|

시장보고서

상품코드

1871136

직접 온라인(DOL) 모터 스타터 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Direct on Line Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

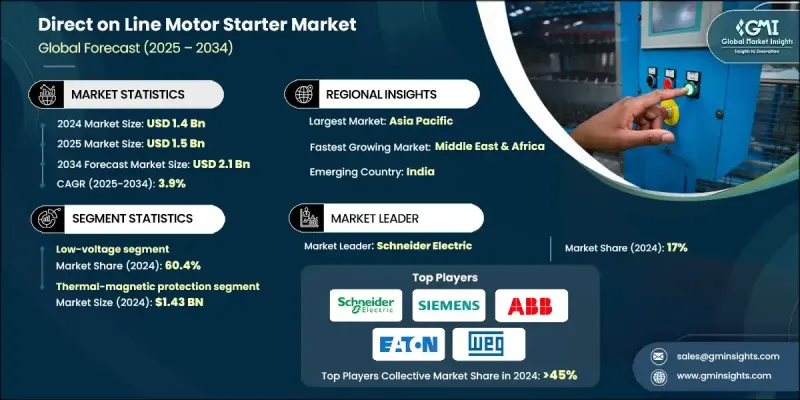

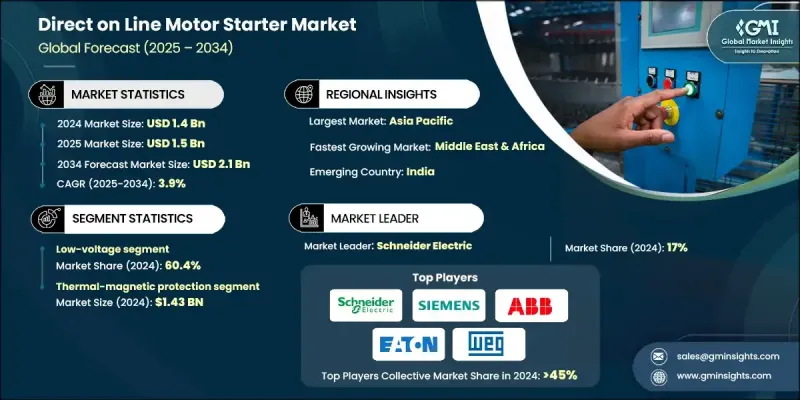

세계의 직접 온라인 모터 스타터 시장은 2024년에 14억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 3.9%를 나타낼 것으로 예측되며 21억 달러에 달할 전망입니다.

전 세계적으로 증가하는 전력 수요와 산업 전기화의 가속화는 특히 중소형 모터 부문에서 DOL 모터 스타터의 채택을 촉진하고 있습니다. 이러한 스타터는 비용 효율성과 운영 간편성으로 인해 지속적으로 선호되고 있습니다. 수자원 인프라 현대화 및 폐수 처리 시설에 대한 투자는 펌프, 송풍기, 보조 모터 부하 전반에 걸쳐 DOL 스타터에 대한 꾸준한 수요를 뒷받침하고 있습니다. 자본 지출 회복과 첨단 공장 업그레이드 추진에 힘입은 아시아 지역의 제조업 성장은 컨베이어 및 유틸리티 장비와 같은 핵심 시스템에서의 도입을 더욱 촉진하고 있습니다. 사하라 이남 아프리카 전역과 아시아 일부 지역에서는 접근성 증대로 기본 모터 제어 시스템의 새로운 활용 사례가 창출되고 있습니다. 국제에너지기구(IEA)의 최신 업데이트는 전력 가용성의 상당한 증가를 강조하며, 이는 DOL 스타터 시스템의 주요 적용 부문인 압축기, 팬, 펌프에 대한 수요 증가로 이어지고 있습니다. 신흥 시장들은 확장되는 인프라 수요에 부응하여 낮은 수명 주기 비용과 쉬운 유지보수를 이유로 이러한 솔루션을 채택하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예측 금액 | 21억 달러 |

| CAGR | 3.9% |

열자기 보호 장치는 경제성, 신뢰성 및 기능적 효율성으로 인해 DOL 스타터에 여전히 널리 채택되고 있습니다. 이러한 복합 메커니즘은 과부하 및 단락 사고에 대한 효과적인 보호를 보장하여 HVAC, 제조, 수자원 관리와 같은 부문에 적합합니다. 산업계가 예산 제약 하에서 안전성과 단순성을 계속 우선시함에 따라, 열-자기 장치들은 성능과 실용성 사이의 이상적인 균형을 제공합니다.

저전압 DOL 스타터 부문은 중소형 전동기에서 널리 사용되어 2024년 60.4%의 점유율을 차지했습니다. 이 카테고리는 설치 용이성, 표준 모터 구성과의 호환성, 대량 적용 시 비용 효율성 덕분에 계속해서 선두를 유지하고 있습니다. 전 세계 시장에서 인프라 개발 확대와 유틸리티 투자 증가 역시 특히 수처리 및 산업 시설에서 저전압 DOL 스타터 선호도를 높이는 데 기여하고 있습니다.

미국의 직접 온라인 모터 스타터 시장은 2024년 1억 6,270만 달러를 기록했습니다. 미국은 상하수도 인프라 현대화 투자로 인해 지속적인 수요 증가를 보이고 있습니다. 펌프 효율 및 모터 제어 기술 개선을 목표로 한 연방 자금 지원이 기존 시스템 교체를 촉진하고 있습니다. 에너지부(DOE)가 추진하는 에너지 효율 기준 역시 공공 및 산업 부문 전반에 걸쳐 최신 저전압 스타터 기술로의 전환을 뒷받침하고 있습니다.

세계의 직접 온라인 모터 스타터 시장에서 경쟁하는 주요 기업으로는 슈나이더 일렉트릭, WEG, 칼프 컨트롤스(Kalp Controls), 로바토 일렉트릭(LOVATO ELECTRIC), BCH 일렉트릭 리미티드(BCH Electric Limited), 제이딥 컨트롤스(Jaydeep Controls), 록웰 오토메이션(Rockwell Automation), ABB, 친트 그룹(CHINT Group), 라우리츠 크누센 일렉트릭 & 오토메이션(Lauritz Knudsen Electrical & Automation), C&S 일렉트릭(C&S Electric), 지멘스(Siemens), LS 일렉트릭(LS ELECTRIC), CMI 스위치기어(CMI Switchgear), CG 파워 & 인더스트리얼 솔루션스(CG Power & Industrial Solutions), 오므론 코퍼레이션(Omron Corporation), 단포스(Danfoss), 노아크 일렉트릭(NOARK Electric), c3컨트롤스(c3controls), 이튼(Eaton) 등이 있습니다. 직접 접속형 모터 스타터 시장에서의 입지를 강화하기 위해 기업들은 신흥 인프라 프로젝트에 맞춤화된 컴팩트하고 모듈식 디자인으로 제품 포트폴리오를 확장하는 등의 전략을 우선시하고 있습니다. 또한 에너지 효율적인 모터 및 스마트 산업 시스템과의 호환성을 강화하고 있습니다. 공공 부문 진출 확대를 위해 정부 주도의 유틸리티 및 수자원 프로젝트와의 전략적 협력을 활용하고 있습니다. 동시에 글로벌 기업들은 리드 타임 단축과 지원 강화를 목표로 현지 생산 시설 및 서비스 센터를 설립하여 고성장 지역을 공략하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 억제요인 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 직접 온 라인(DoL) 모터 스타터의 비용 구조 분석

- 가격 동향 분석(달러/유닛)

- 지역별

- 새로운 기회와 동향

- DoL 모터 스타터의 투자 분석과 미래 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 전략적 대시보드

- 경쟁 벤치마킹

- 혁신과 기술의 정세

제5장 시장 규모와 예측 : 보호 시스템별(2021-2034년)

- 주요 동향

- 전자 과부하 릴레이

- 솔리드 스테이트 과부하 보호

- 열자기 보호 장치

제6장 시장 규모와 예측 : 제어 시스템별(2021-2034년)

- 주요 동향

- PLC

- 필드버스

제7장 시장 규모와 예측 : 전압별(2021-2034년)

- 주요 동향

- 저전압

- 중전압

- 고전압

제8장 시장 규모와 예측 : 전류별(2021-2034년)

- 주요 동향

- 9-27A

- >27-90A

- 90-270A

- >270-810A

- 810A 초과

제9장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 분산형 아키텍처

- 제어캐비닛

- 하이브리드 구성

제10장 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주거용

- 상업용

- 산업용

제11장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 러시아

- 영국

- 이탈리아

- 스페인

- 네덜란드

- 오스트리아

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 인도네시아

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 남아프리카

- 나이지리아

- 라틴아메리카

- 브라질

- 아르헨티나

제12장 기업 프로파일

- ABB

- BCH Electric Limited

- C&S Electric

- CG Power &Industrial Solutions

- CHINT Group

- CMI Switchgear

- c3controls

- Danfoss

- Eaton

- Jaydeep Controls

- Kalp Controls

- Lauritz Knudsen Electrical &Automation

- LOVATO ELECTRIC

- LS ELECTRIC

- NOARK Electric

- Omron Corporation

- Rockwell Automation

- Schneider Electric

- Siemens

- WEG

The Global Direct on Line Motor Starter Market was valued at USD 1.4 Billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 2.1 Billion by 2034.

Increasing global electricity demand and the accelerated pace of industrial electrification are fueling the adoption of DOL motor starters, especially in small to medium motor segments. These starters continue to be favored for their cost efficiency and operational simplicity. Investments in water infrastructure modernization and wastewater facilities are supporting steady demand for DOL starters across pumps, blowers, and auxiliary motor loads. Manufacturing growth in Asia, driven by revived capital expenditure and a strong push toward high-tech plant upgrades, is further boosting deployment in essential systems like conveyors and utility equipment. In regions across sub-Saharan Africa and parts of Asia, increasing access is creating new use cases for basic motor control systems. The IEA's latest updates highlight substantial growth in power availability, which is translating into heightened demand for compressors, fans, and pumps, key applications for DOL starter systems. Emerging markets are adopting these solutions for their low life-cycle cost and easy maintenance, aligning with the needs of expanding infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 3.9% |

Thermal-magnetic protection remains widely adopted in DOL starters due to its affordability, reliability, and functional efficiency. These combined mechanisms ensure effective protection against overload and short-circuit events, making them suitable for sectors such as HVAC, manufacturing, and water management. As industries continue prioritizing safety and simplicity under budget constraints, thermal-magnetic units offer an ideal balance between performance and practicality.

The low-voltage DOL starters segment held 60.4% share in 2024, owing to their prevalent use in small and medium-sized electric motors. This category continues to lead due to ease of installation, compatibility with standard motor configurations, and cost-effectiveness in high-volume applications. Expansion in infrastructure development and rising utility investments across global markets are also contributing to the increasing preference for low-voltage DOL starters, especially in water treatment and industrial facilities.

United States Direct on Line Motor Starter Market generated USD 162.7 million in 2024. U.S. continues to witness strong demand due to investments in modernizing water and wastewater infrastructure. Federal funding aimed at improving pump efficiency and motor control technologies is driving the replacement of legacy systems. Energy efficiency standards promoted by the Department of Energy (DOE) are also supporting the transition toward updated low-voltage starter technologies across both public and industrial sectors.

Key companies competing in the Global Direct on Line Motor Starter Market include Schneider Electric, WEG, Kalp Controls, LOVATO ELECTRIC, BCH Electric Limited, Jaydeep Controls, Rockwell Automation, ABB, CHINT Group, Lauritz Knudsen Electrical & Automation, C&S Electric, Siemens, LS ELECTRIC, CMI Switchgear, CG Power & Industrial Solutions, Omron Corporation, Danfoss, NOARK Electric, c3controls, and Eaton. To strengthen their position in the Direct on Line Motor Starter Market, companies are prioritizing strategies such as expanding product portfolios with compact, modular designs tailored for emerging infrastructure projects. They are also enhancing compatibility with energy-efficient motors and smart industrial systems. Strategic collaborations with government-led utility and water projects are being leveraged to increase public sector penetration. In parallel, global players are targeting high-growth regions by setting up local manufacturing facilities and service centers, aiming to reduce lead times and enhance support.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Protection system trends

- 2.1.3 Control system trends

- 2.1.4 Voltage trends

- 2.1.5 Current trends

- 2.1.6 Application trends

- 2.1.7 End use trends

- 2.1.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Cost structure analysis of Direct on Line (DoL) motor starters

- 3.8 Price trend analysis, (USD/Unit)

- 3.8.1 By region

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future outlook for the DoL motor starter

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Protection System, 2021 - 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 Electronic overload relays

- 5.3 Solid-state overload protection

- 5.4 Thermal-magnetic protection

Chapter 6 Market Size and Forecast, By Control System, 2021 - 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 PLC

- 6.3 Fieldbus

Chapter 7 Market Size and Forecast, By Voltage, 2021 - 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Size and Forecast, By Current, 2021 - 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 > 9 A - 27 A

- 8.3 > 27 A - 90 A

- 8.4 > 90 A - 270 A

- 8.5 > 270 A - 810 A

- 8.6 > 810 A

Chapter 9 Market Size and Forecast, By Application, 2021 - 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 Distributed architecture

- 9.3 Control cabinet

- 9.4 Hybrid configuration

Chapter 10 Market Size and Forecast, By End Use, 2021 - 2034 (Units & USD Million)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.4 Industrial

Chapter 11 Market Size and Forecast, By Region, 2021 - 2034 (Units & USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 Russia

- 11.3.4 UK

- 11.3.5 Italy

- 11.3.6 Spain

- 11.3.7 Netherlands

- 11.3.8 Austria

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 South Korea

- 11.4.4 India

- 11.4.5 Australia

- 11.4.6 New Zealand

- 11.4.7 Indonesia

- 11.5 Middle East & Africa

- 11.5.1 Saudi Arabia

- 11.5.2 UAE

- 11.5.3 Qatar

- 11.5.4 Egypt

- 11.5.5 South Africa

- 11.5.6 Nigeria

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Argentina

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 BCH Electric Limited

- 12.3 C&S Electric

- 12.4 CG Power & Industrial Solutions

- 12.5 CHINT Group

- 12.6 CMI Switchgear

- 12.7 c3controls

- 12.8 Danfoss

- 12.9 Eaton

- 12.10 Jaydeep Controls

- 12.11 Kalp Controls

- 12.12 Lauritz Knudsen Electrical & Automation

- 12.13 LOVATO ELECTRIC

- 12.14 LS ELECTRIC

- 12.15 NOARK Electric

- 12.16 Omron Corporation

- 12.17 Rockwell Automation

- 12.18 Schneider Electric

- 12.19 Siemens

- 12.20 WEG