|

시장보고서

상품코드

2073320

의료 분야 학습 관리 시스템(LMS) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Learning Management System (LMS) In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

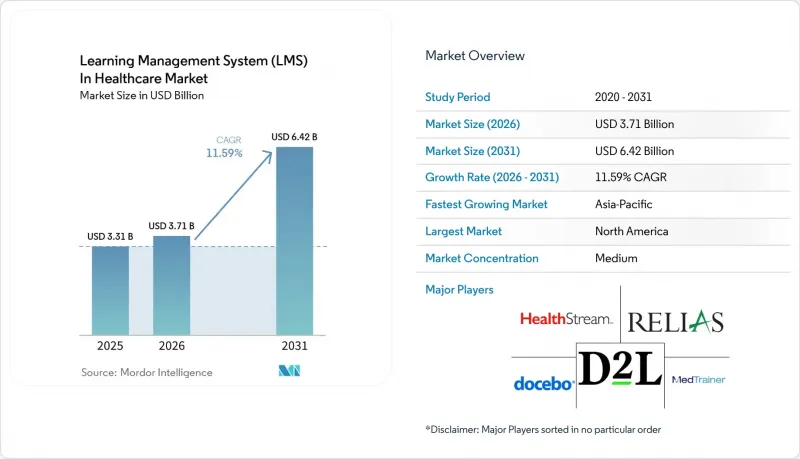

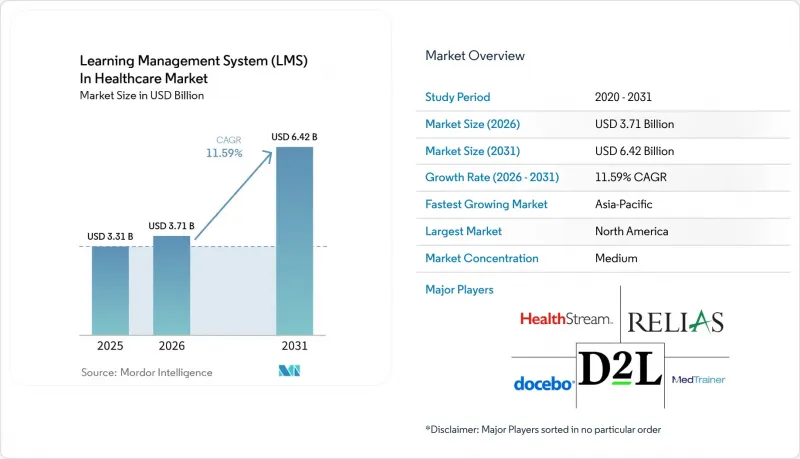

Mordor Intelligence에 의하면, 의료 분야 학습 관리 시스템(LMS) 시장은 2025년에 33억 1,000만 달러로 평가되었습니다. 2031년까지 64억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.59%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드 기반 등), 제공 형태(자기 주도형 및 원격 학습 등), 용도(규정 준수 교육, 임상·간호 교육 등), 최종 사용자(병원 및 의료 시스템 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 분야 학습 관리 시스템(LMS) 시장 동향 및 인사이트

규제 준수 및 인증 현황 추적

의료 분야 학습 관리 시스템(LMS) 시장은 의료 시스템이 운영 위험을 증가시키지 않으면서도 미룰 수 없는 인증 관련 연수 의무로 인해 계속해서 안정적인 수요를 확보하고 있습니다. 문서화된 역할별 역량 검증은 일상적인 인재 관리에 정착되어 있으며, LMS는 단순한 편의성 도구에서 시험, 자격 갱신, 내부 감사 대응과 직결되는 컴플라이언스 시스템으로 변모하고 있습니다. 이는 대규모 의료 제공업체 네트워크에서 특히 중요한데, 이러한 네트워크에서는 정책 승인, 역량 인증 서명, 재교육 기록을 단일 증거 추적 체계 내에서 기관, 부서, 직종을 넘나들며 검색할 수 있도록 해야 합니다. 그 결과, 강력한 전환 비용 효과가 발생합니다. 보고 아키텍처, 감사 로그, 인증 증거가 단일 플랫폼에 통합되면 조달 팀은 공급업체 변경에 대해 더욱 신중해집니다. 또한, 의료 분야 학습 관리 시스템은 전문 분야에 관계없이 평생 교육 요건이 확대됨에 따라 그 혜택을 누리고 있습니다. 왜냐하면, 인원 수가 늘어나지 않더라도 기록이 필수인 연수 행사 건수가 늘어날 가능성이 있기 때문입니다.

인력 부족과 지속적인 임상 기술 향상

의료 분야 학습 관리 시스템은 인력 부족으로 인해 의료 제공업체들이 보다 신속하고 확장성이 뛰어난 연수 모델에 의존할 수밖에 없게 된 점도 이를 뒷받침하고 있습니다. 미국병원협회(AHA)는 2030년까지 6만 4,000명의 간호사가 부족할 것으로 전망하고 있으며, 향후 10년 동안 미국의 신규 일자리의 24%가 의료 분야에서 창출될 것으로 예상하고 있습니다. 이는 새로 창출되는 직무 하나하나가 신입 사원 교육 및 지속 교육에 대한 수요를 높인다는 것을 의미합니다. 미국 의료 그룹 협회(AMGA)의 보고서에 따르면, 2022년부터 2024년에 걸쳐 1차 진료 및 전문 의료 분야의 진료소에서 근무하는 총 직원수는 5%에서 7% 감소했습니다. 한편, 2024년 환자 내원 건수는 2.3% 증가했으며, 바쁜 임상 현장에서 대면 수업만으로 연수를 진행하는 것이 점점 더 어려워지고 있습니다. 이와 유사한 압박은 이직률이 높아 신규 채용에 따른 연수 주기가 길어지고 있는 현장 지원직이나 약국 업무에서도 두드러지게 나타납니다. 약국 기술자 인증 위원회(Pharmacy Technician Certification Board)의 조사에 따르면, 응답자 1만 7,112명을 대상으로 한 조사에서 2025년에는 고용주 주도의 연수 프로그램이 6.3% 증가한 것으로 나타났습니다. 케어 팀의 다양화가 진행되고 역할의 범위가 더욱 전문화됨에 따라, 의료 분야 학습 관리 시스템은 추가적인 대면 관리 인력에 의존하지 않고도 관할 구역, 자격, 케어 경로를 아우르며 교육을 표준화해야 한다는 요구에 힘입어 혜택을 보고 있습니다.

데이터 개인정보 보호 및 사이버 보안 요건

의료 분야 학습 관리 시스템은 직원 연수 기록, 규정 준수 증빙 자료, 사용자 식별 정보를 저장하는 시스템에서 비롯된 보안상의 부담으로 인해 큰 제약을 받고 있습니다. 『Applied Sciences』지에 게재된 2026년 조사에 따르면, 미국 의료 분야의 정보 유출은 2024년에 정점을 찍어 2억 7,600만 건의 기록이 유출되었습니다. 또한, 2025년에는 해당 분야의 사고를 파악하고 차단하는 데 평균 279일이 소요된 것으로 밝혀졌습니다. 이러한 환경에서는 계약 체결에 앞서 구매자가 암호화, 접근 제어, 감사 추적, 테스트 절차 및 공급업체의 문서를 더욱 엄격하게 검토하고 있습니다. 이러한 통제 조치를 검증하는 데 드는 비용은 소규모 병원이나 연방 공인 의료 센터(FQHC)의 도입 비용을 크게 증가시킬 가능성이 있으며, 그 결과 중견 시장은 최상위 의료 시스템보다 가격에 더 민감해지고 있습니다. 따라서 의료 분야 학습 관리 시스템 시장은 공급업체가 보안 규정 준수를 통합적으로 패키지화하여 사내 사이버 보안 자원이 제한적인 고객의 현장 모니터링 부담을 덜어줄 수 있을 때 더욱 빠르게 성장할 것입니다.

부문별 분석

솔루션은 2025년 구성 비율에서 70.12%를 차지하며, 의료 분야 학습 관리 시스템 시장에서 가장 큰 수익원이 되었습니다. 구매자들은 책임 소재가 여러 도구에 분산되는 것이 아니라, 컨텐츠 라이브러리, 워크플로우 자동화, 보고서 기능, 사용자 관리를 단일 인터페이스에 통합한 통합 플랫폼을 선호했습니다. 이러한 구성 덕분에 교육 이수 현황, 정책 승인, 역량 인증 여부를 단일 증거 기록을 통해 확인할 수 있으므로, 감사 시 발생하는 마찰이 줄어듭니다. 또한, 병원, 진료소, 급성기 후 의료시설 전반에 걸쳐 동일한 연수 체계를 필요로 하는 의료 시스템에 있어 중요한, 기업 전체의 표준화도 지원합니다.

서비스 부문은 가장 빠르게 성장하고 있는 분야로, 2031년까지의 연평균 성장률(CAGR)은 12.23%로 전망됩니다. 이는 의료 분야 학습 관리 시스템에서 구매자의 행동에 뚜렷한 변화가 나타나고 있음을 반영합니다. 많은 고객사는 기본적인 플랫폼 도입 단계를 지나, 현재는 도입 지원, 규제 업데이트, 컨텐츠 유지 관리 및 여러 거점 관리에 대해 외부 지원을 요청하고 있습니다. MedTrainer사는 2025년 중 의료 업계용 신규 과정을 250개 이상 출시하고, 소프트웨어 기능 개선을 130건 이상 실시했으며, 엔지니어링 팀을 25% 확대했다고 발표했습니다. 이는 각 벤더들이 소프트웨어 기반 위에 지속적인 서비스 계층을 구축하고 있음을 보여줍니다. 스킬 갭 분석, AI를 활용한 재교육, 분산형 자격 인증 등 활용 사례가 확대됨에 따라, 이 서비스는 의료 제공업체가 대규모 사내 LMS 팀을 고용하지 않고도 학습 환경을 최신 상태로 유지할 수 있는 실용적인 수단이 되고 있습니다.

2025년에는 클라우드 기반 솔루션이 65.23%의 점유율을 차지하며, 의료 분야 학습 관리 시스템 시장에서 여전히 주요 구성 요소로 자리 잡았습니다. 그 주된 이유는 운영 측면에 있습니다. 클라우드 인프라를 활용하면 각 시설에서 로컬 시스템 관리를 할 필요 없이, 모든 거점에서 역할 기반 할당, 컨텐츠 업데이트, 보고서 변경을 일원화하여 수행할 수 있기 때문입니다. 또한, 기존 규정 준수 체계에 부합해야 하는 신규 거점이나 새로 인수된 공급업체 그룹의 신속한 통합도 지원합니다. 대규모 인력을 보유한 기업에서 IT 팀이 소규모 구매자인 경우, 이러한 장점 덕분에 클라우드는 대규모 교육의 연속성을 유지하기 위한 가장 효율적인 모델이 됩니다.

클라우드는 또한 2031년까지 연평균 성장률(CAGR)이 12.46%로 가장 빠르게 성장하고 있는 도입 형태이지만, 규제가 더 엄격한 환경에서는 하이브리드형에 대한 수요도 여전히 중요한 위치를 차지하고 있습니다. 유럽의 “건강 데이터 공간(European Health Data Space)"규제로 인해 디지털 상호운용성을 지원함과 동시에, 관할 구역에 따른 거버넌스 제어 기능을 갖춘 플랫폼의 필요성이 더욱 커졌습니다. 하이브리드 방식은 특정 기록에 대해서는 On-Premise 관리를 유지하면서, 컨텐츠 배포 및 분석에는 클라우드의 확장성을 활용하고자 하는 대규모 대학 부속 병원이나 통합 의료 네트워크에게 여전히 중요한 선택지로 남아 있습니다. 보안 수준이 높은 환경이나 리소스가 제한된 환경에서는 여전히 On-Premise 시스템이 사용되고 있지만, 의료 분야 학습 관리 시스템 시장은 규정 준수 요건을 충족하면서도 유지보수 부담을 줄일 수 있는 호스팅형 아키텍처로 분명히 전환되고 있습니다.

지역별 분석

2025년, 북미는 의료 분야 학습 관리 시스템 시장 점유율의 36.58%를 차지하며 최대 지역 시장이 되었습니다. 미국은 여전히 주요 국내 시장으로서의 지위를 유지하고 있습니다. 이는 CMS(미국 의료보험서비스센터)의 참여 규정, 인증 기준 및 개인정보 보호 의무에 따라 문서화된 교육이 단순한 선택적 소프트웨어 업그레이드가 아니라 업무상 필수 요건이 되었기 때문입니다. 이러한 환경은 온보딩, 역량 검증, 정책 승인 및 기업 차원의 지속적인 규정 준수 관리가 가능한 플랫폼에 대한 안정적인 수요를 뒷받침하고 있습니다. 캐나다에서도 기관 차원의 적극적인 도입이 이루어지고 있으며, 토론토 대학교 테마티 의과대학은 2025년에 “Competence by Design"프레임워크에 따라 의학박사(MD) 과정 및 대학원 교육을 지원하기 위해 클라우드 기반 학습자 관리 플랫폼을 도입했습니다. 멕시코는 해당 지역에서 여전히 시장 규모가 작지만, 보험 가입자와 품질에 대한 기대가 높아짐에 따라 민간 병원 그룹들은 인재 개발 및 역량 입증을 점차 제도화하고 있습니다.

유럽은 밀집된 병원 네트워크와 확대되는 디지털 헬스 거버넌스가 결합되어 있어, 의료 분야 학습 관리 시스템에서 여전히 중요한 위치를 차지하고 있습니다. 2025년에 채택된 “유럽 건강 데이터 공간(European Health Data Space)" 규제는 국경을 초월한 건강 데이터 관리를 위한 보다 견고한 체계를 구축하며, 이에 따라 디지털 기록, 시스템 접근 및 규정 준수 절차를 담당하는 직원에 대한 교육 수요가 증가하고 있습니다. 영국, 독일, 프랑스는 여전히 주요 수요 거점이며, 한편 스페인, 이탈리아, 동유럽에서는 기록의 디지털화와 인재 거버넌스가 더욱 체계화됨에 따라 소규모 기반에서 성장이 진행되고 있습니다. 이로 인해 유럽은 공급업체가 지역별 데이터에 대한 인사이트와 다양한 의료 시스템 모델에 맞추어 교육 체계를 조정할 수 있는 능력을 모두 필요로 하는 시장으로서의 위상을 유지하고 있습니다.

아시아태평양은 의료 분야 학습 관리 시스템 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 13.41%를 나타낼 것으로 전망됩니다. 이러한 성장을 주도하고 있는 요인은 중국과 인도에서 정부 주도의 의료 시스템이 확대되고 있는 점, 동남아시아 전역에서 민간 병원 네트워크가 확장되고 있는 점, 그리고 의료 종사자의 품질 보증을 위해서는 디지털 교육 인프라가 필요하다는 인식이 확산되고 있는 점입니다. 세계보건기구(WHO)는 2025년 기준, 회원국 중 성숙도 수준 3 또는 4에 해당하는 제대로 기능하는 규제 시스템을 갖춘 국가가 고작 30%에 불과하다고 밝히며, 규제 담당자의 역량 강화를 지원하기 위한 학습 카탈로그를 출시했습니다. 이는 일부 개발도상국의 의료 시스템 전반에 걸쳐 체계적인 연수 역량에 대한 광범위한 수요를 반영한 것입니다. 2026년 『Frontiers in Medicine』지에 게재된 연구에서도 중국 의대생들 사이에서 AI를 활용한 임상 학습에 대한 높은 참여도가 나타났습니다. 45.6%가 15분에서 30분 길이의 세션에 참여했으며, 63.4%는 모바일 앱을 통한 제공을 선호하고 있으며, 이 지역 전체에서 “모바일 우선"의 설계가 기대되고 있음을 알 수 있습니다. 호주와 싱가포르는 규모는 작지만 여전히 선진적인 디지털 헬스 시장을 유지하고 있는 반면, 남미, 중동 및 아프리카에서는 브라질, 사우디아라비아, 아랍에미리트(UAE)를 필두로 여전히 초기 단계의 비즈니스 기회가 존재하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the learning management system (LMS) in the Healthcare Market in healthcare reached USD 3.31 billion in 2025 and is forecast to reach USD 6.42 billion by 2031, growing at a CAGR of 11.59% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, and More), Delivery Mode (Self-Paced and Distance Learning, and More), Application (Compliance Training, Clinical and Care Training, and More), End User (Hospitals and Health Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Management System (LMS) In Healthcare Market Trends and Insights

Regulatory Compliance and Accreditation Tracking

The learning management system market in healthcare continues to draw steady demand from accreditation-linked training mandates that health systems cannot defer without increasing operating risk. Documented, role-specific competency validation has become embedded in routine workforce management, turning the LMS from a convenience tool into a compliance system tied to inspections, renewals, and internal audit readiness. This matters even more in large provider networks, where policy acknowledgment, competency sign-off, and retraining records need to be searchable across facilities, units, and job categories within a single evidentiary trail. The result is a strong switching-cost effect: once reporting architecture, audit logs, and accreditation evidence are aligned on a single platform, procurement teams become more cautious about vendor changes. The learning management system in the healthcare market also benefits as continuing education requirements expand across specialties, since the number of training events that must be recorded can rise even without a corresponding increase in headcount.

Workforce Shortages and Continuous Clinical Upskilling

The learning management system in the healthcare market is also being supported by staffing shortages that are forcing providers to rely on faster, more scalable training models. The American Hospital Association projected a shortfall of 64,000 nurses by 2030 and said health care is expected to account for 24% of all new U.S. jobs this decade, meaning every new role created will increase demand for onboarding and continuing education. The American Medical Group Association reported that total clinic staffing in primary care and medical specialties declined by 5% to 7% between 2022 and 2024, even as patient visits rose 2.3% in 2024, making classroom-only delivery harder to sustain in busy clinical settings. The same pressure is visible in frontline support roles, where high turnover expands the annual cycle of onboarding-linked training, and in pharmacy operations, where the Pharmacy Technician Certification Board found employer-based training programs rose 6.3% in 2025 across its survey base of 17,112 respondents. As care teams diversify and role scopes become more specialized, the learning management system in the healthcare market benefits from the need to standardize training across jurisdictions, credentials, and care pathways without relying on additional in-person administrative staff.

Data Privacy and Cybersecurity Requirements

The learning management system in the healthcare market faces a significant brake due to the security burden imposed by systems that store staff training records, compliance evidence, and user-level identifiers. A 2026 survey published in Applied Sciences noted that U.S. health care breaches peaked in 2024 with 276 million records exposed, and that incidents in the sector averaged 279 days to identify and contain in 2025. This environment heightens buyer scrutiny of encryption, access controls, audit trails, testing procedures, and vendor documentation before contracts move forward. The cost of validating these controls can materially increase deployment expenses for smaller hospitals and federally qualified health centers, making the mid-market more price-sensitive than top-tier health systems. The learning management system market in healthcare, therefore, grows faster when vendors can centrally package security compliance and reduce the burden of local oversight for customers with limited internal cyber resources.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Personalized Learning and Skills Analytics

- Cloud-Based and Hybrid Training Delivery Adoption

- Integration Complexity With EHR, HRIS, And Credentialing Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 70.12% of the 2025 component split, making them the largest revenue stream in the healthcare learning management system market. Buyers favored integrated platforms because they combine content libraries, workflow automation, reporting, and user management in a single interface, rather than spreading accountability across multiple tools. That setup reduces audit friction because training completion, policy acknowledgment, and competency sign-off can be reviewed through a single evidence trail. It also supports enterprise standardization, which is important for health systems that need the same training logic across hospitals, clinics, and post-acute settings.

Services are the faster-growing component, with a 12.23% CAGR projected through 2031, reflecting a clear shift in buyer behavior within the learning management system in the healthcare industry. Many customers have moved past basic platform deployment and now want outside help with implementation, regulatory updates, content maintenance, and multi-site administration. MedTrainer said it released more than 250 new healthcare-specific courses and more than 130 software enhancements during 2025, while also expanding its engineering team by 25%, demonstrating how vendors are building recurring service layers on top of the software base. As use cases broaden into skills gap analysis, AI retraining, and distributed credentialing, services become a practical way for providers to keep the learning environment current without hiring large internal LMS teams.

Cloud-based deployment held a 65.23% share in 2025 and remains the leading configuration in the healthcare learning management system market. The main reason is operational, because cloud infrastructure lets role-based assignments, content updates, and reporting changes move across all sites without local system administration at each facility. It also supports faster onboarding for new locations and newly acquired provider groups that need to fit into an existing compliance framework. For buyers with large workforces and lean IT teams, these benefits make cloud the most efficient model for maintaining training continuity at scale.

Cloud is also the fastest-growing deployment mode, with a 12.46% CAGR through 2031, while hybrid demand remains relevant in more tightly regulated environments. The European Health Data Space regulation strengthened the case for platforms that can support digital interoperability together with jurisdiction-aware governance controls. Hybrid deployment remains a key option for large academic medical centers and integrated delivery networks that want on-premises control for selected records while still leveraging cloud elasticity for content delivery and analytics. On-premises systems continue to be used in high-security or resource-constrained environments, but the learning management system market in healthcare is clearly moving toward hosted architectures that offer compliance parity with lower maintenance overhead.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Delivery Mode

- Self-Paced and Distance Learning

- Instructor-Led Training

- Blended Learning

- By Application

- Compliance Training

- Clinical and Care Training

- CME and Certification Training

- Product and Commercial Training

- Patient Safety Training

- EHR/Clinical Systems Training

- Infection Control Training

- Cybersecurity and Data Privacy Training

- Telehealth Training

- Workforce Credentialing and Competency Management

- By End User

- Hospitals and Health Systems

- Clinics and Ambulatory Care Providers

- Pharmaceutical Companies

- Medical Device Companies

- Academic Medical Institutions

- Long-Term Care Facilities

- Home Healthcare Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.58% of the healthcare learning management system market share in 2025, making it the largest regional market. The United States remained the dominant national market because CMS participation rules, accreditation standards, and privacy obligations make documented training an operational requirement rather than an optional software upgrade. This environment supports a stable demand for platforms that can manage onboarding, competency validation, policy acknowledgment, and recurring compliance at enterprise scale. Canada also showed active institutional adoption, and the University of Toronto Temerty Faculty of Medicine selected a cloud-based learner management platform in 2025 to support MD and postgraduate education aligned with the Competence by Design framework. Mexico remains a smaller opportunity in the region, but private hospital groups are gradually formalizing workforce development and competency documentation as payer and quality expectations rise.

Europe remains an important part of the learning management system in the healthcare market because it combines dense hospital networks with expanding digital health governance. The European Health Data Space regulation, adopted in 2025, created a stronger framework for cross-border health data management, which adds training needs for staff who handle digital records, system access, and compliance processes. The United Kingdom, Germany, and France remain the main national demand centers, while Spain, Italy, and Eastern Europe are moving forward from a smaller base as record digitization and workforce governance become more structured. This keeps Europe positioned as a market where vendors need both regional data awareness and the ability to adapt training structures to varied health system models.

Asia-Pacific is the fastest-growing region in the learning management system market for healthcare, with a 13.41% CAGR projected through 2031. Growth is being driven by state-led health system expansion in China and India, by scaling private hospital networks across Southeast Asia, and by a broader recognition that workforce quality assurance requires digital training infrastructure. The World Health Organization said in 2025 that only 30% of member states have well-functioning regulatory systems at Maturity Levels 3 or 4, and it launched a learning catalog to help upskill regulatory workforces, reflecting a wider need for structured training capacity across several developing health systems. A 2026 study in Frontiers in Medicine also showed strong engagement with AI-enabled clinical learning among Chinese medical students, with 45.6% participating in sessions of 15 to 30 minutes and 63.4% preferring mobile app delivery, pointing to mobile-first design expectations across the region. Australia and Singapore remain smaller but advanced digital health markets, while South America, the Middle East, and Africa continue to present earlier-stage opportunities led by Brazil, Saudi Arabia, and the UAE.

- HealthStream, Inc.

- Relias LLC

- MedTrainer, Inc.

- Docebo S.p.A.

- D2L Corporation

- Absorb Software Inc.

- Cornerstone OnDemand, Inc.

- Epignosis LLC

- LearnUpon Limited

- iSpring Solutions, Inc.

- SkyPrep Inc.

- Kallidus Limited

- TOVUTI, Inc.

- Medbridge Inc.

- ACTO Technologies Inc.

- Knowledge Factor, Inc. dba Amplifire

- CareAcademy.co, Inc.

- The World Continuing Education Alliance Ltd

- Biomedical Research Alliance of New York LLC

- Thought Industries, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Compliance and Accreditation Tracking

- 4.2.2 Workforce Shortages and Continuous Clinical Upskilling

- 4.2.3 Cloud-Based and Hybrid Training Delivery Adoption

- 4.2.4 AI-Enabled Personalized Learning and Skills Analytics

- 4.2.5 Retraining Demand From Ambient AI and Digital Workflow Adoption

- 4.2.6 Cross-Site Auditability Needs After Cyber and Patient-Safety Incidents

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Requirements

- 4.3.2 Integration Complexity With EHR, HRIS, and Credentialing Systems

- 4.3.3 Content Governance Bottlenecks in Fast-Changing Clinical Protocols

- 4.3.4 Shift-Based Care Models Reduce Rich-Format Training Completion

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Delivery Mode

- 5.3.1 Self-Paced and Distance Learning

- 5.3.2 Instructor-Led Training

- 5.3.3 Blended Learning

- 5.4 By Application

- 5.4.1 Compliance Training

- 5.4.2 Clinical and Care Training

- 5.4.3 CME and Certification Training

- 5.4.4 Product and Commercial Training

- 5.4.5 Patient Safety Training

- 5.4.6 EHR/Clinical Systems Training

- 5.4.7 Infection Control Training

- 5.4.8 Cybersecurity and Data Privacy Training

- 5.4.9 Telehealth Training

- 5.4.10 Workforce Credentialing and Competency Management

- 5.5 By End User

- 5.5.1 Hospitals and Health Systems

- 5.5.2 Clinics and Ambulatory Care Providers

- 5.5.3 Pharmaceutical Companies

- 5.5.4 Medical Device Companies

- 5.5.5 Academic Medical Institutions

- 5.5.6 Long-Term Care Facilities

- 5.5.7 Home Healthcare Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 HealthStream, Inc.

- 6.4.2 Relias LLC

- 6.4.3 MedTrainer, Inc.

- 6.4.4 Docebo S.p.A.

- 6.4.5 D2L Corporation

- 6.4.6 Absorb Software Inc.

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Epignosis LLC

- 6.4.9 LearnUpon Limited

- 6.4.10 iSpring Solutions, Inc.

- 6.4.11 SkyPrep Inc.

- 6.4.12 Kallidus Limited

- 6.4.13 TOVUTI, Inc.

- 6.4.14 Medbridge Inc.

- 6.4.15 ACTO Technologies Inc.

- 6.4.16 Knowledge Factor, Inc. dba Amplifire

- 6.4.17 CareAcademy.co, Inc.

- 6.4.18 The World Continuing Education Alliance Ltd

- 6.4.19 Biomedical Research Alliance of New York LLC

- 6.4.20 Thought Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment