|

시장보고서

상품코드

1964918

배터리 불필요화가 가져올 새로운 거대 시장(2026-2046년)Battery Elimination Creates Large New Markets 2026-2046 |

||||||

요약

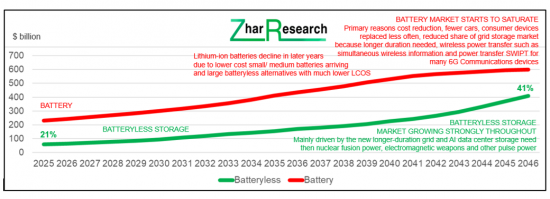

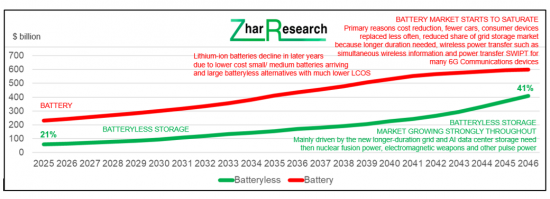

2026년부터 2046년까지 전기에너지 저장 시장 규모는 3배 이상 확대될 것이며, 특히 배터리가 필요 없는 저장 분야는 4,100억 달러라는 거대한 규모로 급성장하여 현재 20%에서 약 40%의 점유율로 확대될 것으로 예상됩니다.

향후 20년 이내에 배터리 시장은 포화상태에 도달할 것으로 예상됩니다. 치열한 가격 경쟁, 최대 응용 분야인 전기자동차 시장의 성장 둔화, 전력망, 데이터센터, 마이크로그리드의 장기 저장, 전자기 무기 및 핵융합 발전의 펄스 전력 응용 등 중요하고 급성장하는 새로운 시장의 수요를 충족시키지 못하는 것이 그 배경입니다. 배터리가 필요 없는 축전 기술은 안전성이 높고, 수명이 크게 연장되며, 성장 분야에서 더 낮은 축전 균등화 비용(LCOS)을 실현할 수 있습니다. 이미 양수 발전만 해도 연간 500억 달러가 넘는 시장 규모를 보이고 있습니다.

또한 수십억 달러 규모의 신흥 시장으로 에너지 저장이 전혀 필요 없는 새로운 시스템이 부상하고 있습니다. 예를 들어, 계획 중인 6세대 통신(6G) 2단계에서는 클라이언트 장비에 백스캐터 기술을 채택하고 있습니다. 또한, 웨어러블 기기는 멀티 모드 에너지 수확을 채택하고 있습니다.

배터리 불필요 기술 시장을 조사했으며, 시장 배경, 배터리의 과제와 배터리 불필요화 동향, 배터리 vs 비배터리 에너지 저장장치의 시장 규모 추정과 예측, 주요 배터리 불필요 기술 개요, 연구개발 동향, 주요 기업의 대응, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

캡션 : 에너지 저장장치 시장(배터리식 vs 비배터리식) 출처 : Zhar Research 보고서 "Battery Elimination Creates Large New Markets 2026-2046"

목차

제1장 요약 및 결론

- 보고서의 목적과 범위

- 조사 방법

- 주요 결론

- 배터리의 현재 과제와 대체품이 채택되는 이유

- 배터리를 사용하지 않는 선택 : 저장소 폐지 또는 대체 저장소 사용

- 센서에서 GW 전원까지 배터리 폐지 추세

- 배터리가 필요 없는 저장장치를 통한 드롭인 교체 이상의 배터리 제거 옵션 제공

- 인포그램 : 그리드 LDES에서 벗어나는 13가지 탈출 경로

- 인포그램 : 데이터센터 마이크로그리드 및 유사 LDES에서 벗어나는 방법

- 배터리 불필요 저장장치 툴킷·SWOT 평가

- 로드맵

- 시장 예측

제2장 소개

- 개요

- 배터리의 한계

- 리튬이온 배터리 화재가 지속적으로 발생하고 있는 상황

- 전동화, 배터리 채용, 배터리 불필요화라는 메가 트렌드

- 보관에 미치는 영향

- 배터리식 및 무전원식 고정식 저장기술의 지속시간과 전력의 관계 및 미래 동향

- 배터리 점유율 감소 전망

- LDES의 필요성과 설계 원칙

제3장 배터리 탈피 경로 : 백스캐터(EAS, RFID, 6G SWIPT), 배터리 제거 회로, 기타 전자기기 옵션, LDES 탈피 경로

- 개요

- 배터리가 필요 없는 저장장치를 통한 드롭인 교체 이상의 배터리 제거 옵션 제공

- 저장을 줄이거나 없애는 전략

- 조합 가능한 자가 구동형, 배터리가 필요 없는 디바이스를 실현하는 것

- 백스캐터 통신·SWOT

- 전자 물품 모니터링(EAS), 패시브 RFID 등

- 6G 통신 및 IoT를 위한 SWIPT AmBC 및 CD-ZED

- SWOT 및 기타 진행상황

- 배터리를 최소화하는 회로 설계

- 배터리 불필요 회로(BEC) : 드론 및 전기자동차에의 적용

- 간헐적 전력에 대응하는 전자 기술 : BFree

- V2G, V2H, V2V, 태양광 패널에서 직접 충전을 통한 배터리 절감 및 폐지

- 수요 관리 : 저장할 필요가 없는 태양광 담수화 장치

- 에너지원 관리의 발전

- 사양 조정을 통한 배터리 불필요화

- 배터리 없는 드론(센서, IoT용)

- 배터리 불필요 카메라

- 배터리가 필요 없는 에너지 수확

- 개요 및 주요 에너지 수확 기술 비교

- 수확 시스템의 요소

- 음향을 포함한 기계식 에너지 회수에 대한 자세한 내용

- 전자기에너지 회수에 대한 자세한 내용

- 유연한 층류 에너지 수확의 중요성

- 장시간 에너지 저장(LDES)에서 벗어나는 경로

- 두 인포그램의 일반적 상황

- 세계 예시 : 덴마크, 싱가포르, 중국, 미국, 미국

- 풍력·태양광 설비 이용률과 LDES 수요의 관계

- 2LDES 회피 기술 연구

- 가정 에너지 관리 시스템 연구

제4장 양수 발전(PHES, APHES)

- 기존 PHES 개요

- 연구 발전과 가능성 전망

- 세계의 프로젝트와 의도

- 경제성

- 정책제안

- PHES 성능 평가

- PHES의 SWOT 분석

- 산악 지형을 필요로 하지 않는 첨단 양수 발전

- APHES 개요·SWOT

- 광산부지 활용

- 지하 가압 방식(Quidnet Energy)

- 중수 이용 방식(RheEnergise)

- 해수/염수 이용(Cavern Energy, Sizable Energy 등)

- 해저 저장(StEnSea, Ocean Grazer)

- 수중 에너지 저장의 SWOT 분석

- 하이브리드 기술

- 최신 연구

제5장 고체중력 에너지 저장(SGES)

- 개요 및 연구 진행 상황

- 일반

- 3단계 운영 프로세스

- 3가지 구조 형식

- 양수 발전과의 비교

- 기본 원리

- SGES의 SWOT 분석

- SGES 성능 평가

- CAPEX 과제

- 운영 비용 문제

- 모래 활용 가능성

- 케이블이 아닌 유압 피스톤 방식

- 기타 SGES 연구

제6장 압축 공기 에너지 저장(CAES)

- 개요 및 연구 진행 상황

- 시장 확대와 모방 기술

- 시장 포지셔닝

- SWOT 평가 및 매개변수 비교

- CAES 기술 옵션

- 열역학

- 등용적 또는 등압 저장

- 단열

- CAES 프로젝트, 서브시스템 제조업체, 목표

- 개요 : 가장 큰 프로젝트는 중국에서

- Siemens Energy Germany

- MAN Energy Solutions Germany

- CAES 보관 시간 및 방전 기간 연장

- 영국과 EU에서의 연구

- CAES 기업 프로파일

- ALCAES Switzerland

- APEX CAES USA

- Augwind Energy Israel

- Keep Energy Systems UK formerly Cheesecake

- Corre Energy Netherlands

- Huaneng Group China

- Hydrostor Canada

- LiGE Pty South Africa

- Storelectric UK

- Terrastor Energy Corporation USA

제7장 전력 지연 공급형 열에너지 저장(ETES)

- 개요 및 연구 진행 상황

- 실패의 교훈 : Siemens Gamesa, Azelio, Steisdal, Lumenion

- 열기관 접근법의 발전 : Echogen USA

- 초고온 + 태양전지 방식

- Antora USA

- Fourth Power USA

- 열과 전력을 동시에 공급하는 플랜트

- MGA Thermal Australia

- Malta Inc Germany

제8장 수소 및 기타 화학 중간체를 이용한 LDES

- 개요 및 연구 진행 상황

- LDES의 수소 저장 파라미터 평가

- LDES의 수소, 메탄, 암모니아 : SWOT 평가

- 실제 프로젝트 예시

- H2ES는 계절별 저장 용도에만 적합하며, 추후에 필요한 것으로 나타났습니다.

- 운영 데이터 부족으로 인해 다른 결론을 나타내는 계산 결과도 존재합니다.

- LDES 시스템에서의 수소 저장 후보 기술

제9장 정전기 저장 : 슈퍼커패시터, 유사 커패시터, 리튬이온 커패시터, 기타 BSH

- 커패시터와 그 변형의 위치

- 선택 범위 : 커패시터에서 슈퍼커패시터, 배터리까지

- 연구 파이프라인 : 퓨어 슈퍼커패시터

- 연구 파이프라인 : 하이브리드 접근법

- 연구 파이프라인 : 의사 커패시터

- 슈퍼커패시터와 그 파생상품의 실제 및 잠재적 주요 용도

- 개요

- 항공기·항공우주

- 전기자동차 : AGV, 자재운반차, 자동차, 트럭, 버스, 전차, 전철, 기차

- 그리드, 마이크로그리드, 피크 컷, 재생에너지, 무정전 전원공급장치

- 의료·웨어러블

- 군사 : 레이저포, 레일건, 펄스 선형가속무기, 레이더, 트럭, 기타

- 전력 및 신호전자, 데이터센터 즉각적인 복구

- 용접

- 슈퍼커패시터 기업 분석(103개사)

- 리튬 이온 커패시터 및 기타 배터리 슈퍼커패시터 하이브리드 BSH 스토리지

- 정의 및 선택

- 시장 포지셔닝

- 에너지 밀도 비교

- 인포그램 : 시장 니즈와 기술 비교

- 연구 분석 및 제안

- SWOT 분석 및 로드맵

Summary

From 2026-2046, the electrical energy storage market will more than triple but the battery-less storage part will surge to a massive $410 billion - about 40% from 20% today. Time to look beyond batteries. On cue we have the new Zhar Research 546-page report, "Battery Elimination Creates Large New Markets 2026-2046" detailing this massive opportunity.

Within 20 years the battery value market will saturate due to vicious price wars, the largest application - electric cars - levelling and the inability of batteries to perform to the requirements of important new, fast-growing markets. These include months of grid, data center and microgrid storage, and pulsing new electromagnetic weapons and nuclear fusion power. Increasingly, batteryless storage is safer, with much longer life and able to provide lower Levelised Cost of Storage LCOS in the growth applications. Already, pumped hydro alone sells at over $50 billion yearly.

Another emerging multi-billion-dollar market will be for new systems that eliminate energy storage completely, such as planned 6G Communications Phase Two using backscatter for client devices. Wearables adopt multi-mode energy harvesting. Uniquely, this report appraises the commercial opportunity for all this with 133 company batteryless activity profiles.

The Executive Summary and Conclusions (58 pages) is sufficient for those with limited time. Here are the basics, methodology, key conclusions, technology comparisons, ongoing battery limitations, emerging large batteryless applications, 12 SWOT appraisals of the toolkit and 35 forecasts as tables and graphs with explanation. The Introduction (36 pages) details energy fundamentals, ongoing battery limitations. Understand why batteries will retain the dominant share of energy storage value markets 2026-2046 but lose share rapidly. Grasp emerging applications that batteries poorly address such as coping with long intermittency of wind and solar power everywhere. See the performance parameters of current batteryless solutions against batteries.

The rest of the report presents a through investigation of escape routes from batteries and sometimes from all energy storage. Specific batteryless technologies are detailed including research advances through 2025-6. The 78 pages of Chapter 3 closely examine "Escape routes from batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, other electronics options, LDES escape routes". Understand increasing deployment of escape routes from batteries and energy storage generally and the heroic future plans. The largest deployment of electronics in numbers is passive RFID tags and their subset anti-theft tags, none with energy storage. Next, their backscatter principle will be applied to 6G Communications client devices such as internet of things IOT tags also in tens of billions of units. See how the intermittency of wind and solar power can be sometimes tolerated and other times reduced without storage.

Chapter 4. Pumped hydro: conventional PHES and advanced APHES (74 pages) presents what is already selling at over $50 billion yearly, the improvements ahead including avoiding the need for mountainsides and the use of seawater. Realise that this takes the batteryless opportunity beyond massive grid storage to smaller applications. See the activities and intentions of key companies involved and 2025-6 research papers.

Chapter 5. Solid gravity energy storage SGES (37 pages) involves lifting weights instead of water as an improvement on grid batteries. Invented in Europe, it is most energetically pursued in China, initially as many huge buildings providing hours of grid storage but potentially even seasonal. See latest research and structures and the ongoing work on variants, including company profiles of use in mines in Europe and Australia.

Chapter 6. Compressed air energy storage CAES has 64 pages because there are ten companies profiled and widespread use worldwide mainly in huge underground caverns for hours of duration and potentially months (beyond batteries). So far, CAES is the strongest pumped hydro competitor. Contrast Chapter 7. Thermal energy storage for delayed electricity ETES where only four companies can be profiled and lessons of a number of exits are presented. Some new proponents have pivoted to combined heat and power or to thermovoltaic versions with white heat. Understand one large commercial version of ETES in Alaska using heat pumps.

Chapter 8. Hydrogen and other chemical intermediary LDES explains how use of intermediary chemical production and then converting it all back to electricity is very inefficient but hydrogen is more attractive than other gases for this. Enthusiasm for the Hydrogen Economy meets serious challenges of safety, leaking through everything and indirectly causing global warming. Use in salt caverns is strongly advocated by the Royal Society in the UK and many other eminent bodies because it can delay the most GWh, they say even seasonally. However, large H2ES projects are not being funded beyond China on hydrogen generally with electricity-to-electricity as a back story. See the small microgrid application in the USA using overground tanks for 24-hour duration and future plans.

Primary author and CEO of Zhar Research Dr Peter Harrop advises, "From all this it is clear that batteries are losing the extremes of grid storage and pulse/ fast charge-discharge applications so the report ends with the latter toolkit - essentially supercapacitors and their variants - in detail."

Chapter 9. "Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH" is the longest chapter at 118 pages because 103 companies are profiled plus a deep dive into the strongly emerging needs including massive banks pulsing nuclear fusion power. Sections cover aircraft and aerospace; electric vehicles: AGV, material handling, car, truck, bus, tram, train; grid, microgrid, peak shaving, renewable energy, uninterrupted power supplies, medical and wearables. Importantly see military: laser cannon, railgun, pulsed linear accelerator weapon, radar, trucks, other pulse-power electronics, data center instant emergency power, welding, pulse metal forming. Since most of the big applications emerge late in the 2026-2046 timeframe, the forecasts only take this to around $14 billion. Add a minor part of the regular capacitor business of around $70 billion at that time. However, there is considerable upside potential on these forecasts.

The new Zhar Research 548-page report, "Battery Elimination Creates Large New Markets 2026-2046" is your essential source of opportunities and latest research in this exciting emerging business serving the future - from nuclear fusion power to AI data centers, smart grids and microgrids.

CAPTION: Energy storage device market battery vs batteryless $ billion 2025-2046. Source: Zhar Research report, "Battery Elimination Creates Large New Markets 2026-2046".

Table of Contents

1. Executive summary and conclusions

- 1.1 Purpose and scope of this report

- 1.2 Methodology of this analysis

- 1.3 Primary conclusions

- 1.4 Battery current challenges and why alternatives are being adopted

- 1.4.1 General situation in electronics and electrical engineering

- 1.4.2 Lithium-ion battery fires are ongoing emitting toxic gas

- 1.4.3 Energy storage decision tree with battery-free examples

- 1.4.4 Battery emerging challenges 2026-2046

- 1.4.5 Battery challenges for 6G Communications and IoT and action arising 2026-2046

- 1.5 Battery-free options: eliminating storage or using alternative storage 2026-2046

- 1.6 Battery elimination trend from sensors to GW power

- 1.7 Battery elimination options beyond drop-in replacement by battery-less storage devices

- 1.7.1 Electronics, telecommunication, electrical engineering

- 1.7.2 To the rescue: WPT, WIET, SWIPT evolution to 2046

- 1.7.3 Evolution of wireless electronic devices needing no on-board energy storage 1980-2046

- 1.7.4 13 primary energy harvesting technologies compared

- 1.8 Infogram: 13 escape routes from grid LDES 2026-2046

- 1.9 Infogram: Escape routes from data center microgrid and similar LDES 2026-2046

- 1.10 Battery-less storage device toolkit 2025-2045 with SWOT appraisals

- 1.10.1 Options by size

- 1.10.2 Example: Lithium-ion capacitor LIC market positioning by energy density spectrum

- 1.10.3 Long duration energy storage LDES toolkit for grids, microgrids, 6G base stations, data centers 2026-2046

- 1.10.4 Possible scenario: stationary storage batteries vs alternatives TWh cumulative 2026-2046

- 1.10.5 Duration hours vs power delivered by project and 12 technologies in 2026

- 1.10.6 System strategies to achieve less or no storage: combine and compromise

- 1.10.7 Enablers of self-powered, battery-free devices that can be combined

- 1.10.6 12 SWOT appraisals of the battery-less device toolkit

- 1.11 Roadmaps 2026-2046

- 1.12 Market forecasts 2026-2046 in 35 lines

- 1.12.1 Energy storage device market battery vs batteryless $ billion 2025-2046

- 1.12.2 Battery-less storage for electricity-to-electricity $ billion 2025-2046 in 11 lines

- 1.12.3 Battery-less storage for pulse and fastest response $ billion 2025-2046 in 4 lines

- 1.12.4 LDES market in 9 technology categories $ billion 2026-2046 table, graphs, explanation

- 1.12.5 Total LDES value market % in three size categories 2026-2046 table, graph, explanation

- 1.12.6 Regional share of LDES value market % in four regions 2026-2046 table, graph, explanation

- 1.12.7 Market for seven types of equipment fitting battery-free storage $ billion 2025-2046

2. Introduction

- 2.1 Overview

- 2.2 Battery limitations

- 2.3 How lithium-ion battery fires are ongoing

- 2.4 Megatrends of electrification, battery adoption and battery elimination

- 2.5 Implications for storage 2026 - 2046

- 2.6 Duration vs power of many battery and batteryless stationary storage technologies deployed and deploying in 2025 showing future trends

- 2.7 How batteries will lose share 2026-2046

- 2.8 LDES need and design principles

- 2.8.1 Energy fundamentals

- 2.8.2 Racing into renewables with rapid cost reduction: 2025 statistics and trends

- 2.8.3 Solar winning and the intermittency challenge

- 2.8.4 Adoption of LDES of increasing duration driven by increased wind/solar percentage and cost reduction

- 2.8.5 LDES definitions and needs

- 2.8.6 LDES metrics

- 2.8.7 LDES projects in 2025-6 showing leading technology subsets

- 2.8.8 LDES impediments, alternatives and investment climate

- 2.8.9 LDES toolkit

- 2.8.10 Latest independent assessments of performance by technology

- 2.8.11 Leading reports on LDES 2026-2046

- 2.8.12 Example: Installed and committed stationary storage projects 2026 showing many battery and battery-less options competing

3. Escape routes from batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, other electronics options, LDES escape routes

- 3.1 Overview

- 3.1.1 Battery elimination options beyond drop-in replacement by battery-less storage devices

- 3.1.2 Strategies to achieve less or no storage

- 3.1.3 Enablers of self-powered, battery-free devices that can be combined

- 3.2 Backscatter with SWOT

- 3.2.1 Electronic Article Surveillance EAS , passive RFID and beyond

- 3.2.2 SWIPT AmBC and CD-ZED for 6G Communications and IOT

- 3.2.3 SWOT and 34 other advances in

- 3.3 Circuit design to minimise batteries

- 3.3.1 Battery elimination circuits BEC in drones and electric cars

- 3.3.2 Intermittency tolerant electronics: BFree

- 3.4 Battery reduction and elimination by V2G, V2H, V2V and vehicle charging directly from solar panels

- 3.5 Demand management: storage-free solar desalinators

- 3.6 Source management advances

- 3.7 Specification compromise eliminates batteries

- 3.7.1 Battery-free drones as sensors and IOT

- 3.7.2 Battery-free cameras

- 3.8 Energy harvesting eliminating batteries

- 3.8.1 Overview and 13 primary energy harvesting technologies compared

- 3.8.2 Elements of a harvesting system

- 3.8.3 Mechanical harvesting including acoustic in detail

- 3.8.4 Harvesting of electromagnetic energy in detail

- 3.8.5 Importance of flexible laminar energy harvesting 2026-2046

- 3.9 Escape routes from Long Duration Energy Storage LDES

- 3.9.1 General situation with two infograms

- 3.9.2 Examples across the world: Denmark, Singapore, China, USA

- 3.9.3 Capacity factor of wind, solar and options that need little or no LDES

- 3.9.4 Extensive 2025 research on LDES escape routes

- 3.9.5 Research in 2025 on Home Energy Management Systems coping with

4. Pumped hydro: conventional PHES and advanced APHES

- 4.1 Conventional PHES overview

- 4.1.1 Three options

- 4.1.2 History, environmental, timescales, potential sites, DOE appraisal

- 4.1.3 Site-limited primarily due environmental concerns not number of appropriate topologies

- 4.1.4 Problem analysis, actions to reduce PHES emissions, ugliness, water use, cost

- 4.2 Research advances and view of potential through 2025

- 4.3 Projects and intentions across the world

- 4.3.1 Geographical

- 4.3.2 Large pumped hydro schemes worldwide

- 4.4 Economics

- 4.5 Policy recommendations

- 4.6 Parameter appraisal of conventional pumped hydro PHES

- 4.7 SWOT appraisal of conventional pumped hydro PHES

- 4.8 Advanced pumped hydro does not need mountains

- 4.8.1 APHES overview with SWOT

- 4.8.2 Using mining sites including research advances through 2025-6

- 4.8.3 Pressurised underground: Quidnet Energy USA

- 4.8.4 Using heavier water up mere hills: RheEnergise UK

- 4.8.5 Using seawater or other brine: Cavern Energy, Sizable Energy, others, SWOT

- 4.8.6 StEnSea Germany, Ocean Grazer Netherlands

- 4.8.7 SWOT appraisal of underwater energy storage for LDES

- 4.8.8 Hybrid technologies: research advances in 2024 and 2025

- 4.8.9 Research advances in 2024 and 2025

5. Solid gravity energy storage SGES

- 5.1 Overview including research in 2025

- 5.1.1 General

- 5.1.2 Three stages of operation

- 5.1.3 Three geometries

- 5.1.4 Pumped hydro gravity storage compared to the three SGES options

- 5.1.5 Basics

- 5.1.6 SWOT appraisal of solid gravity storage SGES for LDES

- 5.1.7 Parameter appraisal of solid gravity energy storage SGES for LDES

- 5.1.8 CAPEX challenge

- 5.1.9 Challenge of ongoing expenses

- 5.1.10 Possibility of pumping sand

- 5.1.11 Hydraulic piston lift instead of cable: 2025 modelling

- 5.1.12 Appraisal of other SGES research through 2025

- 5.2 ARES USA

- 5.3 Energy Vault Switzerland, USA and China, India licensees

- 5.4 Gravitricity

- 5.5 Green Gravity Australia

- 5.6 SinkFloatSolutions France

6. Compressed air energy storage CAES

- 6.1 Overview including research advances announced in 2025

- 6.1.1 Basics

- 6.1.2 Research advances in 2025

- 6.2 Undersupply attracts clones

- 6.3 Market positioning of CAES

- 6.4 SWOT appraisal and parameter comparison of CAES for LDES

- 6.5 CAES technology options

- 6.5.1 Thermodynamic

- 6.4.2 Isochoric or isobaric storage

- 6.4.3 Adiabatic choice of cooling is winning

- 6.6 CAES projects, subsystem manufacturers, objectives, research 2025 onwards

- 6.6.1 Overview: largest projects are in China

- 6.6.2 Siemens Energy Germany

- 6.6.3 MAN Energy Solutions Germany

- 6.6.4 Increasing the CAES storage time and discharge duration

- 6.6.5 Research in UK and European Union 2025 onwards

- 6.7 Profiles of CAES company progress with Zhar Research appraisals

- 6.7.1 ALCAES Switzerland

- 6.7.2 APEX CAES USA

- 6.7.3 Augwind Energy Israel

- 6.7.4 Keep Energy Systems UK formerly Cheesecake

- 6.7.5 Corre Energy Netherlands

- 6.7.6 Huaneng Group China

- 6.7.7 Hydrostor Canada

- 6.7.8 LiGE Pty South Africa

- 6.7.9 Storelectric UK

- 6.7.10 Terrastor Energy Corporation USA

7. Thermal energy storage for delayed electricity ETES

- 7.1 Overview and research advances in 2025

- 7.2 Research advances in 2025 and 2024

- 7.3 Lessons of failure: Siemens Gamesa, Azelio, Steisdal, Lumenion

- 7.4 The heat engine approach proceeds: Echogen USA

- 7.5 Use of extreme temperatures and photovoltaic conversion

- 7.5.1 Antora USA

- 7.5.2 Fourth Power USA

- 7.6 Marketing delayed heat and electricity from one plant

- 7.6.1 Overview

- 7.6.2 MGA Thermal Australia

- 7.6.3 Malta Inc Germany

8. Hydrogen and other chemical intermediary LDES

- 8.1 Overview with research progress in 2025-6

- 8.1.1 Overview

- 8.1.2 Sweet spot for chemical intermediary LDES but safety issues

- 8.1.3 Mainstream research through 2025-6

- 8.1.4 Research dreaming of niches through 2025-6

- 8.1.5 Research on complex mechanisms for hydrogen loss

- 8.1.6 Research on hydrogen leakage causing global warming

- 8.1.7 Examples of hydrogen storage advances 2025-6

- 8.2 Parameter appraisal of hydrogen storage for LDES

- 8.3 SWOT appraisal of hydrogen, methane, ammonia for LDES

- 8.4 The small number of actual projects

- 8.4.1 Calistoga Resiliency Centre USA 48-hour microgrid

- 8.4.2 Ulm University microgrid trial Germany 2025-2027

- 8.4.3 China plans in 2025 and 2026

- 8.5 Calculations showing H2ES best only for seasonal storage, needed later

- 8.6 Calculations with other conclusions partly due to lack of operating data

- 8.7 Candidate technologies for hydrogen storage within LDES systems

9. Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH

- 9.1 The place of capacitors and their variants

- 9.2 Spectrum of choice - capacitor to supercapacitor to battery

- 9.3 Research pipeline: pure supercapacitors

- 9.4 Research pipeline: hybrid approaches

- 9.5 Research pipeline: pseudocapacitors

- 9.6 Actual and potential major applications of supercapacitors and their derivatives

- 9.6.1 Overview

- 9.6.2 Aircraft and aerospace

- 9.6.3 Electric vehicles: AGV, material handling, car, truck, bus, tram, train

- 9.6.4 Grid, microgrid, peak shaving, renewable energy and uninterrupted power supplies

- 9.6.5 Medical and wearables

- 9.6.6 Military: Laser cannon, railgun, pulsed linear accelerator weapon, radar, trucks, other

- 9.6.7 Power and signal electronics, data center instant recovery

- 9.6.8 Welding

- 9.7 103 supercapacitor companies assessed in 10 columns

- 9.8 Lithium-ion capacitors and other battery-supercapacitor hybrid BSH storage

- 9.8.1 Definitions and choices

- 9.8.2 BSH market positioning and choices and LIC market positioning by energy density spectrum

- 9.8.3 Infograms: the most impactful market needs, comparative solutions, 13 conclusions

- 9.8.4 Research analysis and recommendations 2025-2045

- 9.8.5 Two SWOT appraisals and roadmap 2025-2045