|

시장보고서

상품코드

1844289

라스트 마일 배송용 전기자동차 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electric Last Mile Delivery Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

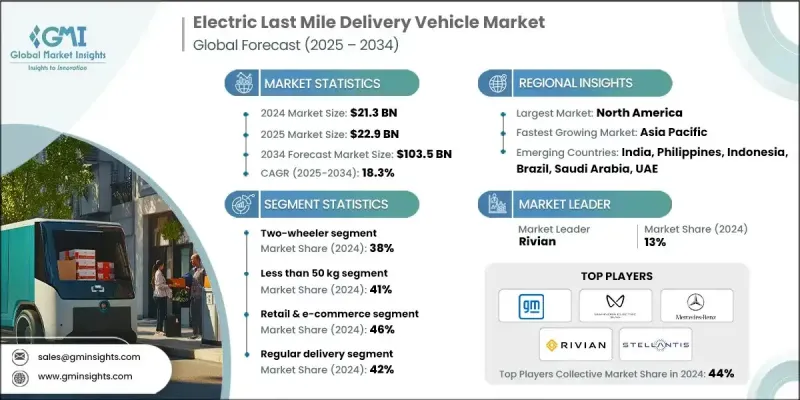

세계의 라스트 마일 배송용 전기자동차 시장 규모는 2024년에 213억 달러로 평가되었고, CAGR 18.3%로 성장할 전망이며, 2034년에는 1,035억 달러에 이를 것으로 추정됩니다.

친환경 도시형 배송 옵션에 대한 수요 증가, 배기 가스 규제 강화, 전자상거래 활동 가속 등 여러 역학이 이 급증에 박차를 가하고 있습니다. 소형 밴, 소형 카고 트라이크, 경량 오토바이 등의 전동 배송 차량은 배출 가스와 유지 보수 비용을 줄이면서 배송 효율을 높이는 것을 목표로하는 플릿 사업자에게 필수적인 존재가 되고 있습니다. 도시의 배출가스 감축을 요구하는 규제 압력도 플릿사업자에게 전기밴, 하이브리드트럭, 소형 배송차로의 전환을 촉구하고 있습니다. AI를 활용한 예지보전, IoT 기반 차량 추적, 고급 텔레매틱스 등의 기술은 차량 성능을 최적화하고 차량 가동 중지 시간을 줄이는 데 핵심적인 존재가 되고 있습니다. 고속 저장소 충전 및 배터리 교체 시스템과 같은 충전 인프라의 혁신은 교통량이 많은 도시 환경에서 장시간 배달 이동을 지원하는 데 중요한 역할을 합니다. 소매, 헬스케어 물류, 식료품 배송, 특히 밀집한 도시 환경에서의 전동 마이크로모빌리티의 이용이 증가하고 있어 시장 상황을 크게 밀어 올리고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 213억 달러 |

| 예측 금액 | 1,035억 달러 |

| CAGR | 18.3% |

2024년에는 전동 이륜차 부문의 점유율이 38%에 달했으며 2034년까지 연평균 복합 성장률(CAGR)은 18%로 성장할 것으로 예측됩니다. 이러한 차량은 합리적인 가격, 조종성, 혼잡한 도시 환경에서의 조작의 용이성 때문에 특히 매력적입니다. 신흥 기업과 소규모 배송 사업자는 운영비가 낮고 단거리 노선에서 신속한 배송 능력으로 전동이륜차를 선호하고 있습니다. 컴팩트한 크기는 교통 밀집지에서 부드러운 주행을 가능하게 하고, 사업자가 배달 속도와 효율성을 극대화하는 데 도움이 됩니다.

적재량 50킬로그램 미만의 차량 부문은 2024년에는 41%의 점유율을 차지했습니다. 도시의 혼잡과 유연하고 저비용 물류 솔루션에 대한 요구는 컴팩트 스쿠터 및 삼륜차와 같은 경량 차량의 채택을 뒷받침하고 있습니다. 이러한 차량은 최소한의 인프라만 필요하며, 배터리 용량이 작기 때문에 초기 비용과 런닝 비용이 낮고, 배기가스 규제 구역에서의 라스트 원마일 배송 업무 최적화를 목표로 하는 소규모 소매업체와 대기업 전자상거래 기업 모두에게 선호되는 옵션이 되고 있습니다.

미국의 라스트 마일 배송용 전기자동차 시장은 86%의 점유율을 차지하며, 2024년에는 68억 달러를 창출했습니다. 연방 정부의 EV 우대 조치, 도시 지역의 배송 인프라 개선, 견조한 전자상거래 활동 등의 요인이 시장을 추진하고 있습니다. 전동화, 차량의 디지털화, AI에 의한 루트 계획과 실시간 추적 등 스마트 기술에 대한 투자가 이 분야를 더욱 전진시키고 있습니다. 함대 운영자는 운영 비용을 줄이고 라스트 원마일 네트워크의 에너지 효율을 향상시키기 위해 이러한 도구를 활용합니다.

세계 라스트 마일 배송용 전기자동차 시장의 주요 기업으로는 Mahindra Electric, Xos, Tata Motors, Ford Motor Company, Mercedes-Benz, Rivian, BYD, GreenPower Motor Company, Stellantis, General Motors 등이 있습니다. 존재감을 넓히기 위해 라스트 마일 배송용 전기자동차 부문의 주요 기업은 몇 가지 전략적 이니셔티브에 주력하고 있습니다. 여기에는 대규모 전기화를 지원하기 위한 전자상거래 플랫폼, 물류기업, 정부기관과의 전략적 제휴 및 파트너십 형성이 포함됩니다. 대부분은 배터리 성능 향상, 항속 거리 연장, 텔레매틱스 시스템의 스마트화 등을 실현한 전기자동차의 새로운 모델을 투입하기 위해 연구 개발에 대한 투자를 강화하고 있습니다. 또한 수요 증가에 대응하기 위해 생산 능력을 확대하는 한편, 충전 인프라 제공업체와 협력하여 급속 충전 및 배터리 교환 솔루션을 전개하고 있습니다. OEM은 또한 AI와 IoT를 통합하여 예지보전 및 업무 효율화를 실현하는 디지털 차량 관리 툴도 중시하고 있으며, 차량 고객에게 부가가치 서비스를 제공하고 브랜드 충성도를 높이는데 도움이 되고 있습니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정과 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자상거래 수요 및 온라인 쇼핑 증가

- 정부 인센티브 및 배출 규제 급증

- 도시화의 진전 및 저배출 존의 확대

- 연료비 및 유지 보수 비용 절감으로 비용 절감 실현

- 배터리 기술 및 급속 충전 솔루션의 진보

- 업계의 잠재적 위험 및 과제

- 차량과 인프라에 대한 높은 초기 투자액

- 한정된 충전 인프라 및 제한된 차량의 주행 거리

- 시장 기회

- 물류 회사에 의한 차량 전동화 프로그램 확대

- 재생에너지를 충전 인프라에 통합

- 신흥 도시 시장에서의 수요 증가

- 카고 오토바이 및 마이크로모빌리티 솔루션 도입 급증

- 플릿 최적화를 위한 AI, IoT, 텔레매틱스의 통합 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 시장 도입 통계

- 전기배송차 도입률

- 차량 전동화의 진척

- 충전 인프라 개발

- 기술 기능의 채용

- 지역적인 채용 패턴

- 고객 만족도 지표

- 운영 성능 측정

- 전자상거래 및 배송 시장의 통합

- 온라인 소매업의 성장에 미치는 영향

- 라스트 마일 배송 수요 분석

- 배송 속도 및 효율 요건

- 고객의 기대의 진화

- 피크 시즌 수요 관리

- 도시 배송 밀도의 최적화

- 지속가능성에 관한 소비자의 기호

- 투자 상황 분석

- 자동차 제조업체의 투자

- 플릿 오퍼레이터의 자본 배분

- 정부의 인프라 자금

- 민간 충전 네트워크에 대한 투자

- 배달 기술의 벤처 캐피탈

- 투자 유형별 ROI 분석

- 그린본드 및 지속가능한 자금조달

- 고객 행동 분석

- 플릿 오퍼레이터의 의사 결정 요인

- 차량 선택 기준

- 테크놀로지의 채용에 관한 취향

- 총소유 비용 우선순위

- 서비스 및 지원 요건

- 지속가능성에 대한 노력의 영향

- 지역에 의한 취향의 차이

- 비즈니스 모델의 진화

- 종래의 자동차 판매 모델

- 차량 서비스(VaaS) 모델

- 임대 및 금융 솔루션

- 통합 플릿 솔루션

- 서비스로서의 과금 모델

- 성과주의 계약

- 성능과 품질 기준

- 상용차의 퍼포먼스 지표

- 배터리의 성능 및 내구성

- 충전 속도 및 효율

- 신뢰성 및 가용성 기준

- 안전성 및 보안 요건

- 환경 성능 기준

- 위험 평가 프레임워크

- 기술 도입 위험

- 배터리 성능 및 열화 위험

- 충전 인프라의 가용성 위험

- 규제 준수 위험

- 시장 수요 변동

- 공급망의 혼란 위험

- 경쟁 기술 위험

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 이륜차

- 전동 자전거

- 전동 스쿠터

- 전동 오토바이

- 삼륜차

- E 오토리키샤

- 전동 삼륜차

- 경상용 삼륜차

- 사륜차

- 소형 상용차

- 소형 상용차(LCV)

- 중형 상용차

- 특수 사륜차

- 마이크로 이동성

- 퍼스널 모빌리티

- 카고 마이크로 이동성

- 이륜차

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 소매 및 전자상거래

- 식품 및 식료품의 배달

- 헬스케어 및 의약품

- 우편물 및 화물

- 기타

제7장 시장 추계 및 예측 : 적재량별(2021-2034년)

- 주요 동향

- 50kg 미만

- 50-500kg

- 500kg 이상

제8장 시장 추계 및 예측 : 배송 방법별(2021-2034년)

- 주요 동향

- 정기 배송

- 당일 배송

- 속달 배송

제9장 시장 추계 및 예측 : 배터리 용량별(2021-2034년)

- 주요 동향

- 30kWh 미만

- 30-70kWh

- 70kWh 이상

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Arrival

- Ford Motor Company

- General Motors

- GreenPower Motor Company

- Mercedes-Benz

- Nissan Motor Company

- Rivian

- Stellantis

- Workhorse

- BYD

- 지역 기업

- Bollinger Motors

- Canoo

- Chanje Energy

- Isuzu Motors

- Lightning eMotors

- Mahindra Electric

- Renault

- Tata Motors

- Volkswagen Commercial Vehicles

- 신흥 기업

- Alke

- Cenntro Electric

- Einride

- Goupil

- SEA Electric

- StreetScooter

- Tevva Motors

- Volta Trucks

- Xos

The Global Electric Last Mile Delivery Vehicle Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 18.3% to reach USD 103.5 billion by 2034.

Several dynamics are fueling this surge, including the rising demand for eco-friendly urban delivery options, stricter emissions regulations, and the accelerating pace of e-commerce activity. Electric delivery vehicles such as small vans, compact cargo trikes, and lightweight bikes are becoming integral to fleet operators aiming to enhance delivery efficiency while reducing emissions and maintenance costs. Regulatory pressure to reduce urban emissions is also compelling fleet operators to switch to electric vans, hybrid trucks, and compact delivery vehicles. Technologies like predictive maintenance powered by AI, IoT-based vehicle tracking, and advanced telematics are becoming central to optimizing fleet performance and reducing vehicle downtime. Charging infrastructure innovations like fast depot charging and battery swapping systems are also playing a critical role in supporting extended delivery shifts in traffic-heavy urban environments. The rising use of electric micro-mobility for retail, healthcare logistics, and grocery delivery, especially in dense urban settings, is significantly boosting the market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $103.5 Billion |

| CAGR | 18.3% |

In 2024, the electric two-wheelers segment held a 38% share and is expected to grow at a CAGR of 18% through 2034. These vehicles are particularly attractive due to their affordability, maneuverability, and operational ease within congested city environments. Startups and small delivery businesses favor electric two-wheelers for their low operating costs and faster delivery capabilities across shorter routes. Their compact size enables smooth navigation through traffic-dense areas, helping businesses maximize delivery speed and efficiency.

The segment of vehicles designed to carry less than 50 kilograms held a 41% share in 2024. Urban congestion and the need for flexible, low-cost logistics solutions have driven the adoption of lightweight vehicles such as compact scooters and three-wheelers. These vehicles require minimal infrastructure, offer lower upfront and running costs due to smaller battery capacities, and are a preferred choice for both small retailers and major e-commerce firms seeking to optimize last-mile delivery operations in emission-regulated zones.

United States Electric Last-Mile Delivery Vehicle Market held an 86% share and generated USD 6.8 billion in 2024. Factors such as federal EV incentives, improved urban delivery infrastructure, and robust e-commerce activity are propelling the market forward. Investments in electrification, fleet digitization, and smart technologies such as route planning through AI and real-time tracking are further advancing the sector. Fleet operators are increasingly leveraging these tools to reduce operational costs and improve energy efficiency across last-mile networks.

Some of the leading companies in the Global Electric Last-Mile Delivery Vehicle Market include Mahindra Electric, Xos, Tata Motors, Ford Motor Company, Mercedes-Benz, Rivian, BYD, GreenPower Motor Company, Stellantis, and General Motors. To expand their presence, major companies in the electric last-mile delivery vehicle sector are focusing on several strategic initiatives. These include forming strategic alliances and partnerships with e-commerce platforms, logistics firms, and government bodies to support large-scale electrification. Many are ramping up investments in R&D to introduce new electric vehicle models with improved battery performance, extended range, and smarter telematics systems. Additionally, they are scaling up production capabilities to meet growing demand, while also collaborating with charging infrastructure providers to deploy fast-charging and battery-swapping solutions. OEMs also emphasizing digital fleet management tools that integrate AI and IoT for predictive maintenance and operational efficiency, helping them deliver value-added services to fleet customers and increase brand loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Payload Capacity

- 2.2.4 Application

- 2.2.5 Delivery Mode

- 2.2.6 Battery Capacity

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in e-commerce demand and online shopping.

- 3.2.1.2 Surge in government incentives and emission regulations.

- 3.2.1.3 Growth in urbanization and expansion of low-emission zones.

- 3.2.1.4 Rise in cost savings from lower fuel and maintenance.

- 3.2.1.5 Advancements in battery technology and fast-charging solutions.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment in vehicles and infrastructure.

- 3.2.2.2 Limited charging infrastructure and restricted vehicle range.

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of fleet electrification programs by logistics companies.

- 3.2.3.2 Integration of renewable energy into charging infrastructure.

- 3.2.3.3 Rise in demand from emerging urban markets.

- 3.2.3.4 Surge in adoption of cargo bikes and micro-mobility solutions.

- 3.2.3.5 Growth in AI, IoT, and telematics integration for fleet optimization.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Market adoption statistics

- 3.13.1 Electric delivery vehicle deployment rates

- 3.13.2 Fleet electrification progress

- 3.13.3 Charging infrastructure development

- 3.13.4 Technology feature adoption

- 3.13.5 Regional adoption patterns

- 3.13.6 Customer satisfaction metrics

- 3.13.7 Operational performance measurements

- 3.14 E-commerce & delivery market integration

- 3.14.1 Online retail growth impact

- 3.14.2 Last mile delivery demand analysis

- 3.14.3 Delivery speed & efficiency requirements

- 3.14.4 Customer expectation evolution

- 3.14.5 Peak season demand management

- 3.14.6 Urban delivery density optimization

- 3.14.7 Sustainability consumer preferences

- 3.15 Investment landscape analysis

- 3.15.1 Vehicle manufacturer investment

- 3.15.2 Fleet operator capital allocation

- 3.15.3 Government infrastructure funding

- 3.15.4 Private charging network investment

- 3.15.5 Venture capital in delivery technology

- 3.15.6 ROI analysis by investment type

- 3.15.7 Green bond & sustainable financing

- 3.16 Customer behavior analysis

- 3.16.1 Fleet operator decision factors

- 3.16.2 Vehicle selection criteria

- 3.16.3 Technology adoption preferences

- 3.16.4 Total cost of ownership priorities

- 3.16.5 Service & support requirements

- 3.16.6 Sustainability commitment influence

- 3.16.7 Regional preference variations

- 3.17 Business model evolution

- 3.17.1 Traditional vehicle sales models

- 3.17.2 Vehicle-as-a-service (VaaS) models

- 3.17.3 Leasing & financing solutions

- 3.17.4 Integrated fleet solutions

- 3.17.5 Charging-as-a-service models

- 3.17.6 Performance-based contracting

- 3.18 Performance & quality standards

- 3.18.1 Commercial vehicle performance metrics

- 3.18.2 Battery performance & durability

- 3.18.3 Charging speed & efficiency

- 3.18.4 Reliability & availability standards

- 3.18.5 Safety & security requirements

- 3.18.6 Environmental performance standards

- 3.19 Risk assessment framework

- 3.19.1 Technology adoption risks

- 3.19.2 Battery performance & degradation risks

- 3.19.3 Charging infrastructure availability risks

- 3.19.4 Regulatory compliance risks

- 3.19.5 Market demand volatility

- 3.19.6 Supply chain disruption risks

- 3.19.7 Competitive technology risks

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.1.1 Two-Wheeler

- 5.1.1.1 E-Bikes/Bicycles

- 5.1.1.2 E-Scooters

- 5.1.1.3 E-Motorcycles

- 5.1.2 Three-Wheeler

- 5.1.2.1 E-Auto Rickshaws

- 5.1.2.2 E-Tricycles

- 5.1.2.3 Light Commercial Three-Wheelers

- 5.1.3 Four-Wheeler

- 5.1.3.1 Micro Commercial Vehicles

- 5.1.3.2 Light Commercial Vehicles (LCV)

- 5.1.3.3 Medium Commercial Vehicles

- 5.1.3.4 Specialized Four-Wheelers

- 5.1.4 Micro Mobility

- 5.1.4.1 Personal Mobility

- 5.1.4.2 Cargo Micro Mobility

- 5.1.1 Two-Wheeler

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Retail & E-commerce

- 6.3 Food & Grocery Delivery

- 6.4 Healthcare & Pharmaceuticals

- 6.5 Mails and Packages

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Payload Capacity, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Less than 50 kg

- 7.3 50 to 500 kg

- 7.4 Above 500 kg

Chapter 8 Market Estimates & Forecast, By Delivery Mode, 2021-2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Regular Delivery

- 8.3 Same-Day Delivery

- 8.4 Express Delivery

Chapter 9 Market Estimates & Forecast, By Battery Capacity, 2021-2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Below 30 kWh

- 9.3 30-70 kWh

- 9.4 Above 70 kWh

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Arrival

- 11.1.2 Ford Motor Company

- 11.1.3 General Motors

- 11.1.4 GreenPower Motor Company

- 11.1.5 Mercedes-Benz

- 11.1.6 Nissan Motor Company

- 11.1.7 Rivian

- 11.1.8 Stellantis

- 11.1.9 Workhorse

- 11.1.10 BYD

- 11.2 Regional Players

- 11.2.1 Bollinger Motors

- 11.2.2 Canoo

- 11.2.3 Chanje Energy

- 11.2.4 Isuzu Motors

- 11.2.5 Lightning eMotors

- 11.2.6 Mahindra Electric

- 11.2.7 Renault

- 11.2.8 Tata Motors

- 11.2.9 Volkswagen Commercial Vehicles

- 11.3 Emerging Players

- 11.3.1 Alke

- 11.3.2 Cenntro Electric

- 11.3.3 Einride

- 11.3.4 Goupil

- 11.3.5 SEA Electric

- 11.3.6 StreetScooter

- 11.3.7 Tevva Motors

- 11.3.8 Volta Trucks

- 11.3.9 Xos