|

시장보고서

상품코드

2073317

제조업 분야 학습 관리 시스템(LMS) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Learning Management System (LMS) In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

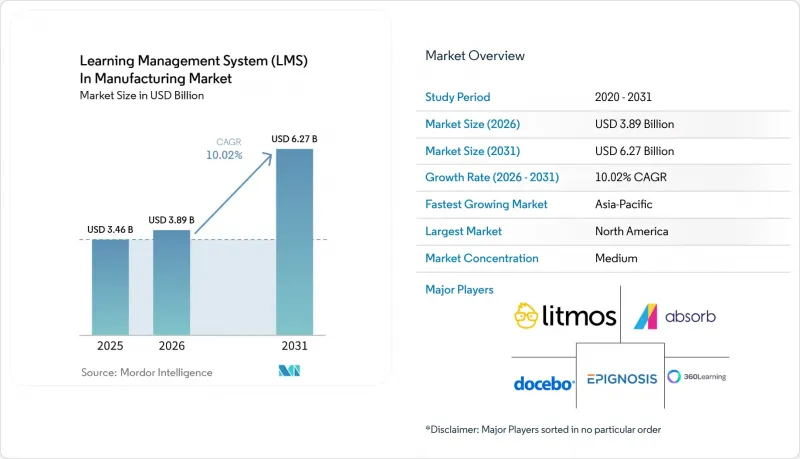

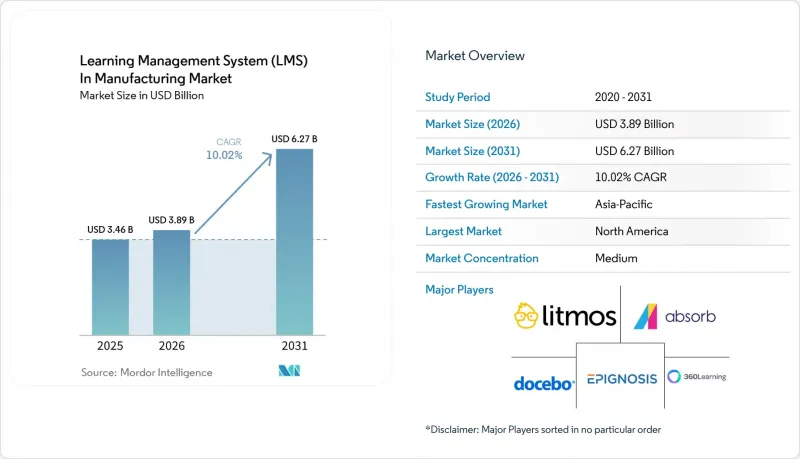

Mordor Intelligence에 의하면, 제조업 분야 학습 관리 시스템(LMS) 시장은 2025년에 34억 6,000만 달러로 평가되었습니다. 2026년에 38억 9,000만 달러로 평가되었고 2031년까지 62억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 10.02%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 모델(클라우드 기반, On-Premise형, 하이브리드형), 최종 사용자의 기업 규모(대기업 및 중소기업), 교육 기능(기술 역량 교육 등), 최종 사용자의 산업 분야(자동차 산업 등), 그리고 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 제조업 분야 학습 관리 시스템(LMS) 시장 동향 및 인사이트

스마트 팩토리에서의 인더스트리 4.0에 따른 재교육

제조업 분야 학습 관리 시스템(LMS) 시장은 디지털 도구의 등장으로 생산 현장에서 요구되는 기술이 변화하는 가운데, 공장 업무의 광범위한 재설계를 통해 점차 형성되고 있습니다. 세계경제포럼(WEF)은 2030년까지 기존 근로자의 기술 중 39%가 변화하거나 시대에 뒤처질 것으로 예측하고 있으며, 선진 제조업 고용주들은 AI, 빅데이터, 로봇공학, 신소재를 가장 시급히 해결해야 할 역량 격차로 꼽고 있습니다. 이러한 변화로 인해 학습 시스템은 단순히 과정을 제공하거나 연례 규정 준수 교육을 갱신하는 데 그치지 않고, 역할에 맞는 역량 구축을 지원해야 할 필요가 생겼습니다. 세계경제포럼과 맥킨지 앤드 컴퍼니의 조사에 따르면, 제조업에 종사하는 Z세대 직원 중 40% 이상이 경력 개발 및 역량 강화의 로드맵이 마련되어 있지 않을 경우 3-6개월 이내에 퇴사를 고려하고 있으며, 이직으로 인한 비용은 현장 직원 1인당 5만 2,000달러에 달할 전망입니다. 제조업 분야 학습 관리 시스템(LMS)(학습 관리 시스템)에서 이러한 점은 초기 도입 후에도 유용성을 유지할 수 있는 방식으로 기술을 기계 유형, 작업 셀, 직종군과 연계할 수 있게 함으로써 플랫폼의 가치를 높여주고 있습니다. 코스 라이브러리만 제공하는 공급업체는 장기적인 경쟁력이 약화될 우려가 있습니다. 왜냐하면 제조업체들은 체계화된 기술 아키텍처를 단순한 교육의 부가 기능이 아니라 공장의 핵심 인프라의 일부로 인식하는 경향이 강해지고 있기 때문입니다.

감사 대응을 위한 규정 준수 및 인증 자격 추적

제조업 분야 학습 관리 시스템(LMS)은 안전, 품질 및 운영 절차에 걸친 직원들의 준비 상태에 대한 문서화된 증거를 유지해야 할 필요성 덕분에 계속해서 이점을 누리고 있습니다. 제조업체들은 이중의 문서화 부담에 직면해 있습니다. 규제 요건에서는 명확한 교육 기록이 요구되는 반면, 보다 광범위한 경영 시스템에서는 관리된 프로세스, 인증 및 정기적인 갱신 주기에 대한 증명이 요구되기 때문입니다. 따라서 규제가 덜한 사무실 환경에 비해, 통합된 보고서 기능, 자동 알림, 그리고 버전 관리가 이루어지는 컨텐츠의 중요성이 훨씬 더 커지고 있습니다. 제조업 분야 학습 관리 시스템(LMS) 시장에서 구매 결정 요인은 플랫폼이 각 사업장 간에 신속하고 일관되게 감사에 대응할 수 있는 기록을 생성할 수 있는지 여부입니다. 이러한 추세에 따라, 제조업체가 스프레드시트나 연동되지 않은 개별 도구를 일일이 대조해야 하는 수고를 덜어주고, 인증 자격, 교육 이수 현황, 역할별 권한을 단일한 감사 가능한 워크플로로 통합할 수 있는 공급업체가 유리한 입지를 점하고 있습니다. 그 결과, 감사 대응이 가능한 보고서 기능이나 자격 정보의 추적 가능성을 갖춘 경우, 단순한 학습 제공 기능만 있는 경우보다 더 강력한 상업적 우위를 뒷받침하는 가격 환경이 형성되고 있습니다.

기존 ERP, MES 및 HRIS와의 통합의 복잡성

제조업 분야 학습 관리 시스템(LMS)은 새로운 학습 시스템이 깊이 통합된 기업 소프트웨어 스택과 연동해야 하는 경우, 여전히 큰 제약에 직면해 있습니다. 2026년에는 제조업계의 ERP 통합 프로젝트 비용이 당초 예산을 평균 72% 초과했으며, 이산형 제조업의 경우 최대 215%에 달하는 예산 초과가 나타났습니다. 이 문제는 학습 시스템 도입에도 영향을 미치고 있습니다. 이는 사용자 프로비저닝, 자격 기록, 직무 역할, 공장 계층 및 교육 트리거가 상호 연동을 염두에 두고 설계되지 않은 ERP, MES, HRIS 시스템에 걸쳐 관리되는 경우가 많기 때문입니다. 이러한 부담은 중견 제조기업에게 특히 무겁게 다가옵니다. 이러한 기업들은 이미 핵심 시스템에 투자한 상태이거나, 맞춤형 API 개발을 담당할 사내 팀이 부족하여 통합 주기가 장기화되는 경향이 있기 때문입니다. 제조업 분야 학습 관리 시스템(LMS) 시장에서 기성 커넥터는 더 이상 차별화를 위한 프리미엄 요소라기보다는 최소한 시장 진입 요건으로 기능하고 있습니다. 왜냐하면 구매자는 해당 플랫폼을 후보 목록에 올리기 전부터 이미 이러한 커넥터를 당연한 것으로 기대하고 있기 때문입니다. 따라서 커넥터 라이브러리가 빈약하거나 도입 수준이 제한적인 벤더는 판매 주기의 장기화, 프로젝트 리스크 증가, 그리고 본래 디지털 교육 시스템이 필요한 구매자층에서의 도입률 하락에 직면하게 될 것입니다.

부문별 분석

2025년 제조업 분야 학습 관리 시스템(LMS) 시장 규모 중 소프트웨어가 72.34%를 차지했으며, 이는 대형 제조업체나 규제 대상 공장에서 플랫폼 라이선스가 이미 도입의 기반으로 얼마나 확고하게 자리 잡았는지를 여실히 보여주고 있습니다. 제조업체는 우선 학습 과정, 인증 기록, 사용자 관리를 일원화하여 관리할 수 있는 시스템이 필요했기 때문에 소프트웨어 계층이 도입의 주된 초점이 되었습니다. 2019년부터 2025년에 걸쳐 더 많은 기관에서 강사 주도형이나 스프레드시트를 활용한 연수 관리 방식 대신 클라우드 플랫폼이 도입됨에 따라, 그 도입 기반이 확대되었습니다. 제조업 분야 학습 관리 시스템(LMS) 시장에서 소프트웨어는 공장이나 교대조를 넘나들며 수동 감독을 최소화하는 동시에 정기적인 규정 준수 프로그램을 실행해야 할 필요성 덕분에 혜택을 보았습니다. 이로 인해, 더 심층적인 서비스 수요가 표면화되기 전에는 구성 요소의 비중이 플랫폼 주도로 보이는 듯했습니다.

그러나 서비스 분야는 2031년까지 연평균 성장률(CAGR) 11.23%를 나타낼 것으로 예측되며, 이는 초기 도입 이후 구매자들의 기대가 변화하고 있음을 시사합니다. 도입이 기본적인 규정 준수 추적에서 스킬 인텔리전스, AI를 활용한 컨텐츠 제작, 공장 전반에 걸친 분석, 워크플로우 통합으로 전환됨에 따라 제조업체들은 도입, 설정 및 관리형 지원에 대한 필요성을 점점 더 느끼고 있습니다. LMS(학습 관리 시스템)의 경우, 제조업 분야에서는 범용적인 엔터프라이즈 LMS 기능만을 제공하는 공급업체나 파트너보다 제조 공정에 대한 지식을 갖춘 공급업체나 파트너를 선호합니다. 이는 또한 제조업 분야 학습 관리 시스템(LMS) 시장에서 단순한 소프트웨어 라이선스 접근 권한뿐만 아니라 성과, 거버넌스, 도입 지원에서 가치를 찾는 번들형 제공 모델로의 광범위한 전환을 반영하고 있습니다. 따라서 플랫폼의 깊이와 공장 차원의 실행력을 결합할 수 있는 공급업체는 교육 프로그램이 업무에 점점 더 통합됨에 따라 확대되는 서비스 수익 점유율을 확보하는 데 유리한 입장에 있습니다.

2025년 기준으로 제조업 분야 학습 관리 시스템(LMS) 시장 점유율의 68.47%를 클라우드 기반 솔루션이 차지했으며, 2031년까지의 예상 연평균 성장률(CAGR)도 12.37%로 가장 높은 성장률을 보이고 있습니다. 이 조합이 주목받는 이유는 가장 많이 도입된 모델이 틈새 시장의 대안 제품들에게 시장 점유율을 빼앗기지 않고 여전히 선두를 더욱 확고히 하고 있음을 보여주기 때문입니다. 제조업체들이 클라우드 시스템에 매력을 느끼는 이유는 분산된 공장 전체에 신속하게 시스템을 도입할 수 있고, 로컬 서버 관리에 따른 인프라 부담이 줄어들기 때문입니다. 제조업 분야 학습 관리 시스템(LMS) 시장에서 클라우드 도입은 정기적인 업데이트, 관리의 용이성, 초기 투자 비용 절감을 원하는 구매자들에게도 매력적입니다. 이러한 특징은 엔터프라이즈급 교육 관리가 필요하지만, 각 사업장에서 요구되는 복잡한 현장 인프라 구축을 정당화할 수 없는 중견 제조업체에게 특히 매력적입니다.

그렇긴 하지만, 교육 데이터, 검증 규칙 또는 업계 고유의 규제로 인해 퍼블릭 클라우드 환경의 이용이 제한되는 경우, On-Premise나 하이브리드 모델은 여전히 중요한 선택지로 남아 있습니다. 제약사는 계속해서 체계적인 변경 관리를 최우선으로 하고 있으며, 방위 관련 사업의 경우 교육 기록 및 관련 데이터의 취급에 대해 더 엄격한 규정이 적용될 수 있습니다. 따라서 하이브리드 도입은 기업이 기밀성이 높은 기록을 자체 관리하에 두면서도, 클라우드를 통해 제공되는 컨텐츠와 다양한 관리 도구를 활용할 수 있다는 점에서 실용적인 타협점으로 남아 있습니다. 제조업 분야 학습 관리 시스템(LMS)에서는 비용이나 속도와 마찬가지로 데이터 소재지에 관한 규제가 아키텍처 결정에 큰 영향을 미치는 유럽 및 아시아의 일부 지역에서 이러한 균형이 중요합니다. 따라서 제조업 분야 학습 관리 시스템(LMS) 시장은 규모의 경제를 추구하며 클라우드를 중심으로 통합이 진행되고 있지만, 유연성과 보다 엄격한 관리가 모두 필요한 규제가 까다로운 업계에서는 여전히 하이브리드 모델이 적용될 여지가 남아 있습니다.

지역별 분석

2025년, 북미는 제조업 분야 학습 관리 시스템(LMS) 시장에서 38.69%의 점유율을 차지했습니다. 이는 다층적인 규정 준수 요건과 감사에 대응할 수 있는 교육 인프라가 필요한 다중 거점 제조업체들이 밀집해 있기 때문입니다. 미국은 지역 수요에서 가장 큰 비중을 차지하고 있는데, 이는 문서화된 교육, 정기적인 인증, 공장 차원의 보고가 제조업의 규정 준수 및 직원 관리에서 여전히 핵심적인 역할을 하고 있기 때문입니다. 캐나다와 멕시코는 국경을 초월한 생산 네트워크를 통해 이러한 수요를 더욱 부추기고 있습니다. 이 분야에서 제조업체들은 미국 표준을 준수하는 동기화된 학습 워크플로우와 다국어 지원을 필요로 하고 있습니다. 따라서 제조업 분야 학습 관리 시스템(LMS) 시장은 북미에서 깊이 뿌리내리고 있습니다. 이는 연수 시스템이 단순히 학습 기회를 제공하는 데 그치지 않고, 증거 제시, 추적 가능성 및 업무의 일관성을 확보하기 위한 목적으로도 활용되고 있기 때문입니다. 이로 인해 이 지역에는 견고한 도입 기반이 구축되어 있으며, 현재 시장 점유율 측면에서 다른 지역이 이에 필적하기는 어렵습니다.

유럽은 제조업 분야 학습 관리 시스템(LMS) 시장에 있어 여전히 중요한 지역입니다. 이는 규정 준수에 대한 기대와 데이터 거버넌스에 대한 요구가 다른 많은 지역보다 플랫폼 선정에 더 직접적인 영향을 미치기 때문입니다. 수요는 독일, 영국, 프랑스에 집중되어 있으며, 이 지역의 구매 담당자들은 교육 관리와 데이터 아키텍처 및 데이터 저장 위치에 관한 요구 사항을 세심하게 고려하는 것 사이의 균형을 맞추어야 합니다. 2026년 2월, 독일 푸프론텐에 4,500 m² 규모의 훈련 센터가 문을 열었습니다. 이는 공식적인 LMS 도입 외에도, 해당 지역이 체계적인 인재 개발 인프라 구축을 위해 지속적으로 노력하고 있음을 보여주는 것입니다. 또한, 유럽에서의 도입 여부는 확장 가능한 컨텐츠 배포와 기록 및 사용자 데이터에 대한 지역별 관리 간의 균형을 맞추어야 할 필요성에 의해서도 좌우됩니다. 이러한 추세에 따라, 해당 지역의 선진적인 제조 클러스터 전반에서 하이브리드형 및 규정 준수를 고려한 클라우드 모델이 계속해서 중요하게 여겨지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 14.37%로 가장 빠르게 성장하고 있는 지역이며, 중국, 인도, 한국, 일본, 그리고 계속해서 확장되고 있는 동남아시아의 제조 거점이 이를 주도하고 있습니다. 중국에서 실시된 2025년 디지털 생산 관리 관련 조사에 따르면, 제조 기업의 65% 이상이 AI를 활용한 교육 추천 시스템의 시범 운영을 진행 중이며, 그 보급률은 85%를 넘어설 것으로 예측됩니다. 일본 경제산업성은 제조업체들의 디지털 전환 진행 상황에 여전히 편차가 있으며, 많은 기업이 전사적인 디지털 역량 강화보다는 개별 프로세스에서의 ‘개선"의 개선에 계속 주력하고 있다고 지적하고 있습니다. 인도의 제조업 확대와 동남아시아에서의 니어쇼어링 확산에 따라, 신속한 온보딩, 직무 인증, 다국어 학습 지원이 필요한 새로운 근로자층이 계속해서 등장하고 있습니다. 남미, 중동 및 아프리카는 현재 시장 점유율 면에서는 여전히 미미하지만, 산업의 다각화와 공식 자격 정보 추적이 점점 더 중요해짐에 따라 그 규모가 확대되고 있습니다. 2026년에는 남미 공장에서 발생한 예정 외 생산 중단 사례의 23%가 자격을 갖추지 못한 인력의 부적절한 배치에서 비롯된 것으로 보고되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the learning management system (LMS) market in manufacturing was valued at USD 3.46 billion in 2025 and USD 3.89 billion in 2026, and is forecast to reach USD 6.27 billion by 2031, expanding at a CAGR of 10.02% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), End-User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Training Function (Technical Skills Training, and More), End-User Industry (Automotive and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Management System (LMS) In Manufacturing Market Trends and Insights

Industry 4.0 Reskilling Across Smart Factories

The LMS in the manufacturing market is being shaped by a broader redesign of factory work as digital tools change the skills required on the production floor. The World Economic Forum projected that 39% of existing worker skill sets will be transformed or outdated by 2030, with advanced manufacturing employers ranking AI and big data, robotics, and new materials among their most urgent capability gaps. That shift means learning systems are now expected to support role-based capability building, not just course delivery or annual compliance refreshers. The World Economic Forum and McKinsey and Company also found that more than 40% of Gen Z employees in manufacturing consider leaving within 3-6 months when career development and skill-building pathways are missing, and the attrition cost reached USD 52,000 per departing frontline employee. In the LMS in the manufacturing market, this raises the value of platforms that can map skills to machine types, work cells, and job families in a way that stays useful after the first deployment. Vendors that provide only course libraries face weaker long-term positioning because manufacturers are increasingly treating structured skills architecture as part of core plant infrastructure rather than a simple training add-on.

Audit-Ready Compliance And Certification Tracking

The LMS in the manufacturing market continues to benefit from the need to maintain documented evidence of workforce readiness across safety, quality, and operating procedures. Manufacturers face a dual documentation burden because regulatory requirements call for explicit training records, while broader management systems require proof of controlled processes, certifications, and recurring refresh cycles. This makes centralized reporting, automated reminders, and version-controlled content much more important than in less regulated office environments. In the LMS manufacturing market, purchasing decisions are often driven by whether the platform can produce inspection-ready records quickly and consistently across sites. That preference strengthens vendors that can tie certifications, training completions, and role permissions into a single auditable workflow, rather than leaving manufacturers to reconcile spreadsheets and disconnected point tools. The result is a pricing environment in which audit-ready reporting and credential traceability support stronger commercial positioning than basic learning-delivery features alone.

Legacy ERP, MES, And HRIS Integration Complexity

The LMS in the manufacturing market still faces a major restraint when new learning systems have to connect with deeply embedded enterprise software stacks. In 2026, manufacturing ERP integration projects exceeded initial budgets by an average of 72%, while discrete manufacturers saw overruns as high as 215%. That problem carries over into learning deployments because user provisioning, credential records, job roles, plant hierarchies, and training triggers often sit across ERP, MES, and HRIS systems that were not designed to work together. The burden is especially heavy for mid-market manufacturers that have already invested in core systems but lack internal teams for custom API work and long integration cycles. In the LMS manufacturing market, pre-built connectors now function more as minimum entry requirements than as premium differentiators, because buyers expect them before a platform is even shortlisted. Vendors with weak connector libraries or limited implementation depth, therefore, face slower sales cycles, higher project risk, and lower adoption among buyers that otherwise need digital training systems.

Other drivers and restraints analyzed in the detailed report include:

- Multi-Site Training Standardization Across Plants And Shifts

- Mobile And Offline Learning For Deskless Workers

- Production-Time Trade-Offs That Limit Learning Hours

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.34% of the LMS market size in manufacturing in 2025, underscoring how strongly platform licenses already anchor adoption across large manufacturers and regulated plants. The software layer became the center of most deployments because manufacturers first needed systems that could manage learning paths, certification records, and user administration in one place. That installed base grew across 2019-2025 as cloud platforms replaced instructor-led and spreadsheet-led training administration in more facilities. In the LMS in the manufacturing market, software also benefited from the need to run recurring compliance programs with less manual oversight across plants and shifts. This made the component mix look heavily platform-led before deeper service demand emerged.

Services, however, are projected to grow at a 11.23% CAGR through 2031, suggesting a shift in what buyers now expect after the first rollout. As deployments move from basic compliance tracking into skills intelligence, AI-assisted content creation, cross-plant analytics, and workflow integration, manufacturers increasingly need implementation, configuration, and managed support. In the LMS, the manufacturing industry favors providers and partners with manufacturing process knowledge over generic enterprise LMS capacity alone. It also reflects a broader shift in the LMS market for manufacturing toward bundled delivery models where the value lies in outcomes, governance, and adoption support, not just in access to software seats. Vendors that can combine platform depth with plant-level execution are therefore better positioned to capture a growing share of services revenue as training programs become more embedded in operations.

Cloud-based deployment held 68.47% of the LMS market share in manufacturing in 2025 and also posted the fastest projected CAGR at 12.37% through 2031. That combination is notable because it shows the largest deployment model is still extending its lead rather than losing ground to niche alternatives. Manufacturers have been drawn to cloud systems because they enable faster rollouts across distributed plants and reduce the infrastructure burden of local server management. In the LMS market for manufacturing, cloud adoption also appeals to buyers who want regular updates, easier administration, and lower upfront investment. These features are especially attractive to mid-sized manufacturers that need enterprise-grade training control but cannot justify the complex on-site infrastructure required at each location.

Even so, on-premises and hybrid models remain relevant where training data, validation rules, or sector-specific controls limit the use of public cloud environments. Pharmaceutical manufacturers continue to prioritize controlled change management, while defense-related operations may face stricter rules for handling training records and supporting data. Hybrid deployment, therefore, remains a practical middle ground because it lets companies keep sensitive records under local control while still using cloud-delivered content and broader administrative tools. In the LMS in the manufacturing industry, that balance matters in Europe and parts of Asia where data residency rules shape architecture decisions as much as cost and speed do. The LMS market in manufacturing is therefore consolidating around cloud for scale, but it still leaves room for hybrid models in regulated verticals that need both flexibility and tighter control.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By Training Function

- Technical Skills Training

- Safety and Compliance Training

- Equipment and Machinery Training

- Quality and Lean Manufacturing Training

- Operational Process Training

- Employee Onboarding

- Other Training Functions

- By End-user Industry

- Automotive

- Electronics and Semiconductors

- Industrial Machinery and Equipment

- Pharmaceuticals and Chemicals

- Food and Beverage

- Aerospace and Defense

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- New Zealand

- Indonesia

- Thailand

- Vietnam

- Malaysia

- Singapore

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held a 38.69% share of the LMS market in manufacturing in 2025, driven by layered compliance requirements and a dense base of multi-site manufacturers that need audit-ready training infrastructure. The United States accounts for the largest share of regional demand because documented learning, recurring certifications, and plant-level reporting remain central to manufacturing compliance and workforce governance. Canada and Mexico add to that demand through cross-border production networks, where manufacturers need synchronized learning workflows and multilingual delivery that can align with U.S.-based standards. The LMS market in manufacturing is therefore deeply established in North America because training systems are used not only for learning delivery but also for proof, traceability, and operational consistency. This gives the region a strong installed base that is difficult for other geographies to match in current share.

Europe remains an important region for the LMS in the manufacturing market because compliance expectations and data governance needs shape platform selection more directly than in many other regions. Demand is concentrated in Germany, the United Kingdom, and France, where buyers must balance training control with close attention to data architecture and residency requirements. A 4,500 m2 training center opened in Pfronten, Germany, in February 2026, which underlines the region's continued commitment to structured workforce development infrastructure even outside formal LMS deployments. European deployment choices are also shaped by the need to balance scalable content delivery with region-specific control over records and user data. That dynamic keeps hybrid and compliance-aware cloud models relevant across advanced manufacturing clusters in the region.

Asia-Pacific is the fastest-growing geography at a 14.37% CAGR through 2031, led by China, India, South Korea, Japan, and the expanding Southeast Asian manufacturing base. In China, a 2025 study on digital production management reported that more than 65% of manufacturing enterprises were piloting AI-powered training recommendation systems, with penetration expected to exceed 85%. Japan's Ministry of Economy, Trade and Industry noted that manufacturers were still advancing digital transformation unevenly, with many firms remaining focused on Kaizen improvements in individual processes rather than enterprise-wide digital upskilling. India's manufacturing expansion and Southeast Asia's nearshoring gains continue to create new cohorts of workers who need rapid onboarding, role certification, and multilingual learning support. South America, the Middle East, and Africa remain smaller in terms of current share, but they are expanding as industrial diversification and formal credential tracking become more important. In 2026, it was reported that 23% of unplanned production stoppages in South American plants originated from the incorrect assignment of unqualified personnel.

- Docebo S.p.A.

- Absorb Software Inc.

- Litmos US, L.P.

- Epignosis LLC

- iSpring Solutions, Inc.

- Intellum, Inc.

- Alchemy Systems, L.P.

- Vector Solutions LLC

- 360Learning S.A.S.

- Zensai ApS

- Dozuki, Inc.

- Valamis Group Oy

- PlatCore, LLC

- Continu, Inc.

- eLeaP Software LLC

- Nvolve Group Limited

- Schoox, Inc.

- SkyPrep Inc.

- Gyrus Systems LLC

- Moodle Pty Ltd.

- Latitude CG, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Industry 4.0 Reskilling Across Smart Factories

- 4.3.2 Audit-Ready Compliance and Certification Tracking

- 4.3.3 Multi-Site Training Standardization Across Plants and Shifts

- 4.3.4 Mobile and Offline Learning for Deskless Workers

- 4.3.5 AI Conversion of SOPs Into Microlearning

- 4.3.6 Contractor and Temporary Labor Credentialing at Plant Gates

- 4.4 Market Restraints

- 4.4.1 Legacy ERP, MES, and HRIS Integration Complexity

- 4.4.2 Production-Time Trade-Offs That Limit Learning Hours

- 4.4.3 Multilingual Content Governance Across Plants

- 4.4.4 Data Residency and IP Leakage Concerns

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Training Function

- 5.4.1 Technical Skills Training

- 5.4.2 Safety and Compliance Training

- 5.4.3 Equipment and Machinery Training

- 5.4.4 Quality and Lean Manufacturing Training

- 5.4.5 Operational Process Training

- 5.4.6 Employee Onboarding

- 5.4.7 Other Training Functions

- 5.5 By End-user Industry

- 5.5.1 Automotive

- 5.5.2 Electronics and Semiconductors

- 5.5.3 Industrial Machinery and Equipment

- 5.5.4 Pharmaceuticals and Chemicals

- 5.5.5 Food and Beverage

- 5.5.6 Aerospace and Defense

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Indonesia

- 5.6.4.8 Thailand

- 5.6.4.9 Vietnam

- 5.6.4.10 Malaysia

- 5.6.4.11 Singapore

- 5.6.4.12 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Docebo S.p.A.

- 6.4.2 Absorb Software Inc.

- 6.4.3 Litmos US, L.P.

- 6.4.4 Epignosis LLC

- 6.4.5 iSpring Solutions, Inc.

- 6.4.6 Intellum, Inc.

- 6.4.7 Alchemy Systems, L.P.

- 6.4.8 Vector Solutions LLC

- 6.4.9 360Learning S.A.S.

- 6.4.10 Zensai ApS

- 6.4.11 Dozuki, Inc.

- 6.4.12 Valamis Group Oy

- 6.4.13 PlatCore, LLC

- 6.4.14 Continu, Inc.

- 6.4.15 eLeaP Software LLC

- 6.4.16 Nvolve Group Limited

- 6.4.17 Schoox, Inc.

- 6.4.18 SkyPrep Inc.

- 6.4.19 Gyrus Systems LLC

- 6.4.20 Moodle Pty Ltd.

- 6.4.21 Latitude CG, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment