|

시장보고서

상품코드

1801939

아조토박터 기반 바이오 비료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Azotobacter-based Biofertilizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

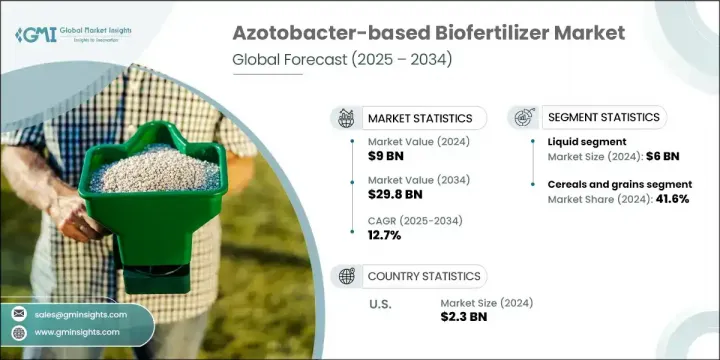

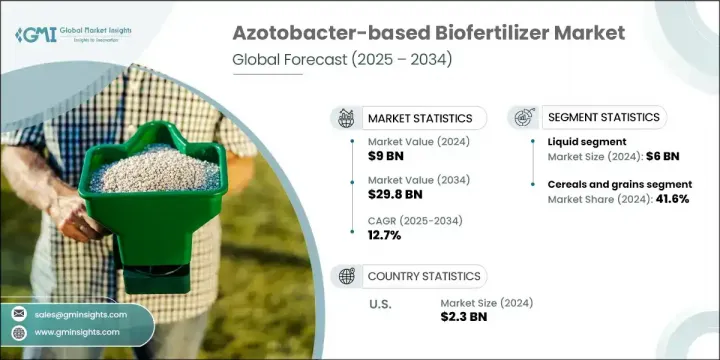

세계의 아조토박터 기반 바이오 비료 시장은 2024년에 90억 달러로 평가되었고, CAGR 12.7%로 성장하여 2034년에는 298억 달러에 이를 것으로 추정되고 있습니다.

이 급성장의 배경은 세계 인구 증가, 지속가능한 농업에 대한 관심 증가와 유기농법으로의 전환을 포함합니다. 화학합성비료의 유해성에 대한 우려가 높아짐에 따라 농가들은 보다 환경친화적인 대체품으로의 전환을 꾸준히 진행하고 있습니다. 화학 비료를 사용하지 않는 농산물을 요구하는 소비자의 목소리는 바이오 비료로의 전환을 더욱 뒷받침하고 있습니다. 정부는 또한 장려금 기반 프로그램을 통해 지속가능한 관행의 촉진에 나서고 있으며, 바이오비료업계에 기세를 기울이고 있습니다. 아조토박터 기반 제품은 대기 중의 질소를 자연스럽게 고정하고 토양의 질을 향상시키고 식물의 발달을 지원합니다.

아조토박터 기반 바이오 비료는 환경 변동으로 인한 성능의 일관성 문제에 직면하고 있습니다. 토양의 pH, 온도, 함수율 등의 요인이 결과에 영향을 주기 때문에 지역에 따라 결과가 변동하면 농가는 낙담할지도 모릅니다. 보존 기간이 제한되어 있는 것도 장애물 중 하나이며 제품의 유효성이 손실되면 사용자 경험이 저하되고 지역에 따라 채택이 억제되어 보급이 지연될 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 90억 달러 |

| 예측 금액 | 298억 달러 |

| CAGR | 12.7% |

액상 제형 부문은 2024년에 60억 달러의 매출을 올렸으며, 그 적용 효율, 균일한 적용 범위, 취급의 용이함에 의해 주도적 지위를 차지하고 있습니다. 이러한 특성은 특히 대규모 농업에 적합한 선택입니다. 농업용 살포 시스템과의 호환성이 여러 농업 환경에서 널리 사용되고 있음을 뒷받침합니다.

곡물 및 곡류는 2024년에 41.6%의 점유율을 차지했으며, 작물 유형별로 최대의 점유율을 유지하고 있습니다. 이러한 이점은 식량안보에 대한 세계 수요 증가, 정부가 지원하는 유기농업에 대한 노력, 곡류 및 곡물작물의 수율을 향상시키는 아조토박터 기반 바이오비료의 입증된 능력에 의해 뒷받침됩니다. 토양의 건전성에 대한 의식이 높아지는 가운데 많은 농가들이 생산성을 유지하면서 지속가능성의 목표를 달성하기 위해 이러한 바이오비료를 채택하고 있습니다.

미국 아조토박터 기반 바이오 비료 2024년 시장 규모는 23억 달러로 현대적인 농업 기술, 유기농업에 대한 강력한 추진, 확립된 농업 부문이 원동력이 되고 있습니다. 지지적인 규제 프레임워크과 토양 보전에 관한 의식의 고조가 계속해서 국가 전체의 도입율을 끌어 올리고 있습니다. 캐나다에서는 환경 친화적인 관행에 대한 신봉이 증가하고 지속 가능한 농업이 중요해지면서 시장이 급성장하고 있습니다. 연구기관과 주요 기업의 협력으로 새로운 효율적인 제품 변형이 생겨 아조토박터 기반 솔루션의 사용 범위가 넓어지고 있습니다.

아조토박터 기반 바이오 비료 시장의 주요 진출기업으로는 Growtech Agri Science, Biotech International, KN BIO SCIENCES, Unisun Agro, IFFCO, Rizobacter, FARMADIL INDIA LLP, Green Vision Life Sciences, Gujarat State Fertilizers &Chemicals,Jaipur Bio Fertilizers.등 입니다. 세계의 아조토박터 기반 바이오 비료 시장에 진출한 기업들은 제품 혁신, 목표를 겨냥한 제휴, 배합의 다양화에 주력함으로써 시장의 존재를 확대하고 있습니다. 대기업은 R&D에 투자하고 다양한 토양 및 기후 조건에 적합한 안정적이고 오래 지속되는 바이오 비료를 개발하고 있습니다. 연구 기관 및 대학과의 전략적 파트너십은 제품 성능과 지역 적응성을 높입니다. 일부 기업은 다양한 작물에 대한 맞춤형 솔루션을 중시하고, 충분한 서비스를 받지 못한 농업 지역에 도달하기 위해 유통망을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에 대해서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2021년-2034년

- 주요 동향

- 액체

- 운반에 기반(분말 또는 과립)

제6장 시장 추정 및 예측 : 작물 유형별, 2021년-2034년

- 주요 동향

- 곡물

- 지방종자 및 콩류

- 과일 및 채소

- 기타(현금 작물, 섬유 작물 등 포함)

제7장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 토양 처리

- 종자 처리

- 잎면 살포

제8장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 농가/재배자

- 연구기관

- 농업협동조합

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Biotech International

- FARMADIL INDIA LLP

- Green Vision Life Sciences

- Growtech Agri Science

- Gujarat State Fertilizers &Chemicals

- IFFCO

- Jaipur Bio Fertilizers

- KN BIO SCIENCES

- Rizobacter

- Unisun Agro

The Global Azotobacter-based Biofertilizer Market was valued at USD 9 billion in 2024 and is estimated to grow at a CAGR of 12.7% to reach USD 29.8 billion by 2034. This rapid growth is being driven by the rising global population, increasing focus on sustainable farming, and a shift toward organic agricultural practices. As concerns around the harmful effects of synthetic fertilizers grow, farmers are steadily moving toward more eco-friendly alternatives. Consumers' demand for chemical-free produce is further encouraging the switch to biofertilizers. Governments are also stepping in to promote sustainable practices through incentive-based programs, creating momentum in the biofertilizer industry. Azotobacter-based products are particularly gaining traction as they naturally fix atmospheric nitrogen, enrich soil quality, and support plant development-all while minimizing the environmental burden and offering a cost-effective solution compared to conventional options.

Azotobacter-based biofertilizers face challenges around consistency in performance due to environmental variability. Factors such as soil pH, temperature, and moisture content influence outcomes and may discourage farmers when results fluctuate across different regions. Limited shelf life is another hurdle, as any loss in product efficacy can lead to poor user experience and restrained adoption in some areas, potentially slowing down widespread use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9 Billion |

| Forecast Value | $29.8 Billion |

| CAGR | 12.7% |

The liquid formulations segment generated USD 6 billion in 2024, holding a leading position due to their application efficiency, uniform coverage, and ease of handling. These attributes make them a preferred option, particularly for large-scale farming operations. Their compatibility with agricultural application systems further supports their widespread use across multiple farming environments.

The cereals and grains accounted for 41.6% share in 2024, maintaining the largest share by crop type. This dominance is supported by rising global demand for food security, government-backed organic farming initiatives, and the proven ability of azotobacter-based biofertilizers to improve grain and cereal crop yields. With growing awareness around soil health, many farmers are adopting these biofertilizers to meet sustainability goals while maintaining productivity.

U.S. Azotobacter-based Biofertilizer Market was valued at USD 2.3 billion in 2024, driven by modern agricultural techniques, a strong push toward organic farming, and a well-established farming sector. Supportive regulatory frameworks and heightened awareness around soil conservation continue to boost adoption rates across the country. In Canada, the market is growing rapidly with increasing adherence to environmentally responsible practices and an emphasis on sustainable agriculture. Collaboration between research organizations and key players is helping bring out new, efficient product variants and expanding the usage scope of azotobacter-based solutions.

Key participants in the Azotobacter-based Biofertilizer Market include Growtech Agri Science, Biotech International, K. N. BIO SCIENCES, Unisun Agro, IFFCO, Rizobacter, FARMADIL INDIA LLP, Green Vision Life Sciences, Gujarat State Fertilizers & Chemicals, and Jaipur Bio Fertilizers. Companies in the global azotobacter-based biofertilizer market are expanding their market presence by focusing on product innovation, targeted collaborations, and diversification of formulations. Leading players are investing in R&D to develop stable, long-lasting biofertilizers suitable for diverse soil and climate conditions. Strategic partnerships with research institutions and universities enhance product performance and regional adaptability. Several firms are emphasizing tailored solutions for different crops and expanding their distribution networks to reach under-served agricultural regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Crop type trends

- 2.2.3 Application method trends

- 2.2.4 End user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid

- 5.3 Carrier-based (powder or granules)

Chapter 6 Market Estimates and Forecast, By Crop Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cereals and grains

- 6.3 Oilseeds and pulses

- 6.4 Fruits and vegetables

- 6.5 Others (including cash crops, fiber crops, etc.)

Chapter 7 Market Estimates and Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Soil treatment

- 7.3 Seed treatment

- 7.4 Foliar application

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Farmers/cultivators

- 8.3 Research institutions

- 8.4 Agricultural cooperatives

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Biotech International

- 10.2 FARMADIL INDIA LLP

- 10.3 Green Vision Life Sciences

- 10.4 Growtech Agri Science

- 10.5 Gujarat State Fertilizers & Chemicals

- 10.6 IFFCO

- 10.7 Jaipur Bio Fertilizers

- 10.8 K. N. BIO SCIENCES

- 10.9 Rizobacter

- 10.10 Unisun Agro