|

시장보고서

상품코드

2073309

소매 및 호스피탈리티 분야 급여 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Payroll Software In Retail and Hospitality - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

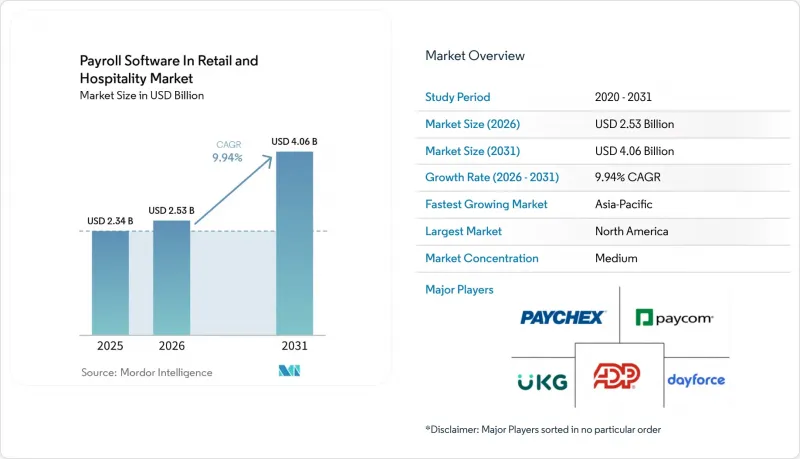

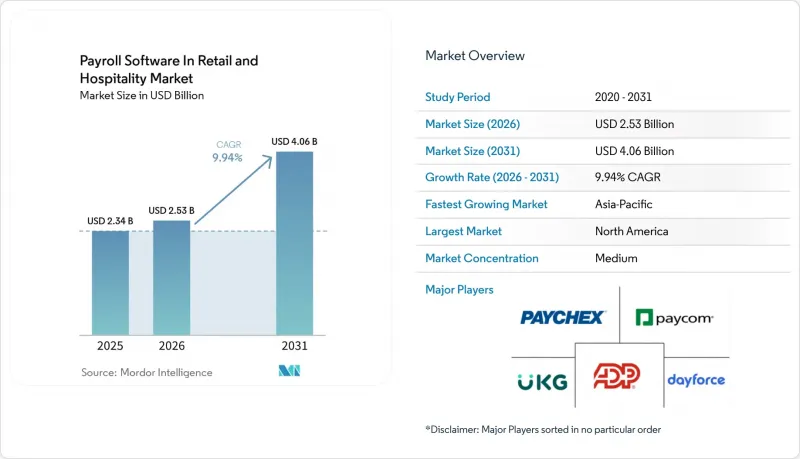

Mordor Intelligence에 의하면, 소매 및 호스피탈리티 분야 급여 소프트웨어 시장 규모는 2025년에 23억 4,000만 달러로 평가되었습니다. 2026년부터 2031년에 걸쳐 CAGR 9.94%로 성장해 2031년에는 25억 3,000만 달러 및 40억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 조직 규모(대기업 및 중소기업), 배포 방식(클라우드 및 On-Premise), 기능(핵심 급여 계산 처리, 근태 관리, 급여 분석 및 보고서 작성, 세무·규정 준수 관리, 기타 기능) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소매 및 호스피탈리티 분야 급여 소프트웨어 시장 동향 및 인사이트

클라우드 기반 급여 계산 솔루션의 도입 확대

클라우드 급여 계산은 단순한 저비용 IT 옵션에 그치지 않고, 여러 거점을 보유한 소매업체나 호텔 및 레스토랑 기업 그룹에게 실용적인 운영 기준으로 자리 잡고 있습니다. 클라우드 시스템은 각 매장 간의 실시간 동기화, 손쉬운 업데이트, 그리고 현장 직원 및 관리직의 모바일 접근을 지원하기 때문에 소매 및 호스피탈리티 분야 급여 소프트웨어 시장은 이러한 변화의 혜택을 누리고 있습니다. UKG사는 자사의 “One View"다국적 급여 계산 솔루션이 120개 통화와 150개국 이상의 급여 계산을 지원한다고 밝혔으며, 이는 전 세계에 흩어져 있는 직원을 둔 고용주에게 클라우드 아키텍처가 현재 제공하는 규모의 경제를 보여줍니다. 이는 소매 및 호스피탈리티 업계의 급여 계산 소프트웨어 시장이 규정 준수 및 업무 규율 두 가지 측면에서 성장 동력을 얻고 있음을 의미하며, ‘클라우드 우선’ 전략을 추구하는 벤더들에게 명확한 단기적 우위를 제공합니다.

소매 및 호스피탈리티 업계에서 규정 준수의 복잡성 증가

소매 및 호스피탈리티 분야의 급여 계산에서는 팁 처리, 초과근무 규정, 최저임금 요건, 그리고 지역별 신고 기준에 따른 끊임없는 변화에 대응해야 합니다. 분산되어 있거나 수작업으로 이루어지는 급여 계산 체계에서는 빈번한 규정 변경을 따라잡기가 훨씬 어렵기 때문에 소매 및 호스피탈리티 분야 급여 소프트웨어는 이러한 압박으로 인해 지지를 얻고 있습니다. Strada Global의 보고서에 따르면, 2025년에는 국가별 급여 계산 복잡도 지수가 평균 5% 상승하여, 시장 전반에 걸쳐 급여 계산 규제를 관리하는 것이 점점 더 어려워지고 있음을 뒷받침했습니다. 미국에서는 IRS 공고 2025-69에 따라, 2026 과세 연도부터 적격 팁과 적격 초과근무 수당에 대해 별도의 W-2 보고가 의무화됨이 확인되었습니다. 이로 인해 각 벤더사는 칩 추적, 원천징수 및 보고 논리를 재설계할 수밖에 없게 되었습니다. 프랑스에서도 호스피탈리티 업계의 급여 계산 시, 야간 근무 수당, 분할 근무 수당, 일요일 및 공휴일 급여, CCN HCR 프레임워크에 따른 현물 급여로서의 식사 처리 등 업계 특유의 계산 사항을 고려해야 합니다. 이로 인해 전문적인 급여 계산 엔진의 가치가 높아지고 있습니다. 따라서 소매 및 호스피탈리티 업계의 급여 계산 소프트웨어 분야에서는 규정 준수 대응에 대한 깊은 전문 지식을 갖춘 공급업체가 우위를 점하고 있는 반면, 소규모 공급업체들은 그 속도를 따라잡아야 한다는 압박감을 점점 더 강하게 느끼고 있습니다.

소규모 호스피탈리티 업계 사업자의 높은 비용 민감도와 낮은 이익률

소규모 호스피탈리티 사업자들은 여전히 가격에 매우 민감하여, 운영상의 이점이 분명하더라도 급여 계산 소프트웨어의 보급을 저해하는 요인이 되고 있습니다. 소매 및 호스피탈리티 분야 급여 소프트웨어는 이러한 장벽에 가장 크게 직면해 있습니다. 레스토랑, 카페, 소규모 호텔 등은 이익률이 낮아 새로운 월정액 구독 서비스를 도입할 여지가 제한적이기 때문입니다. PayFit사의 지적에 따르면, 음식점의 세전 이익률은 3-5% 정도인 반면, 인건비는 매출액의 30-40%를 차지하는 경우가 많아 소프트웨어 투자에 할당할 수 있는 재량 예산은 거의 남아 있지 않습니다. 이러한 압박으로 인해 소규모 사업주들은 기능이 풍부한 급여 계산 플랫폼 대신, 외부에 급여 계산을 위탁하거나, 회계사가 주도하는 업무 흐름, 혹은 기본적인 디지털 도구를 선택하는 경향이 있습니다. 소매 및 호스피탈리티 분야의 급여 계산 소프트웨어의 경우, 직원 수 50명 미만의 기업에 도입을 촉진하기 위해서는 공급업체가 보급형 가격 정책, 모듈식 패키지 구성, 그리고 명확한 투자 회수 전망을 마련해야 함을 의미합니다.

