|

시장보고서

상품코드

2073305

채용 마케팅 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Recruitment Marketing Platform Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

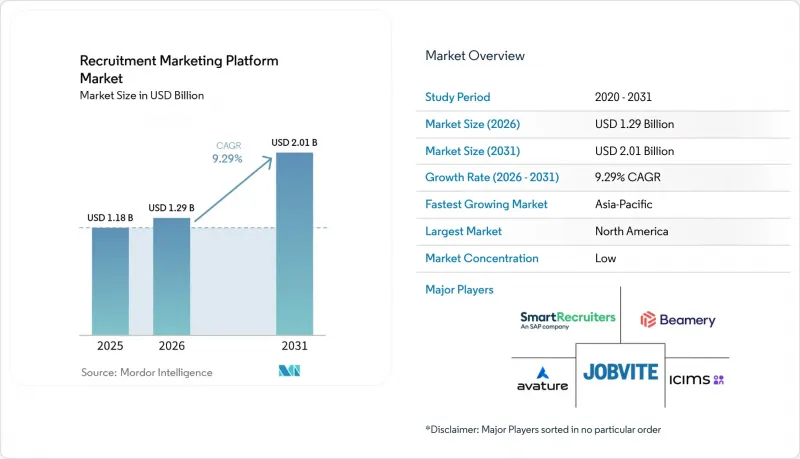

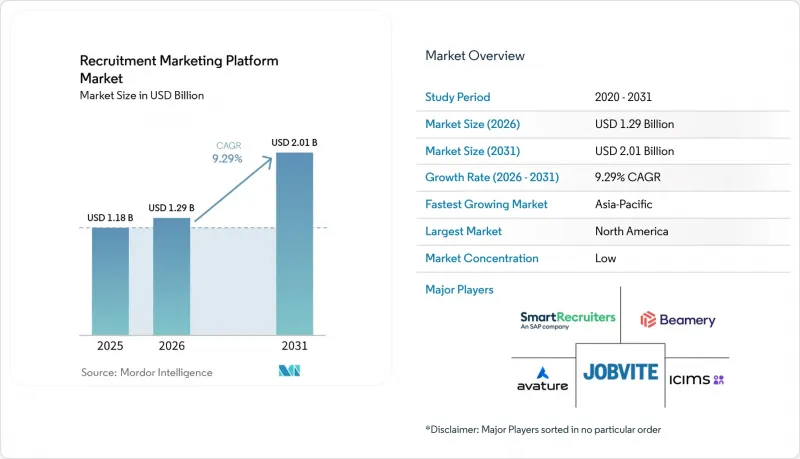

Mordor Intelligence에 의하면, 채용 마케팅 플랫폼 시장 규모는 2025년 11억 8,000만 달러로 평가되었습니다. 2026년 12억 9,000만 달러에서 2031년까지 20억 1,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.29%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어/플랫폼, 서비스), 도입 형태(클라우드 기반, On-Premise형), 조직 규모(대기업, 중소기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등), 기능(후보자 관계 관리 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 채용 마케팅 플랫폼 시장 동향 및 인사이트

프로그램형 구인 광고의 도입 확대

프로그래매틱 채용 광고는 리크루팅·마케팅 플랫폼 시장에서 전문적인 워크플로우에서 보다 일반적인 구매층으로 전환되고 있습니다. 고용주들은 특정 구인사이트에 예산을 배정하는 데만 의존하지 않고, 이를 활용하여 채널 간 지출을 실시간으로 조정하고 있습니다. 이러한 변화가 중요한 이유는 캠페인 이력이 축적되고 반복되는 채용 주기를 통해 입찰 및 전환 데이터의 유용성이 높아짐에 따라 시스템의 가치가 향상되기 때문입니다. 이러한 피드백 루프로 인해, 특히 고용주가 다양한 직종에 걸쳐 지속적으로 채용을 진행할 경우, 알고리즘을 활용한 미디어 구매가 수동 방식의 광고 게재 방식을 점차 능가하고 있습니다. 이러한 변화의 속도는 프로그램형 채용 광고가 채용 마케팅 플랫폼 시장에서 가장 빠르게 성장하고 있는 기능 부문이라는 점에 반영되어 있으며, 2031년까지의 연평균 성장률(CAGR)은 12.48%로 예측됩니다.

AI를 활용한 후보자 관계 관리의 활용 확대

AI 기반 후보자 관계 관리(CRM)는 채용 마케팅 플랫폼 시장이 활발한 채용 주기 사이에 진행되는 채용 활동을 어떻게 지원하는지에 있어 점점 더 핵심적인 역할을 수행하고 있습니다. 고용주들은 유망한 인재 풀을 유지하고, 맞춤형 접근 방식을 적용하며, 채용 담당자가 채용 가능성이 높은 후보자를 찾아낼 수 있도록 돕는 플랫폼을 점점 더 많이 찾고 있습니다. 이에 따라 CRM은 수동적인 연락처 데이터베이스에서 인재 발굴, 재참여 유도, 캠페인 시기 조정을 수행하는 능동적인 운영 단계로 변화하고 있습니다. 또한, AI를 활용한 채용 워크플로우에서 구매자들은 인간의 감독, 문서화, 감사 가능성을 기대하게 되었기 때문에 거버넌스의 중요성도 높아지고 있습니다. 그 결과, 채용 마케팅 플랫폼 시장에서는 명확한 규정 준수 체계를 갖추지 못한 채 AI 도구를 추가하는 벤더보다, 자동화 기능과 관리 기능을 결합한 벤더가 더 많은 지지를 받고 있습니다.

기존 ATS 및 HRIS와의 통합의 복잡성

기존 HR 시스템과의 통합은 여전히 채용 마케팅 플랫폼 시장의 확장에 있어 가장 뚜렷한 제약 요인 중 하나입니다. Remote는 2025년 보고서에서 HR 리더의 51%가 새로운 HRIS를 찾고 있으며, 36%는 시스템의 전면적인 교체를 검토하고 있다고 밝혔습니다. 이는 파편화된 시스템 환경에 대한 광범위한 불만을 보여주고 있습니다. 해당 보고서에서는 연동 실패로 인한 단 한 건의 규정 위반만으로도 4만 2,000달러의 손실을 초래할 수 있다고 지적하고 있으며, 이는 기술적 격차가 구매자에게 직접적인 재무적 위험으로 작용함을 보여줍니다. 따라서 주요 ATS 및 HCM 시스템과의 연동 기능을 기본으로 갖춘 공급업체는 기업 평가에서 더 유리한 입장에서 시장에 진입하고 있습니다. 채용 마케팅 플랫폼 시장에서 폭넓은 네이티브 연동 지원은 단순한 기능적 우위가 아니라, 구매 시 필수 요건으로 자리 잡고 있습니다.

부문별 분석

2025년에는 소프트웨어/플랫폼 라이선스가 매출의 78.46%를 차지하며, 채용 마케팅 플랫폼 시장에서 가장 큰 매출 기준이 되었습니다. 이 비율은 대기업 및 중견 기업의 채용 담당자들의 기술 환경에서 SaaS 구독 서비스가 얼마나 깊이 뿌리내리고 있는지를 반영하고 있습니다. 고용주들은 단일 운영 체제 내에서 캠페인 관리, 워크플로 제어, 후보자와의 소통을 필요로 하기 때문에 소프트웨어 계층은 여전히 대부분의 구매 결정의 기초가 되고 있습니다. 그렇긴 하지만, 더 빠른 성장세가 나타나는 분야는 서비스 부문으로, 2031년까지 연평균 성장률(CAGR) 10.84%로 확대될 것으로 전망됩니다. 이는 채용 마케팅 플랫폼 시장이 단순히 라이선스 이용만으로는 도입의 성공이 보장되지 않는 단계로 접어들고 있음을 보여줍니다.

서비스 분야의 성장이 가속화되고 있는 이유는 구매자들이 소프트웨어를 처음 구매한 후 도입 지원, 시스템 연동 작업, 보고서 설계 및 관리형 분석 지원을 점점 더 필요로 하고 있기 때문입니다. 이러한 추세는 플랫폼이 서로 다른 지역 및 사업 부문에 걸쳐 있는 ATS, HRIS, 분석, 미디어 시스템과 연동됨에 따라 채용 마케팅 플랫폼 업계의 운영 측면에서의 복잡성이 증가하고 있음을 시사합니다. 또한, 플랫폼의 가치가 기능의 폭넓음뿐만 아니라 측정 가능한 이용 현황과 성능을 바탕으로 평가되고 있음을 보여줍니다. 동시에, 기본적인 배포 및 참여 기능은 보다 광범위한 HCM 제품군에 통합하기 쉬워졌으며, 이로 인해 중견 소프트웨어 전문 벤더들의 활동 영역은 좁아지고 있습니다. SHRM의 보고서에 따르면, 2025년 HR 기술에 대한 지출은 전년 대비 9.1% 증가했으나, 그 지출은 '소스 투 하이어(Source to Hire)' ROI(투자 대비 효과)를 입증할 수 있는 도구와의 연계가 점점 더 강화되고 있으며, 이는 채용 마케팅 플랫폼 시장의 서비스 분야에 대한 밝은 전망을 뒷받침하는 것입니다.

2025년, 채용 마케팅 플랫폼 시장 규모의 71.18%를 클라우드 기반 도입이 차지하며, 모든 구매자 그룹에서 주류 제공 모델로 자리 잡았습니다. 또한, 2031년까지 연평균 성장률(CAGR) 10.21%를 나타낼 것으로 예측되고 있으며, 이는 신규 도입의 대부분이 클라우드 방식을 유지하고 있음을 뒷받침하고 있습니다. 그 매력은 실용성에 있습니다. 클라우드 아키텍처는 제품 업데이트를 신속하게 하고, 규정 준수를 용이하게 하며, 클라이언트 간 통합 유지보수의 범위를 넓혀주기 때문입니다. 이러한 장점은 AI 모델, 채널 커넥터, 캠페인 도구를 자주 조정해야 하는 상황에서 특히 중요합니다. 따라서 채용 마케팅 플랫폼 시장은 멀티테넌트형 SaaS 모델을 중심으로 통합이 계속 진행되고 있습니다.

On-Premise에 대한 수요는 정부, 국방 및 일부 금융 서비스 환경과 같이 규제가 엄격한 분야에서는 여전히 뿌리 깊게 자리 잡고 있습니다. 이러한 분야에서는 인프라 관리 및 데이터 저장 장소가 여전히 조달 결정에 영향을 미치고 있습니다. 또 다른 중요한 변화로, 완전한 On-Premise 방식의 비용과 유지보수 부담을 피하면서도 더 높은 제어성을 추구하는 대규모 기관에서 프라이빗 클라우드 및 하이브리드 모델의 활용이 증가하고 있습니다. 일부 대기업에서는 도입 형태뿐만 아니라 통합의 질, 거버넌스, 데이터 흐름이라는 관점에서 시스템 아키텍처를 재검토하고 있기 때문에 이러한 유연성은 중요합니다. Remote사의 조사에 따르면, 2025년 인사정보시스템(HRIS) 교체 결정의 주요 촉진요인은 통합된 시스템으로 밝혀졌습니다. 이는 현재 클라우드 선정이 생태계와의 적합성과 밀접하게 연관되어 있다는 견해를 뒷받침하는 것입니다. 채용 마케팅 플랫폼 시장에서는 기존 및 최신 인사 시스템과의 신뢰할 수 있는 연동을 실현하고, 클라우드 중심의 도입을 지원할 수 있는 벤더가 시스템 교체 기회를 포착하는 데 유리한 입장에 있습니다.

지역별 분석

2025년, 북미는 채용 마케팅 플랫폼 시장 점유율의 38.64%를 차지하며, 이 지역은 1위 자리를 유지했습니다. 이러한 추세는 성숙한 HR 기술의 도입, 기업의 강력한 구매력, 그리고 충분히 발전된 채용 소프트웨어 생태계에 기인합니다. SHRM의 보고서에 따르면, 2025년 HR 예산은 전년 대비 9.1% 증가했으며, HR 비용 대 영업 비용 비율의 중앙값은 2.4%였습니다. 이는 광범위한 비용 절감 움직임에도 불구하고, 도입 기술에 대한 지출이 유지되었음을 시사합니다. 미국은 여전히 핵심 시장이며, 캐나다도 비슷한 기업 구매 패턴을 보였으나, 멕시코는 도입 곡선의 초기 단계에 머물렀습니다. 채용 마케팅 플랫폼 시장 전체에서 이 지역은 SAP의 SmartRecruiters 인수와 Workday의 Paradox 인수 등 대규모 업계 재편이 활발히 이루어진 점에서도 두드러지며, 이로 인해 많은 독립 벤더들경쟁 구도가 변화했습니다.

