|

시장보고서

상품코드

2073370

민간 항공기 리스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Commercial Aircraft Leasing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

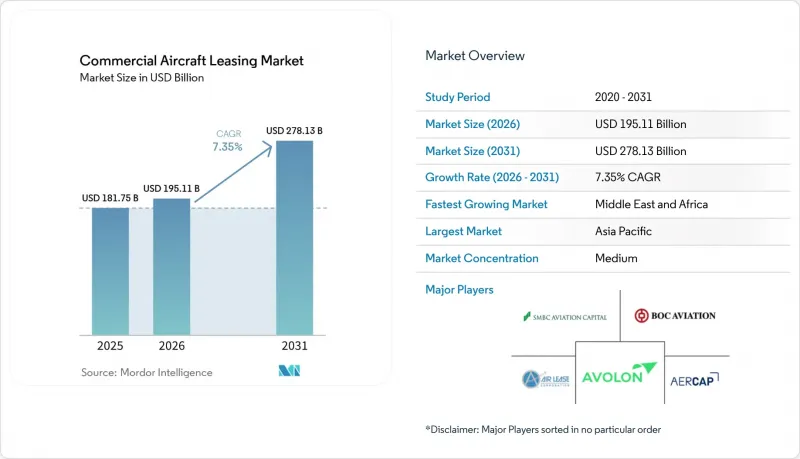

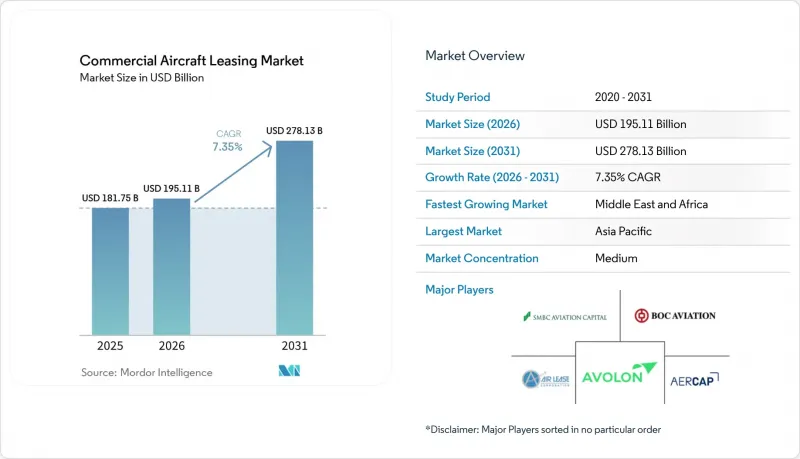

Mordor Intelligence에 의하면, 2026년 민간 항공기 리스 시장 규모는 1,951억 1,000만 달러에 달할 것으로 예상되고, 2025년 1,817억 5,000만 달러에서 증가하고 있습니다.

또한, 2031년의 예측치는 2,781억 3,000만 달러로, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.35%로 성장할 것으로 전망됩니다.

본 보고서는 리스 형태(웨트리스 및 드라이리스), 기체 유형(나로우바디, 와이드바디, 리저널 제트, 화물기/P2F 개조기), 최종 사용자(풀서비스 항공사, 저비용 항공사 등), 리스 기간(단기, 중기, 장기), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 민간 항공기 리스 시장 동향 및 인사이트

저가 항공사의 급속한 확장이 리스 보급률을 높이고 있습니다.

LCC는 현금을 확보하고 신속하게 규모를 확대하기 위해 리스에 의존하고 있으며, 이것이 민간 항공기 리스 시장을 지탱하는 구조적 추세를 만들어내고 있습니다. 인디고(IndiGo)가 BOC 항공과 체결한 A320neo 제트기 4대에 관한 계약과 사우스웨스트 항공이 BBAM과 체결한 2025년 세일 앤 리스백 계약은 항공사가 막대한 초기 자본 지출 없이 운항 능력을 확보할 수 있는 방법을 보여주는 좋은 사례입니다. 또한, 리스를 활용함으로써 LCC는 수요 변동에 따라 기종 구성을 유연하게 조정할 수 있게 되며, 이는 수요가 급변할 때 큰 강점이 됩니다. 인도, 동남아시아, 사하라 이남 아프리카의 중산층 가처분 소득 증가는 노선 확장 주기를 뒷받침하고 있으며, 이에 따라 LCC 부문은 2030년까지 연평균 성장률(CAGR) 8.78%로 성장을 이어가며, 협폭기 수요를 견인하는 동시에 리스 회사의 협상력을 강화하게 될 것입니다.

OEM 생산의 병목 현상이 리스 회사의 가격 결정력을 높입니다.

품질 관리상의 문제와 공급망 혼란으로 인해 에어버스와 보잉의 생산량이 감소하고 있으며, 이로 인해 항공사에는 납품 부족 현상이 발생하고 있어 리스 요율 상승 요인으로 작용하고 있습니다. SMBC 항공 캐피탈의 보고서에 따르면, 2023년 하반기 이후 신형 와이드바디 항공기의 리스 요율은 7-12% 상승했으며, 평균 리스 기간은 12년으로 늘어남에 따라 리스 회사들의 현금 흐름 전망이 확보되고 있습니다. 각 항공사가 운항 능력 부족 위험을 피하기 위해 구형 항공기를 장기간 보유하기로 선택함에 따라, 중고 항공기 시장의 평가액은 견조한 추세를 보이고 있습니다. 생산 병목 현상은 2028년까지 해소되지 않을 전망이며, 이는 향후 몇 년간 임대료에 긍정적인 요인으로 작용할 것입니다.

금리 변동이 수익률 스프레드를 압박

2024년, 미국 연방준비제도이사회(FRB)의 긴축 통화 정책으로 인해 리스 회사의 자금 조달 비용이 상승했으며, 일부 부문에서는 OEM(항공기 제조업체)의 가격 인상이 리스료 상승률을 상회했습니다. 에어 리스 코퍼레이션의 2024년 순이익은 매출이 증가했음에도 불구하고 3억 7,200만 달러로 감소했으며, 이는 이러한 압박 상황을 여실히 보여주고 있습니다. 부채가 많은 리스 회사는 가장 심각한 이익률 압박에 직면해 있지만, 항공기 공급 제약이 그 영향을 일부 상쇄하고 있습니다.

부문별 분석

2025년, 각 항공사가 조종실 및 객실의 표준화, 훈련의 시너지 효과, 비용 관리를 우선시한 결과, 드라이 리스가 민간 항공기 리스 시장의 83.92%를 차지했습니다. 이 압도적인 점유율은 민간 항공기 리스 시장 규모인 1억 5,250만 달러에 해당하며, 리스 회사에 예측 가능한 장기적인 현금 흐름을 가져다주고 있습니다. ACMI 계약으로 이루어진 웻 리스(wet lease) 틈새 시장은 항공사들이 계절적 수송 능력이나 정비 성수기, 조종사 부족 시의 긴급 수송 능력을 필요로 하기 때문에 연평균 성장률(CAGR) 8.31%로 확대되고 있습니다. 노스 애틀랜틱 항공이 B787-9를 계속 보유하면서 B787-8 3대를 반납하기로 한 결정은 항공사가 최적의 기체 크기와 노선 수익성을 확보하기 위해 기종 구성을 재조정하고 있음을 보여줍니다. 웨트리스 사업자는 유럽 및 서아시아의 여름 성수기 기간 동안 그 중요성이 점점 더 커지고 있으며, 네트워크 항공사가 새로운 자본 지출을 하지 않고도 운항 능력 부족을 보완할 수 있게 해주고 있습니다.

예측 기간 동안, 웨트리스 사업자들은 계속해서 ACMI의 유연성을 활용할 것으로 보입니다. 그렇긴 하지만, 드라이 리스는 항공사의 비용 효율성 목표와 리스 회사의 자산 관리 요구 사항을 충족시키기 위해 민간 항공기 리스 시장의 기반으로서 계속 자리매김할 것입니다.

2025년에는 협폭기체가 임대 항공기 총수의 61.22%를 차지했으며, 이는 민간 항공기 임대 시장 규모 1억 1,130만 달러에 해당합니다. 이는 고빈도 노선에서 나로우바디 항공기가 보여주는 타의 추종을 불허하는 경제성을 반영한 것입니다. A321neo 및 B737 MAX의 인도는 기종 교체를 주도하고 있으며, 그 견실한 잔존 가치 덕분에 리스 회사의 대차대조표상에서 가장 위험이 낮은 자산으로 자리매김하고 있습니다. 한편, 화물기 및 여객기에서 화물기로 전환된 항공기(P2F)는 택배 업체들이 국경을 초월한 전자상거래 흐름을 한발 앞서 선점하기 위해 서두르는 가운데, 연평균 성장률(CAGR) 9.08%라는 가장 빠른 성장세를 보이고 있습니다. AviLease는 2025년에 A350F를 발주하여 이 부문에 진출할 예정이며, 이는 와이드바디 화물기가 중동 허브 공항의 성장 축이 될 것임을 시사합니다. 와이드바디 여객기의 경우 단기적으로는 생산 대수가 정체될 전망이지만, 장거리 노선에서의 프리미엄 수요가 리스 요율의 안정을 뒷받침하고 있습니다. 지역 제트기는 브라질, 인도, 미국의 직항 노선 연결을 담당하고 있지만, 그 점유율은 민간 항공기 리스 시장 전체의 5% 미만에 그치고 있습니다.

보잉사는 2043년까지 2,800대의 화물기가 추가될 것으로 전망하고 있으며, 그중 절반 이상이 여객기를 화물기로 개조(P2F)한 기체입니다. 이를 통해 자산 수명의 연장 및 잔존 가치의 향상이 시너지 효과를 발휘하는 선순환이 만들어집니다. 조기 개조 할당량을 확보할 수 있는 리스 회사는 매력적인 수익률을 확보하는 동시에, 경기 변동의 영향을 받기 쉬운 여객 수요에 의존하지 않는 수익 다각화를 도모할 수 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 35.12%를 차지했습니다. 이는 연평균 4.8%라는 급속한 여객 수송량 증가와 2043년까지 19,500대에 달하는 수주 파이프라인이 항공기 증강 수요를 뒷받침했기 때문입니다. 리스 이용률은 가동 중인 장비의 60%에 육박하며, 세계 평균을 크게 상회하고 있습니다. 이는 민간 항공기 리스 시장이 지역 항공사들의 전략에서 핵심적인 역할을 하고 있음을 보여줍니다. 중국 CDB Aviation의 A320neo 80대 수주와, 인도의 '2025년 항공기 관련 법안' (국내 압류법을 케이프타운 협약의 규정에 부합하도록 하는 것)은 해당 지역에 대한 해외 자본의 매력을 높이고 있습니다.

중동 및 아프리카는 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)이 9.33%를 나타낼 것으로 전망됩니다. 사우디아라비아가 소유한 AviLease사는 자사 최초의 보잉 기종으로 B737-8 기종 30대를 발주했으며, 2025년에는 A350F 화물기 계약을 체결했습니다. 이는 사우디아라비아의 '비전 2030' 전략을 뒷받침하는 요소입니다. 아프리카의 항공기 대수는 두 배로 늘어나고, 화물기 대수는 3배로 증가할 것으로 예상되어, 협폭기체를 화물기로 개조하는 것을 전문으로 하는 리스 회사들에게 큰 새로운 시장이 열리게 될 것입니다.

북미와 유럽은 성숙한 시장임에도 불구하고 혁신적인 움직임이 나타나고 있습니다. 더블린, 런던, 뉴욕, 로스앤젤레스에 거점을 둔 리스 회사들은 계속해서 전 세계 자금 조달에서 핵심적인 역할을 수행하고 있습니다. 이 지역에서 시작된 지속가능성 연계형 대출과 그린본드는 민간 항공기 리스 시장 전체의 환경적 투명성을 높이고 있습니다. 두바이 에어로스페이스 엔터프라이즈의 노르딕 항공 캐피털 인수 등 업계 재편은 규모의 경제와 자금 조달 접근성이 여전히 결정적인 요소임을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the commercial aircraft leasing market size in 2026 is estimated at USD 195.11 billion, up from 2025's USD 181.75 billion, with 2031 projections showing USD 278.13 billion, growing at a 7.35% CAGR over 2026-2031.

This report is Segmented by Leasing Type (Wet Lease and Dry Lease), Aircraft Type (Narrowbody, Widebody, Regional Jets, and Freighter/P2F Converted Aircraft), End User (Full-Service Carriers, Low-Cost Carriers, and More), Lease Duration (Short-Term, Medium-Term, and Long-Term), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Aircraft Leasing Market Trends and Insights

Rapid low-cost-carrier expansion increases leasing penetration

Low-cost carriers rely on leasing to conserve cash and scale quickly, driving a structural preference that supports the commercial aircraft leasing market. IndiGo's agreement with BOC Aviation for four A320neo jets and Southwest Airlines' 2025 sale-and-leaseback with BBAM exemplify how carriers secure lift without large upfront capital outlays. Leasing also allows LCCs to recalibrate fleets in response to volatile demand, a key advantage during traffic shocks. Rising middle-class disposable incomes in India, Southeast Asia, and sub-Saharan Africa underpin a route-expansion cycle that will keep the LCC segment growing at an 8.78% CAGR through 2030, reinforcing demand for narrowbody lift and supporting lessor bargaining power.

OEM production bottlenecks elevate lessor pricing power

Quality-control issues and supply-chain disruptions have trimmed Airbus and Boeing output, leaving airlines with delivery shortfalls and pushing lease-rate factors higher. SMBC Aviation Capital reports 7-12% lease-rate growth for new wide-bodies since late 2023, while average lease terms have climbed to 12 years, locking in cash-flow visibility for lessors. Secondary-market valuations are firm because carriers choose to keep older aircraft longer rather than risk capacity gaps. The bottlenecks are unlikely to ease before 2028, underscoring a multi-year tailwind for lease pricing.

Interest-rate volatility erodes yield spreads

Federal Reserve tightening lifted lessor funding costs during 2024, and OEM price hikes outpaced lease-rate growth in certain segments. Air Lease Corporation's net income slipped to USD 372 million in 2024 even as revenues climbed, illustrating the squeeze. Debt-heavy lessors face the sharpest margin pressure, though constrained aircraft supply partly offsets the impact.

Other drivers and restraints analyzed in the detailed report include:

- P2F conversions unlock a secondary growth engine

- Decarbonization roadmaps accelerate fleet renewal

- Geopolitical sanctions complicate asset recovery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry leases held 83.92% of the commercial aircraft leasing market in 2025 as airlines prioritized cockpit-and-cabin standardization, training synergies, and cost control. This dominance translates into USD 152.5 million of the commercial aircraft leasing market size, giving lessors predictable long-run cash flows. The wet-lease niche-comprising ACMI agreements-expands at 8.31% CAGR because carriers need seasonal capacity and contingency lift during maintenance peaks or pilot shortages. Norse Atlantic's decision to return three B787-8s while retaining B787-9s shows how airlines recalibrate portfolios for optimum gauge and trip economics. Wet-lease providers are increasingly important during peak summer schedules in Europe and West Asia, enabling network carriers to plug capacity gaps without fresh capital outlays.

Over the forecast period, wet-lease operators will keep leveraging ACMI flexibility. Still, dry leasing will remain the bedrock of the commercial aircraft leasing market because it meets airline cost-efficiency targets and lessor asset-management preferences.

Narrowbodies represented 61.22% of total leased units in 2025, equivalent to USD 111.3 million of the commercial aircraft leasing market size, reflecting their unmatched economics on high-frequency routes. A321neo and B737 MAX deliveries drive fleet renewal, while strong residual liquidity makes them the least risky assets for lessors' balance sheets. However, freighters and P2F aircraft are the fastest climbers at 9.08% CAGR as express-parcel operators rush to capture cross-border e-commerce flows. AviLease joined the segment with A350F orders during 2025, signalling that wide-body freighters will anchor growth for Middle-East hubs. Wide-body passenger aircraft face muted near-term output, yet premium long-haul demand supports lease-rate endurance. Regional jets serve point-to-point connectivity in Brazil, India, and the US, but their share remains below 5% of the commercial aircraft leasing market.

Boeing projects 2,800 additional freighters by 2043, with more than half coming from P2F conversions, executing a virtuous cycle of asset-life extension and residual-value uplift. Lessors that can secure early conversion slots will lock in attractive yields and diversify income away from cyclical passenger demand.

Complete Report Scope:

- By Leasing Type

- Wet Lease

- Dry Lease

- By Aircraft Type

- Narrowbody

- Widebody

- Regional Jets

- Freighter/P2F Converted Aircraft

- By End-User

- Full-Service/Network Carriers

- Low-Cost Carriers (LCCs)

- Dedicated Cargo Airlines

- Charter and ACMI Operators

- By Lease Duration

- Short-Term

- Medium-Term

- Long-Term

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Ireland

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East and Africa

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific held 35.12% of global revenue during 2025 as rapid traffic expansion, averaging 4.8% annually, and an order pipeline of 19,500 aircraft through 2043 reinforced fleet-growth needs. Leasing penetration already approaches 60% of the active fleet, well above the global average, demonstrating the centrality of the commercial aircraft leasing market to regional airline strategies. China's CDB Aviation order for 80 A320neo jets and India's Aircraft Objects Bill 2025, which aligns domestic repossession law with Cape Town provisions, strengthen the region's attractiveness for foreign capital.

The Middle East and Africa region is the fastest-growing, posting a 9.33% CAGR through 2031. Saudi-owned AviLease placed its first Boeing order for 30 B737-8 jets and signed for A350F freighters in 2025, supporting the Kingdom's Vision 2030 strategy. Africa's fleet is set to double, and its freighter count will triple, opening a major frontier for lessors specializing in narrowbody cargo conversions.

North America and Europe remain mature yet innovative. Lessors based in Dublin, London, New York, and Los Angeles continue to anchor global funding. Sustainability-linked loans and green bonds originated in these regions and drive environmental transparency throughout the commercial aircraft leasing market. Consolidation, such as Dubai Aerospace Enterprise's acquisition of Nordic Aviation Capital, indicates that economies of scale and funding access remain decisive.

- AerCap Holdings N.V.

- SMBC Aviation Capital

- Avolon Aerospace Leasing Limited

- Air Lease Corporation

- BOC Aviation Limited

- Dubai Aerospace Enterprise (DAE) Ltd.

- CDB Aviation Lease Finance DAC

- China Aircraft Leasing Limited (CALC)

- Aviation Capital Group LLC

- ICBC Co., Ltd.

- Jackson Square Aviation Ireland Limited

- TrueNoord Limited

- GA Telesis, LLC

- Carlyle Aviation Partners Ltd.

- Castlelake, L.P.

- Falko Regional Aircraft Limited

- Avation PLC

- AVILEASE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid global adoption of the low-cost-carrier model boosting leased-fleet penetration

- 4.2.2 OEM production bottlenecks extending average lease terms and elevating lease-rate factors

- 4.2.3 Strong demand for passenger-to-freighter conversions creating secondary leasing boom

- 4.2.4 Airline decarbonization roadmaps triggering accelerated replacement cycles

- 4.2.5 Rising lease-rate factors attracting institutional investors

- 4.2.6 Harmonized legal protections reducing repossession risk and lowering cost of capital

- 4.3 Market Restraints

- 4.3.1 Escalating OEM list prices and interest-rate volatility compressing lessor yield margins

- 4.3.2 Complex geopolitical sanctions heightening repossession and redeployment risk

- 4.3.3 ESG-driven lending policies restricting financing for older, less-efficient aircraft

- 4.3.4 Technology uncertainty around next-generation propulsion depressing residual-value outlooks

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Leasing Type

- 5.1.1 Wet Lease

- 5.1.2 Dry Lease

- 5.2 By Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.2.3 Regional Jets

- 5.2.4 Freighter/P2F Converted Aircraft

- 5.3 By End-User

- 5.3.1 Full-Service/Network Carriers

- 5.3.2 Low-Cost Carriers (LCCs)

- 5.3.3 Dedicated Cargo Airlines

- 5.3.4 Charter and ACMI Operators

- 5.4 By Lease Duration

- 5.4.1 Short-Term

- 5.4.2 Medium-Term

- 5.4.3 Long-Term

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Ireland

- 5.5.2.2 United Kingdom

- 5.5.2.3 Germany

- 5.5.2.4 France

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Singapore

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East and Africa

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AerCap Holdings N.V.

- 6.4.2 SMBC Aviation Capital

- 6.4.3 Avolon Aerospace Leasing Limited

- 6.4.4 Air Lease Corporation

- 6.4.5 BOC Aviation Limited

- 6.4.6 Dubai Aerospace Enterprise (DAE) Ltd.

- 6.4.7 CDB Aviation Lease Finance DAC

- 6.4.8 China Aircraft Leasing Limited (CALC)

- 6.4.9 Aviation Capital Group LLC

- 6.4.10 ICBC Co., Ltd.

- 6.4.11 Jackson Square Aviation Ireland Limited

- 6.4.12 TrueNoord Limited

- 6.4.13 GA Telesis, LLC

- 6.4.14 Carlyle Aviation Partners Ltd.

- 6.4.15 Castlelake, L.P.

- 6.4.16 Falko Regional Aircraft Limited

- 6.4.17 Avation PLC

- 6.4.18 AVILEASE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment