|

시장보고서

상품코드

2073569

동남아시아의 폐기물 에너지화 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Southeast Asia Waste-to-Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

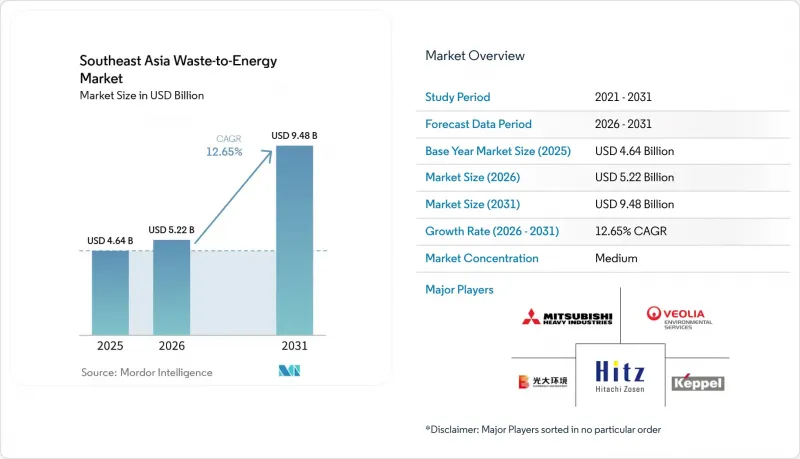

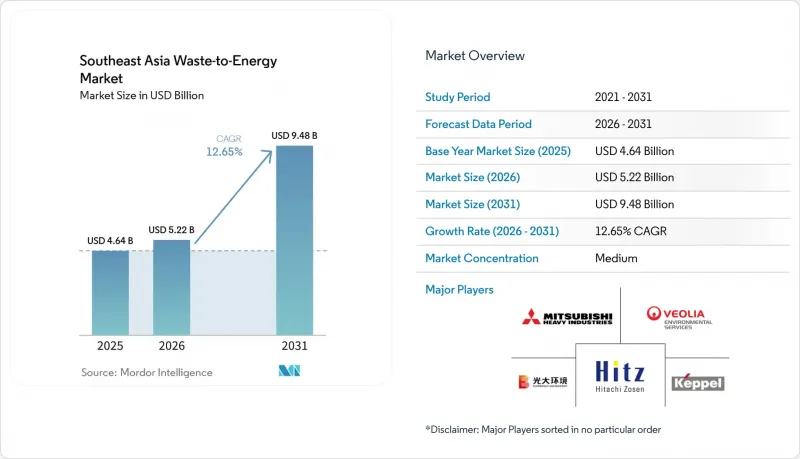

Mordor Intelligence에 의하면, 동남아시아의 폐기물 에너지화 시장 규모는 2025년 46억 4,000만 달러로 평가되었습니다. 2026년에는 52억 2,000만 달러로 확대되어 2031년까지 94억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 12.65%로 성장할 전망입니다.

본 보고서는 기술별(물리적, 열적, 생물학적), 폐기물 유형별(일반 폐기물, 산업 폐기물 등), 에너지 출력별(전력, 열 등), 최종 사용자별(유틸리티체/독립발전사업자, 산업용 자가소비, 지역난방, 연료 판매업자), 지역별(인도네시아, 말레이시아, 태국, 싱가포르, 베트남, 필리핀, 기타 동남아시아)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

동남아시아의 폐기물 에너지화 시장 동향 및 인사이트

폐기물 발생량 증가가 매립지의 처리 능력을 초과합니다.

인도네시아에서는 2023년에 5,663만 톤의 일반 폐기물이 발생했으나, 그중 적절하게 관리된 양은 고작 39%에 그쳐, 수거·처리 시스템이 폐기물 발생량에 비해 여전히 크게 뒤처져 있음을 알 수 있습니다. 핵심적인 문제는 폐기물 양 증가뿐만 아니라, 대도시와 2급 도시권 간의 수거, 처리 및 최종 처분 능력 격차가 확대되고 있다는 점에 있습니다. 폐기물 증가가 더 이상 거대 도시에만 국한되지 않고, 소규모 도시권도 상업적 처리 시설을 운영할 수 있는 규모에 도달함에 따라 이러한 격차는 점점 더 중요해지고 있습니다. 따라서, 수거 네트워크가 아직 대규모 중앙집중형 프로젝트를 감당할 수 없는 일부 지역에서는 하루 200-500톤의 처리 능력을 갖춘 플랜트 형태의 도입 가능성이 높아지고 있습니다. 이러한 현지 상황으로 인해, 규모, 물류, 자금 조달을 변경하지 않는 한 해외에서 도입된 대규모 플랜트 모델을 그대로 적용하기는 어려워지고 있습니다. 그 결과, 동남아시아의 폐기물 에너지화 시장은 대도시권에 국한된 솔루션에서 더 광범위한 지자체 인프라 분야로 확대되고 있습니다.

자금 조달을 가능하게 하는 정부의 인센티브와 PPP 체계

인도네시아의 2025년 대통령령 제109호는 기존의 “처리 수수료"와 “전력 임베디드"의 이중 구조를, 30년간의 전력 임베디드 계약에 근거한 1kWh당 0.20달러의 단일 고정 요금제로 대체함으로써, 프로젝트의 자금 조달 가능성을 대폭 개선했습니다. 또한, 해당 규제로 인해 조달 체계가 더욱 일원화됨에 따라, 지자체 내 의사결정과 프로젝트 실행 간의 단절 현상이 완화되었습니다. 태국에서는 아시아개발은행(ADB)이 지원하는 12곳의 산업폐기물 에너지화소를 위한 166억 바트(5억 2,150만 달러 상당) 규모의 지원 패키지가, 다자간 기구의 지원을 통해 그동안 자금 조달에 어려움을 겪어왔던 프로젝트의 실현 가능성을 열어주었습니다. 요금, 폐기물 반입 및 운영권 조건이 조기에 확정되면 민간 자본의 유입이 가속화되므로, 이러한 정책 조치는 중요합니다. 또한, 이러한 조치는 긴 거래처 사슬에 의존하지 않고 자금 조달에서 설계, 플랜트 운영으로 원활하게 전환할 수 있는 사업 주체에게 유리하게 작용합니다. 이것이 바로 동남아시아의 폐기물 에너지화 시장이 산발적인 시범 사업에서 더 대규모이고 재현성이 높은 프로젝트 파이프라인으로 전환되고 있는 가장 분명한 이유 중 하나입니다.

초기 설비 투자 비용이 높아 지역 전체 프로젝트의 자금 조달 가능성을 압박하고 있습니다.

최근 프로젝트 발표에 따르면, 해당 지역의 1,000 tpd급 플랜트에는 여전히 수억 달러 규모의 자본 투자가 필요하며, 신규 진입업체의 자금 조달 장벽은 여전히 높은 상태입니다. 말레이시아의 숭가이 우단 시설은 34년간의 운영권 계약에 따라 일일 1,056톤 및 22MW의 처리 능력을 갖추고 있으며, 프로젝트 비용은 6억 6,000만 링깃(1억 4,900만 달러 상당)에 달할 전망입니다. 하노이 소크손의 2단계 확장 계획에서는 하루 1,600톤의 처리 능력을 추가하며, 투자액은 5조 8,300억 동(2억 3,900만 달러 상당)에 달할 전망입니다. 장기적인 운영권 기간은 수익 전망을 명확히 하는 데 도움이 되지만, 자산의 운영 기간 동안 요금이 인플레이션에 맞추어 조정되지 않는 경우, 금융 기관들은 여전히 신중한 태도를 유지하고 있습니다. 전처리 시스템, 배기가스 제어, 건설 리스크는 플랜트가 안정 가동에 들어가기도 전부터 진입 비용을 상승시킵니다. 이는 동남아시아의 폐기물 에너지화 시장에서 여전히 더 견고한 재무 기반을 갖추고, 계약업체에 대한 관리 능력이 뛰어나며, 정부나 다자간 기구로부터 지원을 받을 수 있는 후원사가 유리한 입장에 있음을 의미합니다.

부문별 분석

2025년, 동남아시아의 폐기물 에너지화 시장에서 열처리 기술은 62.1%의 점유율을 차지하며, 대규모 도시 폐기물 처리 시스템에서 여전히 주류 처리 방식으로서의 위상을 유지했습니다. 이러한 우위는 화격자식 소각로와 처리 용량이 큰 도시 폐기물 간의 적합성에서 비롯되며, 특히 프로젝트의 경제성이 지속적인 폐기물 반입과 확실한 전력 임베디드 계약에 의존하는 지역에서 두드러집니다. 하노이의 쏭쑤언 시설은 2025년 10월 가동을 시작할 당시 이미 해당 도시의 일일 생활폐기물 처리량의 70%를 처리하고 있었으며, 이는 열처리 시스템이 대도시의 폐기물 처리량을 얼마나 효율적으로 감당할 수 있는지를 보여줍니다. 또한, 열처리 플랜트는 보다 성숙한 운영 모델, 풍부한 계약업체 풀, 그리고 유틸리티자 및 지방 자치단체와의 명확한 상업적 협력의 이점도 누리고 있습니다.

생물학적 처리 기술은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.3%로 확대될 것으로 예상되며, 동남아시아의 폐기물 에너지화 시장에서 가장 빠르게 성장하는 기술 부문이 될 전망입니다. 이 부문의 성장을 주도하고 있는 것은 주로 말레이시아와 인도네시아의 팜유 공장 폐수(POME) 프로젝트이며, 이 지역들은 폐기물 흐름이 집중되어 있어 메탄 회수가 상업적으로 의미 있는 사업이 되고 있습니다. 말레이시아와 인도네시아에서는 2025년에 8,040만 메트르톤의 원팜유를 생산했으며, 이는 전 세계 생산량의 83%에 해당합니다. 이를 통해 혐기성 소화 및 바이오가스 시스템을 위한 매우 대규모의 잔류물 기반이 뒷받침되고 있습니다. 그러나 2026년 초 시점에서 인도네시아의 팜유 공장 중 혐기성 소화 설비를 도입한 곳은 10% 미만에 불과했으며, 원료 확보 가능성은 높지만 도입 기반이 낮기 때문에 성장은 그 시점에서 시작되고 있습니다. 폐기물 유래 연료(RDF) 생산이나 기계생물학적 처리(MBT)와 같은 물리적 기술은 여전히 혼소 및 자원 회수 수단을 뒷받침하고 있지만, 동남아시아의 폐기물 에너지화 업계에서는 열처리 및 생물학적 처리에 이은 부차적인 위치에 머물러 있습니다.

2025년, 동남아시아의 폐기물 에너지화 시장 규모 중 56.4%를 도시 고형 폐기물이 차지했으며, 이에 따라 이 지역 전체에서 프로젝트 개발의 중심적인 위치를 유지했습니다. 이러한 위치는 도시 폐기물 수거 시스템과 정부가 지원하는 컨세션 모델 사이에 직접적인 연관성이 있음을 반영하고 있습니다. 인도네시아의 국가 프로그램은 2029년까지 34개 도시 및 30개 광역권을 대상으로 하루 3만 3,000톤의 폐기물을 처리할 계획이며, 이에 따라 향후 처리 시설의 주요 처리량 기반으로서 도시 쓰레기의 중요성이 더욱 커지고 있습니다. 또한 태국과 베트남에서는 산업단지 및 수출용 제조 구역에 대한 환경 규제가 강화됨에 따라 산업 폐기물의 비중도 높아지고 있습니다.

농업 및 농업 관련 산업에서 발생하는 잔여물은 2026년부터 2031년까지 연평균 성장률(CAGR) 13.8%로 증가할 것으로 예상되며, 동남아시아의 폐기물 에너지화 시장에서 가장 빠르게 성장하는 폐기물 유입원이 될 전망입니다. 가장 큰 비즈니스 기회는 팜유 산업에 있으며, 메탄을 풍부하게 함유한 대량의 잔여물이 여전히 충분히 활용되지 못하고 있습니다. 2025년 10월, 말레이시아의 바이오이코노미 코퍼레이션은 폴라리스 바이오사와 20곳 이상의 바이오 CNG 시설로 구성된 7억 링깃(1억 5,800만 달러 상당) 규모의 네트워크 구축에 관한 양해각서(MOU)를 체결했습니다. 이는 잔여물의 수익화에 대한 상업적 관심이 높아지고 있음을 보여주는 것입니다. 필리핀에서도 분산형 잔여물 전환이 시범적으로 시행되고 있으며, 라구나주에서 ‘바이오스페어(Biosfair)"시범 사업에서는 연간 1,200톤의 유기성 폐기물을 처리하고, 연간 25만 kWh의 전력을 생산할 예정입니다. 이러한 프로젝트들은 원료가 집중된 지역에서는 잔여물을 기반으로 한 시스템이 신속하게 확대될 수 있으며, 혼합 일반 폐기물 시스템에 비해 수거 물류가 간소하다는 점을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the southeast asia waste-to-Energy market size is expected to increase from USD 4.64 billion in 2025 to USD 5.22 billion in 2026 and reach USD 9.48 billion by 2031, growing at a CAGR of 12.65% over 2026-2031.

This report is Segmented by Technology (Physical, Thermal, Biological), Waste Type (MSW, Industrial, and More), Energy Output (Electricity, Heat and More), End-User (Utilities/IPPs, Industrial Captive, District Heating, Fuel Distributors), and Geography (Indonesia, Malaysia, Thailand, Singapore, Vietnam, Philippines, Rest of Southeast Asia). Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia Waste-to-Energy Market Trends and Insights

Waste Generation Pressure Outpaces Landfill Absorption Capacity

Indonesia generated 56.63 million tonnes of municipal solid waste in 2023, and only 39% of that volume was properly managed, which shows how far collection and treatment systems still lag the waste stream itself. The core issue is not only the rise in waste volumes, but the widening gap between collection, treatment, and final disposal capacity across large cities and second-tier urban centers. That gap is becoming more important because waste growth is no longer concentrated only in megacities, and smaller urban clusters are now large enough to support commercial treatment assets. This is why plant formats in the 200 to 500 tpd range are becoming more viable in parts of the region where collection networks cannot yet support very large centralized projects. These local conditions make imported large-plant models less transferable without changes in scale, logistics, and financing. As a result, the Southeast Asia waste-to-energy market is expanding from a narrow metropolitan solution into a wider municipal infrastructure category.

Government Incentives and PPP Frameworks Unlocking Financing

Indonesia's Presidential Regulation No. 109 of 2025 replaced the earlier dual tipping-fee and power-purchase structure with a single fixed tariff of USD 0.20/kWh under a 30-year power purchase agreement, which materially changed project bankability. The regulation also moved procurement into a more centralized framework, which reduced fragmentation between municipal decision-making and project execution. In Thailand, an Asian Development Bank-backed THB 16.6 billion package, equal to USD 521.5 million, for 12 industrial waste-to-energy plants showed how multilateral backing can unlock projects that had previously faced financing constraints. These policy steps matter because private capital moves faster when tariffs, waste delivery, and concession terms are defined early. They also favor sponsors that can move from financing to engineering to plant operations without depending on a long chain of counterparties. This is one of the clearest reasons the Southeast Asia waste-to-energy market is moving from scattered pilots toward larger and more repeatable project pipelines.

High Upfront Capex Strains Project Bankability Across the Region

Recent project announcements show that 1,000 tpd class plants in the region still require capital commitments in the hundreds of millions of dollars, which keeps financing barriers high for new entrants. Malaysia's Sungai Udang facility carries a project cost of RM660 million, equal to USD 149 million, for 1,056 tpd and 22 MW under a 34-year concession. Hanoi's Phase 2 expansion at Soc Son adds 1,600 tpd and carries an investment of VND 5,830 billion, equal to USD 239 million. Long concession terms help revenue visibility, but lenders remain cautious when tariffs do not adjust for inflation over the operating life of the asset. Pretreatment systems, emissions controls, and construction risk raise the entry cost even before a plant reaches stable utilization. This means the Southeast Asia waste-to-energy market still favors sponsors with stronger balance sheets, better contractor control, and access to sovereign or multilateral support.

Other drivers and restraints analyzed in the detailed report include:

- Renewable Energy and Sustainability Targets Raising Mandatory WtE Throughput

- Landfill Closure Mandates Creating Captive Feedstock for New Plants

- Feedstock Variability Imposes Hidden Technology Adaptation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal technology held 62.1% of the Southeast Asia waste-to-energy market share in 2025, which kept it as the dominant route for large urban treatment systems. That lead comes from the fit between grate-furnace incineration and high-throughput municipal waste, especially where project economics depend on continuous intake and firm power offtake. Hanoi's Soc Son facility was already processing 70% of the city's daily household waste when it was inaugurated in October 2025, which shows how well thermal systems can absorb large city waste streams. Thermal plants also benefit from more mature operating models, deeper contractor pools, and a clearer commercial interface with utilities and local authorities.

Biological technology is projected to expand at 14.3% CAGR from 2026 to 2031, making it the fastest-growing technology segment in the Southeast Asia waste-to-energy market. The segment is being driven mainly by palm oil mill effluent projects in Malaysia and Indonesia, where waste streams are concentrated and methane capture is commercially meaningful. Malaysia and Indonesia were expected to produce 80.4 million metric tonnes of crude palm oil in 2025, or 83% of global output, which supports a very large residue base for anaerobic digestion and biogas systems. Yet fewer than 10% of Indonesian palm oil mills had installed anaerobic digestion by early 2026, so growth is starting from a low installed base even though feedstock availability is high. Physical technologies such as refuse-derived fuel production and mechanical biological treatment still support co-firing and recovery pathways, but they remain secondary to thermal and biological routes in the Southeast Asia waste-to-energy industry.

Municipal solid waste accounted for 56.4% of the Southeast Asia waste-to-energy market size in 2025, which kept it at the center of project development across the region. This position reflects the direct link between city waste collection systems and government-backed concession models. Indonesia's national programme is targeting 34 cities and 30 agglomeration zones by 2029, with planned waste intake of 33,000 tpd, which reinforces municipal waste as the main volume base for future plants. Industrial waste is also gaining weight in Thailand and Vietnam as environmental compliance standards tighten in industrial parks and export manufacturing zones.

Agricultural and agro-industrial residues are projected to grow at 13.8% CAGR from 2026 to 2031, making them the fastest-growing waste stream in the Southeast Asia waste-to-energy market. The strongest opportunity sits in the palm oil economy, where large volumes of methane-rich residue remain underused. In October 2025, Malaysia's Bioeconomy Corporation signed an MOU with Polaris Bio for a RM700 million network, equal to USD 158 million, of more than 20 Bio-CNG facilities, which highlighted growing commercial interest in residue monetization. The Philippines is also testing decentralized residue conversion, and the Biosfair pilot in Laguna is set to process 1,200 tonnes of organic waste annually while generating 250,000 kWh per year. These projects show that residue-based systems can scale quickly where feedstock is concentrated, and collection logistics are simpler than in mixed municipal waste systems.

Complete Report Scope:

- By Technology

- Physical (Refuse-Derived Fuel, Mechanical Biological Treatment)

- Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc)

- Biological (Anaerobic Digestion, Fermentation)

- By Waste Type

- Municipal Solid Waste

- Industrial Waste

- Agricultural and Agro-industrial Residues

- Sewage Sludge

- Others (Commercial, Construction, Hazardous)

- By Energy Output

- Electricity

- Heat

- Combined Heat and Power (CHP)

- Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol)

- By End-user

- Utilities and IPPs

- Industrial Captive Plants

- District Heating Operators

- Transport Fuel Distributors

- By Geography

- Indonesia

- Malaysia

- Thailand

- Singapore

- Vietnam

- Philippines

- Rest of Southeast Asia

List of Companies Covered in this Report:

- Mitsubishi Heavy Industries Ltd

- Hitachi Zosen Corp

- Keppel Infrastructure Holdings

- Sembcorp Industries

- Veolia Environment SA

- China Everbright Environment Group

- China Jinjiang Environment

- Jiangsu Tianying Group

- Covanta Energy

- Babcock & Wilcox Volund

- MVV Energie AG

- Martin GmbH

- DP CleanTech

- Ramboll Group

- PT Yokogawa Indonesia

- Gulf Energy Development

- Earth Tech Environment

- Wastech Exponential

- Suez SA

- WTE International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing waste generation in fast-growing urban hubs

- 4.2.2 Renewable-energy & sustainability targets (net-zero, RE100)

- 4.2.3 Government incentives & PPP frameworks unlocking financing

- 4.2.4 Rising landfill-tipping fees and closure mandates

- 4.2.5 Carbon-credit monetisation via voluntary markets

- 4.3 Market Restraints

- 4.3.1 High upfront capex / long payback periods

- 4.3.2 Public opposition over dioxin & NOx emissions

- 4.3.3 Low-calorific, high-moisture feedstock variability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Physical (Refuse-Derived Fuel, Mechanical Biological Treatment)

- 5.1.2 Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc)

- 5.1.3 Biological (Anaerobic Digestion, Fermentation)

- 5.2 By Waste Type

- 5.2.1 Municipal Solid Waste

- 5.2.2 Industrial Waste

- 5.2.3 Agricultural and Agro-industrial Residues

- 5.2.4 Sewage Sludge

- 5.2.5 Others (Commercial, Construction, Hazardous)

- 5.3 By Energy Output

- 5.3.1 Electricity

- 5.3.2 Heat

- 5.3.3 Combined Heat and Power (CHP)

- 5.3.4 Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol)

- 5.4 By End-user

- 5.4.1 Utilities and IPPs

- 5.4.2 Industrial Captive Plants

- 5.4.3 District Heating Operators

- 5.4.4 Transport Fuel Distributors

- 5.5 By Geography

- 5.5.1 Indonesia

- 5.5.2 Malaysia

- 5.5.3 Thailand

- 5.5.4 Singapore

- 5.5.5 Vietnam

- 5.5.6 Philippines

- 5.5.7 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Mitsubishi Heavy Industries Ltd

- 6.4.2 Hitachi Zosen Corp

- 6.4.3 Keppel Infrastructure Holdings

- 6.4.4 Sembcorp Industries

- 6.4.5 Veolia Environment SA

- 6.4.6 China Everbright Environment Group

- 6.4.7 China Jinjiang Environment

- 6.4.8 Jiangsu Tianying Group

- 6.4.9 Covanta Energy

- 6.4.10 Babcock & Wilcox Volund

- 6.4.11 MVV Energie AG

- 6.4.12 Martin GmbH

- 6.4.13 DP CleanTech

- 6.4.14 Ramboll Group

- 6.4.15 PT Yokogawa Indonesia

- 6.4.16 Gulf Energy Development

- 6.4.17 Earth Tech Environment

- 6.4.18 Wastech Exponential

- 6.4.19 Suez SA

- 6.4.20 WTE International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment