|

시장보고서

상품코드

2019205

군사 위성 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Military Satellite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

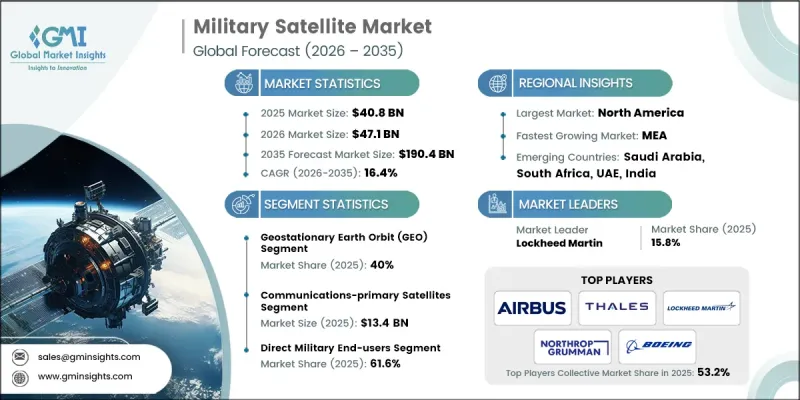

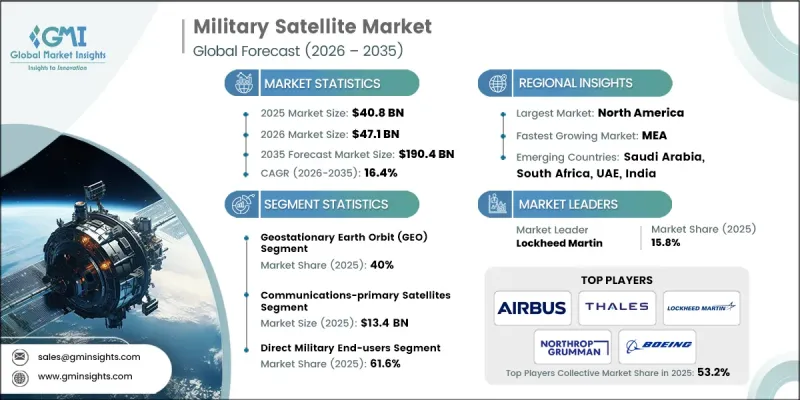

세계의 군사 위성 시장은 2025년에 408억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.4%로 성장하여 1,904억 달러에 이를 것으로 추정되고 있습니다.

시장의 급속한 성장은 지정학적 긴장이 고조되고, 안전하고 장애에 강하며 기술적으로 진보된 우주 기반 시스템에 대한 수요가 증가함에 따라 촉진되고 있습니다. 군 조직은 정보, 감시, 정찰(ISR), 미사일 경보 및 감지, 보안 통신, 통합 지휘통제 작전을 위해 위성을 우선적으로 활용하고 있습니다. 현대의 국방 전략은 육상, 공중, 해상, 사이버, 우주 등 각 영역의 상호 운용성을 보장하기 위해 위성을 다영역 작전에 통합하는 것을 점점 더 많이 추진하고 있습니다. 각국 정부는 실시간 군사 작전, 전략적 상황 인식 및 신속한 위협 대응을 지원하기 위해 소형 위성 별자리, 첨단 발사 기술 및 내결함성 통신 네트워크에 투자하고 있습니다. 우주 영역 인식, 위성 생존성 및 궤도 혼잡 관리의 중요성이 증가함에 따라 우주 자산은 전 세계 국가 안보 및 전략적 방어 능력의 초석이 되고 있으며, 이에 대한 투자도 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 408억 달러 |

| 예측액 | 1,904억 달러 |

| CAGR | 16.4% |

2025년에는 정지궤도(GEO) 부문이 시장 점유율의 40%를 차지하며 통신, 항법, ISR(정보, 감시, 정찰), 미사일 경보 기능에서 지속적인 세계 커버리지를 제공할 수 있다는 점에서 이 분야를 주도할 것으로 예측됩니다. GEO 위성은 궤도상의 위치를 고정하고 유지하며, 감시, 군사 지휘 및 전략 작전에 대한 지속적인 지원을 제공합니다. 장기적인 관찰이나 끊김 없는 통신 링크가 필요한 용도에서 선호되고 있습니다.

미사일 경계를 주 목적으로 하는 위성 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 18.7%를 나타낼 것으로 예측됩니다. 이러한 성장은 조기 경보 시스템, 세계 미사일 감지 네트워크, 전략적 방어 이니셔티브에 대한 투자 확대에 힘입어 이루어졌습니다. 이 분야는 고해상도 적외선 센서, 저지연 데이터 전송 및 실시간 위협 모니터링의 발전으로 인해 군이 미사일 위협과 잠재적 보안 침해에 신속하게 대응할 수 있게 되었습니다.

2025년 기준 북미 군사 위성 시장은 42.2%의 점유율을 차지했습니다. 이 지역의 성장은 군사비 증가, 지속적인 지정학적 긴장, 안전하고 장애에 강한 우주 통신 시스템의 필요성에 의해 뒷받침되고 있습니다. 저궤도(LEO) 별자리, 우주 상황 인식 및 안전한 통신 플랫폼에 대한 투자가 시장 확대에 기여하고 있습니다. 또한, 이 지역은 첨단 항공우주 인프라, 숙련된 인력, 그리고 강력한 국방 연구개발 능력의 혜택을 누리고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 궤도 분류별, 2022-2035

제6장 시장 추산 및 예측 : 주요 임무별, 2022-2035

제7장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSHThe Global Military Satellite Market was valued at USD 40.8 billion in 2025 and is estimated to grow at a CAGR of 16.4% to reach USD 190.4 billion by 2035.

The market's rapid growth is fueled by increasing geopolitical tensions and the rising demand for secure, resilient, and technologically advanced space-based systems. Military organizations are prioritizing satellites for intelligence, surveillance, reconnaissance (ISR), missile warning and detection, secure communications, and integrated command-and-control operations. Modern defense strategies are increasingly integrating satellites into multi-domain operations to ensure interoperability across land, air, sea, cyber, and space. Governments are investing in small satellite constellations, advanced launch technologies, and resilient communication networks to support real-time military operations, strategic situational awareness, and rapid threat response. The rising importance of space domain awareness, satellite survivability, and orbital congestion management also drives investment, making space-based assets a cornerstone of national security and strategic defense capabilities worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.8 Billion |

| Forecast Value | $190.4 Billion |

| CAGR | 16.4% |

The geostationary earth orbit (GEO) segment accounted for 40% share in 2025, leading the sector due to its ability to provide persistent global coverage across communications, navigation, ISR, and missile warning functions. GEO satellites maintain fixed orbital positions, delivering enduring support for surveillance, military command, and strategic operations. They are preferred for applications requiring long-term observation and uninterrupted communication links.

The missile warning-primary satellites segment is expected to grow at a CAGR of 18.7% during 2026-2035. Growth is driven by increasing investments in early warning systems, global missile detection networks, and strategic defense initiatives. The sector benefits from advancements in high-resolution infrared sensors, low-latency data transmission, and real-time threat monitoring, enabling militaries to rapidly detect and respond to missile threats and potential security breaches.

North America Military Satellite Market held 42.2% share in 2025. The region's growth is supported by elevated military spending, ongoing geopolitical tensions, and the need for secure, resilient, space-based communication systems. Investments in low Earth orbit (LEO) constellations, space situational awareness, and secure communications platforms contribute to market expansion. The region also benefits from advanced aerospace infrastructure, skilled workforce, and strong defense research and development capabilities.

Prominent players operating in the Global Military Satellite Market include Airbus, Boeing, Lockheed Martin, BAE Systems, Northrop Grumman, Thales, General Dynamics Mission Systems, Inc., Elbit Systems, Viasat, Israel Aerospace Industries, China Aerospace Science and Technology Corporation, and SpaceX. Key strategies employed by companies in the military satellite market focus on technological innovation, strategic partnerships, and portfolio diversification. Firms are investing heavily in next-generation satellites, high-resolution sensors, and secure communication payloads to meet evolving defense needs. Companies form alliances with governments, defense contractors, and launch service providers to secure contracts and expand market reach. Emphasis on research and development enables the creation of modular, multi-mission satellite platforms capable of ISR, communications, and missile defense. Additionally, companies pursue geographic expansion, cost optimization, and after-sales service networks to enhance operational efficiency and strengthen long-term market presence. Competitive differentiation is achieved through proprietary technologies, space situational awareness capabilities, and enhanced satellite survivability in contested orbital environments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Orbital Classification trends

- 2.2.2 Primary mission trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising geopolitical tensions driving secure military satellite communications

- 3.2.1.2 Expansion of space-based missile warning and detection capabilities

- 3.2.1.3 Advancements in small satellites and reusable launch technologies

- 3.2.1.4 Integration of satellites into multi-domain military operations

- 3.2.1.5 Growing reliance on satellite-based intelligence surveillance and reconnaissance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs for satellite development launch and maintenance

- 3.2.2.2 Threats from cyberattacks, jamming and anti-satellite weapons

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of low Earth orbit defense constellations

- 3.2.3.2 Growing public-private partnerships in military satellite programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense Budget Analysis

- 3.9 Global Defense Spending Trends

- 3.10 Regional Defense Budget Allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Key Defense Modernization Programs

- 3.12 Budget Forecast (2026-2035)

- 3.12.1 Impact on Industry Growth

- 3.12.2 Defense Budgets by Country

- 3.13 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.14 Risk Assessment and Management

- 3.15 Major Contract Awards (2022-2025)

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Orbital Classification, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Low earth orbit (LEO)

- 5.3 Medium earth orbit (MEO)

- 5.4 Geostationary earth orbit (GEO)

- 5.5 Highly elliptical orbit (HEO)

Chapter 6 Market Estimates and Forecast, By Primary Mission, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Communications-primary satellites

- 6.3 Intelligence & surveillance-primary satellites

- 6.4 Navigation & timing-primary satellites

- 6.5 Missile warning-primary satellites

- 6.6 Space situational awareness-primary satellites

- 6.7 Multi-mission satellites

Chapter 7 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Direct military end-users

- 7.3 Intelligence & security agencies

- 7.4 International military organizations

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Airbus

- 9.1.2 Boeing

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Lockheed Martin

- 9.2.1.2 Northrop Grumman

- 9.2.1.3 SpaceX

- 9.2.2 Asia Pacific

- 9.2.2.1 China Aerospace Science and Technology Corporation

- 9.2.2.2 General Dynamics Mission Systems, Inc.

- 9.2.2.3 Viasat

- 9.2.3 Europe

- 9.2.3.1 BAE Systems

- 9.2.3.2 Elbit Systems

- 9.2.3.3 Thales

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Israel Aerospace Industries