부문별 분석

2025년, 소프트웨어는 시장의 77.48%를 차지하며 소매 및 호스피탈리티 분야 급여 소프트웨어 전체에서 계속해서 가장 큰 수익원으로 자리매김했습니다. 이 지위는 처리, 규정 준수 대응 및 직원 데이터를 단일 환경에서 통합하는 구독형 급여 계산 엔진이 수행하는 핵심적인 역할을 반영하고 있습니다. 구매자는 특히 근태 기록, 세무 처리 및 보고의 정확성을 엄격하게 관리해야 하는 경우, 소프트웨어 계층을 “시스템 오브 레코드(핵심 시스템)"라고 계속 받아들이고 있습니다. 이러한 구매자의 행동 패턴은 통합 수준이 높은 플랫폼이 소매 및 호스피탈리티 분야 급여 소프트웨어 시장에서 여전히 지출의 대부분을 차지하고 있는 이유를 설명해 줍니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 10.68%로 확대되고 있으며, 소매·호스피탈리티 업계의 급여 계산 소프트웨어 시장 규모에서 가장 빠르게 성장하는 구성 요소로 자리매김하고 있습니다. 이러한 성장은 일회성 도입이라기보다는 관리형 급여 계산 아웃소싱, 규정 준수 지원, 그리고 공급업체 주도의 업무 수행에 의해 주도되고 있습니다. SD Worx에 따르면, 이 회사는 스페인과 프랑스의 호텔 브랜드 ‘Hesperia"이나 “Ibis"를 포함한 95,000개 이상의 고객사를 대상으로 매월 600만 건 이상의 급여 계산을 처리하고 있으며, 이는 서비스의 심도가 대량 처리가 필요한 급여 계산 환경을 어떻게 뒷받침하고 있는지를 보여줍니다. 이러한 변화로 인해, 소매·호텔·외식 업계의 급여 계산 소프트웨어 분야에서 ‘구매"와 “자체 개발"의 균형이 변화하고 있습니다. 이는 복잡한 근무 일정을 관리해야 하고 인사팀 인력이 제한적인 고용주들이 소프트웨어 소유권과 마찬가지로 위험 전가를 점점 더 중요하게 여기고 있기 때문입니다. 인터넷 서비스 제공업체가 신고, 계산, 현지 규정 준수 업무를 직접 관리하게 되면 고객 유지율이 높아지고, 타사로의 전환이 어려워집니다. 따라서 수익의 대부분은 여전히 소프트웨어가 차지하고 있지만, 서비스 부문의 성장 속도는 더 빨라지고 있습니다. 따라서 소매 및 호텔·외식 업계의 급여 계산 소프트웨어 시장은 소프트웨어가 핵심이 되는 플랫폼을 구축하고 서비스가 시간이 지남에 따라 고객 가치를 심화시켜 나가는 모델로 전환되고 있습니다.

2025년, 소매·호텔·외식 업계의 급여 계산 소프트웨어 시장 점유율의 64.92%를 대기업이 차지했으며, 이는 해당 업계에서 급여 계산이 복잡하고 계약 규모가 크기 때문입니다. 대형 소매업체와 호텔 그룹은 다국적 환경 대응, 통합된 직원 데이터, 그리고 관련 인사 시스템과의 원활한 연동이 필요합니다. 또한, 더 많은 현장 직원, 더 많은 사업장, 그리고 더욱 엄격해진 규정 준수 요건을 관리해야 하기 때문에 급여 계산 아키텍처에 대한 막대한 투자가 정당화됩니다. 이로 인해 소매 및 호스피탈리티 분야 급여 소프트웨어 분야에서 대기업 고객이 여전히 수익의 중심을 차지하고 있습니다.

한편, 중소기업(SME)은 2031년까지 연평균 성장률(CAGR) 10.12%를 나타낼 것으로 예측되며, 더욱 빠르게 확대되고 있는 고객층입니다. 이러한 성장은 클라우드 네이티브 가격 책정, 모바일 직원 셀프 서비스, 그리고 급여 계산 및 실용적인 규정 준수 자동화를 결합한 제품에 의해 뒷받침되고 있습니다. UKG가 2025년 12월에 Inova Payroll을 인수한 것은 일선 직원을 다수 고용하고 있는 4,000개 이상의 중소기업을 지원해 온 이 회사의 사례에서도 알 수 있듯이, 주요 벤더들이 아웃소싱 및 중소기업의 급여 계산을 단순한 부수적인 부문이 아닌 전략적 성장 영역으로 간주하고 있음을 보여줍니다. 엔터프라이즈용 벤더들이 하류 시장으로 진출하는 한편, 신규 진출기업들이 더욱 폭넓은 제품 번들을 무기로 하이엔드 시장에 진출하는 가운데, 소매 및 호스피탈리티 분야 급여 소프트웨어는 이러한 변화에 대응해 나가고 있습니다. 그동안 중소기업 구매자들은 레거시 플랫폼을 통한 지원이 가장 부족했으나, 그 격차는 점차 줄어들고 있습니다. 이러한 변화로 인해, 엔터프라이즈 계약이 여전히 주요 수익원인 것은 사실이지만, 소매 및 호스피탈리티 분야 급여 소프트웨어 시장은 2031년까지 더 폭넓은 성장 기반을 유지할 것으로 전망됩니다. 또한, 기능의 충실도뿐만 아니라 가격, 도입 속도, 사용 편의성 등의 요소가 중소기업에게 더 중요하기 때문에 이러한 측면에서의 경쟁 압력도 높아지고 있습니다.

지역별 분석

2025년, 북미는 소매 및 호텔·외식 업계의 급여 계산 소프트웨어 시장 점유율의 35.74%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역은 성숙한 급여 계산 소프트웨어 생태계, 밀집된 매장 및 시설 네트워크, 시간제 근로자를 위한 일정 관리 도구의 활발한 활용 등 여러 이점을 누리고 있습니다. 미국은 복잡한 임금 및 초과근무 규정은 물론, 팁 제도나 교대 근무제를 도입한 고용주가 다수 존재하기 때문에 여전히 주요 수익원으로 자리 잡고 있습니다. IRS 공지 2025-69에 따라, 2026 과세연도부터 “적격 칩" 및 “적격 초과근무 수당"에 대한 개별 보고 요건이 확인되면서, 급여 계산 시스템의 업데이트 필요성이 즉시 대두되었습니다. 캐나다의 경우, 주별 급여 계산 방식의 차이와 안정적인 정규직 고용 기반 덕분에 꾸준한 수요가 예상되지만, 멕시코는 클라우드 기반 급여 계산 시스템의 도입이 아직 확대 단계에 있기 때문에 시장 침투율이 비교적 낮은 기회로 작용하고 있습니다.

유럽은 규모보다는 규정 준수 요건의 밀도 면에서 두드러지며, 이로 인해 전문화된 급여 계산 플랫폼에 명확한 역할이 부여되고 있습니다. 프랑스에서는 호텔, 카페, 레스토랑의 급여 계산 시 CCN HCR 체계에 따라 야간 근무 수당, 분할 근무 수당, 일요일 및 공휴일 급여, 그리고 현물 급여 형태의 식사비 계산을 고려해야 합니다. 이로 인해 고용주들은 전용으로 설계되었거나 고도로 맞춤화된 급여 계산 시스템을 도입할 수밖에 없게 되었습니다. 또한, 프랑스에서는 DSN(디지털 급여 신고) 제출이 의무화되어 있으며, 정확하고 시기적절한 디지털 제출이 권장되고 있기 때문에 최신 급여 계산 소프트웨어 도입이 업무상 이점으로 더욱 부각되고 있습니다. 이러한 상황은 소매 및 호스피탈리티 분야의 급여 계산 소프트웨어 전반에 대한 수요를 뒷받침하고 있으며, 특히 업계 협약이 급여 규정을 직접 규정하고 있는 분야에서는 이러한 경향이 두드러집니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역이며, 소매 및 호스피탈리티 분야 급여 소프트웨어 시장 규모는 2031년까지 연평균 성장률(CAGR) 11.06%로 확대될 것으로 예측됩니다. 이러한 성장은 서비스업 분야의 노동 정규화, 호스피탈리티 업무에서의 디지털 도입 확대, 그리고 모바일 우선 급여 계산 플랫폼에 대한 관심 증가에 힘입어 이루어지고 있습니다. 인도는 그 대표적인 예입니다. 현지 상황에 맞춘 이 제품은 합리적인 가격의 실용적인 규정 준수 도구를 필요로 하는 호스피탈리티 업계의 고용주를 위해 급여 계산과 PF(직원 적립 기금), ESI(직원 사회보험), TDS(원천징수세) 처리 기능을 이미 통합하고 있기 때문입니다. 또한, 이 지역 전체적으로 현장 직원의 이직률이 높기 때문에 신속한 온보딩 및 급여 계산과 연동된 직원용 액세스 도구의 가치가 높아지고 있습니다. 따라서 현재 매출액 기준으로는 북미가 여전히 1위를 차지하고 있지만, 소매 및 호스피탈리티 분야 급여 소프트웨어 시장은 성숙한 지역보다 아시아태평양에서 빠르게 성장하고 있습니다. 이러한 주요 지역 이외의 곳에서는 도입 현황에 여전히 편차가 나타나고 있지만, 관광 활동의 활성화와 정규직 고용 확대가 중기적인 수요를 지속적으로 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the payroll software in retail and hospitality market size was USD 2.34 billion in 2025 and is projected to reach USD 2.53 billion and USD 4.06 billion by 2031, at a CAGR of 9.94% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, and SMEs), Deployment Mode (Cloud, and On-Premises), Functionality (Core Payroll Processing, Time and Attendance Management, Payroll Analytics and Reporting, Tax and Compliance Management, and Other Functionalities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Payroll Software In Retail and Hospitality Market Trends and Insights

Growing Adoption Of Cloud-Based Payroll Solutions

Cloud payroll has become a practical operating standard for multi-location retailers and hospitality groups, not just a lower-cost IT option. The payroll software in retail and hospitality market is benefiting from this shift because cloud systems support real-time synchronization across outlets, easier updates, and mobile access for frontline workers and managers. UKG stated that its One View multi-country payroll suite supports payroll across 120 currencies and more than 150 countries, which shows the scale advantage that cloud architecture now offers to employers with distributed workforces. This means the payroll software in retail and hospitality market is being pushed by compliance and operating discipline at the same time, which gives cloud-first vendors a clear near-term advantage.

Increasing Compliance Complexity In Retail And Hospitality

Retail and hospitality payroll must absorb constant changes in tip treatment, overtime rules, minimum wage requirements, and location-specific filing standards. The payroll software in retail and hospitality market is gaining support from this pressure because fragmented or manual payroll setups are much less able to keep pace with frequent rule changes. Strada Global reported that per-country payroll complexity scores rose by an average of 5% in 2025, which confirms that payroll regulation is becoming more difficult to manage across markets. In the United States, IRS Notice 2025-69 confirmed separate W-2 reporting for qualified tips and qualified overtime compensation starting with the 2026 tax year, which forces vendors to redesign tip-tracking, withholding, and reporting logic. In France, hospitality payroll must also account for sector-specific calculations such as night work premiums, split-shift allowances, Sunday and holiday pay, and benefit-in-kind meal treatment under the CCN HCR framework, which raises the value of specialized payroll engines. The payroll software in retail and hospitality market is therefore favoring providers with dedicated compliance engineering depth, while smaller vendors face growing pressure to keep up.

High Cost Sensitivity And Narrow Margins In Small Hospitality Businesses

Small hospitality operators remain highly price sensitive, which limits payroll software penetration even when the operational case is clear. The payroll software in retail and hospitality market faces this friction most strongly, where restaurants, cafes, and small hotels operate with thin margins and limited room for new monthly subscriptions. PayFit noted that food and beverage establishments often run on pre-tax margins of 3-5%, while personnel costs can represent 30-40% of revenue, which leaves little discretionary budget for software spend. This pressure tends to push very small employers toward external payroll processing, accountant-led workflows, or basic digital tools instead of full-featured payroll platforms. For the payroll software in retail and hospitality market, that means vendors need entry-level pricing, modular packaging, and a clear payback story if they want stronger adoption below the 50-employee threshold.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand For Integrated HR And Payroll Suites Among SMEs

- Workforce Digitalization Accelerated By COVID-19 Recovery

- Data Security And Privacy Concerns Over SaaS Payroll

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 77.48% of the market in 2025, which kept it as the leading revenue component across the payroll software in retail and hospitality market. That position reflects the central role of subscription-based payroll engines that combine processing, compliance support, and workforce data in one environment. Buyers continue to treat the software layer as the system of record, especially when they need strong control over time capture, tax treatment, and reporting accuracy. The same buyer behavior also explains why platforms with stronger integration depth still command the largest part of spending in the payroll software in retail and hospitality market.

The services segment is expanding at a 10.68% CAGR through 2031, which makes it the faster-growing component in the payroll software in retail and hospitality market size. Growth is being driven less by one-time implementation and more by managed payroll outsourcing, compliance support, and vendor-led operational execution. SD Worx stated that it processes more than 6 million payrolls each month across more than 95,000 clients, including hotel brands such as Hesperia and Ibis in Spain and France, which shows how service depth supports large-volume payroll environments. This shift changes the buy-versus-build balance in the payroll software in retail and hospitality industry because employers with complex schedules and limited HR teams increasingly value risk transfer as much as software ownership. Once a provider manages filings, calculations, and local compliance tasks directly, customer stickiness rises and replacement becomes harder. That is why services is growing faster even though software still anchors most revenue. The payroll software in retail and hospitality market is therefore moving toward a model where software creates the core platform and services deepen account value over time.

Large enterprises held 64.92% of the payroll software in retail and hospitality market share in 2025, which reflects their broader payroll complexity and higher contract values. Large retailers and hotel groups need multi-country support, consolidated workforce data, and dependable integration with adjacent HR systems. They also manage larger frontline headcounts, more locations, and heavier compliance exposure, which supports premium spending on payroll architecture. This keeps enterprise accounts central to revenue across the payroll software in retail and hospitality market.

At the same time, SMEs are projected to grow at a 10.12% CAGR through 2031, making them the faster-moving customer group. That growth is supported by cloud-native pricing, mobile employee self-service, and products that package payroll with practical compliance automation. UKG's December 2025 acquisition of Inova Payroll, which supported more than 4,000 SMBs with frontline-heavy workforces, showed that major vendors see outsourced and smaller business payroll as a strategic growth zone rather than a side segment. The payroll software in retail and hospitality industry is adjusting to this shift as enterprise vendors move downstream and newer entrants move upmarket with broader product bundles. SME buyers were historically the least well served by legacy platforms, but that gap is narrowing. This change should keep the payroll software in retail and hospitality market on a broader growth base through 2031, even as enterprise contracts remain the main revenue anchor. It also raises competitive pressure on pricing, onboarding speed, and ease of use, because these factors matter more to SMEs than feature depth alone.

Complete Report Scope:

- By Component

- Software

- Services

- By Organization Size

- Large Enterprises

- SMEs

- By Deployment Mode

- Cloud

- On-Premises

- By Functionality

- Core Payroll Processing

- Time and Attendance Management

- Payroll Analytics and Reporting

- Tax and Compliance Management

- Other Functionalities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America accounted for 35.74% of the payroll software in retail and hospitality market share in 2025, which made it the largest regional contributor. The region benefits from a mature payroll software ecosystem, dense store and property networks, and strong use of scheduling tools for hourly labor. The United States remains the main revenue center because it combines complex wage and overtime rules with a large base of tipped and shift-based employers. IRS Notice 2025-69 added another layer by confirming separate reporting requirements for qualified tips and qualified overtime compensation from the 2026 tax year, which immediately raised the need for payroll system updates. Canada adds steady demand through provincial payroll variation and a stable formal employment base, while Mexico presents a more underpenetrated opportunity where cloud payroll adoption is still building.

Europe stands out less for size than for compliance density, and that gives specialized payroll platforms a clear role. In France, payroll for hotels, cafes, and restaurants must account for night-shift premiums, split-shift allowances, Sunday and holiday pay, and benefit-in-kind meal calculations under the CCN HCR framework, which pushes employers toward purpose-built or heavily configured payroll systems. France also faces DSN filing demands that reward accurate and timely digital submission, reinforcing the operational case for modern payroll software. These conditions support software and service demand across the payroll software in retail and hospitality market, especially where sector agreements shape pay rules directly.

Asia-Pacific is the fastest-growing region, with the payroll software in retail and hospitality market size expected to expand at an 11.06% CAGR through 2031. Growth is supported by formalization in service labor, rising digital adoption in hospitality operations, and stronger interest in mobile-first payroll platforms. India is a key example because locally relevant products are already packaging payroll with PF, ESI, and TDS handling for hospitality employers that need practical compliance tools at accessible price points. The broader region also benefits from high frontline turnover, which increases the value of faster onboarding and payroll-linked worker access tools. The payroll software in retail and hospitality market is therefore moving faster in Asia-Pacific than in more mature regions, even though North America still leads in current revenue. Outside these core geographies, adoption remains more uneven, but growing tourism activity and formal employment expansion continue to support medium-term demand.

- ADP LLC

- Paychex Inc.

- Paycor Inc.

- Ceridian HCM Holding Inc.

- UKG Inc.

- Paycom Software Inc.

- Gusto Inc.

- Square Inc.

- Intuit Inc.

- Oracle Corporation

- SAP SE

- Workday Inc.

- BambooHR LLC

- Zenefits Inc.

- Rippling People Center Inc.

- Namely Inc.

- Deel Inc.

- Papaya Global Ltd.

- HiBob Inc.

- CloudPay Inc.

- Justworks Inc.

- Patriot Software Company LLC

- Paylocity Holding Corporation

- Automatic Payroll Systems Inc.

- Sage Group plc

- Xero Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based Payroll Solutions

- 4.2.2 Increasing Compliance Complexity in Retail and Hospitality

- 4.2.3 Rising Demand for Integrated HR and Payroll Suites among SMEs

- 4.2.4 Workforce Digitalization Accelerated by COVID-19 Recovery

- 4.2.5 Surge in Multi-Country Seasonal Staffing Patterns Driving Real-Time Global Payroll

- 4.2.6 Expansion of On-Demand Pay and Tip Management Features in Hospitality Chains

- 4.3 Market Restraints

- 4.3.1 High Cost Sensitivity and Narrow Margins in Small Hospitality Businesses

- 4.3.2 Data Security and Privacy Concerns Over SaaS Payroll

- 4.3.3 Fragmented POS and Time-Clock Ecosystems Hindering Seamless Payroll Integration

- 4.3.4 Slow Internet Penetration in Rural Tourist Destinations Limits Cloud Adoption

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 SMEs

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By Functionality

- 5.4.1 Core Payroll Processing

- 5.4.2 Time and Attendance Management

- 5.4.3 Payroll Analytics and Reporting

- 5.4.4 Tax and Compliance Management

- 5.4.5 Other Functionalities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADP LLC

- 6.4.2 Paychex Inc.

- 6.4.3 Paycor Inc.

- 6.4.4 Ceridian HCM Holding Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Paycom Software Inc.

- 6.4.7 Gusto Inc.

- 6.4.8 Square Inc.

- 6.4.9 Intuit Inc.

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 Workday Inc.

- 6.4.13 BambooHR LLC

- 6.4.14 Zenefits Inc.

- 6.4.15 Rippling People Center Inc.

- 6.4.16 Namely Inc.

- 6.4.17 Deel Inc.

- 6.4.18 Papaya Global Ltd.

- 6.4.19 HiBob Inc.

- 6.4.20 CloudPay Inc.

- 6.4.21 Justworks Inc.

- 6.4.22 Patriot Software Company LLC

- 6.4.23 Paylocity Holding Corporation

- 6.4.24 Automatic Payroll Systems Inc.

- 6.4.25 Sage Group plc

- 6.4.26 Xero Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment