|

시장보고서

상품코드

1936011

고급 분석 시장 : 제공별, 딜리버리 방식별 - 세계 예측(-2031년)Advanced Analytics Market by Offering (Agentic (Copilots, Assistants, Autonomous Analytics Agents), Augmented (Insight Discovery, Automation, Orchestration), Predictive, Prescriptive), Delivery Mode (Cloud & Lakehouse, Edge) - Global Forecast to 2031 |

||||||

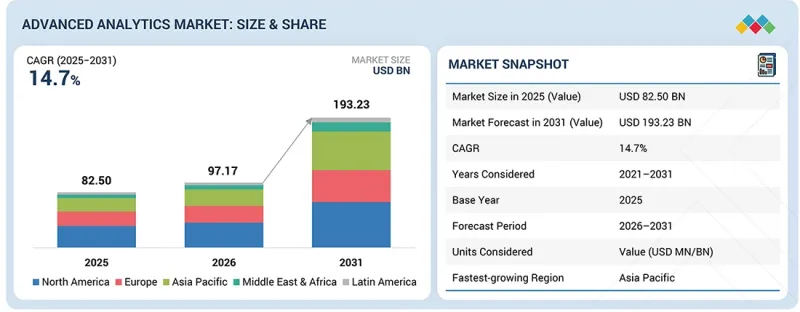

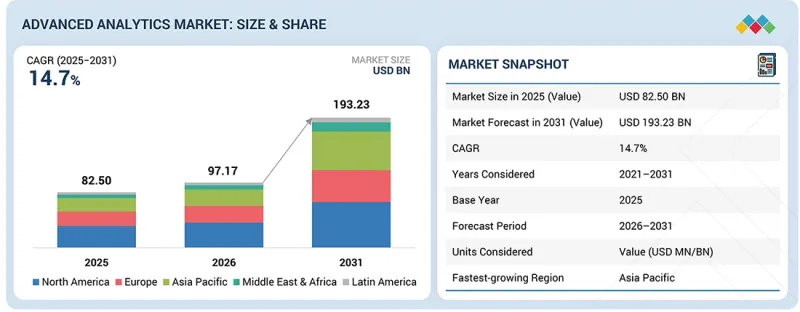

세계의 고급 분석 시장 규모는 2026년 971억 7,000만 달러에서 2031년까지 1,932억 3,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 14.7%의 성장이 전망됩니다.

주요 촉진요인으로는 기업의 데이터 양 증가, AI 및 클라우드 플랫폼 도입 확대, 그리고 산업 전반에 걸쳐 보다 신속하고 정확한 비즈니스 의사결정에 대한 요구가 증가하고 있는 점을 들 수 있습니다. 조직은 효율성 향상, 비용 절감, 리스크 관리를 위해 핵심 업무에 애널리틱스를 통합하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러 |

| 부문 | 제공, 딜리버리 방식, 용도, 업계, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

그러나 데이터 품질 문제, 레거시 시스템 간 통합의 복잡성, 숙련된 분석 전문가 부족 등 시장 성장을 저해하는 요인들이 존재합니다. 데이터 프라이버시, 모델 설명 가능성, 규제 준수에 대한 우려도 특정 규제 산업에서 채택을 지연시키는 요인으로 작용하고 있으며, 벤더들은 거버넌스 및 보안 기능에 대한 투자를 요구받고 있습니다.

"지능형 의사결정 자동화는 가장 높은 성장률을 보이는 응용 분야입니다."

용도별로는 지능형 의사결정 자동화 부문이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다. 기업들은 인사이트를 넘어 가격 책정, 부정 방지, IT 운영, 공급망 관리 등의 분야에서 자동으로 조치를 권장하거나 실행할 수 있는 시스템으로 전환하고 있습니다. 이러한 성장은 의사결정의 지연을 줄이고, 복잡성을 관리하며, 인적 개입을 최소화하면서 대규모로 운영해야 할 필요성에 의해 촉진되고 있습니다. AI 기반 의사결정 엔진, 규칙 오케스트레이션, 클로즈드 루프 분석을 통해 조직은 변화하는 상황에 실시간으로 대응할 수 있습니다. 기업들이 정적인 보고가 아닌 측정 가능한 성과를 추구함에 따라 지능형 의사결정 자동화는 분석 벤더들에게 중요한 성장 경로가 되고 있습니다.

"머신러닝 기반 분석이 2026년 솔루션 제공에서 우위를 점합니다."

솔루션 제공별로 보면 머신러닝 기반 분석 부문이 2026년 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이러한 우위는 재무, 운영, 고객 인텔리전스, 리스크 관리 분야에서 예측 분석과 처방적 분석을 광범위하게 채택함으로써 뒷받침되고 있습니다. 머신러닝을 통해 조직은 숨겨진 패턴을 발견하고, 결과를 예측하고, 대규모 의사결정을 최적화할 수 있습니다. 각 벤더들은 AutoML, 모델 관리, AI 지원 분석 기능을 통해 이 부문을 강화하여 사용자의 기술적 장벽을 낮추고 있습니다. 기업이 정확성, 확장성, 지속적인 학습을 우선시하는 가운데, 머신러닝 기반 분석은 산업을 막론하고 첨단 분석의 핵심 요소로 자리 잡고 있습니다.

"북미가 규모를 주도하고, 아시아태평양이 성장을 가속화합니다."

북미는 가장 큰 고급 분석 시장으로, 초기 기술 도입, 강력한 기업 IT 지출, 주요 분석 클라우드 벤더의 존재에 의해 주도되고 있습니다. BFSI, 의료, 소매, 기술 분야의 기업들은 첨단 분석을 업무에 깊숙이 통합하고 있습니다. 한편, 아시아태평양은 예측 기간 동안 가장 빠른 성장이 예상되는 지역입니다. 급속한 디지털화, 클라우드 인프라의 확대, 정부 주도의 기술 관련 노력, 기업 전반의 AI 도입 증가로 인해 분석에 대한 투자가 가속화되고 있습니다. 이러한 지역적 추세는 북미의 성숙한 수익 기반과 아시아태평양의 강력한 미래 성장 모멘텀을 강조하고 있습니다.

세계의 고급 분석 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 전략적 파괴 : 특허, 디지털, AI 채용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 고급 분석 시장 : 제공별

제10장 고급 분석 시장 : 딜리버리 방식별

제11장 고급 분석 시장 : 용도별

제12장 고급 분석 시장 : 업계별

제13장 고급 분석 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.02.27The advanced analytics market is projected to grow from USD 97.17 billion in 2026 to USD 193.23 billion by 2031, at a CAGR of 14.7% during the forecast period. Key drivers include rising enterprise data volumes, growing adoption of AI and cloud platforms, and demand for faster, more accurate business decisions across industries. Organizations are embedding analytics into core operations to improve efficiency, reduce costs, and manage risk.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | USD (Billion) |

| Segments | Offering, Delivery Mode, Application, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

However, market growth faces restraints such as data quality challenges, integration complexity across legacy systems, and shortages of skilled analytics professionals. Concerns around data privacy, model explainability, and regulatory compliance also slow adoption in certain regulated industries, requiring vendors to invest in governance and security capabilities.

"Intelligent decision automation to be the fastest-growing application segment"

By application, the intelligent decision automation segment is expected to witness the highest growth rate during the forecast period. Enterprises are moving beyond insights toward systems that can automatically recommend or execute actions in areas such as pricing, fraud prevention, IT operations, and supply chain management. The growth is driven by the need to reduce decision latency, manage complexity, and operate at scale with limited human intervention. AI-driven decision engines, rules orchestration, and closed-loop analytics are enabling organizations to respond in real time to changing conditions. As enterprises seek measurable outcomes rather than static reporting, intelligent decision automation is becoming a critical growth avenue for analytics vendors.

"Machine learning driven analytics to dominate solution offerings in 2026"

By solution offering, the machine learning driven analytics segment is estimated to hold the largest market share in 2026. This dominance is supported by widespread adoption of predictive and prescriptive analytics across finance, operations, customer intelligence, and risk management. Machine learning enables organizations to uncover hidden patterns, forecast outcomes, and optimize decisions at scale. Vendors are strengthening this segment through AutoML, model management, and AI-assisted analytics capabilities that lower technical barriers for users. As enterprises prioritize accuracy, scalability, and continuous learning, machine learning-driven analytics remains the backbone of advanced analytics deployments across industries.

"North America leads in scale while Asia Pacific accelerates in growth"

North America represents the largest advanced analytics market, driven by early technology adoption, strong enterprise IT spending, and the presence of major analytics and cloud vendors. Enterprises across the BFSI, healthcare, retail, and technology sectors have deeply embedded advanced analytics into operations. In contrast, Asia Pacific is expected to be the fastest-growing region during the forecast period. Rapid digitalization, expanding cloud infrastructure, government-led technology initiatives, and increasing adoption of AI across enterprises are accelerating analytics investments. Together, these regional dynamics highlight a mature revenue base in North America and strong future growth momentum in Asia Pacific.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the advanced analytics market.

- By Company: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: Directors - 25%, Managers - 35%, and Others - 40%

- By Region: North America - 40%, Europe - 22%, Asia Pacific - 26%, Middle East & Africa - 5%, and Latin America - 7%

The report includes the study of key players offering advanced analytics solutions and services. It profiles major vendors in the advanced analytics market. The major players in the market include IBM (US), Microsoft (US), Google (US), Palantir (US), Oracle (US), SAS Institute (US), SAP (Germany), Adobe (US), Zoho (India), Sisense (US), Workday (US), Infor (US), Epic Systems (US), Savant Labs (US), AWS (US), Mu Sigma (US), Splunk (US), Strategy (US), Teradata (US), Qlik (US), Pegasystems (US), Fractal Analytics (US), Salesforce (US), NICE (Israel), FICO (US), Altair (US), Celonis (Germany), TIBCO (US), Alteryx (US), Anaplan (US), Databricks (US), Moody's Analytics (US), Dataiku (US), C3 AI (US), Domo (US), Snowflake (US), ThoughtSpot (US), GoodData (US), DataRobot (US), Yellowfin (Australia), ServiceNow (US), H2O.ai (US), Domino Data Lab (US), KNIME (Switzerland), Accenture (Ireland), Deloitte (UK), Capgemini (France), and Cognizant (US).

Research Coverage

This research report covers the advanced analytics market and is segmented by offering, delivery mode, application, and vertical. The offering segment comprises solutions and services. The solution segment contains Rule-based & Statistical Analytics, Machine Learning Driven Analytics, Augmented & Decision-centric Analytics, and Agentic & Autonomous Analytics. The delivery mode segment includes Standalone Analytics Software, Embedded & In-application Delivery, Cloud-native & Lakehouse-based Delivery, Edge & Distributed Analytics Delivery, and Agent-based & Autonomous Delivery Models. The application segment includes Customer & Revenue Intelligence, Financial Risk & Performance Management, Supply Chain & Operations Intelligence, Process & Quality Management, Human Capital Analytics, Product, Digital, & IT Operations Analytics, and Intelligent Decision Automation. The vertical segment includes BFSI, Healthcare & Life Sciences, Retail & E-commerce, Manufacturing, Telecommunications, Energy & Utilities, Media & entertainment, Government & Public Sector, Transportation & Mobility, Technology & Software, and Other Verticals. The regional analysis of the advanced analytics market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall advanced analytics market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (analytics revenue is now directly attributed to AI workloads, analytics is embedded inside core enterprise software, consulting & services revenue confirms analytics demand is execution-led), restraints (advanced analytics fails without data engineering spend, data governance, security, and compliance overhead), opportunities (shift from descriptive to prescriptive & decision automation, vertical-specific analytics monetization, consumption-based pricing aligns analytics spend with value), and challenges (analytics ROI is difficult to attribute at enterprise scale, fragmentation of the analytics stack)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the advanced analytics market

- Market Development: Comprehensive information about lucrative markets; the report analyzes the advanced analytics market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the advanced analytics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like IBM (US), Microsoft (US), Google (US), Palantir (US), Oracle (US), SAS Institute (US), SAP (Germany), Adobe (US), Zoho (India), Sisense (US), Workday (US), Infor (US), Epic Systems (US), Savant Labs (US), AWS (US), Mu Sigma (US), Splunk (US), Strategy (US), Teradata (US), Qlik (US), Pegasystems (US), Fractal Analytics (US), Salesforce (US), NICE (Israel), FICO (US), Altair (US), Celonis (Germany), TIBCO (US), Alteryx (US), Anaplan (US), Databricks (US), Moody's Analytics (US), Dataiku (US), C3 AI (US), Domo (US), Snowflake (US), ThoughtSpot (US), GoodData (US), DataRobot (US), Yellowfin (Australia), ServiceNow (US), H2O.ai (US), Domino Data Lab (US), KNIME (Switzerland), Accenture (Ireland), Deloitte (UK), Capgemini (France), and Cognizant (US) among others in the advanced analytics market. The report also helps stakeholders understand the pulse of the market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ADVANCED ANALYTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES IN ADVANCED ANALYTICS MARKET

- 3.2 ADVANCED ANALYTICS MARKET, BY REGION

- 3.3 ADVANCED ANALYTICS MARKET: TOP THREE SOLUTIONS

- 3.4 NORTH AMERICA: ADVANCED ANALYTICS MARKET, BY DELIVERY MODE AND APPLICATION

- 3.5 ADVANCED ANALYTICS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Alignment with AI spending cycles is re-prioritizing analytics investment

- 4.2.1.2 Platform-centric enterprise architectures are reshaping analytics procurement

- 4.2.1.3 Agentic and autonomous analytics enabling self-directed intelligence

- 4.2.2 RESTRAINTS

- 4.2.2.1 Advanced analytics fails without data engineering spend

- 4.2.2.2 Data governance, security, and compliance overhead

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Shift from descriptive to prescriptive & decision automation

- 4.2.3.2 Vertical-specific analytics monetization

- 4.2.3.3 Consumption-based pricing aligns analytics spend with value

- 4.2.4 CHALLENGES

- 4.2.4.1 Analytics RoI difficult to attribute at enterprise scale

- 4.2.4.2 Fragmentation of analytics stack

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ADVANCED ANALYTICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITION RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AI INDUSTRY

- 5.2.4 TRENDS IN GLOBAL BIG DATA & ANALYTICS INDUSTRY

- 5.3 ECOSYSTEM ANALYSIS

- 5.3.1 SOLUTION PROVIDERS

- 5.3.1.1 Rule-based & statistical analytics providers

- 5.3.1.2 Machine learning-driven analytics providers

- 5.3.1.3 Augmented & decision-centric analytics providers

- 5.3.1.4 Agentic & autonomous analytics providers

- 5.3.2 SERVICE PROVIDERS

- 5.3.2.1 Professional service providers

- 5.3.2.2 Managed service providers

- 5.3.1 SOLUTION PROVIDERS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2026

- 5.5.2 AVERAGE SELLING PRICE OF SOLUTIONS, BY APPLICATION, 2026

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 ZYNEX DRIVING 60% ANALYTICS COST SAVINGS THROUGH SAVANT LABS

- 5.7.2 HOLCIM ENABLING REAL-TIME PREDICTIVE MAINTENANCE ACROSS INDUSTRIAL ASSETS USING C3 AI

- 5.7.3 TRANSFORMING END-TO-END BUSINESS PROCESSES THROUGH PROCESS INTELLIGENCE

- 5.7.4 ROKU ENHANCING FINANCIAL PLANNING AGILITY WITH SCALABLE SCENARIO MODELING

- 5.7.5 STRENGTHENING FRAUD DETECTION WITH AGENTIC AI-DRIVEN DECISION INTELLIGENCE

- 5.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

6 STRATEGIC DISRUPTION: PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY TECHNOLOGIES

- 6.1.1 DATA MINING

- 6.1.2 DATA STREAM PROCESSING

- 6.1.3 DECISION ANALYTICS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIG DATA TECHNOLOGIES

- 6.2.2 CLOUD COMPUTING

- 6.2.3 BUSINESS INTELLIGENCE

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 MACHINE LEARNING

- 6.3.2 ARTIFICIAL INTELLIGENCE (AI)

- 6.3.3 INTERNET OF THINGS (IOT)

- 6.4 PATENT ANALYSIS

- 6.4.1 METHODOLOGY

- 6.4.2 PATENTS FILED

- 6.4.3 INNOVATION AND PATENT APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON ADVANCED ANALYTICS MARKET

- 6.5.1 BEST PRACTICES IN ADVANCED ANALYTICS MARKET

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN ADVANCED ANALYTICS MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ADVANCED ANALYTICS MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATIONS

- 7.1.2.1 North America

- 7.1.2.1.1 Securities Exchange Act of 1934 (SEC)

- 7.1.2.1.2 Artificial Intelligence and Data Act-AIDA (Canada)

- 7.1.2.1.3 Commodity Exchange Act (CFTC)

- 7.1.2.1.4 PIPEDA (Canada)

- 7.1.2.2 Europe

- 7.1.2.2.1 Europe Artificial Intelligence Act (European Union)

- 7.1.2.2.2 General Data Protection Regulation (European Union)

- 7.1.2.2.3 Data Protection Act 2018 (UK)

- 7.1.2.2.4 Federal Data Protection Act (Germany)

- 7.1.2.2.5 Personal Data Protection Code-Legislative Decree 196/2003 (Italy)

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 PDPA (Singapore)

- 7.1.2.3.2 Digital Personal Data Protection Act, 2023 (India)

- 7.1.2.3.3 Act on Protection of Personal Information (Japan)

- 7.1.2.3.4 Basic Act on Artificial Intelligence (South Korea)

- 7.1.2.4 Middle East & Africa

- 7.1.2.4.1 Federal Decree-Law No. 45 of 2021 on Protection of Personal Data (UAE)

- 7.1.2.4.2 Personal Data Protection Law (KSA)

- 7.1.2.4.3 Protection of Personal Information Act (South Africa)

- 7.1.2.4.4 Personal Data Privacy Protection Law (Qatar)

- 7.1.2.4.5 Law on Protection of Personal Data No. 6698 (Turkey)

- 7.1.2.5 Latin America

- 7.1.2.5.1 General Data Protection Law - LGPD (Brazil)

- 7.1.2.5.2 Federal Law on Protection of Personal Data Held by Private Parties (Mexico)

- 7.1.2.5.3 Personal Data Protection Law No. 25,326 (Argentina)

- 7.1.2.1 North America

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS INDUSTRY VERTICALS

9 ADVANCED ANALYTICS MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 DRIVERS: ADVANCED ANALYTICS MARKET, BY OFFERING

- 9.2 SOLUTIONS

- 9.2.1 RULE-BASED & STATISTICAL ANALYTICS

- 9.2.1.1 Enabling foundational insights through standardized reporting and statistical analysis

- 9.2.1.2 Reporting & dashboards tools

- 9.2.1.3 Self-service and ad-hoc analytics

- 9.2.1.4 Descriptive & diagnostic analytics

- 9.2.2 MACHINE LEARNING-DRIVEN ANALYTICS

- 9.2.2.1 Tapping into forward-looking insights with improved scalability through data-driven learning models

- 9.2.2.2 Predictive analytics

- 9.2.2.3 Prescriptive analytics

- 9.2.3 AUGMENTED & DECISION-CENTRIC ANALYTICS

- 9.2.3.1 Accelerating decision-making through AI-assisted insight generation and execution

- 9.2.3.2 Augmented insight discovery

- 9.2.3.3 AutoML-assisted analytics

- 9.2.3.4 Analytics automation and orchestration

- 9.2.3.5 Embedded and in-workflow analytics

- 9.2.4 AGENTIC & AUTONOMOUS ANALYTICS

- 9.2.4.1 Enabling continuous, self-directed decision-making through autonomous analytics systems

- 9.2.4.2 Analytics copilots & assistants

- 9.2.4.3 Autonomous analytics agents

- 9.2.4.4 Multi-agent decision execution

- 9.2.1 RULE-BASED & STATISTICAL ANALYTICS

- 9.3 SERVICES

- 9.3.1 PROFESSIONAL SERVICES

- 9.3.1.1 Enabling successful analytics adoption through expert-led strategy and execution

- 9.3.1.2 Strategy & consulting

- 9.3.1.3 Implementation & integration

- 9.3.1.4 Advanced modeling & AI development

- 9.3.2 MANAGED SERVICES

- 9.3.2.1 Sustaining analytical performance through continuous management and optimization

- 9.3.2.2 Managed data & Intelligence platforms

- 9.3.2.3 Model operations & optimization

- 9.3.2.4 Autonomous & AI-driven operations

- 9.3.1 PROFESSIONAL SERVICES

10 ADVANCED ANALYTICS MARKET, BY DELIVERY MODE

- 10.1 INTRODUCTION

- 10.1.1 DRIVERS: ADVANCED ANALYTICS MARKET, BY DELIVERY MODE

- 10.2 STANDALONE ANALYTICS SOFTWARE

- 10.2.1 ENABLING CONTROLLED AND CUSTOMIZABLE ANALYTICS THROUGH INDEPENDENT PLATFORMS

- 10.3 EMBEDDED & IN-APPLICATION DELIVERY

- 10.3.1 DRIVING ANALYTICS' ADOPTION BY DELIVERING INSIGHTS DIRECTLY WITHIN BUSINESS WORKFLOWS

- 10.4 CLOUD-NATIVE & LAKEHOUSE-BASED DELIVERY

- 10.4.1 SCALING ADVANCED ANALYTICS THROUGH FLEXIBLE AND CLOUD-FIRST ARCHITECTURES

- 10.5 EDGE & DISTRIBUTED ANALYTICS DELIVERY

- 10.5.1 ENABLING REAL-TIME ANALYTICS CLOSER TO DATA SOURCES AND OPERATIONS

- 10.6 AGENT-BASED & AUTONOMOUS DELIVERY MODELS

- 10.6.1 AUTOMATING ENTERPRISE DECISIONS THROUGH SELF-DIRECTED AND INTELLIGENT ANALYTICS SYSTEMS

11 ADVANCED ANALYTICS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.1.1 DRIVERS: ADVANCED ANALYTICS MARKET, BY APPLICATION

- 11.2 CUSTOMER & REVENUE INTELLIGENCE

- 11.2.1 OFFERING DATA-DRIVEN CUSTOMER UNDERSTANDING AND REVENUE OPTIMIZATION ACROSS SECTORS

- 11.2.2 CUSTOMER SEGMENTATION, CLV, AND CHURN

- 11.2.3 MARKETING ATTRIBUTION & CAMPAIGN EFFECTIVENESS

- 11.2.4 PRICING, PROMOTION, AND RECOMMENDATION

- 11.3 FINANCIAL RISK & PERFORMANCE MANAGEMENT

- 11.3.1 STRENGTHENING FINANCIAL STABILITY THROUGH ANALYTICS-DRIVEN RISK CONTROL AND PERFORMANCE OPTIMIZATION

- 11.3.2 FINANCIAL PLANNING, FORECASTING, AND PERFORMANCE

- 11.3.3 CREDIT, MARKET, AND OPERATIONAL RISK

- 11.3.4 FRAUD MANAGEMENT, AML, AND COMPLIANCE

- 11.4 SUPPLY CHAIN & OPERATIONS INTELLIGENCE

- 11.4.1 BUILDING RESILIENT AND ADAPTIVE SUPPLY CHAINS THROUGH ANALYTICS-DRIVEN OPERATIONAL VISIBILITY

- 11.4.2 DEMAND PLANNING & FORECASTING

- 11.4.3 SUPPLY CHAIN, LOGISTICS, AND NETWORK OPTIMIZATION

- 11.4.4 ASSET PERFORMANCE & MAINTENANCE PLANNING

- 11.5 PROCESS & QUALITY MANAGEMENT

- 11.5.1 IMPROVING OPERATIONAL EXCELLENCE THROUGH ANALYTICS-LED PROCESS VISIBILITY AND QUALITY CONTROL

- 11.5.2 PROCESS INTELLIGENCE & OPTIMIZATION

- 11.5.3 QUALITY MANAGEMENT & DEFECT REDUCTION

- 11.5.4 YIELD & THROUGHPUT OPTIMIZATION

- 11.6 HUMAN CAPITAL ANALYTICS

- 11.6.1 ENABLING DATA-DRIVEN WORKFORCE DECISIONS TO IMPROVE PRODUCTIVITY AND ORGANIZATIONAL RESILIENCE

- 11.6.2 WORKFORCE PLANNING & CAPACITY MANAGEMENT

- 11.6.3 EMPLOYEE PERFORMANCE & ENGAGEMENT

- 11.6.4 TALENT ACQUISITION, RETENTION, AND ATTRITION

- 11.7 PRODUCT, DIGITAL, AND IT OPERATIONS ANALYTICS

- 11.7.1 ENHANCING DIGITAL RELIABILITY AND PRODUCT PERFORMANCE THROUGH ANALYTICS-LED OPERATIONAL INTELLIGENCE

- 11.7.2 PRODUCT USAGE & PERFORMANCE

- 11.7.3 DIGITAL EXPERIENCE MONITORING

- 11.7.4 IT & PLATFORM OPERATIONS ANALYTICS

- 11.8 INTELLIGENT DECISION AUTOMATION

- 11.8.1 ACCELERATING BUSINESS OUTCOMES THROUGH ANALYTICS-DRIVEN AND AUTOMATED DECISION EXECUTION

- 11.8.2 AUTOMATED DECISION MANAGEMENT

- 11.8.3 CLOSED-LOOP BUSINESS PROCESS CONTROL

- 11.8.4 PREDICTIVE INTERVENTION & EXCEPTION MANAGEMENT

12 ADVANCED ANALYTICS MARKET, BY VERTICAL

- 12.1 INTRODUCTION

- 12.1.1 DRIVERS: ADVANCED ANALYTICS MARKET, BY VERTICAL

- 12.2 BFSI

- 12.2.1 STRENGTHENING FINANCIAL TRUST AND PROFITABILITY THROUGH RISK-AWARE AND DATA-DRIVEN INTELLIGENCE

- 12.3 HEALTHCARE & LIFE SCIENCES

- 12.3.1 IMPROVING PATIENT OUTCOMES AND OPERATIONAL EFFICIENCY THROUGH ANALYTICS-ENABLED HEALTHCARE INTELLIGENCE

- 12.4 RETAIL & ECOMMERCE

- 12.4.1 DRIVING REVENUE GROWTH AND PERSONALIZATION THROUGH CUSTOMER-CENTRIC ANALYTICS

- 12.5 MANUFACTURING

- 12.5.1 DRIVING OPERATIONAL EXCELLENCE AND RESILIENCE THROUGH ANALYTICS-LED MANUFACTURING INTELLIGENCE

- 12.6 TELECOMMUNICATIONS

- 12.6.1 ENHANCING NETWORK PERFORMANCE AND CUSTOMER EXPERIENCE THROUGH ANALYTICS-DRIVEN TELECOM INTELLIGENCE

- 12.7 ENERGY & UTILITIES

- 12.7.1 IMPROVING RELIABILITY AND SUSTAINABILITY THROUGH ANALYTICS-ENABLED ENERGY INTELLIGENCE

- 12.8 MEDIA & ENTERTAINMENT

- 12.8.1 MAXIMIZING AUDIENCE ENGAGEMENT AND MONETIZATION THROUGH ANALYTICS-DRIVEN CONTENT INTELLIGENCE

- 12.9 GOVERNMENT & PUBLIC SECTOR

- 12.9.1 ENHANCING TRANSPARENCY AND SERVICE DELIVERY THROUGH ANALYTICS-ENABLED PUBLIC SECTOR INTELLIGENCE

- 12.10 TRANSPORTATION & MOBILITY

- 12.10.1 IMPROVING SAFETY, EFFICIENCY, AND SUSTAINABILITY THROUGH ANALYTICS-LED MOBILITY INTELLIGENCE

- 12.11 TECHNOLOGY & SOFTWARE

- 12.11.1 SCALING DIGITAL INNOVATION AND PLATFORM PERFORMANCE THROUGH ANALYTICS-NATIVE SOFTWARE INTELLIGENCE

- 12.12 OTHER VERTICALS

13 ADVANCED ANALYTICS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: ADVANCED ANALYTICS MARKET DRIVERS

- 13.2.2 US

- 13.2.2.1 Scaling governed, cloud-native analytics driven by AI investment, regulatory focus, and hyperscale infrastructure expansion

- 13.2.3 CANADA

- 13.2.3.1 Advancing trusted and compliant analytics adoption through strong AI research, data sovereignty focus, and public-sector leadership

- 13.3 EUROPE

- 13.3.1 EUROPE: ADVANCED ANALYTICS MARKET DRIVERS

- 13.3.2 UK

- 13.3.2.1 Accelerating analytics adoption through strong digital regulation, cloud maturity, and AI-first enterprise strategies

- 13.3.3 GERMANY

- 13.3.3.1 Driving industrial and manufacturing analytics through Industry 4.0 leadership and data sovereignty priorities

- 13.3.4 FRANCE

- 13.3.4.1 Expanding analytics adoption through strong public-sector leadership and national AI investment programs

- 13.3.5 ITALY

- 13.3.5.1 Accelerating analytics adoption through enterprise digitalization, cloud modernization, and EU-backed investment programs

- 13.3.6 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: ADVANCED ANALYTICS MARKET DRIVERS

- 13.4.2 CHINA

- 13.4.2.1 Scaling analytics adoption through state-led digital infrastructure, AI investment, and platform-driven data ecosystems

- 13.4.3 INDIA

- 13.4.3.1 Accelerating analytics growth through digital public infrastructure, cloud adoption, and enterprise modernization

- 13.4.4 JAPAN

- 13.4.4.1 Advancing analytics maturity through enterprise modernization, productivity focus, and industrial data integration

- 13.4.5 ASEAN

- 13.4.6 REST OF ASIA PACIFIC

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: ADVANCED ANALYTICS MARKET DRIVERS

- 13.5.2 SAUDI ARABIA

- 13.5.2.1 Scaling advanced analytics through Vision 2030-driven digital transformation and data-led governance

- 13.5.3 UAE

- 13.5.3.1 Advancing analytics maturity through smart government leadership and AI-first national strategies

- 13.5.4 TURKEY

- 13.5.4.1 Advancing analytics adoption through financial-sector leadership and enterprise digital transformation

- 13.5.5 SOUTH AFRICA

- 13.5.5.1 Anchoring analytics growth through BFSI dominance, public-sector modernization, and risk-focused use cases

- 13.5.6 REST OF MIDDLE EAST & AFRICA

- 13.6 LATIN AMERICA

- 13.6.1 LATIN AMERICA: ADVANCED ANALYTICS MARKET DRIVERS

- 13.6.2 BRAZIL

- 13.6.2.1 Driving analytics adoption through large-scale enterprise digitalization and financial-sector innovation

- 13.6.3 MEXICO

- 13.6.3.1 Expanding analytics usage through manufacturing integration and cross-border digital transformation

- 13.6.4 REST OF LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES, 2021-2025

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 MARKET RANKING ANALYSIS, 2025

- 14.5 BRAND COMPARATIVE ANALYSIS

- 14.5.1 BRAND COMPARATIVE ANALYSIS (1/2)

- 14.5.1.1 IBM (US)

- 14.5.1.2 Microsoft (US)

- 14.5.1.3 SAP (Germany)

- 14.5.1.4 SAS Institute (US)

- 14.5.1.5 Alteryx (US)

- 14.5.2 BRAND COMPARATIVE ANALYSIS FOR BY AGENTIC & AUTONOMOUS ANALYTICS (2/2)

- 14.5.2.1 Palantir (US)

- 14.5.2.2 C3 AI (US)

- 14.5.2.3 Celonis (Germany)

- 14.5.2.4 SAS Institute (US)

- 14.5.2.5 Savant Labs (US)

- 14.5.1 BRAND COMPARATIVE ANALYSIS (1/2)

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS (TIER 1)

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS (TIER 1), 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Regional footprint

- 14.6.5.3 Offering footprint

- 14.6.5.4 Delivery mode footprint

- 14.6.5.5 Application footprint

- 14.6.5.6 Vertical footprint

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS (TIER 2 & 3)

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS (TIER 2 & 3), 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Regional footprint

- 14.7.5.3 Offering footprint

- 14.7.5.4 Delivery mode footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 Vertical footprint

- 14.8 COMPANY EVALUATION MATRIX: KEY PLAYERS (AGENTIC & AUTONOMOUS ANALYTICS)

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 COMPANY FOOTPRINT: KEY PLAYERS (AGENTIC & AUTONOMOUS ANALYTICS), 2025

- 14.8.3.1 Company footprint

- 14.8.3.2 Regional footprint

- 14.8.3.3 Offering footprint

- 14.8.3.4 Delivery mode footprint

- 14.8.3.5 Application footprint

- 14.8.3.6 Vertical footprint

- 14.9 COMPANY VALUATION AND FINANCIAL METRICS

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 14.10.2 DEALS

15 COMPANY PROFILES

- 15.1 INTRODUCTION

- 15.2 KEY PLAYERS

- 15.2.1 IBM

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Product launches and enhancements

- 15.2.1.3.2 Deals

- 15.2.1.4 MnM view

- 15.2.1.4.1 Key strengths

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses and competitive threats

- 15.2.2 GOOGLE

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches and enhancements

- 15.2.2.3.2 Deals

- 15.2.2.4 MnM view

- 15.2.2.4.1 Key strengths

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses and competitive threats

- 15.2.3 MICROSOFT

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches and enhancements

- 15.2.3.3.2 Deals

- 15.2.4 MOODY'S ANALYTICS

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches and enhancements

- 15.2.4.3.2 Deals

- 15.2.4.4 MnM view

- 15.2.4.4.1 Key strengths

- 15.2.4.4.2 Strategic choices

- 15.2.4.4.3 Weaknesses and competitive threats

- 15.2.5 SALESFORCE

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches and enhancements

- 15.2.5.3.2 Deals

- 15.2.6 PEGASYSTEMS

- 15.2.6.1 Business overview

- 15.2.6.2 Products/Solutions/Services offered

- 15.2.6.3 Recent developments

- 15.2.6.3.1 Product launches and enhancements

- 15.2.6.3.2 Deals

- 15.2.7 SNOWFLAKE

- 15.2.7.1 Business overview

- 15.2.7.2 Products/Solutions/Services offered

- 15.2.7.3 Recent developments

- 15.2.7.3.1 Product launches and enhancements

- 15.2.7.3.2 Deals

- 15.2.8 ORACLE

- 15.2.8.1 Business overview

- 15.2.8.2 Products/Solutions/Services offered

- 15.2.8.3 Recent developments

- 15.2.8.3.1 Product launches and enhancements

- 15.2.8.3.2 Deals

- 15.2.9 SERVICENOW

- 15.2.10 AWS

- 15.2.11 SAP

- 15.2.12 NICE

- 15.2.13 WORKDAY

- 15.2.14 ADOBE

- 15.2.15 SPLUNK (CISCO)

- 15.2.16 INFOR (KOCH INDUSTRIES)

- 15.2.17 TERADATA

- 15.2.1 IBM

- 15.3 TIER 2 & 3 PLAYERS

- 15.3.1 FICO

- 15.3.2 ANAPLAN

- 15.3.3 H2O.AI

- 15.3.4 DATABRICKS

- 15.3.5 ALTAIR

- 15.3.6 TIBCO

- 15.3.7 FRACTAL ANALYTICS

- 15.3.8 MU SIGMA

- 15.3.9 EPIC SYSTEMS

- 15.3.10 STRATEGY

- 15.3.11 QLIK

- 15.3.12 THOUGHTSPOT

- 15.3.13 DOMO

- 15.3.14 SISENSE

- 15.3.15 YELLOWFIN (IDERA)

- 15.3.16 ZOHO

- 15.3.17 GOODDATA

- 15.3.18 ALTERYX

- 15.3.19 DOMINO DATA LAB

- 15.3.20 KNIME

- 15.4 AGENTIC & AUTONOMOUS ANALYTICS PLAYERS

- 15.4.1 SAVANT LABS

- 15.4.1.1 Business overview

- 15.4.1.2 Products/Solutions/Services offered

- 15.4.1.3 Recent developments

- 15.4.1.3.1 Product launches and enhancements

- 15.4.1.3.2 Deals

- 15.4.1.4 MnM view

- 15.4.1.4.1 Key strengths

- 15.4.1.4.2 Strategic choices

- 15.4.1.4.3 Weaknesses and competitive threats

- 15.4.2 PALANTIR

- 15.4.2.1 Business overview

- 15.4.2.2 Products/Solutions/Services offered

- 15.4.2.3 Recent developments

- 15.4.2.3.1 Product launches and enhancements

- 15.4.2.3.2 Deals

- 15.4.2.4 MnM view

- 15.4.2.4.1 Key strengths

- 15.4.2.4.2 Strategic choices

- 15.4.2.4.3 Weaknesses and competitive threats

- 15.4.3 C3.AI

- 15.4.3.1 Business overview

- 15.4.3.2 Products/Solutions/Services offered

- 15.4.3.3 Recent developments

- 15.4.3.3.1 Product launches and enhancements

- 15.4.3.3.2 Deals

- 15.4.3.3.3 Other Developments

- 15.4.3.4 MnM view

- 15.4.3.4.1 Key strengths

- 15.4.3.4.2 Strategic choices

- 15.4.3.4.3 Weaknesses and competitive threats

- 15.4.4 SAS INSTITUTE

- 15.4.5 CELONIS

- 15.4.6 DATAROBOT

- 15.4.7 DATAIKU

- 15.4.1 SAVANT LABS

- 15.5 OTHER PLAYERS

- 15.5.1 ACCENTURE

- 15.5.2 DELOITTE

- 15.5.3 CAPGEMINI

- 15.5.4 COGNIZANT

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Breakup of primary profiles

- 16.1.2.2 Key industry insights

- 16.2 DATA TRIANGULATION

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 TOP-DOWN APPROACH

- 16.3.2 BOTTOM-UP APPROACH

- 16.4 MARKET FORECAST

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 STUDY LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS