|

시장보고서

상품코드

1740985

V2G(Vehicle to Grid) 기술 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Vehicle-to-Grid (V2G) Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

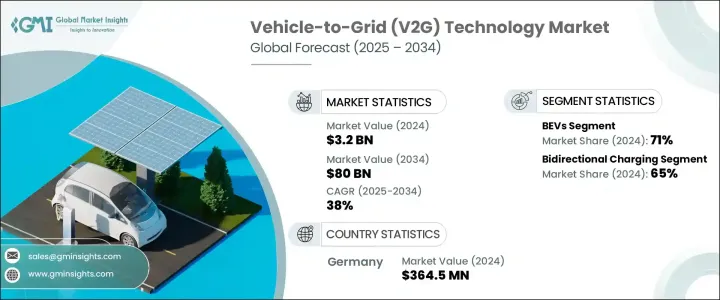

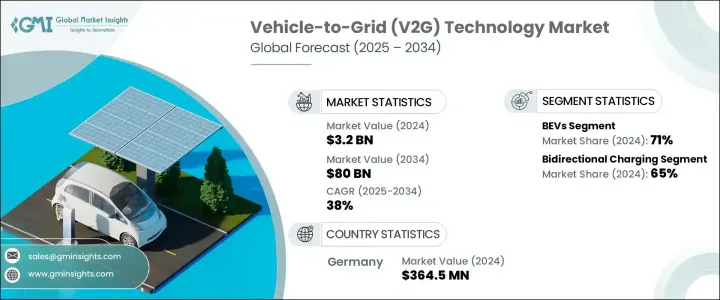

세계의 V2G(Vehicle to Grid) 기술 시장은 2024년에는 32억 달러로 평가되었으며 CAGR 38%을 나타내 2034년에는 800억 달러에 이를 것으로 추정됩니다.

이는 전기자동차 도입이 가속화되고, 스마트 그리드 시스템에 대한 투자가 증가하고 있으며, 저탄소 인프라를 추진하는 세계 기후 목표에 추진되고 있기 때문입니다. 세계가 보다 깨끗한 에너지 솔루션으로 향하는 동안, V2G 기술은 미래의 에너지 전망의 중요한 기둥이 되고 있습니다. 전기차가 주류가 되고 재생가능에너지의 통합이 급무가 되고 있는 가운데, V2G 플랫폼은 에너지의 유연성을 실현하는 중요한 수단으로 자리매김하고 있습니다.

자동차 및 에너지 분야의 기업은 피크 부하 관리를 지원하고 전력 공급을 안정화시키고 화석 연료에 대한 의존을 최소화하는 V2G 시스템의 상업화에 적극적으로 임하고 있습니다. 분산형 에너지 시스템에 대한 동향은 현대 에너지·에코시스템에서 V2G의 역할을 더욱 증대시켜 EV 소유자, 전력회사, 테크놀로지 프로바이더 모두에게 새로운 수익원을 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 32억 달러 |

| 예측 금액 | 800억 달러 |

| CAGR | 38% |

각국 정부는 양방향 충전 네트워크를 지원함으로써 국가전략을 국제적인 기후 변화 목표와 정합시켜 EV가 에너지 소비자나 에너지 공급자로서 그리드와 상호작용할 수 있도록 하고 있습니다. 그리드 자산으로 활용하여 재생 가능 에너지의 변동을 관리하며, 피크 수요의 압력을 완화합니다. 이러한 차량은 축전된 전력을 방전하여 그리드 회복력에 기여하며 화석 연료 발전에 대한 의존성을 최소화합니다. 등의 고급 기능을 갖춘 플랫폼을 구축하고 가치 창조를 뒷받침하고 있습니다. 일부 지역에서는 정부의 자금 지원, 인센티브, 인프라 정비로 표준 EV 충전 시스템의 V2G 대응으로의 전환이 가속화되고 있습니다.

배터리 전기자동차(BEV)는 2024년 차종별 시장 점유율로 약 71%를 차지했으며, CAGR 38.3%를 나타내 선두를 유지할 것으로 예측되고 있습니다. BEV는 대중 교통 및 라스트 원 마일 딜리버리와 같은 상업용 차량 및 도시 이동성 프로그램에 널리 통합되어 있습니다.

V2G(Vehicle to Grid) 기술 시장의 양방향 충전 분야는 2024년에는 65%의 점유율을 차지했으며, 2034년까지의 CAGR은 37.7%를 나타낼 것으로 예측되고 있습니다. 필요에 따라 전력을 되돌릴 수 있습니다. 전력 회사와 차량 운행 회사는 잉여 재생 가능 에너지를 저장하고 수요 피크시에 방출함으로써 송전망의 효율을 최적화하고 에너지 비용을 절감할 수 있기 때문에 이러한 시스템을 우선하고 있습니다.

독일의 V2G(Vehicle to Grid) 기술 시장은 2024년에 39%의 점유율을 차지했으며, 3억 6,450만 달러를 창출했습니다. 에너지 전환과 전화를 지원하는 독일의 연방 정부의 이니셔티브와, 송전망 근대화에의 다액의 투자가, V2G 인프라의 스케일 업을 가속시키고 있습니다.

세계 주요 자동차 제조업체와 에너지 기업은 도시 중심부, 공업지대, 플리트허브에서 V2G 플랫폼을 적극적으로 시험·도입하고 있습니다. Energy 등이 있습니다. 대기업 V2G 기업은 보다 효율적이고 확장 가능한 양방향 충전 기술을 개발하기 위해 RandD에 많은 투자를 실시했습니다. 파일럿 프로젝트와 대규모 배포를 가속화하고 있습니다. 많은 기업은 그리드 최적화, AI를 활용한 부하 관리, 에너지 시장 통합 등 소프트웨어의 진보에 주력하여 수익을 극대화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 충전 인프라 제공업체

- 그리드 오퍼레이터

- V2G 서비스 제공업체

- 기술 공급자

- 최종 용도

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- V2G 도입을 지원하는 정부 규제와 재정적 인센티브

- 세계에서 전기자동차의 보급이 진행

- 도시화와 산업화의 진전

- V2G 기술의 지속적인 기술 진보

- 업계의 잠재적 위험 및 과제

- 기존 충전 인프라 업그레이드에 따른 고비용

- 표준화된 충전 인프라의 부족

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정·예측 : 차량별(2021-2034년)

- 주요 동향

- BEV

- PHEV

- FCV

제6장 시장 추정·예측 : 충전별(2021-2034년)

- 주요 동향

- 단방향 충전

- 양방향 충전

제7장 시장 추정·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 스마트 미터

- EVSE

- 홈 에너지 관리

- 소프트웨어 솔루션

제8장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 국내

- 상업

제9장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- ABB

- AC Propulsion

- Boulder Electric Vehicle

- Denso Corporation

- Edison International

- EnerDel

- Engie Group

- Fermata Energy

- Groupe Renault

- Hitachi

- Honda Motor

- Indra

- Mitsubishi Motors Corporation

- Nissan Motor Corporation

- NRG Energy

- Nuvve Corporation

- OVO Energy

- PG&E Corporation

- Toyota Shokki

- Wallbox

The Global Vehicle-To-Grid Technology Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 38% to reach USD 80 billion by 2034, driven by the accelerating adoption of electric vehicles, rising investment in smart grid systems, and global climate goals pushing for low-carbon infrastructure. As the world moves toward cleaner energy solutions, V2G technologies are becoming a key pillar of the future energy landscape. With electric vehicles becoming mainstream and renewable energy integration gaining urgency, V2G platforms are positioned as critical enablers of energy flexibility.

Companies across the automotive and energy sectors are working aggressively to commercialize V2G systems that can support peak load management, stabilize power supplies, and minimize dependence on fossil fuels. Growing urbanization, government incentives, technological innovations, and the increasing need for energy storage solutions are creating a fertile environment for the expansion of V2G networks. The trend toward decentralized energy systems is further amplifying the role of V2G in modern energy ecosystems, creating new revenue streams for EV owners, utilities, and technology providers alike. As countries intensify efforts to cut transportation emissions, V2G is seen as a key strategy for aligning national energy agendas with global climate targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $80 Billion |

| CAGR | 38% |

Governments are aligning national strategies with international climate goals by supporting bidirectional charging networks, allowing EVs to interact with the grid as both energy consumers and energy providers. Utilities leverage EVs as grid assets to manage renewable energy variability and ease peak demand pressures. V2G-enabled EV fleets are increasingly used in cities and industrial areas to replace conventional power sources during high-demand periods. These vehicles contribute to grid resilience by discharging stored electricity, which minimizes reliance on fossil-fueled generation. Technology providers are building platforms with advanced features like predictive energy usage, real-time grid communication, and energy trading capabilities to boost value creation. In several regions, government funding, incentives, and infrastructure upgrades are accelerating the conversion of standard EV charging systems into V2G-capable ones.

Battery electric vehicles (BEVs) dominated the market by vehicle type in 2024, capturing about 71% share, and are forecasted to maintain their lead with a CAGR of 38.3%. Their ability to support bidirectional energy flows and zero-emission operation makes them highly compatible with V2G systems. BEVs are widely integrated into commercial fleets and urban mobility programs, including public transportation and last-mile delivery. Their expanding availability, coupled with supportive policies, is boosting their presence in the V2G ecosystem.

The bidirectional charging segment in the vehicle-to-grid (V2G) technology market held a 65% share in 2024 and is expected to grow at a CAGR of 37.7% through 2034. These chargers allow energy to move in both directions, enabling EVs to not only charge from the grid but also return power when needed. Utilities and fleet operators prioritize these systems for their ability to store surplus renewable energy and release it during demand peaks, optimizing grid efficiency and reducing energy costs.

The Germany Vehicle-To-Grid (V2G) Technology Market held a 39% share in 2024, generating USD 364.5 million. The country's leadership stems from its deep-rooted expertise in automotive manufacturing, extensive EV deployment programs, and a well-developed electric grid capable of supporting bidirectional energy flow. Germany's federal initiatives supporting energy transition and electrification, combined with significant investments in grid modernization, are accelerating the scale-up of V2G infrastructure.

Major automakers and energy companies worldwide are actively testing and implementing V2G platforms in urban centers, industrial zones, and fleet hubs. Key players in the Global Vehicle-To-Grid (V2G) Technology Market include ABB, Mitsubishi Motors, NRG Energy, Denso, Hitachi, AC Propulsion, Nissan Motor, Nuvve, Honda Motor, and OVO Energy. To strengthen their footprint, major V2G players are investing heavily in RandD to develop more efficient and scalable bidirectional charging technologies. They are forming partnerships with automotive manufacturers and utility companies to accelerate pilot projects and large-scale deployments. Many firms focus on software advancements, including grid optimization, AI-driven load management, and energy market integration to maximize returns.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Charging infrastructure providers

- 3.2.2 Grid operators

- 3.2.3 V2G service providers

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Supportive government regulations and financial incentives for V2G deployment

- 3.9.1.2 Growing adoption of electric vehicles across the globe

- 3.9.1.3 Rising urbanization and industrialization

- 3.9.1.4 Ongoing technological advancements in V2G technology

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost associated with upgrading existing charging infrastructure

- 3.9.2.2 Lack of standardized charging infrastructure

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 BEVs

- 5.3 PHEVs

- 5.4 FCVs

Chapter 6 Market Estimates & Forecast, By Charging, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Unidirectional charging

- 6.3 Bidirectional charging

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Smart meters

- 7.3 Electric vehicle supply equipment (EVSE)

- 7.4 Home energy management

- 7.5 Software solutions

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Domestic

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 AC Propulsion

- 10.3 Boulder Electric Vehicle

- 10.4 Denso Corporation

- 10.5 Edison International

- 10.6 EnerDel

- 10.7 Engie Group

- 10.8 Fermata Energy

- 10.9 Groupe Renault

- 10.10 Hitachi

- 10.11 Honda Motor

- 10.12 Indra

- 10.13 Mitsubishi Motors Corporation

- 10.14 Nissan Motor Corporation

- 10.15 NRG Energy

- 10.16 Nuvve Corporation

- 10.17 OVO Energy

- 10.18 PG&E Corporation

- 10.19 Toyota Shokki

- 10.20 Wallbox