|

시장보고서

상품코드

1907332

종이 포장 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

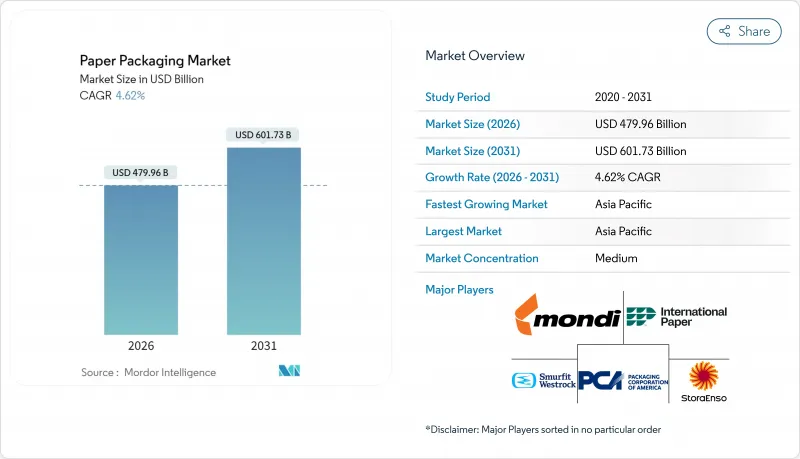

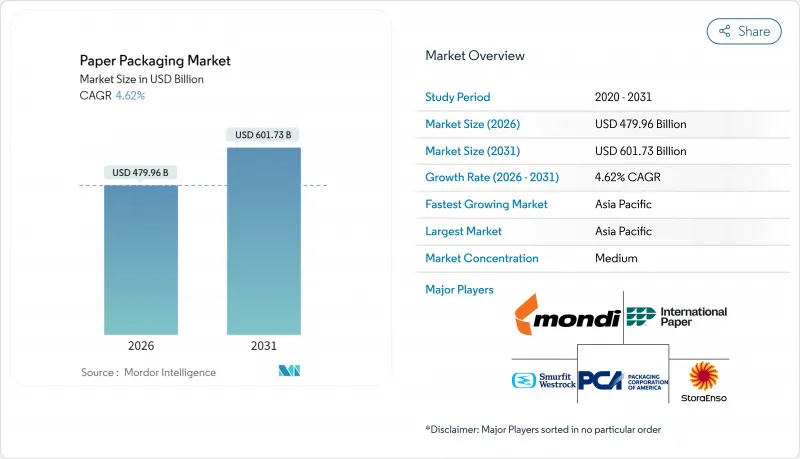

종이 포장 시장은 2025년에 4,588억 달러로 평가되었으며, 2026년 4,799억 6,000만 달러에서 2031년까지 6,017억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년) CAGR은 4.62%로 성장이 전망됩니다.

이 확대는 재생 가능한 기판을 장려하는 환경 규제, 온라인 소매의 지속적인 성장, 종이가 플라스틱과 수분 및 유분 저항성으로 경쟁할 수 있는 바이오베이스 배리어 코팅의 급속한 발전으로 추진되고 있습니다. 생산자는 다층 플라스틱에 비해 섬유 기반 재료의 컴플라이언스 비용을 줄이는 확장 생산자 책임(EPR) 수수료 시스템의 혜택을 누리고 있습니다. 동시에 나노셀룰로오스 기술에 대한 투자는 미국과 EU의 화학 물질 단계적 폐지에 부합하는 PFAS 프리 성능을 약속합니다. 디지털 인쇄와 소량 생산의 경제성에 의해 지원되는 공급측의 유연성으로 컨버터는 매력적인 이익률로 단납기 및 고도로 커스터마이즈된 캠페인에 대응할 수 있게 되어 종이 포장 시장의 대응 가능량이 확대되고 있습니다.

세계의 종이 포장 시장 동향 및 인사이트

배리어 코팅지판 솔루션의 개발이 프리미엄 용도를 견인

바이오폴리머나 나노셀룰로오스를 기반으로 한 고도의 방수, 방습 및 방유 배리어 코팅은 종이의 성능을 향상시키면서 재활용성을 유지하고 있습니다. 실험실 시험은 셀룰로오스 나노피브릴 코팅이 코팅되지 않은 판지와 비교하여 산소 투과율을 90% 이상 감소시키고 접힘 내구성을 두 배로 증가시키는 것으로 확인되었습니다. 미국 식품의약국(FDA)은 PFAS를 포함한 내유제가 식품 접촉 시장에서 철수되었음을 확인하고 수요는 보다 안전한 화학물질로 전환하고 있습니다. 유럽에서는 여러 가공업자가 강력한 수증기 차단성을 제공하고 퇴비화 기준을 충족하는 붕산 가교 폴리비닐알코올 코팅의 산업 생산을 급속히 진행하고 있습니다. 브랜드 소유자가 보존 기간을 손상시키지 않고 플라스틱 대체를 추구하는 동안, 프리미엄 배리어 코팅 판지는 즉석 식품, 냉동 식품, 퍼스널케어 선물 팩의 표준 사양이 되어 종이 포장 시장의 가치 성장을 가속하고 있습니다.

전자상거래용 골판지 수요 급증으로 생산 우선순위 재구축

세계의 온라인 소매는 실제 매장 판매를 능가하는 성장을 계속하고 있으며, 각 소포에는 자동화 처리에 견딜 수 있는 보호성 및 적재성을 갖춘 외장 포장이 요구됩니다. 골판지 케이스는 현재 EC 출하의 약 80%를 차지하는 것으로 추정되어 라스트마일 물류의 주력으로서 지위를 확고히 하고 있습니다. 중국과 인도를 중심으로 한 아시아의 거대 시장에서는 2024년에 소포수가 수십억개 증가해, 상자 공장의 확장 및 웹숍용 고속 디지털 인쇄 라인의 도입이 진행되고 있습니다. 생산 구성은 운송 비용을 줄이면서 압축 강도를 유지하는 경량 플루트 프로파일로 이행하고 있으며, 통합 생산 기업은 EC 수요의 견인을 추종하기 위해 그래픽 용지 등급보다 골판지 원지의 증산을 우선하고 있습니다. 이 수요 기반은 성숙 경제권 및 신흥 경제권 모두에서 종이 포장 시장의 꾸준한 양 성장을 지원합니다.

삼림 벌채 감시는 기존 공급망 구조에 문제를 일으킵니다.

EU 산림 파괴 규정에 따라 수입업체는 2025년 말까지 모든 목재 원료에 대해 구획 수준의 추적성 증명을 의무화합니다. EU용 특수 그레이드 펄프 수입의 60%를 차지하는 미국산 크래프트 펄프에는 제3자 기관에 의한 검증된 지리 좌표의 기재가 필수가 되었습니다. 위성 모니터링 및 관리망 감사의 도입은 조달 비용 증가와 배송 지연 위험을 수반합니다. 고급 데이터 시스템이 부족한 중소 제지 공장은 인증 삼림을 보유한 수직 통합형 대기업에 점유율을 빼앗겨 종이 포장 시장 내 경쟁 균형이 변할 수 있습니다. 시간이 지남에 따라 더 엄격한 원산지 규칙이 공급을 압박하고 수입 섬유에 의존하는 시장에서 이 분야의 성장 가능성을 억제할 수 있습니다.

부문 분석

2025년 시점에서 골판지 원지는 골판지 산업의 기반이 갖추어지고 있으며, 전자상거래 배송에 중심적인 역할을 하고 있기 때문에 종이 포장 시장에서 54.12%의 점유율을 차지했습니다. 반면, 카톤 보드는 섬유 등급 중 가장 높은 7.05%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 식품 및 퍼스널케어 제품의 슬리브 포장에 있어서의 고급품 침투를 반영해, 카톤 보드 용도의 종이 포장 시장 규모는 확대가 전망됩니다. 컨버터 각사는 휴면 중인 그래픽 용지 제조기를 고형 표백 황산 펄프(SBS)나 폴딩 박스용 판지(Folding Boxboard) 생산에 적합한 코팅 헤드로 개조하여 설비 가동률의 향상을 도모하고 있습니다. 접이식 상자용 판지는 고화질 디지털 인쇄와의 궁합이 좋고, 매장에서의 소구력을 높입니다. 또 분산 배리어성의 향상에 의해 냉장 식품 분야에 대한 진입이 가능하게 되었습니다. 동시에 골판지 원지 제조업체는 운송 중량 삭감을 위해 경량 크래프트 라이너에 대한 투자를 추진하여 지속가능성 향상을 도모하고 있습니다. 버진 및 재생재의 혼합 사용은 강도 대 중량비를 최적화하고 골판지 원지의 경쟁력을 유지합니다. 이에 따라 종이 포장 시장에서 주력 제품으로서의 지위를 확고한 것으로 하고 있습니다.

카톤 보드의 성장성에 따라 유럽과 북미에서는 급속한 생산 능력 확대를 위한 자본이 유입되고 있으며, 신규 설비의 가동량은 2026년까지 100만 톤을 넘을 전망입니다. 식품 접촉 인증 및 의약품 클린 룸 대응으로 특히 고형 표백 등급의 톤당 가치가 향상되고 있습니다. EU 여러 국가의 흑색 플라스틱 규제로 고급 과자와 화장품 포장이 백색 카톤 보드 형식으로 이동하여 수요를 더욱 밀어 올리고 있습니다. 나노클레이와 같은 성능 향상 첨가제는 재활용성을 손상시키지 않고 방습성을 제공하여 플라스틱 필름에 대한 의존도를 줄입니다. 소매 브랜드가 품질과 지속가능성을 전달하는 단일 소재 포장을 추구하는 동안, 판지는 종이 포장 시장에서 가장 큰 수혜자로 부상하고 있습니다.

골판지 상자는 수송, 산업 및 식료품 유통 분야에서 비교할 수 없는 보호 강도와 범용성으로 2025년 시점에서 종이 포장 시장의 61.48%를 차지했습니다. 그러나 접이식 카톤은 개인화된 그래픽, 빠른 계절 캠페인 대응, 소량 생산을 배경으로 전체 성장률을 넘는 5.12%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측되고 있습니다. 금형 추출기에 통합된 디지털 프린트 헤드는 전환 시간을 단축하고 비용이 많이 드는 인벤토리를 갖지 않고 대량 사용자 정의를 실현합니다. 고급 화장품, 영양 보조 식품, 식물성 식품은 모두 미적 유연성과 선반 밖으로 가능한 형식에서 접이식 판지를 선호 채용하고 있습니다.

골판지 제조업체는 내면 인쇄나 고채도 인쇄 기술로 브랜드 표시 영역을 확보하려고 대응하고 있습니다만, 접이식 카톤은 촉감 마무리나 엠보싱 가공에 있어서 우위성을 유지하고 있습니다. 가전 액세서리는 플라스틱 클램 쉘 포장에서 성형 섬유 인서트를 결합한 강화 카톤으로의 전환이 진행되어 지속가능성을 중시하는 소비자층을 획득하고 있습니다. 게다가 유연한 파우치로부터 착상을 얻은 획기적인 티어 스트립(파선) 개봉 기능에 의해 편리성이 한층 향상되고 있습니다. 이러한 디자인과 기술의 진보는 종이 포장 시장 전체의 꾸준한 점유율 확대를 지원하고 있습니다.

지역별 분석

아시아태평양은 2025년 47.62%의 수익 점유율로 종이 포장 시장을 견인해 2031년까지 연평균 복합 성장률(CAGR) 5.51%로 확대될 것으로 전망됩니다. 남아시아와 동남아시아에서는 급속한 도시화, 확대하는 중산계급 구매력, 대규모 식품 배달 생태계가 섬유 수요를 지원하고 있습니다. 지역 기업은 식림림과 자사 가공 시설을 결합한 비용 효율적인 통합 공장을 활용하여 수출 지향 고객을 위한 리드 타임을 단축하고 있습니다. 지방 정부는 에너지 절약 기계에 대한 관세 환급을 통해 지속 가능한 포장에 대한 투자를 장려하고 생산 능력 확대를 더욱 가속화하고 있습니다.

북미는 혁신의 핵심 지역으로 디지털 인쇄 기술의 보급을 추진하고 나노셀룰로오스의 파일럿 상업화를 주도하고 있습니다. 여러 주에서 강화되는 매립 규제는 호별 회수 가능한 포장재에 대한 수요를 높여 국내 컨테이너 보드 수요를 지원하고 있습니다. 미국은 풍부한 침엽수 자원으로 축적되어 수입고지(OCC)와 혼합하는 버진 펄프의 안정 공급이 확보되고 있습니다. 한편 유럽에서는 엄격한 재활용 목표와 확대 생산자 책임(EPR) 제도의 도입으로 설비의 지속적인 갱신을 촉진하는 예측 가능한 정책 환경이 형성되고 있습니다. 독일과 스칸디나비아의 공장에서는 화석 연료 보일러에서 바이오매스 보일러로의 전환이 진행되고 있으며, 고에너지 가격 하에서도 스코프 1 배출량을 삭감하고 비용 경쟁력을 높이고 있습니다.

라틴아메리카, 중동 및 아프리카는 현재 각각 약간의 점유율만을 차지하고 있지만, 두 지역 모두 세계 평균을 웃도는 성장을 기록하고 있습니다. 브라질 펄프 생산자는 상품 사이클의 영향을 완화하기 위해 하류 판지 사업에 통합하고 걸프 협력 회의(GCC) 회원국은 확장하는 전자상거래 허브를 수용하기 위해 골판지 생산 능력을 강화하고 있습니다. 아프리카에서는 수집 네트워크가 발달되지 않기 때문에 재생 섬유 공급이 방해되고 있지만, 국제 개발 프로그램은 파일럿 재료 회수 시설에 자금을 제공하고 미래의 순환 경제의 기초를 구축하고 있습니다. 이 지역 동향은 종이 포장 시장의 장기적인 탄력성을 지원하는 다양한 수요 기반을 강화하는 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 배리어 코트 종이판 솔루션 개발

- 전자상거래에 있어서 골판지 수요 증가

- 브랜드 오너의 단일 소재 포장으로의 이행

- 확대 생산자 책임(EPR)의 의무화

- 나노셀룰로오스 배리어 기술의 획기적인 진전

- 가공 공장에서 현장 디지털 인쇄의 경제성

- 시장 성장 억제요인

- 삼림 벌채 및 섬유 공급의 정사

- 변동이 심한 재생 섬유 가격

- PFAS '영구 화학물질'의 단계적 폐지 비용

- 신흥 시장에서 한정된 회수물류

- 업계 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 세계의 재생지 생산 통계

- 재생지-생산 수량

- 재생지-수입액 및 수량

- 재생지-수출액 및 수량

- 재생지 생산량-주요 생산국

- 카톤보드의 수출입 상황

- 수출(금액 및 수량)

- 수입(금액 및 수량)

제5장 시장 규모 및 성장 예측

- 등급별

- 판지 보드

- 고형 표백 황산 펄프(SBS)

- 무표백 황산 펄프(SUS)

- 접이식 판지(FBB)

- 코트 재생 판지(CRB)

- 무도공 재생 판지(URB)

- 기타 판지 등급

- 컨테이너 보드

- 화이트 톱 크래프트 라이너

- 기타 크래프트 라이너

- 화이트 톱 테스트 라이너

- 기타 테스트 라이너

- 세미 케미컬 프루팅

- 재생 플루트

- 판지 보드

- 제품별

- 접이식 판지

- 골판지 상자

- 기타 제품

- 최종 사용자 업계별

- 식품

- 음료

- 헬스케어

- 퍼스널케어

- 가정용품

- 전기 및 전자 기기

- 기타 최종 사용자 산업

- 포장 형태별

- 경질(골판지, 판지)

- 반경질(접이식 골판지 상자)

- 플렉서블지(소봉지, 포장지)

- 성형 섬유 및 펄프

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Graphic Packaging International, LLC

- Nippon Paper Industries Co. Ltd.

- Sonoco Products Company

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Sappi Limited

- Ilim Group

- Klabin SA

- Asia Pulp & Paper(APP)

제7장 시장 기회 및 장래 전망

AJY 26.01.22The paper packaging market was valued at USD 458.8 billion in 2025 and estimated to grow from USD 479.96 billion in 2026 to reach USD 601.73 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

This expansion is propelled by environmental regulations that reward recyclable substrates, the continued rise of online retail, and rapid progress in bio-based barrier coatings that let paper compete with plastics on moisture and grease resistance. Producers benefit from Extended Producer Responsibility fee schedules that lower compliance costs for fiber-based materials relative to multilayer plastics. At the same time, investments in nano-cellulose technology promise PFAS-free performance that aligns with looming U.S. and EU chemical phase-outs. Supply-side flexibility, powered by digital printing and smaller batch economics, is enabling converters to serve short-run, highly customized campaigns at attractive margins, expanding addressable volume for the paper packaging market.

Global Paper Packaging Market Trends and Insights

Development of Barrier-Coated Paperboard Solutions Drive Premium Applications

Advanced water-, oxygen-, and grease-barrier coatings based on bio-polymers and nano-cellulose are elevating paper's performance while preserving its recyclability. Laboratory trials show that cellulose nanofibril coatings can reduce oxygen transmission by more than 90% and double folding endurance compared with uncoated board. The U.S. Food & Drug Administration confirmed that grease-proofing agents containing PFAS have exited the food-contact market, shifting demand toward safer chemistries. In Europe, several converters are fast-tracking industrial runs of boric-acid-cross-linked poly(vinyl alcohol) coatings that deliver robust water vapor protection and meet compostability standards. As brand owners pursue plastic replacement without compromising shelf life, premium barrier-coated board is becoming the default for ready-to-eat foods, frozen meals, and personal-care gift packs, boosting value growth in the paper packaging market.

E-Commerce Corrugated Demand Surge Reshapes Production Priorities

Global online retail continues to outperform brick-and-mortar channels, and each parcel requires protective, stackable outer packaging that can withstand automated handling. Corrugated cases now account for an estimated 80% of e-commerce shipments, cementing their role as the workhorse for last-mile logistics. Asian mega-markets led by China and India added double-digit billions of parcels in 2024, prompting box-plant expansions and high-speed digital print lines dedicated to web-shop volumes. The production mix is shifting toward lightweight fluting profiles that cut freight costs yet retain compression strength, and integrated producers are prioritizing incremental containerboard tonnage over graphic paper grades to keep pace with e-commerce pull-through. This demand foundation underpins steady volume growth for the paper packaging market in both mature and emerging economies.

Deforestation Scrutiny Challenges Traditional Supply-Chain Structures

The EU Deforestation Regulation obliges importers to demonstrate plot-level traceability for all wood-based inputs by the end of 2025. U.S. Kraft pulp, representing 60% of EU specialty-grade imports, must now carry geo-coordinates verified by third parties. Implementing satellite monitoring and chain-of-custody audits raises procurement costs and risks of shipment delays. Smaller mills lacking sophisticated data systems may cede share to vertically integrated majors with certified forests, altering competitive balances within the paper packaging market. Over time, tighter provenance rules could squeeze supply and curb the sector's growth potential in markets that rely on imported fiber.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Migration Toward Mono-Material Packaging Architectures

- Extended Producer Responsibility Mandates Accelerate Market Transformation

- Volatile Recycled-Fiber Pricing Creates Margin Compression Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerboard held a 54.12% paper packaging market share in 2025, supported by deep corrugated infrastructure and its central role in e-commerce shipping. Meanwhile, cartonboard is registering a 7.05% CAGR, the fastest among fiber grades. The paper packaging market size for cartonboard applications is projected to rise, reflecting premium penetration in food and personal-care sleeves. Converters are refitting idle graphic-paper machines with coating heads suited to Solid Bleached Sulfate and Folding Boxboard production, improving asset utilization. Folding Boxboard's compatibility with high-definition digital print elevates shelf appeal, while dispersion-barrier upgrades enable chilled-food entry. At the same time, containerboard producers are investing in lightweight kraftliner to cut shipping mass, enhancing sustainability credentials. Virgin-recycled blends optimize strength-to-weight ratios and keep containerboard competitive, ensuring it remains the volume backbone of the paper packaging market.

Cartonboard's growth profile attracts capital for rapid European and North American capacity expansions, with start-ups exceeding 1 million tons by 2026. Food-contact certification and pharmaceutical clean-room compliance boost value per ton, particularly for solid-bleached grades. Regulatory bans on black plastics in several EU countries redirect premium confectionery and cosmetic packs to white cartonboard formats, lifting demand further. Performance-enhancing additives such as nano-clays deliver moisture barriers without compromising recyclability, reducing reliance on plastic films. As retail brands demand mono-material packs that convey quality and sustainability, cartonboard emerges as the prime beneficiary within the paper packaging market.

Corrugated boxes occupied 61.48% of the paper packaging market in 2025 owing to their unmatched protective strength and versatility across shipping, industrial, and grocery channels. Folding cartons, however, are forecast to outpace overall growth, expanding at a 5.12% CAGR on the back of personalized graphics, quick-response seasonal campaigns, and smaller lot sizes. Digital printheads integrated into die-cutters reduce changeover times, paving the way for mass-customization without costly inventories. Premium beauty, nutraceuticals, and plant-based foods all favor folding cartons for their aesthetic flexibility and shelf-ready formats.

Corrugated producers respond with inside-print and high-color capabilities to keep hold of branding real estate, but folding cartons maintain an edge in tactile finishes and embossing. Consumer-electronics accessories increasingly shift from plastic clamshells to reinforced cartons married with molded-fiber inserts, capturing sustainability-minded shoppers. Novel tear-strip opening features borrowed from flexible pouches further boost convenience. These design and technology advances underpin steady share migration within the broader paper packaging market.

The Paper Packaging Market Report is Segmented by Grade (Cartonboard [Solid Bleached Sulphate, and More], and Containerboard [White-Top Kraftliner, and More]), Product (Folding Cartons, Corrugated Boxes, and More), End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, and More), Packaging Format (Rigid, Semi-Rigid, Flexible, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the paper packaging market with a 47.62% revenue share in 2025 and is projected to record a 5.51% CAGR to 2031. Rapid urbanization, expanding middle-class purchasing power, and large-scale food-delivery ecosystems underpin fiber demand in South and Southeast Asia. Regional players leverage cost-efficient integrated mills that pair plantation forests with in-house converting, shortening lead times for export-oriented customers. Local governments incentivize sustainable-pack investments through duty rebates on energy-efficient machinery, further accelerating capacity additions.

North America remains an innovation nucleus, driving digital-print adoption and spearheading nano-cellulose pilot commercialization. Tightening landfill legislation in several states spurs demand for curbside-recyclable packs, bolstering domestic containerboard offtake. The United States also benefits from abundant softwood resources, ensuring steady virgin-fiber availability to blend with imported OCC. Meanwhile, Europe's stringent recyclability targets and EPR rollouts create a predictable policy environment that favors continuous equipment upgrades. German and Scandinavian mills transition from fossil to biomass boilers, reducing Scope 1 emissions and sharpening cost competitiveness despite high energy prices.

Latin America and the Middle East and Africa collectively hold modest shares today, yet both regions register above-global average growth. Brazilian pulp producers integrate downstream into cartonboard to mitigate commodity cycles, while Gulf Cooperation Council economies add corrugated capacity to serve expanding e-commerce hubs. Africa's underdeveloped collection network hinders recycled-fiber supply, but international development programs are funding pilot materials-recovery facilities, laying groundwork for future circularity. Collectively, these regional trajectories reinforce the diversified demand base that supports the long-term resilience of the paper packaging market.

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Graphic Packaging International, LLC

- Nippon Paper Industries Co. Ltd.

- Sonoco Products Company

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Sappi Limited

- Ilim Group

- Klabin S.A.

- Asia Pulp & Paper (APP)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development of barrier-coated paperboard solutions

- 4.2.2 Rise in e-commerce corrugated demand

- 4.2.3 Brand-owner shift toward mono-material packs

- 4.2.4 Extended Producer Responsibility (EPR) mandates

- 4.2.5 Nano-cellulose barrier breakthroughs

- 4.2.6 Converting-plant on-site digital printing economics

- 4.3 Market Restraints

- 4.3.1 Deforestation and fibre-supply scrutiny

- 4.3.2 Volatile recycled-fibre pricing

- 4.3.3 PFAS "forever-chemicals" phase-out costs

- 4.3.4 Limited recovery logistics in emerging markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Global Recovered Paper Production Statistics

- 4.8.1 Recovered Paper - Production Quantity

- 4.8.2 Recovered Paper - Import Value and Quantity

- 4.8.3 Recovered Paper - Export Value and Quantity

- 4.8.4 Recovered Paper Production - Leading Countries

- 4.9 Cartonboard EXIM Scenario

- 4.9.1 Exports (Value and Volume)

- 4.9.2 Imports (Value and Volume)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Cartonboard

- 5.1.1.1 Solid Bleached Sulphate (SBS)

- 5.1.1.2 Solid Unbleached Sulphate (SUS)

- 5.1.1.3 Folding Boxboard (FBB)

- 5.1.1.4 Coated Recycled Board (CRB)

- 5.1.1.5 Uncoated Recycled Board (URB)

- 5.1.1.6 Other Cartonboard Grades

- 5.1.2 Containerboard

- 5.1.2.1 White-top Kraftliner

- 5.1.2.2 Other Kraftliners

- 5.1.2.3 White-top Testliner

- 5.1.2.4 Other Testliners

- 5.1.2.5 Semi-chemical Fluting

- 5.1.2.6 Recycled Fluting

- 5.1.1 Cartonboard

- 5.2 By Product

- 5.2.1 Folding Cartons

- 5.2.2 Corrugated Boxes

- 5.2.3 Other Products

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Personal Care

- 5.3.5 Household Care

- 5.3.6 Electrical and Electronics

- 5.3.7 Other End-User Industries

- 5.4 By Packaging Format

- 5.4.1 Rigid (Corrugated, Solid Board)

- 5.4.2 Semi-rigid (Folding Cartons)

- 5.4.3 Flexible Paper (Sachets, Wraps)

- 5.4.4 Molded Fibre and Pulp

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mondi plc

- 6.4.4 Packaging Corporation of America

- 6.4.5 Stora Enso Oyj

- 6.4.6 Graphic Packaging International, LLC

- 6.4.7 Nippon Paper Industries Co. Ltd.

- 6.4.8 Sonoco Products Company

- 6.4.9 Oji Holdings Corporation

- 6.4.10 Georgia-Pacific LLC

- 6.4.11 Nine Dragons Paper Holdings

- 6.4.12 Lee & Man Paper Manufacturing

- 6.4.13 Sappi Limited

- 6.4.14 Ilim Group

- 6.4.15 Klabin S.A.

- 6.4.16 Asia Pulp & Paper (APP)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment