|

시장보고서

상품코드

1892903

자동차 커튼 에어백 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Curtain Airbags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

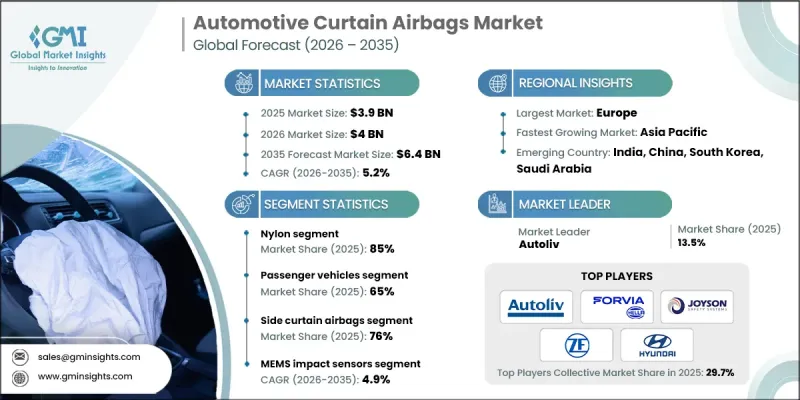

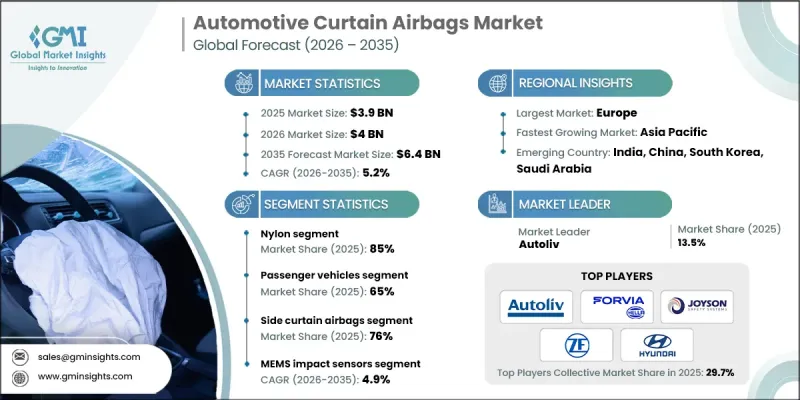

세계의 자동차 커튼 에어백 시장은 2025년에 39억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.2%를 나타내 64억 달러에 이를 것으로 예측됩니다.

SUV와 크로스오버 차량의 판매가 꾸준히 성장하고 있는 것이 주요 요인이며, 캐빈의 폭이 넓어지고 지붕 라인의 높이가 머리 보호 시스템의 필요성을 높이고 있습니다. 자동차 제조업체는 커튼 에어백을 더 많은 차량에 표준 장비로 순차적으로 도입하고 있으며 세계 경쟁력있는 가격으로 고급 안전 솔루션을 제공합니다. EV용 스케이트보드 플랫폼의 진화는 차량 구조를 변화시키고 센서와 안전 시스템의 배치 방법에 영향을 미치고 있습니다. 이 변화에 의해 커튼 에어백의 통합성이 향상해, 공급업체는 경량으로 컴팩트한 팽창 설계나, 한정된 캐빈 스페이스에서도 강력한 보호 성능을 발휘하는 개량형 섬유 소재의 개발을 추진하고 있습니다. 여러 지역에서 규제가 강화되는 가운데 OEM 제조업체는 거의 모든 차종 클래스에서 측면 충돌 보호 기능을 제공해야 합니다. 소비자의 차량안전성에 대한 관심 증가도 자동차 제조업체에 지역기준에 준거한 선진적인 수동안전시스템에 의한 라인업의 차별화를 촉구하고 있어 탑승자 보호를 중시하는 구매자층에 대한 소구력이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 39억 달러 |

| 예측 금액 | 64억 달러 |

| CAGR | 5.2% |

나일론 소재 부문은 2025년에 85%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 4.2%를 나타낼 것으로 예측됩니다. 나일론 폴리에스터 하이브리드, 차세대 나일론 배합, 바이오 폴리아미드의 향후 개발은 성능 향상과 지속가능성 목표 달성을 기대할 것입니다. 섬유 화학의 진보로 나일론과 대체 소재의 성능 차이는 계속 축소되고 있습니다.

승용차 부문은 2025년에 65%의 점유율을 차지했고 2026년부터 2035년에 걸쳐 CAGR 5.5%를 나타낼 것으로 예상됩니다. 채용 패턴은 차종 등급에 따라 다르다 : 고급차 모델에서는 커튼 에어백 시스템이 널리 채용되고 있는 한편, 중급차에서는 급속한 통합이 진행되고 있습니다. 엔트리 레벨 시장에서는 여전히 비용 제약이 있지만, 규제 요건의 강화와 세계 소비자의 안전 의식이 증가함에 따라 전반적인 채용은 증가하는 경향이 있습니다.

미국의 자동차 커튼 에어백 시장은 2025년 8억 7,150만 달러에 달했습니다. 규제 당국은 측면 충돌 및 방출 방지 시험의 요건을 확대하고 있으며, 제조업체에게 대형 SUV나 픽업 트럭에 최적화된 첨단 커튼 에어백의 채용을 촉구하고 있습니다. 이러한 업데이트된 시스템은 전통적인 설계보다 넓은 커버리지 범위와 탁월한 횡단 성능을 제공합니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률 분석

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 승무원 안전 기준에의 적합성에 대한 중요성 증가

- SUV 및 크로스오버 차량의 보급 확대

- 적응형 에어백 시스템의 기술적 진보

- 신흥 자동차 거점에서의 생산 확대

- 지속 가능한 소재로의 이행

- 업계의 잠재적 위험 및 과제

- 높은 시스템 통합성과 부품 비용

- 신흥 시장의 안전규제 부족

- 시장 기회

- 자율주행차 및 준자율주행차의 성장

- 애프터마켓용 교환부품 및 리콜에 따른 수요

- 상용차 및 플릿으로의 확대

- 지속가능성을 중시한 조달 시프트

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 - FMVSS 214 측면 충돌 보호

- 캐나다 - CMVSS 214 측면 충돌 보호

- 유럽

- 독일 - 유엔 규제135 폴사이드 충돌 보호 장치

- 영국 - UNECE 규제95 측면 충돌 보호

- 프랑스 - EU 일반 안전 규제 2019/2144

- 이탈리아 유엔 규제 21 실내 장비의 안전성

- 스페인 - EU 규정 661/2009 일반 차량 안전 기준

- 아시아태평양

- 중국 - GB 20071 측면 충돌 보호

- 인도 - AIS-099 측면 충돌 규제

- 일본 - JNCAP 측면 충돌 내성 시험 프로토콜

- 호주 - ADR 72 측면 충돌 보호

- 한국 - KMVSS 측면 충돌 보호

- 라틴아메리카

- 브라질- Contran 결의 518 측면 충돌 보호

- 멕시코 - NOM-194-SCFI 차량 안전 기준

- 아르헨티나 - IRAM-AITA 1-20 측면 충돌 기준

- 중동 및 아프리카

- 남아프리카 - SANS 20079 측면 충돌 보호

- 사우디아라비아 - SASO 2915 차량 안전 규제

- UAE - UAE.S 5010-5 차량 충돌 보호

- 튀르키예 - UNECE 규정 95 측면 충돌 보호 장치

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 현황

- 현행 기술

- 신흥 기술

- 가격 동향

- 제품별

- 지역별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 향후 시장 전망과 기회

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획과 자금 조달

제5장 시장 추계·예측 : 유형별(2022-2035년)

- 사이드 커튼 에어백

- 나일론

- 폴리에스터

- 프론트 커튼 에어백

- 나일론

- 폴리에스터

- 리어 커튼 에어백

- 나일론

- 폴리에스터

제6장 시장 추계·예측 : 재료별(2022-2035년)

- 나일론

- 폴리에스터

제7장 시장 추계·예측 : 센서별(2022-2035년)

- MEMS 충격 센서

- 롤오버 자이로 센서

- 통합 안전 ECU

제8장 시장 추계·예측 : 차량별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계·예측 : 판매 채널별(2021-2034년)

- OEM

- 애프터마켓

제10장 시장 추계·예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 포르투갈

- 크로아티아

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제11장 기업 프로파일

- 세계 기업

- Autoliv

- ZF Friedrichshafen

- Joyson Safety Systems

- Continental

- Hyundai

- Toyoda Gosei

- Daicel

- Bosch Passive Safety Systems

- Magna International

- Denso

- Valeo

- Delphi Automotive/BorgWarner

- 지역 제조업체

- Forvia Hella

- Kolon Industries

- Nihon Plast

- Porcher Industries

- Toray Industries

- Sumitomo

- SEIREN

- Toyota Boshoku

- Ashimori Industry

- U-Shin

- 신흥·틈새 기업

- Yanfeng Automotive Trim Systems

- Wuhu Ruili Automobile Airbag

- ARC Automotive

- Tata AutoComp Systems

- Ningbo Joyson Electronic

- Changzhou Changrui

The Global Automotive Curtain Airbags Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 6.4 billion by 2035.

Steady growth in SUV and crossover sales is a major driver, as wider cabins and taller rooflines increase the need for head protection systems. Automakers are progressively equipping more vehicles with curtain airbags as standard features, making advanced safety solutions available at competitive pricing worldwide. The evolution of EV skateboard platforms is reshaping vehicle architecture, influencing how sensors and safety systems are positioned. This shift enables better integration of curtain airbags, prompting suppliers to engineer lighter, compact inflatable designs and improved textile materials capable of providing strong protection in increasingly constrained cabin spaces. With global regulations tightening across multiple regions, OEMs are required to deliver side-impact protection across nearly all vehicle classes. Rising consumer focus on vehicle safety is also pushing automakers to differentiate their lineups with advanced passive safety systems that comply with regional standards and appeal to buyers who prioritize comprehensive occupant protection.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 5.2% |

The nylon material segment accounted for an 85% share in 2025 and is projected to grow at a CAGR of 4.2% through 2035. Future developments in nylon-polyester hybrids, next-generation nylon formulations, and bio-based polyamides are expected to improve performance while addressing sustainability goals. Advancements in fiber chemistry continue to narrow the performance gap between nylon and alternative materials.

The passenger vehicle segment held a 65% share in 2025 and is anticipated to grow at a CAGR of 5.5% from 2026 to 2035. Adoption patterns vary depending on vehicle class: high-end models have widespread use of curtain airbag systems, while mid-range vehicles have seen rapid integration. Entry-level markets still face cost limitations, but overall adoption is rising as regulatory requirements strengthen and as safety becomes a higher priority among consumers worldwide.

US Automotive Curtain Airbags Market reached USD 871.5 million in 2025. Regulatory authorities have been expanding requirements for side-impact and ejection mitigation testing, encouraging manufacturers to adopt more advanced curtain airbags optimized for larger SUVs and pickup trucks. These updated systems offer broader coverage and better rollover performance than earlier designs.

Key companies operating in the Automotive Curtain Airbags Market include Autoliv, Continental, Hella, Hyundai, Joyson Safety Systems, Kolon Industries, Neaton Auto Products Manufacturing, Toyoda Gosei, and ZF Friedrichshafen. Companies within the Automotive Curtain Airbags Market are strengthening their competitive presence by advancing material technology, reducing system weight, and developing compact inflators that improve deployment efficiency. Many manufacturers are collaborating closely with automakers to design airbag systems tailored to new EV platforms and evolving vehicle geometries. Investments in improved textile engineering, enhanced sensor integration, and high-performance inflator mechanisms form a major part of ongoing R&D. Firms are also prioritizing compliance with global regulatory updates to secure broader OEM adoption. Expanding production capacity in strategic regions, focusing on cost-efficient manufacturing, and ensuring consistent quality control help companies maintain strong international footprints.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022-2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Sensor

- 2.2.5 Vehicle

- 2.2.6 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing emphasis on occupant safety compliance

- 3.2.1.2 Rising adoption of SUVs and crossovers

- 3.2.1.3 Technological advancements in adaptive airbag systems

- 3.2.1.4 Production expansion in emerging automotive hubs

- 3.2.1.5 Shift toward sustainable materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration and component costs

- 3.2.2.2 Limited safety regulations in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in autonomous and semi-autonomous vehicles

- 3.2.3.2 Aftermarket replacement and recall-driven demand

- 3.2.3.3 Expansion into commercial vehicles and fleets

- 3.2.3.4 Sustainability-driven procurement shifts

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States- FMVSS 214 side impact protection

- 3.4.1.2 Canada- CMVSS 214 side impact protection

- 3.4.2 Europe

- 3.4.2.1 Germany-UN regulation 135 pole side impact protection

- 3.4.2.2 United Kingdom-UNECE regulation 95 lateral impact protection

- 3.4.2.3 France-EU general safety regulation 2019/2144

- 3.4.2.4 Italy-UN regulation 21 interior fittings safety

- 3.4.2.5 Spain-EU regulation 661/2009 general vehicle safety

- 3.4.3 Asia Pacific

- 3.4.3.1 China-GB 20071 side impact protection

- 3.4.3.2 India-AIS-099 side impact regulation

- 3.4.3.3 Japan-JNCAP side impact crashworthiness protocol

- 3.4.3.4 Australia-ADR 72 side impact protection

- 3.4.3.5 South Korea-KMVSS side impact crash protection

- 3.4.4 Latin America

- 3.4.4.1 Brazil-Contran resolution 518 side impact protection

- 3.4.4.2 Mexico-NOM-194-SCFI vehicle safety standard

- 3.4.4.3 Argentina-IRAM-AITA 1-20 side impact standard

- 3.4.5 Middle East & Africa

- 3.4.5.1 South Africa-SANS 20079 side impact protection

- 3.4.5.2 Saudi Arabia-SASO 2915 vehicle safety regulation

- 3.4.5.3 UAE-UAE.S 5010-5 vehicle crash protection

- 3.4.5.4 Turkey-UNECE regulation 95 side impact protection

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Price trends

- 3.8.1 By Product

- 3.8.2 By region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future market outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Side curtain airbags

- 5.2.1 Nylon

- 5.2.2 Polyester

- 5.3 Front curtain airbags

- 5.3.1 Nylon

- 5.3.2 Polyester

- 5.4 Rear curtain airbags

- 5.4.1 Nylon

- 5.4.2 Polyester

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Nylon

- 6.3 Polyester

Chapter 7 Market Estimates & Forecast, By Sensor, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 MEMS Impact Sensors

- 7.3 Rollover Gyro Sensors

- 7.4 Unified Safety ECUs

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCVs)

- 8.3.2 Medium commercial vehicles (MCVs)

- 8.3.3 Heavy commercial vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.3.10 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Autoliv

- 11.1.2 ZF Friedrichshafen

- 11.1.3 Joyson Safety Systems

- 11.1.4 Continental

- 11.1.5 Hyundai

- 11.1.6 Toyoda Gosei

- 11.1.7 Daicel

- 11.1.8 Bosch Passive Safety Systems

- 11.1.9 Magna International

- 11.1.10 Denso

- 11.1.11 Valeo

- 11.1.12 Delphi Automotive / BorgWarner

- 11.2 Regional Players

- 11.2.1 Forvia Hella

- 11.2.2 Kolon Industries

- 11.2.3 Nihon Plast

- 11.2.4 Porcher Industries

- 11.2.5 Toray Industries

- 11.2.6 Sumitomo

- 11.2.7 SEIREN

- 11.2.8 Toyota Boshoku

- 11.2.9 Ashimori Industry

- 11.2.10 U-Shin

- 11.3 Emerging & Niche Players

- 11.3.1 Yanfeng Automotive Trim Systems

- 11.3.2 Wuhu Ruili Automobile Airbag

- 11.3.3 ARC Automotive

- 11.3.4 Tata AutoComp Systems

- 11.3.5 Ningbo Joyson Electronic

- 11.3.6 Changzhou Changrui