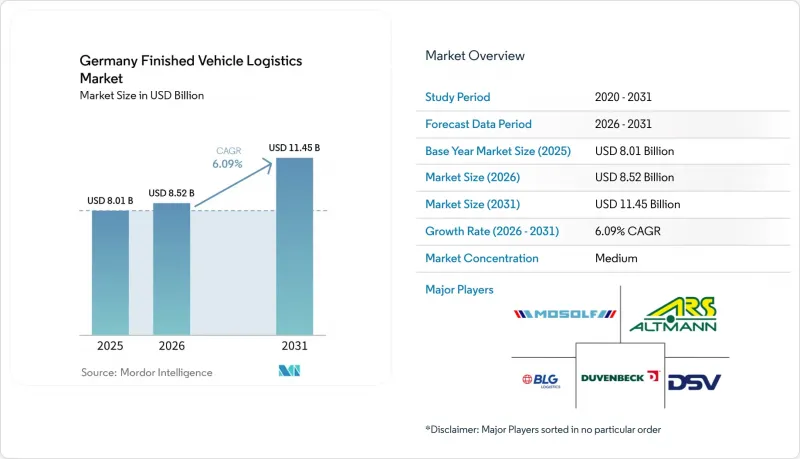

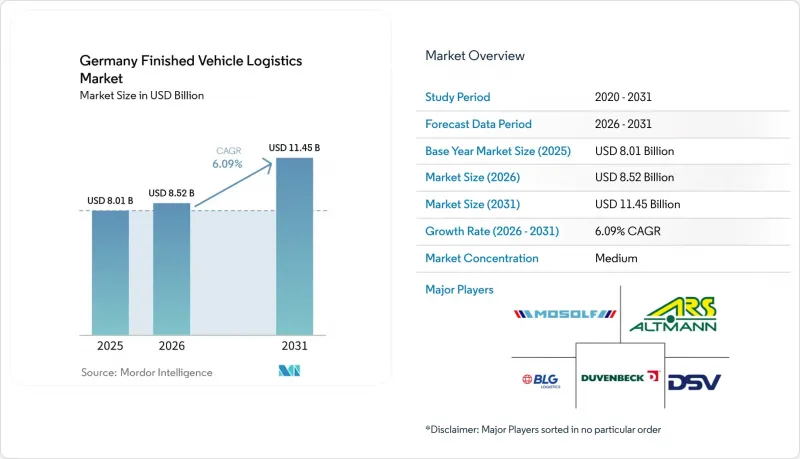

Mordor Intelligence에 의하면, 독일 완성 차량 물류 시장 규모는 2025년에 80억 1,000만 달러로 평가되었고 2026년에는 85억 2,000만 달러, 2031년까지 114억 5,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.09%로 성장할 전망입니다.

독일의 완성 차량 물류 시장은 현재, 기존 차량의 출하 대수 감소와 전기 모빌리티로의 급속한 전환에 적응해 나가면서 구조적인 변화를 겪고 있습니다. 본 보고서는 물류 기능별(운송, 창고·유통, 부가가치 서비스), 목적지별(국내, 국제), 차량 유형별(승용차, 상용차, 오프로드 차량), 최종 사용자 산업별(OEM, 딜러, 기타), 지역별(노르트라인-베스트팔렌주, 바이에른주, 바덴-뷔르템베르크주 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일 완성 차량 물류 시장 동향과 인사이트

OEM을 통한 JIS(Just-in-Sequence) 차량 납품에 대한 수요

독일의 자동차 제조업체들은 순서 오류를 허용하지 않는 수주 생산 체제를 유지하고 있기 때문에 ‘저스트-인-시퀀싱(Just-in-Sequence)’ 납품은 독일 완성 차량 물류 시장에서 물류 계약 및 서비스 설계의 핵심 요소로 자리 잡고 있습니다. BMW는 대규모 공장 개보수를 거쳐 2026년 8월부터 ‘노이에 클라세” 생산을 위해 뮌헨 공장의 준비 작업을 진행하고 있습니다. 이 변경 사항은 전기차와 내연기관 차량의 생산 프로그램이 동일한 제조 공간을 공유하기 때문에 새로운 출하 흐름 계획과 직접적으로 연결됩니다. 아우디 역시 Q3 생산 과정에서 잉골슈타트와 제르의 공동 활동을 통해, 그리고 잉골슈타트에서 신형 전기차 모델 출시 준비를 통해 생산과 물류의 통합을 강화하고 있으며, 거점 간 차체 운송에는 이미 철도 운송이 도입되어 있습니다. 공급업체 차원에서는 창고 내 주문 관리, 자동화된 이송, 실시간 현황 공유가 더 이상 선택적인 부가 기능이 아니라, 각 OEM 업체들이 이를 표준 업무 수행의 일부로 점점 더 기대하고 있습니다. 이로 인해 운송업체 선정에 있어 기술력의 깊이가 더욱 중요해지고 있습니다. 왜냐하면, 업체는 현재 물리적 처리 능력과 차량의 전체 운송 경로에 걸친 일관된 이벤트 수준 보고 능력을 모두 입증해야 하기 때문입니다. 따라서, 동기화된 납기 일정이나 투명한 마일스톤 추적을 지원하지 못하는 운송업체는 대형 OEM 업체가 입찰을 재개할 경우, 독일 완성 차량 물류 시장에서의 점유율을 잃을 가능성이 높아집니다.

철도와의 연계를 통한 항만 및 내륙 터미널의 처리 능력 확대

철도와의 연계 인프라가 트럭에 대한 의존도를 낮추고, 저배출 가스 계약을 지원하며, 항만과 내륙 복합 시설 간의 장거리 연결 품질을 향상시킴으로써, 독일의 완성 차량 물류 시장에서 가장 뚜렷한 경쟁 우위 요소 중 하나로 자리매김하고 있습니다. 듀이스포트는 21개의 항만 유역, 10개의 컨테이너 터미널, 그리고 약 200킬로미터에 달하는 자체 철도망을 통해 연간 1억 톤 이상의 화물을 처리하고 있어, 노르트라인-베스트팔렌주에 비할 데 없이 확고한 위상을 안겨주고 있습니다. ARS Altmann AG는 4,000량 이상의 전용 철도 화물차(유럽 최대 규모의 민간 소유 철도 차량 함대)를 보유하고 있으며, 공장에서 항구로의 운송 계획에서 큰 우위를 발휘함으로써 이러한 복합운송으로의 전환을 지원하고 있습니다. OBB Rail Cargo Group은 2026년에 베로나-뒤스부르크 구간의 운행 횟수를 주 10왕복으로 확대하여 서독의 복합운송 연결성을 향상시키는 동시에, 국경을 넘는 자동차 물류의 회복력을 높였습니다. 더 많은 물류 흐름이 복합운송을 중심으로 재설계됨에 따라, 철도 접근성, 터미널 관리, 그리고 강력한 복합운송 스케줄링 역량을 갖춘 사업자는 계약 확대 기회를 포착하는 데 있어 더 유리한 입장에 있습니다. 이로 인해 독일의 완성 차량 물류 시장에서 고정 인프라의 소유 가치가 높아지고 있습니다. 이는 철도와 연결된 거점까지의 접근성이 서비스의 신뢰성과 배기가스 성능 모두에 영향을 미치게 되었기 때문입니다.

도로 운송 분야의 운전기사 부족과 임금 압박

독일은 여전히 전문 운전기사 부족 문제에 직면해 있으며, 완성 차량 물류 업계는 이러한 압박을 더욱 강하게 느끼고 있습니다. 이는 자동차 운송에는 전문적인 적재, 고정 및 상태 관리 기술이 요구되기 때문입니다. 이 문제는 단순한 채용난에 그치지 않고, 수주 상황이 호조를 보이더라도 차량이 유휴 상태가 될 가능성이 있어, 자산 가동률을 저하시키고 수요가 급증할 때 서비스 회복을 지연시키는 요인이 됩니다. 이러한 압박은 국내 트럭 운송에 크게 의존하고, 운임 규제가 엄격하며, 노선 선택의 유연성이 제한된 사업자들에게 가장 심각합니다. 임금 인상과 규정 준수 비용 역시 소규모 지역 운송업체에게는 더 큰 타격이 됩니다. 왜냐하면 이러한 업체들은 광범위한 서비스 구성을 통해 비용 증가를 분산시킬 여지가 적기 때문입니다. 이러한 상황으로 인해, 육상 운송만을 전문으로 하는 사업자들은 운송량 변동을 흡수하거나, 딜러 및 차량 대여업체를 대상으로 한 배송과 관련된 보다 기술적인 업무를 수행하는 능력이 저하되고 있습니다. 따라서 운전기사 부족은 장기적으로는 멀티모달 및 복합형 방식에 의한 가치 창출로의 전환이라는 흐름을 바꾸지는 않겠지만, 단기적으로는 독일의 완성 차량 물류 시장에 있어 명백한 제약 요인으로 작용하고 있습니다.

부문별 분석

2025년, 독일의 완성 차량 물류 시장에서 운송 부문은 64.86%의 점유율을 차지했습니다. 라스트 마일 차량 배송은 여전히 국내 노선에서 트럭의 유연한 접근성에 의존하고 있기 때문에 딜러, 리스 업체 및 차량 대여 업체로의 인도에 있어서는 도로 운송이 주요 배송 수단으로 남아 있었습니다. 철도는 공장에서 항만까지 이어지는 중·장거리 주요 운송 통로 역할을 담당하고 있으며, 이로 인해 제3자에게만 의존하지 않고 운송 능력을 직접 관리할 수 있는 사업자에게 있어 자산의 소유 가치가 높아졌습니다. 이 분야에서 ARS Altmann AG는 4,000량 이상의 철도 화물차를 보유하고 있으며, 유럽 전역의 철도 인프라 분야에서 가장 확고한 입지 중 하나를 구축하고 있습니다. 해상 운송 및 내륙 수로는 독일 국내에서는 여전히 부차적인 위치를 차지하고 있지만, 주요 관문 회랑과 관련된 수출 및 잉여 물류를 지속적으로 뒷받침하고 있습니다.

창고·유통 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 7.84%를 나타낼 것으로 예측되며, 독일의 완성 차량 물류 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 그 이유는 단순히 보관 수요 때문만은 아닙니다. 전기차 인도 전 작업 공정이 장기화되고 있는 점, 소프트웨어 검증, 충전 준비, 프로모션 업무, 출하 전 상태 관리 프로세스 등이 부가가치의 변화를 가져오고 있기 때문입니다. BLG 로지스틱스는 2025년에 전체 네트워크에서 420만 대의 차량을 취급하며, 브레머하펜 자동차 터미널만 해도 125만 대를 처리하고 있어, 생산 환경이 부진한 상황에서도 종합적인 취급량이 여전히 얼마나 중요한지를 여실히 보여주고 있습니다.

2025년, 독일의 완성 차량 물류 시장에서 국내 물류가 62.51%의 점유율을 차지하며 최대 운송 목적지 범주가 되었습니다. 이러한 취급량은 국내의 밀집된 도시 지역 및 산업 지대 회랑에서 딜러에 대한 재고 보충, 리스 차량 인도, 그리고 플릿 차량 납품에 의해 뒷받침되고 있으며, 이러한 지역에서는 기본적인 노선망의 커버리지뿐만 아니라 서비스 빈도와 인도 품질도 중요하게 여겨지고 있습니다. 국내 수요는 독일의 거대한 신차 시장과, 수출 여건이 악화되더라도 지속되는 차량 교체 주기와 밀접하게 연관되어 있어 비교적 안정적입니다. 한편, 국내 운송의 경우 라스트 마일 배송 시간대, 운전기사 확보, 상태 관리가 요구되는 인도 절차 등이 모두 서비스 비용에 영향을 미치기 때문에 도로 운송을 통한 실행에 대한 압박이 커집니다. 따라서 이 부문에 해당하는 순수 도로 운송 사업자들은 멀티모달 및 복합 운송을 주력으로 하는 사업자들보다 더 어려운 수익률 상황에 직면해 있습니다.

국제 물류 시장은 2031년까지 연평균 성장률(CAGR) 7.44%로 확대될 것으로 예상되며, 독일의 완성 차량 물류 시장에서 가장 빠르게 성장하는 부문으로 꼽히고 있습니다. 독일의 조립 생산은 여전히 유럽 내외의 광범위한 딜러 및 유통업체 네트워크에 공급되고 있기 때문에 수출 흐름이 중요하며, 항만 접근성과 철도망 연결성은 경쟁 우위를 확보하는 데 있어 계속해서 핵심적인 역할을 하고 있습니다. 이 부문에서는 독일 외부의 생산 거점에서 도착하는 차량이 증가하고 있으며, 현지 유통 채널에 투입되기 전에 내륙에서 처리해야 하기 때문에 수입 규모가 더욱 빠르게 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the germany finished vehicle logistics were valued at USD 8.01 billion in 2025 and are expected to reach USD 8.52 billion in 2026 and USD 11.45 billion by 2031, growing at a CAGR of 6.09% over 2026-2031. The Germany finished vehicle logistics market is currently undergoing structural transformation as it adapts to declining conventional vehicle volumes and a rapid shift toward electric mobility. This report is Segmented by Logistics Function (Transportation, Warehousing & Distribution, Value-Added Services), by Destination (Domestic, International), by Type of Vehicles (Passenger, Commercial, Off-Highway), by End-User Industry (OEMs, Dealers, Others), and by Region (North Rhine-Westphalia, Bavaria, Baden-Wurttemberg, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Finished Vehicle Logistics Market Trends and Insights

OEM Demand for Just-in-Sequence Vehicle Deliveries

German automakers continue to run build-to-order production systems that leave little room for sequencing mistakes, so just-in-sequence delivery remains central to finished vehicle logistics contracts and to service design in the Germany finished vehicle logistics market. BMW is preparing its Munich plant for Neue Klasse production from August 2026, following a major plant overhaul. That change is directly tied to new outbound flow planning as electric and combustion programs share the same manufacturing footprint. Audi is also tightening production and logistics integration through joint Ingolstadt and Gyor activity for the Q3 and through preparations for a new electric model in Ingolstadt, with rail already embedded in body transport between sites. At the provider level, warehouse sequencing, automated movements, and real-time status sharing are no longer optional add-ons; OEMs increasingly expect them as part of standard execution. This makes technology depth more important in carrier selection because a provider now has to prove both physical handling capability and consistent event-level reporting across the vehicle journey. Operators that cannot support synchronized delivery windows and transparent milestone tracking are therefore more likely to lose share in the Germany finished vehicle logistics market when large OEM tenders are reissued.

Rail-Linked Port and Inland Terminal Capacity Expansion

Rail-linked infrastructure is becoming one of the clearest competitive advantages in the Germany finished vehicle logistics market because it reduces truck dependence, supports lower-emission contracts, and improves the quality of long-distance connections between ports and inland compounds. Duisport gives North Rhine-Westphalia an unusually strong position because it handles more than 100 million tons a year across 21 port basins, 10 container terminals, and around 200 kilometers of its own rail network. ARS Altmann AG supports this intermodal shift with more than 4,000 dedicated rail wagons, the largest privately owned vehicle rail fleet in Europe, and a major advantage in plant-to-port transport planning. OBB Rail Cargo Group expanded its Verona-Duisburg service to 10 weekly round trips in 2026, improving west German intermodal connectivity and adding resilience to cross-border automotive flows. As more flows are redesigned around intermodal execution, providers with rail access, terminal control, and strong multimodal scheduling are better positioned to capture contract growth. This is raising the value of fixed infrastructure ownership inside the Germany finished vehicle logistics market because access to rail-linked nodes now affects both service reliability and emissions performance.

Driver Shortages and Wage Pressure in Road Carrying

Germany continues to face a shortage of professional drivers, and finished vehicle logistics feels that pressure more sharply because car carrying requires specialized loading, securing, and condition-control skills. This problem affects more than just recruitment because equipment can sit idle even when order books are healthy, lowering asset utilization and slowing service recovery during demand spikes. The pressure is strongest for operators that depend heavily on domestic truck movements, where rate discipline is tight, and route flexibility is limited. Wage inflation and compliance costs also hit smaller regional carriers harder because they have less room to spread cost increases across a broader service mix. These conditions reduce the ability of road-only providers to absorb volume swings or take on more technical work around dealer and fleet deliveries. The driver gap, therefore, acts as a clear near-term restraint on the Germany finished vehicle logistics market, even though it does not alter the longer-term shift toward multimodal, compound-led value creation.

Other drivers and restraints analyzed in the detailed report include:

- EV-Specific Vehicle Handling and Pre-Delivery Processing Needs

- Digital Visibility, Damage Reduction, and Exception Management

- Infrastructure Bottlenecks Across German Corridors and Ports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 64.86% of the Germany finished vehicle logistics market share in 2025. Road transport remained the main delivery mode for dealer, leasing, and fleet handovers because last-mile vehicle distribution still depends on flexible truck access across domestic routes. Rail handled the main medium- and long-distance plant-to-port corridors, making asset ownership more valuable for operators who could control capacity directly rather than rely solely on third parties. ARS Altmann AG stood out in this layer with more than 4,000 rail wagons, giving it one of the strongest positions in rail infrastructure across Europe. Sea transport and inland waterways remained secondary within Germany itself, but they still supported export and overflow flows tied to major gateway corridors.

Warehousing and distribution is projected to grow at a 7.84% CAGR from 2026 to 2031, making it the fastest-growing logistics function in the Germany finished vehicle logistics market. The reason is not simple storage demand alone because the value shift comes from longer EV pre-delivery routines, software validation, charging readiness, campaign work, and condition-control processes before release. BLG Logistics handled 4.2 million vehicles across its network in 2025, while AutoTerminal Bremerhaven alone processed 1.25 million, underscoring how much compound throughput still matters even in softer production conditions.

Domestic flows held 62.51% of the Germany finished vehicle logistics market share in 2025, making them the largest destination category. This volume rested on dealer replenishment, leasing handovers, and fleet deliveries across the country's dense urban and industrial corridors, where service frequency and handover quality matter as much as basic route coverage. Domestic demand is relatively stable because it is tied to Germany's large new-vehicle market and to replacement cycles that continue even when export conditions weaken. At the same time, domestic work places more pressure on road-based execution because last-mile delivery windows, driver availability, and condition-sensitive handovers all affect service cost. That is why pure road-haul operators serving this layer are facing tighter margin conditions than multimodal or compound-led providers.

International logistics is forecast to expand at a 7.44% CAGR through 2031, making it the faster-moving destination layer in the Germany finished vehicle logistics market. Export flows remain important because German assembly output still serves wide dealer and distributor networks across Europe and outside Europe, which keeps port access and rail connectivity central to competitive positioning. Import flows are rising faster in this category because more vehicles are arriving from non-German production bases and require inland processing before release into local channels.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing & Distribution

- Value-added Services and Others

- Transportation

- By Destination

- Domestic

- International

- Import/Inbound

- Export/Outbound

- By Type of Vehicles

- Passenger Vehicles (Including Two and Three-Wheelers)

- Commercial Vehicles

- Off-Highway Vehicles

- By End-user Industry

- OEMs

- Dealers

- Others (Rental Companies, Fleet leasing companies, Government & Defense Fleets, etc.)

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- MOSOLF Group

- ARS Altmann AG

- BLG Logistics Group

- DSV A/S (including DB Schenker)

- Duvenbeck Group

- Hodlmayr International AG

- CAT Automobillogistik GmbH & Co. KG

- Kuehne + Nagel

- DHL Group

- Rhenus Automotive

- Schnellecke Logistics

- CEVA Logistics (CMA CGM)

- Galliker Transport AG

- Koopman Logistics Group

- Grupo CAT

- Anji Logistics Europe

- Wallenius Wilhelmsen

- United European Car Carriers (UECC)

- Hyundai GLOVIS Europe

- Autokontor Bayern GmbH

- Lagermax Autotransport GmbH

- Hellmann Worldwide Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Finished Vehicle

- 4.2 Automotive Spending Trends

- 4.3 Market Drivers

- 4.3.1 OEM Demand for Just-in-Sequence Vehicle Deliveries

- 4.3.2 Rail-Linked Port and Inland Terminal Capacity Expansion

- 4.3.3 EV-Specific Vehicle Handling and Pre-Delivery Processing Needs

- 4.3.4 Digital Visibility, Damage Reduction, and Exception Management

- 4.3.5 Low-Emission Logistics Procurement by German OEMs

- 4.3.6 Plant and Port Network Reconfiguration Toward Intermodal Flows

- 4.4 Market Restraints

- 4.4.1 Rail Slot Scarcity and Long Lead-Time Planning Constraints

- 4.4.2 Driver Shortages and Wage Pressure in Road Car Carrying

- 4.4.3 Infrastructure Bottlenecks Across German Corridors and Ports

- 4.4.4 Damage Risk, Empty Backhauls, and Asset Underutilization

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Finished Vehicle Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.2.2.1 Import/Inbound

- 5.2.2.2 Export/Outbound

- 5.3 By Type of Vehicles

- 5.3.1 Passenger Vehicles (Including Two and Three-Wheelers)

- 5.3.2 Commercial Vehicles

- 5.3.3 Off-Highway Vehicles

- 5.4 By End-user Industry

- 5.4.1 OEMs

- 5.4.2 Dealers

- 5.4.3 Others (Rental Companies, Fleet leasing companies, Government & Defense Fleets, etc.)

- 5.5 By Region

- 5.5.1 North Rhine-Westphalia

- 5.5.2 Bavaria (Bayern)

- 5.5.3 Baden-Wurttemberg

- 5.5.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 MOSOLF Group

- 6.4.2 ARS Altmann AG

- 6.4.3 BLG Logistics Group

- 6.4.4 DSV A/S (including DB Schenker)

- 6.4.5 Duvenbeck Group

- 6.4.6 Hodlmayr International AG

- 6.4.7 CAT Automobillogistik GmbH & Co. KG

- 6.4.8 Kuehne + Nagel

- 6.4.9 DHL Group

- 6.4.10 Rhenus Automotive

- 6.4.11 Schnellecke Logistics

- 6.4.12 CEVA Logistics (CMA CGM)

- 6.4.13 Galliker Transport AG

- 6.4.14 Koopman Logistics Group

- 6.4.15 Grupo CAT

- 6.4.16 Anji Logistics Europe

- 6.4.17 Wallenius Wilhelmsen

- 6.4.18 United European Car Carriers (UECC)

- 6.4.19 Hyundai GLOVIS Europe

- 6.4.20 Autokontor Bayern GmbH

- 6.4.21 Lagermax Autotransport GmbH

- 6.4.22 Hellmann Worldwide Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment