|

시장보고서

상품코드

2073655

아시아태평양의 데이터센터 전력 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

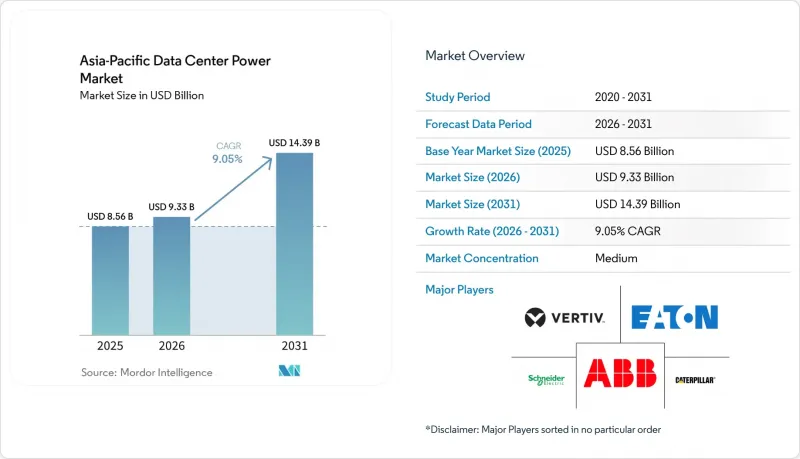

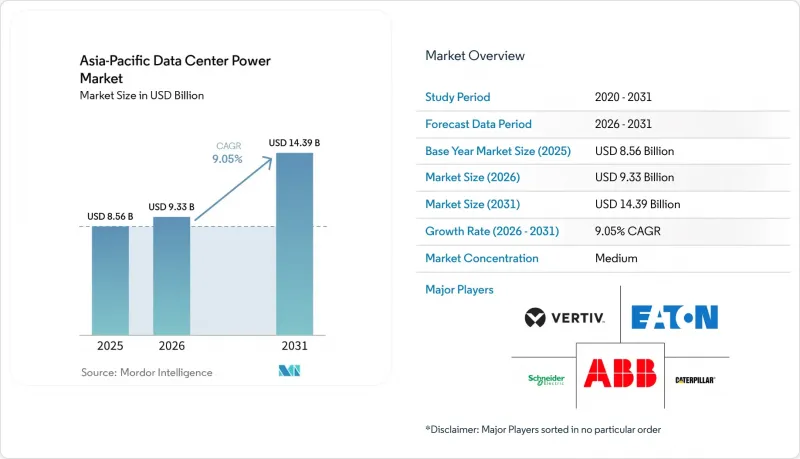

Mordor Intelligence에 의하면, 아시아태평양 데이터센터 전력 시장 규모는 2025년에 85억 6,000만 달러로 평가되었고 2026년 93억 3,000만 달러에서 2031년까지 143억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.05%를 나타낼 전망입니다.

본 보고서는 구성 요소(전기 솔루션 및 서비스), 데이터센터 유형(하이퍼스케일러/클라우드 서비스 제공업체, 코로케이션 제공업체 등), 데이터센터 규모(소규모 데이터센터, 중규모 데이터센터, 대규모 데이터센터 등), 티어 유형(Tier I 및 II, Tier III, Tier IV), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양 데이터센터 전력 시장 동향과 인사이트

하이퍼스케일 및 AI 주도형 메가 캠퍼스 구축

현재 AI 훈련 클러스터는 랙당 40-50 kW의 전력을 필요로 하고 있으며, 이는 기존 도입 사례의 5배 이상에 해당합니다. 이로 인해 배전 토폴로지와 이중화 방식에 대한 전면적인 재설계가 시급해졌습니다. 실리콘 카바이드(SiC)와 같은 광대역 갭 파워 반도체는 변환 손실을 줄이고 열적 안정성을 유지하기 위해, 새로운 홀에서는 액체 냉각이 표준화되고 있습니다(오크리지 국립연구소). 싱가포르의 Singtel사가 발표한 “Banyan Park II"와 같은 프로젝트에서는 향후 AI 부하 증가에 대비할 수 있도록 내진성이 뛰어난 버스웨이 및 랙 수준의 액체 매니폴드가 사양으로 정해져 있습니다. 이러한 시스템에는 드라이브스루 지원, 전력망의 과도 현상 완화, 그리고 발전기 시동을 수반하지 않는 보다 급격한 부하 단계 변화를 가능하게 하기 위한 축전지가 통합되어 있습니다. 임차인들이 AI 지원 용량을 요구함에 따라, 이러한 연쇄적인 영향으로 인해 코로케이션 시설 전체의 사양 수준이 높아지고 있습니다.

정부의 디지털 경제 및 데이터 주권에 관한 인센티브

중국과 인도의 정책에 따라 국내 데이터 상주가 의무화되어 있으며, 클라우드 제공업체는 현지 하이퍼스케일 캠퍼스를 운영하고 더 높은 가용성 수준을 충족하기 위해 배전 설비를 업그레이드해야 합니다. 싱가포르에서는 에퀴닉스(Equinix)와의 민관 공동 조사 프로그램을 통해 열대 기후의 운영 조건을 대상으로 한 지속 가능한 전력 프로토타입 개발에 400만 달러가 투자되고 있습니다. 아세안(ASEAN)은 2030년까지 데이터센터 수요의 30%를 충당할 수 있는 재생에너지의 통합을 장려하고 있습니다. 말레이시아와 베트남의 인센티브 제도에서는 부지 내에 태양광 발전 설비나 고효율 UPS를 도입한 시설에 대해 요금을 환급해 주고 있습니다. 규제에 따라 명확한 조달 일정이 수립됨에 따라 개폐 장치 및 에너지 저장 장치의 조달량이 증가하고 있으며, 이는 예측 가능한 공급망의 확장을 뒷받침하고 있습니다.

고효율 전력 시스템을 위한 초기 설비 투자

고성능 UPS나 실리콘 카바이드(SiC) 컨버터는 기존 장비에 비해 최대 40% 더 비싸기 때문에 재정 기반이 제한적인 중소규모 공급업체에게는 진입 장벽이 되고 있습니다. 액체 냉각 시스템을 도입하려면 공장에서 사전 제작된 버스바와 펌프 매니폴드가 필요하며, 이로 인해 설치 과정이 복잡해지고 리드타임이 늘어납니다. 평균 랙 부하가 여전히 8kW 전후에 머무르고 있는 신흥국에서는 사업자들이 고객 수요가 본격화될 때까지 업그레이드를 미루는 경우가 많습니다. “서비스형 에너지(EaaS)”계약 등의 자금 조달 메커니즘이 보급되기 시작하고 있지만, 그 도입 현황에는 편차가 있어 가장 효율적인 아키텍처의 단기적인 보급을 제한하고 있습니다.

부문별 분석

2025년, 아시아태평양의 데이터센터 전력 시장에서 UPS 시스템은 매출 점유율의 31.65%를 차지하며, 24시간 가동되는 디지털 서비스를 보호하는 데 있어 그 역할을 여실히 보여주었습니다. 리튬 이온 배터리와 실리콘카바이드(SiC) 파워트레인을 채택함으로써 온라인 효율이 96%를 초과했으며, 단가는 높아졌지만 운영 비용을 절감하고 있습니다. UPS와 배터리를 통합한 모듈 덕분에 설치 면적이 줄어들고 유지보수가 간소화됨에 따라, 구성 요소의 구성도 변화하고 있습니다. 연평균 성장률(CAGR) 10.3%로 가장 빠르게 성장하고 있는 하위 부문인 지능형 PDU에는 콘센트별 전력 측정 기능이 내장되어 있으며, 이 데이터는 AI 분석을 통해 워크로드 배치에 활용되어 유휴 전력 용량을 줄여줍니다. 발전기는 여전히 중요한 백업 수단으로서의 위상을 유지하고 있지만, 지속가능성을 중시하는 하이퍼스케일러들 사이에서는 연료전지 시제품이 시범 도입 사례로 주목받고 있습니다.

전력 가격 변동이라는 외부 압력으로 인해, 라이드스루 지원과 수요 요금 경감을 겸하는 배터리 에너지 저장 시스템의 도입이 가속화되고 있습니다. 개폐 장치의 기술 혁신은 아크 플래시 안전성과 현장 방문 횟수를 줄여주는 원격 진단에 중점을 두고 있습니다. 기술 인력이 부족하고 가동 시간의 허용 범위가 좁은 엣지 환경에서는 원격 전원 패널의 도입이 증가하고 있습니다. 아시아태평양의 데이터센터 전력 업계 전반에서 현대 전력 시스템의 복잡성이 증가하고 있음을 반영하여, 사업자가 OEM 제조업체에 디지털 트윈을 활용한 예측 유지보수를 위탁하는 사례가 늘어나면서 서비스 수익이 확대되고 있습니다.

코로케이션 사업자들은 기업 수요를 집약하고 규모의 경제를 활용함으로써, 2025년에는 아시아태평양 데이터센터 전력 시장의 53.85%를 차지했습니다. 이 회사의 비즈니스 모델은 모듈식 2-3MW 블록을 통해 전력 설계를 표준화하고, 건설 기간을 단축하는 대규모 멀티테넌트 홀을 뒷받침하고 있습니다. 한편, 하이퍼스케일 클라우드 제공업체는 소버린 클라우드 의무화로 인해 전 세계 플랫폼들이 현지 구축을 추진하고 있는 가운데, 연평균 성장률(CAGR) 10.05%로 성장하고 있습니다. 이러한 사이트에는 고밀도 AI 클러스터가 통합되어 있어, 기존의 코로케이션 레이아웃으로는 대응하기 어려운 칩 직결형 액체 냉각 및 전용 400 VAC 버스웨이가 필요합니다.

기업들은 하이브리드 아키텍처를 채택하여, 지연 시간에 민감한 워크로드를 On-Premise에서 유지하면서 코로케이션이나 하이퍼스케일 플랫폼으로부터 버스트 용량을 빌려 쓰고 있습니다. 5G 기지국 주변에서는 엣지 노드가 급증하고 있어, 대규모 시설과 설계 이념을 공유하면서도 콤팩트하면서도 신뢰성이 높은 전원 셸프가 요구되고 있습니다. 그 결과, 해당 벤더는 kW급 엣지 랙부터 150MW 규모의 하이퍼스케일 팜에 이르기까지 아우르는 포트폴리오를 구축했으며, 아시아태평양 데이터센터 전력 시장에서 부문 간 기술 이전을 촉진하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the asia-Pacific data center power market size was valued at USD 8.56 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 14.39 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031).

This report is Segmented by Component (Electrical Solutions and Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV) and by Country. The Market Forecasts are Provided in Terms of Value (USD)

Asia-Pacific Data Center Power Market Trends and Insights

Hyperscale & AI-led Mega-Campus Build-out

AI training clusters now demand 40-50 kW per rack, more than five times traditional deployments, forcing total redesigns of distribution topologies and redundancy schemes. Wide-bandgap power semiconductors such as silicon carbide reduce conversion losses, while liquid cooling becomes standard in new halls to maintain thermal stability, Oak Ridge National Laboratory. Projects like Singtel's Banyan Park II in Singapore specify seismic-resilient busways and rack-level liquid manifolds to future-proof against higher AI loads. These systems integrate battery storage for ride-through support, smoothing grid transients, and enabling more aggressive load step changes without generator starts. The cascading effect raises specification levels across colocation builds as tenants request AI-ready capacity.

Government Digital-Economy & Data-Sovereignty Incentives

Policies in China and India require domestic data residency, obliging cloud providers to commission local hyperscale campuses and upgrade power distribution for higher availability tiers. Singapore's public-private research program with Equinix funds USD 4 million in sustainable power prototypes targeting tropical operating conditions. ASEAN frameworks encourage renewable integration that could meet 30% of data-center demand by 2030. Incentive schemes in Malaysia and Vietnam grant tariff rebates for facilities that deploy on-site solar and high-efficiency UPS. As regulation sets clear procurement timelines, volume commitments for switchgear and energy storage rise, supporting predictable supply-chain scaling.

Up-front Capex for High-Efficiency Power Systems

Advanced UPS and silicon-carbide converters cost up to 40% more than legacy equipment, a hurdle for smaller providers with constrained balance sheets. Liquid-cooling integration demands factory-prefabricated busbar and pump manifolds, raising installation complexity and lead times. In emerging economies where average rack loads still hover near 8 kW, operators often delay upgrades until customer demand materializes. Financing mechanisms such as energy-as-a-service contracts are beginning to spread, but adoption remains uneven, limiting near-term penetration of the most efficient architectures.

Other drivers and restraints analyzed in the detailed report include:

- Cloud/5G Traffic Surge Elevating Power Density

- High Electricity Tariffs Boosting Demand for Efficient UPS & PDUs

- Grid & Land Constraints in Tier-1 APAC Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UPS systems held the largest 31.65% revenue share in 2025 within the Asia-Pacific data center power market, underscoring their role in safeguarding always-on digital services. Adoption of lithium-ion batteries and silicon-carbide power trains pushes online efficiency above 96%, trimming operating expenditures despite higher unit prices. The component mix is changing as integrated UPS-battery modules reduce footprint and simplify maintenance. Intelligent PDUs, the fastest-growing sub-segment with a 10.3% CAGR, embed per-outlet metering that feeds AI analytics for workload placement, reducing stranded power capacity. Generators retain critical backup status but fuel-cell prototypes are gaining pilot traction among sustainability-focused hyperscalers.

External pressures from electricity-price volatility accelerate the deployment of battery energy storage that doubles as ride-through support and demand-charge mitigation. Switchgear advances concentrate on arc-flash safety and remote diagnostics that lower truck rolls. Remote power panels rise in edge deployments where technicians are scarce and uptime tolerance is low. Service revenue grows as operators contract OEMs for predictive maintenance tied to digital twins, reflecting the rising complexity of modern power trains across the Asia-Pacific data center power industry.

Colocation operators commanded 53.85% of the Asia-Pacific data center power market in 2025 by aggregating enterprise demand and leveraging economies of scale. Their business model supports large multitenant halls where modular 2-3 MW blocks standardize power design and shorten build schedules. Hyperscale cloud providers, however, are expanding at 10.05% CAGR as sovereign-cloud mandates drive local build commitments from global platforms. These sites integrate high-density AI clusters, necessitating direct-to-chip liquid cooling and dedicated 400 VAC busways that traditional colocation layouts rarely accommodate.

Enterprises adopt hybrid architectures, retaining latency-sensitive workloads on-premises while renting burst capacity from colo and hyperscale platforms. Edge nodes proliferate near 5G towers, requiring compact yet highly reliable power shelves that share design DNA with large facilities. Consequently, solutions vendors tailor portfolios that span kilowatt-class edge racks to 150 MW hyperscale farms, reinforcing cross-segment technology transfer within the Asia-Pacific data center power market.

Complete Report Scope:

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Country

- Australia

- China

- India

- Indonesia

- Philippines

- Singapore

- Malaysia

- Japan

- New Zealand

- Other Asia-Pacific Countries

List of Companies Covered in this Report:

- ABB

- Schneider Electric

- Vertiv

- Eaton

- Huawei Digital Power

- Caterpillar

- Cummins

- Rolls-Royce Power Systems (MTU)

- Delta Electronics

- Legrand

- Mitsubishi Electric

- Socomec

- Piller Power Systems

- Rittal

- Kohler Power

- Cisco (DCIM and Smart-UPS integration)

- Fujitsu (facility services)

- AEG Power Solutions

- Tripp Lite

- Generac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale and AI-led mega-campus build-out

- 4.2.2 Government digital-economy and data-sovereignty incentives

- 4.2.3 Cloud/5G traffic surge elevating power density

- 4.2.4 High electricity tariffs boosting demand for efficient UPS and PDUs

- 4.2.5 Grid-connection delays driving onsite micro-grids

- 4.2.6 Corporate 100 %-renewable commitments (on-site solar and BESS)

- 4.3 Market Restraints

- 4.3.1 Up-front capex for high-efficiency power systems

- 4.3.2 Grid and land constraints in Tier-1 APAC hubs

- 4.3.3 Diesel-price volatility inflating generator OPEX

- 4.3.4 Skilled-labour gap for liquid-cooling power installs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Electrical Solutions

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.2.1 Diesel Generators

- 5.1.1.2.2 Gas Generators

- 5.1.1.2.3 Hydrogen Fuel-cell Generators

- 5.1.1.3 Power Distribution Units

- 5.1.1.4 Switchgear

- 5.1.1.5 Transfer Switches

- 5.1.1.6 Remote Power Panels

- 5.1.1.7 Energy-storage Systems

- 5.1.2 Service

- 5.1.2.1 Installation and Commissioning

- 5.1.2.2 Maintenance and Support

- 5.1.2.3 Training and Consulting

- 5.1.1 Electrical Solutions

- 5.2 By Data Center Type

- 5.2.1 Hyperscaler/Cloud Service Providers

- 5.2.2 Colocation Providers

- 5.2.3 Enterprise and Edge Data Center

- 5.3 By Data Center Size

- 5.3.1 Small Size Data Centers

- 5.3.2 Medium Size Data Centers

- 5.3.3 Large Size Data Centers

- 5.3.4 Massive Size Data Centers

- 5.3.5 Mega Size Data Centers

- 5.4 By Tier Level

- 5.4.1 Tier I and II

- 5.4.2 Tier III

- 5.4.3 Tier IV

- 5.5 By Country

- 5.5.1 Australia

- 5.5.2 China

- 5.5.3 India

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Singapore

- 5.5.7 Malaysia

- 5.5.8 Japan

- 5.5.9 New Zealand

- 5.5.10 Other Asia-Pacific Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB

- 6.4.2 Schneider Electric

- 6.4.3 Vertiv

- 6.4.4 Eaton

- 6.4.5 Huawei Digital Power

- 6.4.6 Caterpillar

- 6.4.7 Cummins

- 6.4.8 Rolls-Royce Power Systems (MTU)

- 6.4.9 Delta Electronics

- 6.4.10 Legrand

- 6.4.11 Mitsubishi Electric

- 6.4.12 Socomec

- 6.4.13 Piller Power Systems

- 6.4.14 Rittal

- 6.4.15 Kohler Power

- 6.4.16 Cisco (DCIM and Smart-UPS integration)

- 6.4.17 Fujitsu (facility services)

- 6.4.18 AEG Power Solutions

- 6.4.19 Tripp Lite

- 6.4.20 Generac

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment