|

시장보고서

상품코드

2073334

영국의 AI 활용 에너지 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

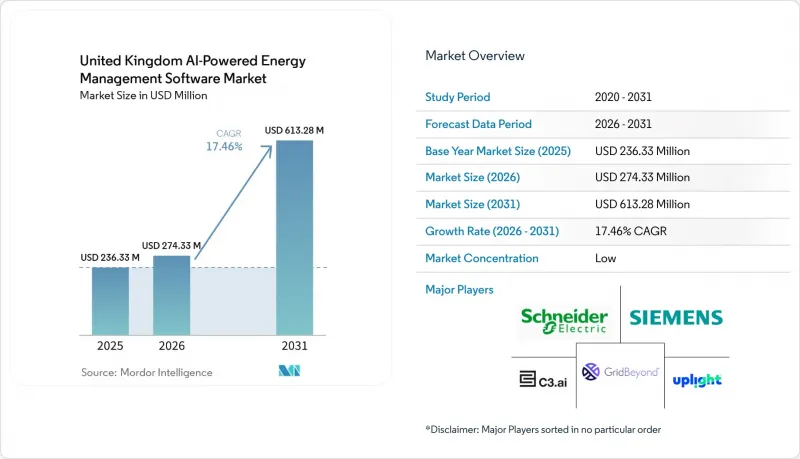

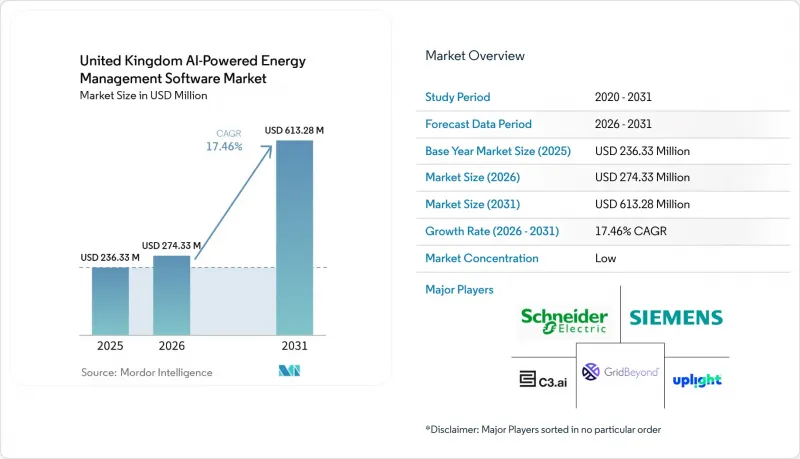

Mordor Intelligence에 의하면, 영국의 AI 활용 에너지 관리 소프트웨어 시장 규모는 2025년에 2억 3,633만 달러로 평가되었습니다. 2026년 2억 7,433만 달러에서 2031년까지 6억 1,328만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 예측 기간 동안 CAGR은 17.46%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 용도(에너지 제어, 자산 성과, 스마트 그리드 분석, 재생에너지 관리 등) 및 최종 사용자(유틸리티, 상업용 건물, 산업 시설, 주택)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

영국의 AI 활용 에너지 관리 소프트웨어 시장 동향 및 인사이트

AI를 활용한 실시간 부하 최적화가 플랫폼에 대한 구조적 수요를 견인하고 있습니다.

영국의 AI 활용 에너지 관리 소프트웨어 시장은 분산형 자산의 조정이 어려워짐에 따라, 실시간 부하 최적화가 단순한 성능상의 기능에서 송전망 관리의 필수 요건으로 전환되고 있는 점에 힘입어 성장하고 있습니다. 내셔널 그리드(National Grid)가 발표한 ‘에메랄드 AI(Emerald AI)"의 시범 운영을 통해, AI를 도입한 데이터센터가 송전망에서 전송되는 실시간 신호에 따라 1분 이내에 전력 수요를 최대 40%까지 조절할 수 있음이 입증되었습니다. 과학·혁신·기술부는 2026년 6월, 청정 에너지 분야에서의 실용적 수준의 도입과 시범 사업을 구분하는 핵심 요소는 확률론적이며 위험을 고려한 최적화라고 밝혔습니다. 이는 많은 그리드 에지 자산 및 산업용 자산에서 1초 미만의 시간 단위 내 제어 결정이 필요하기 때문에 중요한 점이며, 원격 클라우드 실행에만 의존하는 것이 아니라 엣지 컴퓨팅과 AI를 결합한 공급업체에게 경쟁 우위를 제공합니다. 그 결과, 영국의 AI 활용 에너지 관리 소프트웨어 시장에서 구매 기준은 로컬 추론, 신속한 응답, 그리고 제어 시스템과의 보다 긴밀한 통합으로 점차 변화하고 있습니다.

영국의 탄소중립 달성을 위한 노력이 정책 주도형 소프트웨어 수요를 창출하고 있습니다.

영국의 AI 활용 에너지 관리 소프트웨어 시장은 단기적인 비용 절감 프로그램보다 지속 가능한 정책적 의무에 의해 뒷받침되고 있습니다. 2026년 6월에 발표된 정부의 기후 행동 업데이트에서는 2038년부터 2042년에 걸쳐 배출량을 87% 감축하는 것을 목표로 하는 ‘제7차 탄소 예산"안이 지지를 얻었으며, 저탄소 인프라에 관한 의사결정에서 장기적인 계획 기간의 중요성이 재확인되었습니다. “에너지 디지털화 프레임워크"에서는 디지털화를 협력적이고 상호 연결된 에너지 시스템을 실현하기 위한 기반으로 규정하고, 51-66GW의 유연한 발전 용량의 필요성과 직접적으로 연결하고 있습니다. 이 정책 방침에 따라 전략 수립부터 조달에 이르는 과정이 단축될 것으로 보입니다. 특히 규제 대상 사업자의 경우, 거버넌스 기준이나 데이터 규정이 공식적으로 제정되면 일반적으로 시스템 투자가 가속화되기 때문입니다. 이를 통해 영국의 AI 활용 에너지 관리 소프트웨어 시장에는 단순한 에너지 절약에 그치지 않는 정책 기반이 마련되어, 유틸리티, 인프라 및 대규모 상업시설에서 수요가 뒷받침될 것입니다.

레거시 OT의 통합과 데이터 상호운용성의 복잡성이 도입을 지연시키고 있습니다.

구식 제어 환경은 여전히 영국의 AI 활용 에너지 관리 소프트웨어 시장에 큰 걸림돌이 되고 있습니다. 그 이유는 많은 에너지 자산이 상호 운용 가능한 데이터 교환이나 최신 사이버 제어 시스템을 염두에 두고 설계되지 않았기 때문입니다. DESNZ의 운영 기술(OT) 취약점 조사에 따르면, 이러한 시스템의 상당수는 이를 관리하는 IT 네트워크 외에는 통합된 보호 기능을 거의 갖추고 있지 않은 것으로 나타났습니다. 이 때문에 플랫폼 제공업체는 본격적인 운영 개시 전에 데이터 추출, 제어 로직, 안전성 검증 및 규정 준수 심사를 수행해야 하므로, 구매자는 더 긴 도입 주기를 감수할 수밖에 없습니다. 『2026-2030년 에너지 부문 사이버 보안 전략』에서는 OT(운영 기술) 엔지니어링과 사이버 보안 간의 연계 구축을 해당 분야에서 가장 어렵고 중요한 과제 중 하나로 꼽고 있습니다. 공통 아키텍처가 더 널리 정착되기 전까지는 통합 비용이 프로젝트마다 편차를 보이며, 이는 영국의 AI 활용 에너지 관리 소프트웨어 시장의 도입 지연을 계속해서 초래할 것입니다.

부문별 분석

2025년, 소프트웨어는 시장의 41.07%를 차지하며 영국의 AI 활용 에너지 관리 소프트웨어 시장에서 주요 제품으로 자리매김했습니다. 구매자가 통합형 소프트웨어를 선호한 이유는 기준선 모니터링, 최적화, 보고서 작성을 단일 운영 계층에서 통합할 수 있다는 점에 있습니다. 이는 여러 자산에 걸친 가시성을 높이고 보고 요건을 충족해야 했던 상업용 건물, 공공시설, 산업 시설에서 특히 중요했습니다. 또한 SaaS 모델은 초기 계약 규모를 축소하고, 공급업체가 추후 분석 모듈, 커넥터, 통합 계층을 통해 서비스를 확장할 수 있도록 함으로써 보다 광범위한 도입을 촉진했습니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 19.78%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 많은 구매자들이 소프트웨어를 처음 구매한 후에도 OT(운영 기술)와의 통합, 모델 재학습, 제어 미세 조정, 지속적인 보고서 작성 등에서 지원이 필요하다는 사실을 반영하고 있습니다. Trane Technologies의 BrainBox AI 진출은 설비 및 빌딩 시스템 관련 기업들이 AI 소프트웨어의 기능을 활용하여 에너지 관리 및 자율형 빌딩 제어 분야에서 장기적인 서비스 가치를 심화시키고 있음을 보여줍니다. 실제로는 소프트웨어 도입과 실제로 실현되는 비용 절감 사이의 가치 격차로 인해, 영국의 AI 활용 에너지 관리 소프트웨어 시장 전반에서 관리형 서비스나 성과 연계형 서비스로의 계약 전환이 진행되고 있습니다.

2025년, 영국의 AI 활용 에너지 관리 소프트웨어 시장 규모 중 클라우드 기반 도입이 58.15%를 차지하며, 주요 도입 모델로서의 위상을 유지했습니다. 많은 상업용 빌딩 운영 사업자들은 고립된 On-Premise형 시스템에 비해 도입이 신속하고 인프라 부담도 적다는 이유로 클라우드 플랫폼을 선호하여 도입했습니다. 또한, 클라우드 플랫폼은 계량기, 자산, 소비자 데이터 등 다양한 환경에 걸쳐 표준화된 인터페이스를 제공할 수 있으므로, 보다 광범위한 상호 운용성이라는 목표에도 부합합니다. 이에 따라 지연에 미치는 영향이 비교적 적은 이용 사례에서 중앙 집중형 분석이나 포트폴리오 전체에 대한 가시성이 가장 중요하게 여겨지는 상황에서는 클라우드 도입이 현실적인 선택지가 되었습니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 18.67%로 확대될 것으로 예상되며, 일부 제어 결정은 자산 현장에서 내려야 하기 때문에 인기가 높아지고 있습니다. 배터리 저장, 전기차 충전, 히트 펌프, 스마트 인버터의 경우, 현지에서 매우 신속한 의사 결정이 필요한 경우가 많으며, 순수한 클라우드 아키텍처로는 이를 항상 실현할 수 있는 것은 아닙니다. 따라서 하이브리드 시스템으로의 전환은 사이버 보안이나 데이터 소재지에 대한 우려와 마찬가지로 운영상의 필요성에 기인합니다. 영국의 AI 활용 에너지 관리 소프트웨어 시장이 유틸리티, 산업, 그리드 에지 분야의 활용 사례로 더욱 깊이 침투함에 따라, 중앙 집중형 분석과 현지 제어 간의 이러한 균형 덕분에 하이브리드 도입은 계속해서 견조한 추세를 보일 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united kingdom AI-powered energy management software market size was valued at USD 236.33 million in 2025 and estimated to grow from USD 274.33 million in 2026 to reach USD 613.28 million by 2031, at a CAGR of 17.46% during the forecast period 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Application (Energy Control, Asset Performance, Smart Grid Analytics, Renewable Energy Management, and More), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom AI-Powered Energy Management Software Market Trends and Insights

AI-Based Real-Time Load Optimization Drives Structural Platform Demand

The United Kingdom AI-powered energy management software market is gaining from the shift in real-time load optimization from a performance feature to a grid management requirement as distributed assets become harder to coordinate. National Grid's Emerald AI trial showed that AI-enabled data centers could flex power demand by up to 40% in under a minute in response to live grid signals. The Department for Science, Innovation and Technology stated in June 2026 that probabilistic and risk-aware optimization is the key feature that separates production-grade deployment from pilot activity in clean energy applications. This matters because many grid-edge and industrial assets need control decisions in sub-second timeframes, which gives an advantage to suppliers that combine edge computing with AI rather than relying only on remote cloud execution. As a result, buying criteria in the United Kingdom AI-powered energy management software market are moving toward local inference, rapid response, and deeper control-system integration.

UK Net-Zero Compliance Generates Policy-Led Software Demand

The United Kingdom AI-powered energy management software market is also supported by policy obligations that are more durable than short-cycle cost-reduction programs. The government's climate action update in June 2026 backed the proposed 7th Carbon Budget, which targets an 87% reduction in emissions across 2038-2042 and reinforces the long planning horizon for low-carbon infrastructure decisions. The Energy Digitalization Framework described digitalization as enabling infrastructure for a coordinated, connected energy system and tied it directly to the need for 51-66 GW of flexible capacity. The same policy direction is likely to shorten the path from strategy to procurement, especially for regulated operators, which typically accelerate system investment once governance standards and data rules are formalized. This gives the UK AI-powered energy management software market a policy base that extends beyond energy savings alone and supports demand in utilities, infrastructure, and larger commercial estates.

Legacy OT Integration And Data Interoperability Complexity Slows Deployment

Legacy control environments remain a major brake on the United Kingdom AI-powered energy management software market because many energy assets were not designed for interoperable data exchange or modern cyber controls. DESNZ research on operational technology vulnerabilities stated that many of these systems have little integrated protection beyond the IT network that manages them. This pushes buyers into longer deployment cycles because platform providers must address data extraction, control logic, safety validation, and compliance review before live operation begins. The Energy Sector Cyber Security Strategy for 2026-2030 calls the bridge between OT engineering and cybersecurity one of the hardest and most important issues in the sector. Until common architectures are more widely established, integration costs will remain uneven across projects and will keep slowing deployment in the United Kingdom AI-powered energy management software market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity Price Volatility Sharpens The Commercial Case

- Smart Meter And IoT Data Readiness Expands AI Use Cases

- Cybersecurity And Data Sovereignty Concerns Constrain Enterprise Adoption Pace

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 41.07% of the market in 2025, making it the leading offering in the United Kingdom AI-powered energy management software market. Buyers favored integrated software because it could combine baseline monitoring, optimization, and reporting in a single operating layer. This was especially relevant for commercial buildings, utilities, and industrial facilities that needed better visibility across multiple assets and reporting requirements. The SaaS model also supported wider adoption by reducing initial contract size and allowing vendors to expand later through analytics modules, connectors, and integration layers.

Services are projected to expand at a 19.78% CAGR through 2031, making them the fastest-growing segment. This growth reflects the fact that many buyers need help with OT integration, model retraining, controls tuning, and ongoing reporting after the initial software purchase. Trane Technologies' move into BrainBox AI showed how equipment and building-system players are using AI software capabilities to deepen long-term service value in energy management and autonomous building control. In practice, the value gap between software installation and realized savings is pushing more contracts toward managed or outcome-linked services across the UK AI-powered energy management software market.

Cloud-based deployment accounted for 58.15% of the United Kingdom AI-powered energy management software market size in 2025, which kept it as the dominant deployment model. Many commercial building operators preferred cloud platforms because they offered faster onboarding and lower infrastructure burden than isolated on-premises systems. Cloud platforms also fit well with broader interoperability goals because they can expose standardized interfaces across meter, asset, and consumer data environments. This made cloud deployment a practical choice in less latency-sensitive use cases where central analytics and portfolio-wide visibility mattered most.

Hybrid deployment is projected to expand at a 18.67% CAGR through 2031 and is gaining popularity because some control decisions must be made close to the asset. Battery storage, EV charging, heat pumps, and smart inverters often need very fast local decision-making, which pure cloud architectures cannot always deliver. The push toward hybrid systems is therefore based on operational need as much as on cyber assurance or data residency concerns. This balance between central analytics and local control is likely to keep hybrid adoption strong as the UK AI-powered energy management software market moves deeper into utility, industrial, and grid-edge use cases.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

List of Companies Covered in this Report:

- C3.ai, Inc.

- GridBeyond Limited

- Uplight, Inc.

- Bidgely, Inc.

- Copperleaf Technologies Inc.

- BrainBox AI Inc.

- Kaluza Limited

- Verdigris Technologies, Inc.

- EnergyCAP, LLC

- Schneider Electric SE

- Spacewell International N.V.

- Wattics Limited

- Dexma Sensors, S.L.U.

- Smart Energy Water, Inc.

- Encentiv Energy, Inc.

- Logical Buildings, Inc.

- nZero, Inc.

- Energy Elephant Limited

- Passiv Systems Limited

- EM3

- Greenbyte AB

- Siemens AG

- RetrofitAI, Inc.

- Noda AI Ltd.

- Power Factors, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Based Real-Time Load Optimization Across Distributed Assets

- 4.2.2 United Kingdom Net-Zero Compliance and Carbon Reporting Pressure

- 4.2.3 Rising Electricity Price Volatility and Peak Demand Exposure

- 4.2.4 Smart Meter, IoT, and Building Automation Data Readiness

- 4.2.5 Digital Twin Adoption for Predictive Energy Control

- 4.2.6 Data Center, Commercial Property, and Industrial Efficiency Mandates

- 4.3 Market Restraints

- 4.3.1 Legacy OT Integration and Data Interoperability Complexity

- 4.3.2 Cybersecurity and Data Sovereignty Concerns

- 4.3.3 Unclear Payback Period for Mid-Market Buyers

- 4.3.4 Shortage of AI, Energy, and Controls Talent

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 C3.ai, Inc.

- 6.4.2 GridBeyond Limited

- 6.4.3 Uplight, Inc.

- 6.4.4 Bidgely, Inc.

- 6.4.5 Copperleaf Technologies Inc.

- 6.4.6 BrainBox AI Inc.

- 6.4.7 Kaluza Limited

- 6.4.8 Verdigris Technologies, Inc.

- 6.4.9 EnergyCAP, LLC

- 6.4.10 Schneider Electric SE

- 6.4.11 Spacewell International N.V.

- 6.4.12 Wattics Limited

- 6.4.13 Dexma Sensors, S.L.U.

- 6.4.14 Smart Energy Water, Inc.

- 6.4.15 Encentiv Energy, Inc.

- 6.4.16 Logical Buildings, Inc.

- 6.4.17 nZero, Inc.

- 6.4.18 Energy Elephant Limited

- 6.4.19 Passiv Systems Limited

- 6.4.20 EM3

- 6.4.21 Greenbyte AB

- 6.4.22 Siemens AG

- 6.4.23 RetrofitAI, Inc.

- 6.4.24 Noda AI Ltd.

- 6.4.25 Power Factors, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment