|

시장보고서

상품코드

1667129

주전원용 발전용 왕복 엔진 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Prime Power Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

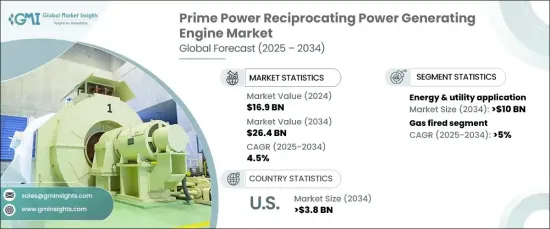

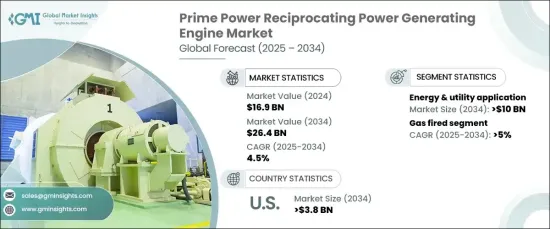

세계의 주전원용 발전용 왕복 엔진 시장 규모는 2024년 169억 달러로 평가되었고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.5%로 성장할 것으로 예측됩니다.

이러한 성장의 주요 요인은 산업, 건강 관리, 데이터센터, 비전화 기지 등 다양한 분야에서 안정적인 일정 전력에 대한 요구가 증가하고 있다는 것입니다. 이 엔진은 효율성, 수명 및 큰 전력 부하를 처리하는 능력을 높이 평가하며 발전 용도로 선호됩니다.

에너지 및 유틸리티 부문이 시장을 독점하고 2034년까지 100억 달러의 매출이 예상됩니다. 이 엔진은 단일 사이클에서 50%, 결합 사이클에서 최대 70%의 놀라운 전기 효율을 달성할 수 있기 때문에 원동기로서 지지를 모으고 있습니다. 인프라에 대한 투자가 확대되고 정부 주도의 전동화 구상이 계속 확대되고 있는 가운데 이러한 엔진에 대한 수요는 증가하고 시장 확대를 더욱 뒷받침할 것으로 보입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 169억 달러 |

| 예측 금액 | 264억 달러 |

| CAGR | 4.5% |

시장의 가스 동력 부문은 2034년까지 연평균 복합 성장률(CAGR)은 5%를 나타낼 것으로 예측됩니다. 이는 엔진 성능과 효율을 향상시키는 기술의 발전과 더불어 엄격한 환경 규제를 준수할 필요성이 증가하고 있기 때문입니다. 신재생에너지원을 중시하는 세계의 고조도 가스연마 엔진 수요촉진에 큰 역할을 하고 있습니다. 가스 연소 엔진은 높은 변환 효율, 최적화된 요소, 효율적인 연소, 낮은 유지보수 등의 이점을 제공합니다. 이러한 특성은 다양한 산업에서 이러한 엔진이 널리 채택되는 원인이 되었습니다.

미국 주전원용 발전용 왕복 엔진 시장은 2034년까지 38억 달러를 창출할 것으로 예측됩니다. 이 성장의 요인은 무정전 전력에 대한 요구 증가와 비정상적인 기상으로 인한 전력 중단의 빈도 증가입니다. 전력 수요가 증가함에 따라 기존 전력망에 부담이 되고 있기 때문에 신뢰할 수 있는 백업 전력 솔루션을 제공하는 이러한 엔진의 중요성이 부각되고 있습니다. 또한 데이터센터와 같은 중요한 시설에서 백업 전원 공급 장치 수요가 증가함에 따라 이러한 엔진의 채택을 촉진하고 있습니다. 신뢰할 수 있는 전원의 필요성에 대한 의식이 높아짐에 따라 시장 성장 전망을 더욱 높일 수 있습니다.

산업계와 정부가 에너지 효율과 지속가능성 확보에 중점을 두고 있는 가운데 주전원용 발전용 왕복 엔진 수요는 상승 기조를 계속할 것으로 예상되며, 증가하는 세계의 에너지 수요를 충족시키는 데 중요한 역할을 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 시장 추계·예측 파라미터

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 전략적 전망

- 혁신과 지속가능성의 전망

제5장 시장 규모와 예측 : 연료 유형별(2021-2034년)

- 주요 동향

- 가스 연소

- 디젤 연소

- 이중 연료

- 기타

제6장 시장 규모와 예측 : 정격 출력별(2021-2034년)

- 주요 동향

- 0.5 MW-1 MW

- 1 MW-2 MW 이상

- 2 MW-3.5 MW 이상

- 3.5 MW-5 MW 이상

- 5 MW-7.5 MW 이상

- 7.5 MW 이상

제7장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 산업용

- CHP

- 에너지 및 유틸리티

- 매립지 및 바이오가스

- 기타

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 이탈리아

- 스페인

- 네덜란드

- 덴마크

- 노르웨이

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 태국

- 싱가포르

- 인도네시아

- 말레이시아

- 중동 및 아프리카

- UAE

- 사우디아라비아

- 카타르

- 오만

- 쿠웨이트

- 이란

- 이집트

- 터키

- 요르단

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

- 페루

제9장 기업 프로파일

- AB Volvo Penta

- Caterpillar

- Cummins

- Deere &Company

- DEUTZ AG

- Kirloskar

- KUBOTA Corporation

- MITSUBISHI HEAVY INDUSTRIES

- Perkins Engines Company

- Rehlko

- Rolls-Royce

- Sulzer

- Wartsila

- YANMAR HOLDINGS

- Yuchai International

The Global Prime Power Reciprocating Power Generating Engines Market was valued at USD 16.9 billion in 2024 and is projected to grow at a CAGR of 4.5% during 2025-2034. This growth is primarily driven by the increasing need for reliable, constant power across several sectors, including industries, healthcare, data centers, and off-grid locations. These engines are highly regarded for their efficiency, longevity, and capacity to handle substantial power loads, making them a favored choice in power generation applications.

The energy and utility sector is expected to dominate the market, with revenues generating USD 10 billion by 2034. These engines are gaining traction as prime movers due to their ability to achieve impressive electrical efficiencies-over 50% in a single cycle and up to 70% in combined cycles. As investments in infrastructure grow and government-led electrification initiatives continue to expand, the demand for these engines is set to rise, further supporting the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $26.4 Billion |

| CAGR | 4.5% |

The gas-powered segment of the market is forecast to grow at a CAGR of 5% through 2034. This is attributed to technological advancements that enhance engine performance and efficiency, as well as the increasing need to adhere to stringent environmental regulations. The growing global emphasis on renewable energy sources has also played a significant role in driving the demand for gas-fired engines, which offer benefits such as high translation, optimized elements, efficient combustion, and low maintenance. These attributes contribute to the broader adoption of these engines across various industries.

U.S. prime power reciprocating power generating engine market is anticipated to generate USD 3.8 billion by 2034. Factors contributing to this growth include the increasing need for uninterrupted power and the growing frequency of power disruptions due to extreme weather events. The strain on existing electrical grids, coupled with the rising electricity demand, has underscored the importance of these engines in providing a reliable backup power solution. Additionally, the growing demand for backup power in critical facilities, such as data centers, is driving the adoption of these engines. Increased awareness of the need for reliable power sources further boosts the market's growth prospects.

As industries and governments focus on ensuring energy efficiency and sustainability, the demand for prime power reciprocating power generating engines is expected to continue its upward trajectory, playing a crucial role in meeting the growing global energy demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 – 2034 (Units, MW & USD Million)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 – 2034 (Units, MW & USD Million)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (Units, MW & USD Million)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (Units, MW & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Caterpillar

- 9.3 Cummins

- 9.4 Deere & Company

- 9.5 DEUTZ AG

- 9.6 Kirloskar

- 9.7 KUBOTA Corporation

- 9.8 MITSUBISHI HEAVY INDUSTRIES

- 9.9 Perkins Engines Company

- 9.10 Rehlko

- 9.11 Rolls-Royce

- 9.12 Sulzer

- 9.13 Wartsila

- 9.14 YANMAR HOLDINGS

- 9.15 Yuchai International