|

시장보고서

상품코드

1885813

신장 식이 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Renal Diet Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

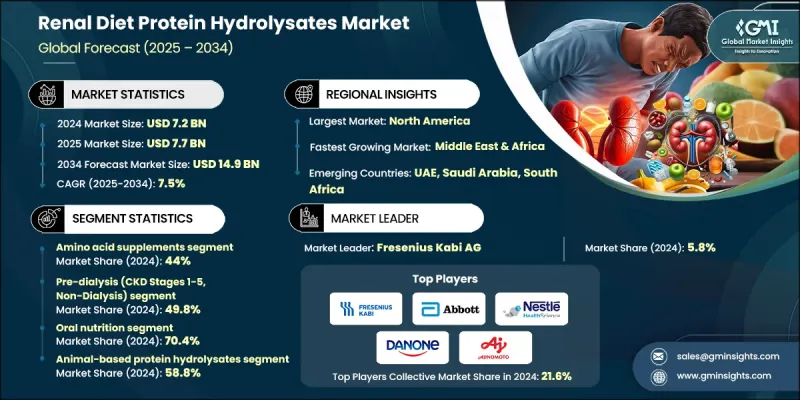

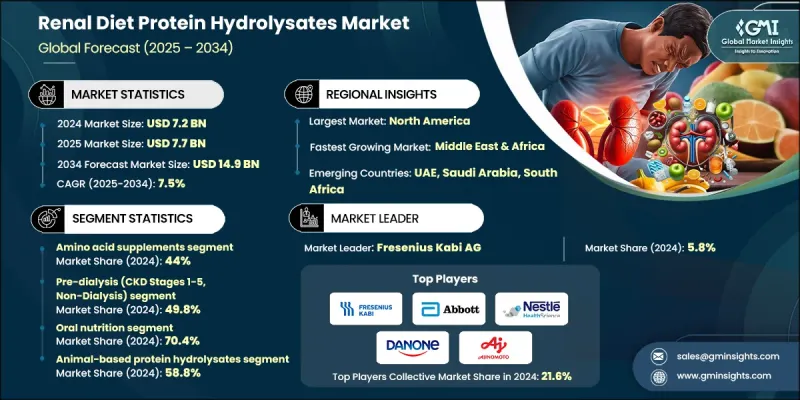

세계의 신장 식이 단백질 가수분해물 시장은 2024년에 72억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7.5%로 성장할 전망이며, 149억 달러에 이를 것으로 예측되고 있습니다.

이 성장은 세계적인 만성 신장 질환의 부담 증가 및 신장 관리에서 전문 영양의 중요성에 대한 인식 증가에 의해 추진되고 있습니다. 의료 시스템은 신장 기능을 지원하기 위한 단백질 관리를 보다 중시하고 있으며, 처리가 용이하고 신장에 대한 부담을 경감하면서 필수 영양소를 공급할 수 있는 가수분해 단백질 솔루션 수요를 끌어올리고 있습니다. 노화에 따른 신장질환이 보다 광범위해짐에 따라 고령화하는 세계 인구도 크게 기여하고 있습니다. 이 연구는 신장 기능 장애가 있는 사람들을 겨냥하여 영양을 제공하는 데 있어 가수분해 단백질의 임상적 이점을 계속 강조하고 있습니다. 조기 발견 및 개인화된 식이요법이 보급됨에 따라 이러한 전문 제제에 대한 수요가 더욱 높아질 것으로 예측됩니다. 효소 가수분해 기술의 진보로 제품의 균일성 및 생산 효율이 향상되고 세계적인 공급량이 증가하고 있습니다. 의료비 증가 및 질병 진행을 늦추는 비용 효과적인 영양 요법의 필요성은 시장의 장기 전망을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 72억 달러 |

| 예측 금액 | 149억 달러 |

| CAGR | 7.5% |

아미노산 보충제 부문은 2024년에 44%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 7.5%로 성장할 것으로 예측됩니다. 이러한 보충제는 만성 신장 질환(CKD) 환자의 영양 요건을 충족하면서 단백질 섭취와 관련된 합병증을 최소화하는 데 중요한 역할을 합니다. 단백질 제한 식이를 섭취하는 환자에게는 개별적으로 조정된 아미노산 배합이 필수적이며, 배합 과학의 지속적인 진보로 보다 우수한 흡수성과 정밀한 영양 공급이 기대됩니다.

투석 전 카테고리(CKD 스테이지 1-5, 비투석 환자 대상)는 2024년에 49.8%의 점유율을 차지하였고, 2025-2034년 CAGR 7.4%로 성장할 것으로 예측됩니다. 이 부문이 최대 규모인 배경에는 투석에 이르기 전에 조기 영양 개입이 필요한 환자 수가 매우 많다는 것을 들 수 있습니다. 신장 기능의 악화를 늦추기 위해 단백질 섭취량 관리를 중시하는 가이드라인이 계속되는 가운데, 특수한 가수분해물 기반 제품에 대한 수요는 계속 견조하게 추이할 것으로 예측됩니다.

북미의 신장 식이 단백질 가수분해물 시장은 2024년 35.3%의 점유율을 차지했습니다. 이 지역은 고급 의료 시스템, 확립된 상환 제도 및 만성 신장 질환의 높은 이환율의 이점을 가지고 있습니다. 의료 영양 제품의 광범위한 채용과 식이 관리를 위한 견고한 임상 프레임워크는 이 지역의 주도적 지위에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제1장 주요 요약

제2장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 신장병(CKD)의 유병률 상승 및 고령화 인구 동태

- 식물성 단백질 가수분해물을 지지하는 임상적 근거

- 효소 가수분해에 있어서 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용 및 규제의 복잡성

- 특정 가수분해물에 대한 제한적 임상적 증거

- 시장 기회

- 개인화된 영양학 및 정밀의료

- 식물 유래의 혁신 및 지속가능성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제3장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제4장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 아미노산 보충제

- α-케토 아날로그

- 분지쇄 아미노산(BCAA)

- 완전 가수분해 단백질

- 비타민 및 미네랄 보충제

- 수용성 비타민

- 비타민 D 아날로그

- 관리된 미네랄 배합

- 미네랄 보충제

- 철분 보충제

- 칼슘 베이스 제품

- 인 제한 배합 제품

- 프로바이오틱스

- 단일 균주 배합 제품

- 여러 균주의 조합

- 신바이오틱스 제품

제5장 시장 추계 및 예측 : CKD 스테이지별(2021-2034년)

- 주요 동향

- 투석 전(CKD 스테이지 1-5, 비투석)

- 초기 단계 만성 신장병(스테이지 1-2)

- 중등도 만성 신장병(스테이지 3)

- 고도 만성 신장병(스테이지 4-5)

- 혈액 투석 환자

- 통상형 혈액 투석

- 고플럭스 혈액 투석

- 혈액 투석 여과

- 복막 투석 환자

- 지속적 휴대형 복막 투석(CAPD)

- 자동 복막 투석(APD)

- 말기 신부전(ESRD)

- 이식 대기 환자

- 보존적 치료

- 급성신장애(AKI)로부터의 회복

제6장 시장 추계 및 예측 : 투여 방법별(2021-2034년)

- 주요 동향

- 경구 영양

- 즉시 마시는 제형

- 분말 보충제

- 고형 제형

- 경장 영양

- 경관영양제제

- 경구 영양 보조 식품(ONS)

- 모듈형 제품

- 비경구 영양

- 완전정맥영양(TPN)

- 말초정맥영양(PPN)

제7장 시장 추계 및 예측 : 단백질원별(2021-2034년)

- 주요 동향

- 동물성 단백질 가수분해물

- 유청 단백질 가수분해물

- 카제인 가수분해물

- 달걀 흰자위 단백질 가수분해물

- 물고기 단백질 가수분해물

- 식물성 단백질 가수분해물

- 완두콩 단백질 가수분해물

- 콩 단백질 가수분해물

- 쌀 단백질 가수분해물

- 헴프 단백질 가수분해물

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Fresenius Kabi AG

- Abbott Laboratories

- Nestle Health Science

- Danone Nutricia

- Ajinomoto Co.

- B. Braun Melsungen

- Grifols SA

- Baxter/Vantive

- Ajanta Pharma Limited

- Mankind Pharma Ltd.

The Global Renal Diet Protein Hydrolysates Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 14.9 billion by 2034.

This growth is driven by the increasing global burden of chronic kidney disease and rising awareness of the importance of specialized nutrition in kidney care. Healthcare systems are placing greater emphasis on protein management to support kidney function, pushing demand for hydrolyzed protein solutions that are easier to process and deliver essential nutrients with reduced strain on the kidneys. An aging global population has also contributed significantly, as age-related kidney conditions become more widespread. Research continues to highlight the clinical benefits of protein hydrolysates in providing targeted nutrition for kidney-impaired individuals. With early detection and personalized dietary interventions gaining traction, demand for these specialized formulations is expected to intensify. Improvements in enzymatic hydrolysis technologies have enhanced product consistency and production efficiency, increasing availability worldwide. Rising healthcare expenditures and the need for cost-effective nutritional therapies to help slow disease progression further reinforce the market's long-term outlook.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 7.5% |

The amino acid supplements segment held a 44% share in 2024 and is projected to grow at a CAGR of 7.5% through 2034. These supplements play a key role in meeting nutrient requirements for individuals with chronic kidney disease while minimizing the complications associated with intact protein intake. Tailored amino acid formulations are essential for patients following protein-limited diets, and ongoing progress in formulation science is expected to support better absorption and precise nutrient delivery.

The pre-dialysis category, covering CKD Stages 1-5 (non-dialysis), accounted for a 49.8% share in 2024 and is anticipated to grow at a CAGR of 7.4% from 2025 to 2034. This segment is the largest due to the substantial number of patients who require early nutritional intervention before reaching dialysis. As guidelines continue to emphasize controlled protein intake to slow kidney deterioration, demand for specialized hydrolysate-based products is expected to remain strong.

North America Renal Diet Protein Hydrolysates Market held a 35.3% share in 2024. The region benefits from advanced healthcare systems, established reimbursement structures, and a high incidence of chronic kidney disease. Widespread adoption of medical nutrition products and strong clinical frameworks for dietary management contribute significantly to regional leadership.

Key companies in the Renal Diet Protein Hydrolysates Market include Fresenius Kabi AG, Abbott Laboratories, Nestle Health Science, Danone Nutricia, Ajinomoto Co., B. Braun Melsungen, Grifols S.A., Baxter/Vantive, Ajanta Pharma Limited, and Mankind Pharma Ltd. Companies operating in the Renal Diet Protein Hydrolysates Market follow several strategies to strengthen their competitive position. Many focus on developing more bioavailable formulations using advanced enzymatic processes that improve nutrient absorption and minimize metabolic load on the kidneys. Expanding product portfolios tailored to different CKD stages helps brands reach a broader patient base. Investments in clinical research support evidence-backed nutritional solutions and improve physician recommendations. Firms collaborate with healthcare providers and dietitians to increase the adoption of medical nutrition products. Geographic expansion through partnerships, distribution networks, and localized manufacturing enhances market accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 1 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 CKD stage trends

- 2.2.4 Administration mode trends

- 2.2.5 Protein source trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 2 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising CKD prevalence & aging demographics

- 3.2.1.2 Clinical evidence supporting plant-based protein hydrolysates

- 3.2.1.3 Technological advances in enzymatic hydrolysis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & regulatory complexity

- 3.2.2.2 Limited clinical evidence for specific hydrolysates

- 3.2.3 Market opportunities

- 3.2.3.1 Personalized nutrition & precision medicine

- 3.2.3.2 Plant-based innovation & sustainability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 3 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 4 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Amino acid supplements

- 5.2.1 Alpha-ketoanalogues

- 5.2.2 Branched-chain amino acids (BCAAS)

- 5.2.3 Complete protein hydrolysates

- 5.3 Vitamin & mineral supplements

- 5.3.1 Water-soluble vitamins

- 5.3.2 Vitamin D analogues

- 5.3.3 Controlled mineral formulations

- 5.4 Mineral supplements

- 5.4.1 Iron supplements

- 5.4.2 Calcium-based products

- 5.4.3 Phosphorus-restricted formulations

- 5.5 Probiotics

- 5.5.1 Single-strain formulations

- 5.5.2 Multi-strain combinations

- 5.5.3 Synbiotic products

Chapter 5 Market Estimates and Forecast, By CKD Stage, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pre-dialysis (CKD stages 1-5, non-dialysis)

- 6.2.1 Early-stage CKD (stages 1-2)

- 6.2.2 Moderate CKD (stage 3)

- 6.2.3 Advanced CKD (stages 4-5)

- 6.3 Hemodialysis patients

- 6.3.1 Conventional hemodialysis

- 6.3.2 High-flux hemodialysis

- 6.3.3 Hemodiafiltration

- 6.4 Peritoneal dialysis patients

- 6.4.1 Continuous ambulatory peritoneal dialysis (CAPD)

- 6.4.2 Automated peritoneal dialysis (APD)

- 6.5 End-stage renal disease (ESRD)

- 6.5.1 Pre-transplant patients

- 6.5.2 Conservative management

- 6.5.3 Acute kidney injury (AKI) recovery

Chapter 6 Market Estimates and Forecast, By Administration Mode, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Oral nutrition

- 7.2.1 Ready-to-drink formulations

- 7.2.2 Powder supplements

- 7.2.3 Solid dosage forms

- 7.3 Enteral nutrition

- 7.3.1 Tube feeding formulations

- 7.3.2 Oral nutritional supplements (ONS)

- 7.3.3 Modular products

- 7.4 Parenteral nutrition

- 7.4.1 Total parenteral nutrition (TPN)

- 7.4.2 Peripheral parenteral nutrition (PPN)

Chapter 7 Market Estimates and Forecast, By Protein Source, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Animal-based protein hydrolysates

- 8.2.1 Whey protein hydrolysates

- 8.2.2 Casein hydrolysates

- 8.2.3 Egg white protein hydrolysates

- 8.2.4 Fish protein hydrolysates

- 8.3 Plant-based protein hydrolysates

- 8.3.1 Pea protein hydrolysates

- 8.3.2 Soy protein hydrolysates

- 8.3.3 Rice protein hydrolysates

- 8.3.4 Hemp protein hydrolysates

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 10.1 Fresenius Kabi AG

- 10.2 Abbott Laboratories

- 10.3 Nestle Health Science

- 10.4 Danone Nutricia

- 10.5 Ajinomoto Co.

- 10.6 B. Braun Melsungen

- 10.7 Grifols S.A.

- 10.8 Baxter/Vantive

- 10.9 Ajanta Pharma Limited

- 10.10 Mankind Pharma Ltd.