|

시장보고서

상품코드

1885814

염증성 장질환(IBD)용 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Protein Hydrolysates for Inflammatory Bowel Disease Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

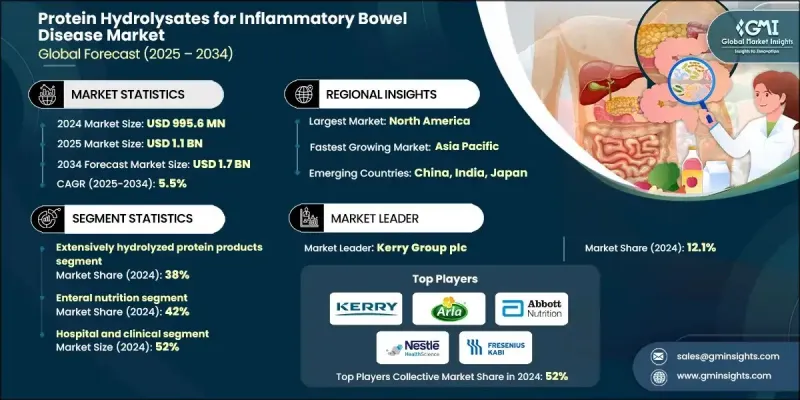

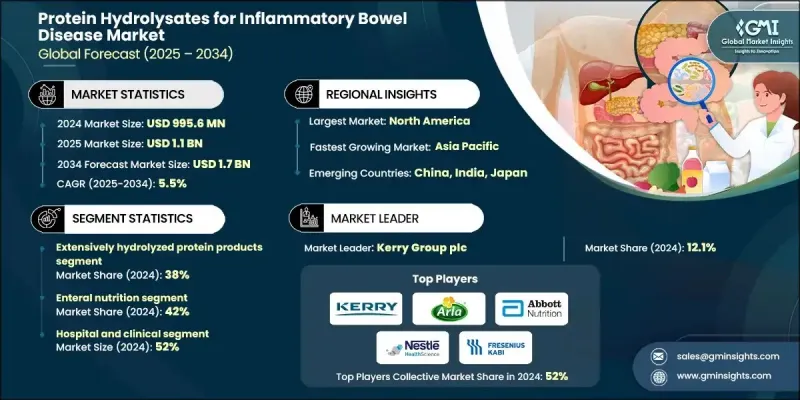

세계의 염증성 장질환(IBD)용 단백질 가수분해물 시장은 2024년에 9억 9,560만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.5%로 성장할 전망이며, 17억 달러에 달할 것으로 예측되고 있습니다.

최근의 임상연구 결과가 치료적 가치를 뒷받침하는 가운데 강력한 과학적 뒷받침으로 업계 확대가 계속되고 있습니다. 이러한 제품은 확립된 진단 시스템 및 첨단 의료 시스템이 있는 지역, 특히 염증성 장질환(IBD)의 감지율이 높은 시장에서 주목을 받고 있습니다. 아시아태평양 등 급성장을 이루고 있는 지역에서는 특히 동아시아에서 인지도 향상 및 발병률 증가 동향으로 시장 확대가 가속화되고 있습니다. 시장을 재구성하는 또 다른 주요 요인은 식물성 영양으로의 세계 전환 확대입니다. 채식주의자 및 채식주의 라이프스타일이 퍼지는 가운데, 염증 관리 및 장내 건강 유지의 가능성을 강조하는 조사에 힘입어 식물 유래의 단백질 가수분해물에 대한 수요가 급격히 높아지고 있습니다. 또한 전문 의료 영양에 대한 광범위한 경향도 시장의 관심을 끌고 있으며, 단백질 가수분해물은 만성 소화기 질환을 관리하는 개인을 위한 치료 식이 요법 전략에서 중요한 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 9억 9,560만 달러 |

| 예측 금액 | 17억 달러 |

| CAGR | 5.5% |

고도의 가수분해 단백질 제제 분절은 2024년에 38%의 점유율을 차지했으며, 심한 염증성 장질환에 대한 적응성과 고소화성 및 저항원성 솔루션의 필요성이 있었습니다. 이 제품은 더 작은 영양 성분으로 가공되기 때문에 장 기능의 유지와 회복 촉진에 필수적인 주요 영양소를 공급하면서 면역 반응의 유도를 완화합니다. 정밀한 영양 개입을 필요로 하는 환자에게의 지원 효과에 의해 임상 현장에서의 수용성은 계속 높아지고 있습니다.

장 영양분은 2024년에 42%의 점유율을 차지했습니다. 이 카테고리는 영양 지원을 영양 보충 시스템이나 액체 기반 식단 관리를 통해 필요한 염증성 장질환 환자에게 널리 사용됩니다. 임상적 증거는 특히 전통적인 치료가 불충분한 경우에 경장 영양의 이점을 일관되게 보여주며, 그 견조한 실적은 질병의 악화 관리에서 전문적인 영양 요법에 대한 지속적인 의존을 반영합니다.

미국의 염증성 장질환용 단백질 가수분해물 시장은 2024년 3억 3,040만 달러 규모에 달했습니다. 이는 인구의 약 0.72%가 영향을 받는 방대한 IBD 환자층에 의해 지원됩니다. 이 지역의 견고한 의료 시스템, 활발한 임상 연구 환경, 의료 영양에 대한 지원적인 규제, 보험 적용 범위가 높은 보급률에 기여하고 있습니다. 주요 연구 기관 주도의 지속적인 조사는 치료 영양 개선 및 리더십 유지를 위한 이 지역의 대처를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 규모 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 고도 가수분해 단백질 제품

- 부분 가수분해 단백질 제품

- 아미노산계 제형

- 기타

제6장 시장 규모 및 예측 : 원료별(2021-2034년)

- 주요 동향

- 우유 유래 가수분해물

- 유청 단백질 가수분해물

- 카제인 가수분해물

- α-락트알부민 농축물

- 기타

- 식물 유래 가수분해물

- 쌀 단백질 가수분해물

- 완두콩 단백질 가수분해물

- 콩 단백질 가수분해물

- 기타

- 해양 유래 가수분해물

- 기타

제7장 시장 규모 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 경장 영양

- 경구 영양 보조 식품

- 의료용 식품

- 기타

제8장 시장 규모 및 예측 : 최종용도별(2021-2034년)

- 주요 동향

- 병원 및 임상 시설

- 재택 치료

- 전문 영양 센터

- 기타

제9장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Kerry Group

- Arla Foods Ingredients

- Abbott Nutrition

- Nestle Health Science

- Fresenius Kabi

- Nutricia

- Reckitt

- Ajinomoto

- DSM Nutritional Products

The Global Protein Hydrolysates for Inflammatory Bowel Disease Market was valued at USD 995.6 million in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 1.7 billion by 2034.

Industry expansion continues to benefit from strong scientific support, as recent clinical findings reinforce their therapeutic value. These products are gaining traction across regions with established diagnostic systems and advanced healthcare capabilities, particularly in markets where IBD detection rates are high. Areas experiencing rapid growth, such as Asia Pacific, are accelerating due to rising awareness and increasing incidence trends, especially in East Asia. Another major force reshaping the market is the growing global shift toward plant-based nutrition. As vegan and vegetarian lifestyles expand, demand for plant-derived protein hydrolysates is rising sharply, supported by research that highlights their potential in managing inflammation and supporting gut health. Market interest is also driven by the broader trend toward specialized medical nutrition, where protein hydrolysates are becoming an important part of therapeutic dietary strategies for individuals managing chronic digestive conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $995.6 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 5.5% |

The extensively hydrolyzed protein formulations segment held a 38% share in 2024, driven by their suitability for severe inflammatory bowel disease and the need for highly digestible, low-antigen solutions. These products are processed into smaller nutritional components, helping reduce immune triggers while still supplying key nutrients essential for maintaining intestinal function and promoting recovery. Their clinical acceptance continues to rise due to their effectiveness in supporting patients requiring precise nutritional interventions.

The enteral nutrition segment held a 42% share in 2024. This category is widely used for individuals with inflammatory bowel disease who require nutritional support through feeding systems or liquid-based dietary management. Clinical evidence consistently highlights the benefits of enteral nutrition, particularly in cases where conventional therapies are insufficient, and its strong performance reflects continued reliance on specialized nutritional regimens for managing disease flares.

U.S. Protein Hydrolysates for Inflammatory Bowel Disease Market generated USD 330.4 million in 2024, supported by a significant IBD patient pool, with about 0.72% of the population affected. The region's robust healthcare systems, active clinical research landscape, supportive regulations for medical nutrition, and insurance coverage contribute to strong adoption. Ongoing studies led by major research institutions underscore the region's commitment to improving therapeutic nutrition and maintaining its leadership position.

Key companies participating in the Protein Hydrolysates for Inflammatory Bowel Disease Market industry include Kerry Group plc, Arla Foods Ingredients, Abbott Nutrition, Nestle Health Science, Fresenius Kabi, Nutricia, Reckitt, Ajinomoto, and DSM Nutritional Products. Companies in the Protein Hydrolysates for Inflammatory Bowel Disease Market are widening their market footprint by investing heavily in clinical research to validate therapeutic advantages and secure stronger medical acceptance. Many manufacturers are refining production technologies to enhance protein digestibility and reduce antigenicity, helping them meet the needs of patients with severe gastrointestinal challenges. Firms are also diversifying their portfolios with plant-based hydrolysates to align with rising consumer preference for vegan and vegetarian medical nutrition. Strategic collaborations with healthcare institutions, product innovation geared toward advanced enteral formulations, and expansion into high-growth regions are central to their competitive approach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Source material

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product Type, 2021-2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Extensively hydrolyzed protein products

- 5.3 Partially hydrolyzed protein products

- 5.4 Amino acid-based formulations

- 5.5 Others

Chapter 6 Market Size and Forecast, By Source Material, 2021-2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy-derived hydrolysates

- 6.2.1 Whey protein hydrolysates

- 6.2.2 Casein hydrolysates

- 6.2.3 Alpha-lactalbumin concentrates

- 6.2.4 Others

- 6.3 Plant-based hydrolysates

- 6.3.1 Rice protein hydrolysates

- 6.3.2 Pea protein hydrolysates

- 6.3.3 Soy protein hydrolysates

- 6.3.4 Others

- 6.4 Marine-derived hydrolysates

- 6.5 Others

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Enteral nutrition

- 7.3 Oral nutritional supplements

- 7.4 Medical foods

- 7.5 Others

Chapter 8 Market Size and Forecast, By End Use, 2021-2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Hospitals & clinical settings

- 8.3 Home healthcare

- 8.4 Specialized nutrition centers

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Kerry Group

- 10.2 Arla Foods Ingredients

- 10.3 Abbott Nutrition

- 10.4 Nestle Health Science

- 10.5 Fresenius Kabi

- 10.6 Nutricia

- 10.7 Reckitt

- 10.8 Ajinomoto

- 10.9 DSM Nutritional Products