유럽은 독일, 영국, 프랑스의 기업 수요에 힘입어 채용 마케팅 플랫폼 시장에서 여전히 2위 지역 시장을 유지했습니다. 특히 독일의 경우, 해당국의 엄격한 개인정보 보호 및 동의 관련 요건이 EU 전역에서 플랫폼을 도입할 때 실질적인 규정 준수 기준으로 작용하는 경우가 많기 때문에 큰 비중을 차지했습니다. 독일과 북유럽 국가들의 기업 구매 담당자들은 정보 보안 인증을 차별화 요소가 아닌 기본적인 조달 요건으로 간주하는 경향이 강해지고 있습니다. EU AI법에 따라 고용주가 투명성, 문서화, 인적 감독 요건에 대해 현행 시스템을 재검토함에 따라, 중기적인 플랫폼 업데이트 주기가 촉진될 가능성이 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.93%를 기록하며 성장할 것으로 예상되며, 채용 마케팅 플랫폼 시장에서 가장 두드러진 성장을 보일 지역 부문이 될 전망입니다. 이 지역은 디지털 채용의 급속한 확산, 풍부한 인재 풀, 그리고 인도와 동남아시아 전역에서 활발한 모바일 이용의 혜택을 누리고 있습니다. 2025년 9월, eRoad의 보고서에 따르면, 중국 내 채용 활동에 AI 도입률은 조사 대상 기업의 84.13%에 달하며, AI를 활용한 채용 도구가 이미 주류를 이루고 있는 시장임이 드러났습니다. 중동도 사우디아라비아와 UAE에서 현지화를 중시하는 채용 프로그램을 통해 진전을 보이고 있지만, 아프리카는 여전히 초기 단계에 있으며, 남아프리카공화국과 나이지리아가 가장 두드러진 도입 거점으로 자리 잡고 있습니다. 남미 지역은 브라질과 아르헨티나를 중심으로 시장을 지속적으로 확대하고 있으며, 채용 마케팅 플랫폼 시장에서는 현지 언어 지원 기능과 노동 보고 규정 준수 여부가 중요한 선정 기준으로 작용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the recruitment marketing platform market size is projected to expand from USD 1.18 billion in 2025 and USD 1.29 billion in 2026 to USD 2.01 billion by 2031, registering a CAGR of 9.29% between 2026 and 2031.

This report is Segmented by Component (Software/Platform, and Services), Deployment Type (Cloud-Based, and On-Premises), Organization Size (Large Enterprise, and SMEs), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), Functionality (Candidate Relationship Management, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Recruitment Marketing Platform Market Trends and Insights

Growth In Programmatic Job Advertising Adoption

Programmatic job advertising is moving from a specialist workflow into a more standard buying layer within the recruitment marketing platform market. Employers are using it to shift spending across channels in real time instead of relying on fixed job board allocations. This change matters because the value of the system improves as campaign history builds and as bid and conversion data become more useful over repeated hiring cycles. That feedback loop is helping algorithmic media buying pull ahead of manual placement methods, especially where employers recruit continuously across many roles. The pace of that shift is reflected in programmatic job advertising being the fastest-growing functionality segment in the recruitment marketing platform market, with a projected 12.48% CAGR through 2031.

Increasing Use Of AI-Powered Candidate Relationship Management

AI-led candidate relationship management is becoming more central to how the recruitment marketing platform market supports hiring between active requisition cycles. Employers increasingly want platforms that can help them maintain warm talent pools, personalize outreach, and guide recruiters toward higher-probability candidates. This is changing CRM from a passive contact database into an active operating layer for sourcing, re-engagement, and campaign timing. It also raises the importance of governance, because buyers now expect human oversight, documentation, and auditability in AI-supported recruiting workflows. As a result, the recruitment marketing platform market is favoring vendors that combine automation with control features rather than vendors that add AI tools without a clear compliance structure.

Integration Complexity With Legacy ATS And HRIS

Integration with older HR systems remains one of the clearest limits on expansion in the recruitment marketing platform market. Remote reported in 2025 that 51% of HR leaders were searching for a new HRIS, and 36% were considering a full system switch, which points to broad dissatisfaction with fragmented system environments. The same report noted that a single compliance incident linked to integration failure could cost USD 42,000, which turns technical gaps into a direct financial risk for buyers. This is why vendors with pre-built connectors to major ATS and HCM systems enter enterprise evaluations from a stronger position. In the recruitment marketing platform market, broad native integration support is becoming a buying requirement rather than a feature advantage.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Employer-Branding Budgets Among Enterprises

- Surge In Mobile-First Job Search Behavior

- Data-Privacy And Compliance Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software/platform licenses accounted for 78.46% of revenue in 2025, giving them the largest revenue base in the recruitment marketing platform market. That weighting reflects how deeply SaaS subscriptions are embedded in hiring technology environments across large enterprise and mid-market buyers. The software layer still anchors most buying decisions because employers need campaign management, workflow control, and candidate engagement within a single operating system. Even so, the faster movement is occurring in services, which are forecast to expand at a 10.84% CAGR through 2031. This shows that the recruitment marketing platform market is moving into a phase where successful adoption depends on more than license access.

Services are growing faster because buyers increasingly need implementation help, integration work, reporting design, and managed analytics support after the initial software purchase. This pattern suggests that the recruitment marketing platform industry is becoming more operationally complex as platforms connect with ATS, HRIS, analytics, and media systems across different regions and business units. It also indicates that platform value is being judged on measurable usage and performance, not just on feature breadth. At the same time, basic distribution and engagement features are becoming easier for broader HCM suites to bundle, which narrows room for mid-tier software-only vendors. SHRM reported that HR technology spending rose 9.1% year over year in 2025, but that spending was increasingly tied to tools that could show return from source to hire, which supports the stronger services outlook in the recruitment marketing platform market.

Cloud-based deployment accounted for 71.18% of the recruitment marketing platform market size in 2025, making it the dominant delivery model across buyer groups. It is also forecast to grow at a 10.21% CAGR through 2031, which confirms that most new adoption is staying on the cloud path. The appeal is practical because cloud architectures support faster product updates, easier compliance changes, and broader integration maintenance across clients. These advantages are especially important where AI models, channel connectors, and campaign tools need frequent adjustment. For that reason, the recruitment marketing platform market is continuing to consolidate around multi-tenant SaaS models.

On-premises demand remains prevalent in regulated settings such as government, defense, and selected financial services environments, where infrastructure control and data residency continue to influence procurement decisions. A meaningful secondary shift is the rise of private cloud and hybrid models for large institutions that want more control without full on-premises cost and maintenance. That flexibility matters because some large employers are reevaluating system architecture through the lens of integration quality, governance, and data flow rather than deployment style alone. Remote found that unified system integration was the main driver of HRIS replacement decisions in 2025, which supports the view that cloud selection is now tied closely to ecosystem fit. In the recruitment marketing platform market, vendors that can support cloud-led deployment with reliable integration into legacy and modern HR systems are in a better position to capture replacement cycles.

Complete Report Scope:

- By Component

- Software/Platform

- Services

- By Deployment Type

- Cloud-based

- On-premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Functionality

- Candidate Relationship Management

- Job Distribution and Posting

- Recruitment Analytics and Reporting

- Employer Branding

- Programmatic Job Advertising

- Other Functionality Types

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 38.64% of the recruitment marketing platform market share in 2025, which kept the region in the top position. That lead came from mature HR technology adoption, strong enterprise buying capacity, and a well-developed recruiting software ecosystem. SHRM reported that HR budgets rose 9.1% year over year in 2025 and that the median HR-expense-to-operating-expense ratio was 2.4%, which suggests that hiring technology spending remained protected despite broader cost discipline. The United States remained the core market, while Canada followed a similar enterprise-buying pattern, and Mexico remained earlier in its adoption curve. Across the recruitment marketing platform market, the region also stood out for major consolidation activity, including SAP's acquisition of SmartRecruiters and Workday's acquisition of Paradox, which changed the competitive landscape for many independent vendors.

Europe remained the second-largest regional market in the recruitment marketing platform market, supported by enterprise demand in Germany, the United Kingdom, and France. Germany carried particular weight because strict privacy and consent requirements there often functioned as a practical compliance benchmark for wider EU platform adoption. Enterprise buyers across Germany and the Nordics increasingly treated information security certification as a basic procurement requirement rather than as a differentiator. The EU AI Act is likely to drive a medium-term platform refresh cycle as employers review current systems for transparency, documentation, and human oversight needs.

Asia-Pacific is projected to grow at an 11.93% CAGR through 2031, making it the fastest-growing regional segment in the recruitment marketing platform market size. The region is gaining from rapid digital hiring adoption, large candidate pools, and strong mobile engagement behavior across India and Southeast Asia. In September 2025, eRoad reported that AI adoption in Chinese recruitment reached 84.13% of surveyed companies, pointing to a market where AI-enabled hiring tools are already mainstream. The Middle East is also advancing through localization-driven hiring programs in Saudi Arabia and the UAE, while Africa remains earlier stage with South Africa and Nigeria as the clearest adoption hubs. South America continues to build from Brazil and Argentina, where local language capability and labor reporting fit remain important selection criteria in the recruitment marketing platform market.

- Jobvite Inc.

- Avature Holding Corp.

- iCIMS Inc.

- Beamery Ltd.

- SmartRecruiters Inc.

- Phenom People Inc.

- Workable Technology Limited

- Zoho Corporation Pvt. Ltd.

- Symphony Talent LLC

- Sense Talent Labs Inc.

- Recruitee B.V.

- Hireology Inc.

- PageUp Pty Ltd

- Talenteria Inc.

- Jobilla Oy

- GR8 People Inc.

- Yello Inc.

- TalentLyft (Zero Molecule d.o.o.)

- Radancy

- SmartDreamers S.R.L.

- Clinch Technology Ltd.

- Eightfold AI Inc.

- Breezy HR Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Programmatic Job Advertising Adoption

- 4.2.2 Increasing Use of AI-Powered Candidate Relationship Management

- 4.2.3 Expansion of Employer-Branding Budgets Among Enterprises

- 4.2.4 Surge in Mobile-First Job Search Behaviour

- 4.2.5 Rising Demand for Data-Driven Recruiting Metrics

- 4.2.6 Acceleration of Remote and Hybrid Work Hiring Models

- 4.3 Market Restraints

- 4.3.1 Integration Complexity with Legacy ATS and HRIS

- 4.3.2 Data-Privacy and Compliance Constraints (GDPR, CCPA)

- 4.3.3 Budget Pressures in SME Segments During Economic Downturns

- 4.3.4 Limited Analytics Maturity in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software/Platform

- 5.1.2 Services

- 5.2 By Deployment Type

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Industrial Manufacturing

- 5.4.4 Healthcare and Lifesciences

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-User Industries

- 5.5 By Functionality

- 5.5.1 Candidate Relationship Management

- 5.5.2 Job Distribution and Posting

- 5.5.3 Recruitment Analytics and Reporting

- 5.5.4 Employer Branding

- 5.5.5 Programmatic Job Advertising

- 5.5.6 Other Functionality Types

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Jobvite Inc.

- 6.4.2 Avature Holding Corp.

- 6.4.3 iCIMS Inc.

- 6.4.4 Beamery Ltd.

- 6.4.5 SmartRecruiters Inc.

- 6.4.6 Phenom People Inc.

- 6.4.7 Workable Technology Limited

- 6.4.8 Zoho Corporation Pvt. Ltd.

- 6.4.9 Symphony Talent LLC

- 6.4.10 Sense Talent Labs Inc.

- 6.4.11 Recruitee B.V.

- 6.4.12 Hireology Inc.

- 6.4.13 PageUp Pty Ltd

- 6.4.14 Talenteria Inc.

- 6.4.15 Jobilla Oy

- 6.4.16 GR8 People Inc.

- 6.4.17 Yello Inc.

- 6.4.18 TalentLyft (Zero Molecule d.o.o.)

- 6.4.19 Radancy

- 6.4.20 SmartDreamers S.R.L.

- 6.4.21 Clinch Technology Ltd.

- 6.4.22 Eightfold AI Inc.

- 6.4.23 Breezy HR Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment