|

시장보고서

상품코드

2019039

펠렛타이저 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Pelletizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

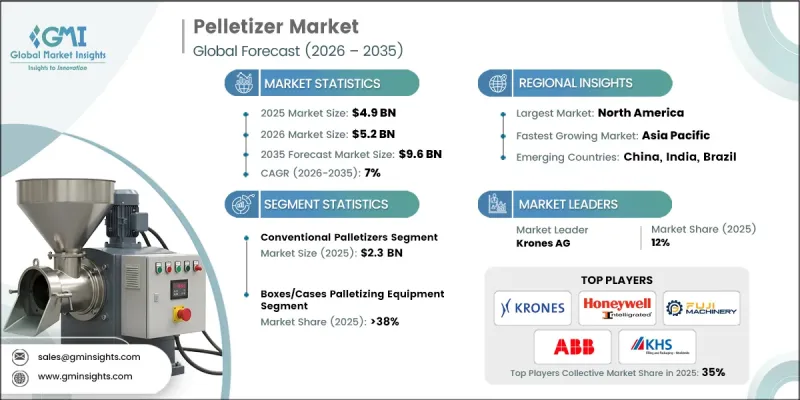

세계의 펠렛타이저 시장은 2025년에 49억 달러로 평가되었으며, CAGR 7%로 성장하여 2035년까지 96억 달러에 달할 것으로 예측됩니다.

기업들은 업무 효율성과 워크플로우의 일관성 향상에 초점을 맞추고 있으며, 이는 첨단 펠릿화 시스템의 도입을 촉진하고 있습니다. 과거에는 생산설비의 보조적인 존재로 여겨졌던 것이 이제는 일상적인 업무 관리와 늘어나는 생산량 처리에 필수적인 요소로 자리 잡고 있습니다. 공급망의 복잡성과 업무 효율성에 대한 기대치가 높아짐에 따라 기업들은 통합이 쉽고, 사용하기 쉽고, 다양한 생산 환경에 적응할 수 있는 시스템에 투자하고 있습니다. 또한, 작업장 안전과 안정적인 생산량에 대한 관심이 높아지면서 시스템 설계에 영향을 미치고 있으며, 제조업체들은 최소한의 모니터링으로 기존 설비에 원활하게 통합할 수 있는 솔루션을 개발하고 있습니다. 다양한 제품 형태에 대응할 수 있는 유연한 설비에 대한 수요 증가도 시장을 더욱 형성하고 있으며, 기업들은 효율성과 적응성의 균형 잡힌 기술을 모색하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 49억 달러 |

| 예측 규모 | 96억 달러 |

| CAGR | 7% |

기존 펠렛타이저 시장은 반복적이고 표준화된 대량 생산 환경에서 비용 효율성을 실현할 수 있다는 장점에 힘입어 2025년 23억 달러의 시장 규모를 기록했습니다. 이 시스템은 안정적인 생산 조건에 적합하며, 안정적인 처리 능력과 긴 작동 수명을 제공합니다. 기존 제조 레이아웃과의 호환성은 특히 인프라 업그레이드가 필요한 시설에서 그 입지를 더욱 확고히 하고 있습니다. 기존 시스템의 신뢰성과 내구성은 기존 산업 환경에서 폭넓게 채택되고 있습니다.

박스 및 케이스 부문은 2025년 38%의 점유율을 차지했습니다. 이 부문은 자동화된 생산 및 물류 프로세스에서 표준화된 포장 형태를 광범위하게 사용함으로써 여전히 지배적인 지위를 유지하고 있습니다. 균일한 구조로 자동화 시스템 내에서 효율적인 취급과 업무의 합리화를 가능하게 합니다. 이 부문을 위해 설계된 장비는 다른 포장 공정과 효과적으로 통합되어 전반적인 운영 효율성을 향상시킵니다. 구조화된 포장 형태에 대한 지속적인 의존도가 더 넓은 시장 환경에서 이 부문의 확고한 지위를 뒷받침하고 있습니다.

미국 펠렛타이저 시장은 84%의 점유율을 차지하며 2025년 13억 달러의 시장 규모를 기록했습니다. 한국은 제조 및 물류 부문 전반에서 높은 자동화 도입률로 인해 선도적인 위치를 유지하고 있습니다. 인력 확보와 안전 기준에 대한 지속적인 이슈가 자동화 솔루션으로의 전환을 가속화하고 있습니다. 탄탄한 산업 인프라와 첨단 기술에 대한 지속적인 투자가 시장 성장을 더욱 촉진하고 있습니다. 확립된 자동화 생태계의 존재는 혁신을 촉진하고 다양한 산업에서 펠릿화 시스템의 광범위한 도입을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 취급 능력별, 2022-2035

제7장 시장 추정 및 예측 : 통합 유형별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

제10장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM 26.05.06The Global Pelletizer Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.6 billion by 2035.

Businesses are focusing on streamlining operations and improving workflow consistency, which is driving the adoption of advanced pelletizing systems. What was once considered a supplementary addition to production facilities is now becoming a critical component in managing daily operations and handling increasing production volumes. Rising complexity in supply chains and higher expectations for operational efficiency are encouraging companies to invest in systems that are easy to integrate, user-friendly, and adaptable to different production environments. In addition, the growing emphasis on workplace safety and consistent output is influencing system design, with manufacturers developing solutions that require minimal supervision and fit seamlessly into existing setups. Increasing demand for flexible equipment capable of handling varied product formats is further shaping the market, as businesses seek technologies that balance efficiency with adaptability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 7% |

The conventional pelletizers segment generated USD 2.3 billion in 2025, supported by their ability to deliver cost efficiency in high-volume production environments where operations are repetitive and standardized. These systems are well-suited for consistent production conditions, offering reliable throughput and long operational lifespans. Their compatibility with established manufacturing layouts further strengthens their position, particularly in facilities where upgrading infrastructure may present challenges. The dependability and durability of conventional systems continue to support their widespread adoption across established industrial environments.

The boxes and cases segment accounted for 38% share in 2025. This segment remains dominant due to the widespread use of standardized packaging formats in automated production and logistics processes. Their uniform structure allows for efficient handling and streamlined operations within automated systems. Equipment designed for this segment integrates effectively with other packaging processes, enhancing overall operational efficiency. The continued reliance on structured packaging formats supports the segment's strong position within the broader market landscape.

United States Pelletizer Market held an 84% share, generating USD 1.3 billion in 2025. The country maintains its leadership due to a high level of automation adoption across the manufacturing and logistics sectors. Ongoing challenges related to labor availability and safety standards are accelerating the shift toward automated solutions. Strong industrial infrastructure and continued investment in advanced technologies are further reinforcing market growth. The presence of established automation ecosystems supports innovation and widespread implementation of pelletizing systems across various industries.

Key companies operating in the Global Pelletizer Market include ABB Group, Krones AG, Fanuc Corporation, Kuka AG, BEUMER Group GmbH & Co. KG, Columbia Machine, Inc., Premier Tech Chronos, Schneider Packaging Equipment Co., Inc., Honeywell Intelligrated, ARPAC LLC, Gebo Cermex (part of Sidel Group), Brenton Engineering (part of ProMach), Fuji Machinery Co., Ltd., Intralox, LLC (part of Laitram, LLC), and KHS GmbH. Companies in the Global Pelletizer Market are strengthening their competitive position through technological innovation and strategic expansion initiatives. They are investing in advanced automation technologies to improve system efficiency, flexibility, and ease of integration. Expanding product portfolios to address diverse industry requirements is a key focus area. Businesses are also forming strategic partnerships and collaborations to enhance market reach and improve service capabilities. In addition, companies are emphasizing user-friendly designs and customizable solutions to meet evolving customer demands. Strengthening after-sales support and maintenance services is another important strategy to build long-term customer relationships.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Key Trends

- 2.2.1 Region

- 2.2.2 Product type

- 2.2.3 Handling capacity

- 2.2.4 Integration type

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Ecosystem mapping

- 3.1.1.1 OEM

- 3.1.1.2 Integrators

- 3.1.1.3 End-users

- 3.1.1.4 Component suppliers

- 3.1.2 Stakeholder interdependence

- 3.1.3 Value chain analysis (Driven by Primary Research)

- 3.1.3.1 Value chain stages: manufacturing, distribution, installation, aftermarket

- 3.1.3.2 Profit margin analysis by value chain stage

- 3.1.3.3 Value capture mechanisms

- 3.1.1 Ecosystem mapping

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation adoption across manufacturing and warehousing

- 3.2.1.2 Growing e-commerce and need for high-speed material handling

- 3.2.1.3 Increasing focus on workplace safety and ergonomics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and integration costs

- 3.2.2.2 Need for skilled technicians and maintenance personnel

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of robotic and collaborative palletizing solutions

- 3.2.3.2 Integration of ai, vision systems, and smart analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 High-growth regional opportunities

- 3.3.2 High-growth segment opportunities

- 3.3.3 Emerging application verticals

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Emerging technology trends

- 3.5.2 Innovation roadmap by technology type

- 3.5.3 Technology adoption curves by region

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2022-2025)

- 3.6.2 Price variation by technology type (Robotic vs Conventional Automated)

- 3.6.3 Regional pricing dynamics

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade data analysis (driven by primary research) (HS Code: 8479)

- 3.8.1 Import/Export volume and value trends

- 3.8.2 Key trade corridors and tariff impact

- 3.8.3 Cross-border equipment flow patterns

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing palletizer business models

- 3.9.2 GenAI use cases and adoption roadmaps (predictive maintenance, route optimization)

- 3.9.3 Risks, limitations and regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Company tier benchmarking (Driven by Primary Research)

- 4.5.1 Tier classification criteria and qualifying thresholds

- 4.5.2 Tier positioning matrix

- 4.5.3 Brands positioning of BW Packaging against Competitors

- 4.6 Competitive positioning matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Robotic palletizers

- 5.2.1 Articulated arm robots (4/5/6-axis)

- 5.2.2 Gantry/portal robots

- 5.2.3 Collaborative robots (cobots)

- 5.3 Conventional palletizers (non-robotic)

- 5.3.1 Mechanical layer formers

- 5.3.2 In-line conventional systems

- 5.4 Semi-Automated palletizers

- 5.5 Manual palletizers

Chapter 6 Market Estimates & Forecast, By Handling Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low-speed palletizers (up to 10 cases/min)

- 6.3 Medium-speed palletizers (10-25 cases/min)

- 6.4 High-speed palletizers (25-50 cases/min)

- 6.5 Ultra-high-speed palletizers

Chapter 7 Market Estimates & Forecast, By Integration Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Standalone palletizing cells

- 7.3 Integrated in-line systems

- 7.4 End-of-line palletizing

- 7.5 Multi-line palletizing

- 7.6 Mobile/flexible units

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Bags palletizing equipment

- 8.3 Boxes/cases palletizing equipment

- 8.4 Bottles/containers palletizing equipment

- 8.5 Drums/kegs palletizing equipment

- 8.6 Trays palletizing equipment

- 8.7 Mixed material handling systems

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals

- 9.4 Consumer goods

- 9.5 Building materials

- 9.6 Chemicals

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB Group

- 12.2 ARPAC LLC

- 12.3 BEUMER Group GmbH & Co. KG

- 12.4 Brenton Engineering (part of ProMach)

- 12.5 Columbia Machine, Inc.

- 12.6 Fanuc Corporation

- 12.7 Fuji Machinery Co., Ltd.

- 12.8 Gebo Cermex (part of Sidel Group)

- 12.9 Honeywell Intelligrated

- 12.10 Intralox, LLC (part of Laitram, LLC)

- 12.11 KHS GmbH

- 12.12 Krones AG

- 12.13 Kuka AG

- 12.14 Premier Tech Chronos

- 12.15 Schneider Packaging Equipment Co., Inc.