|

시장보고서

상품코드

1851046

고급 분석 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Advanced Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

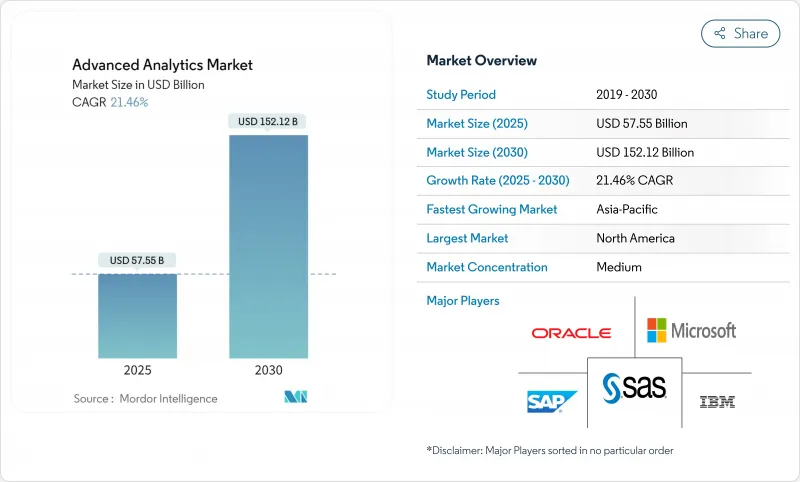

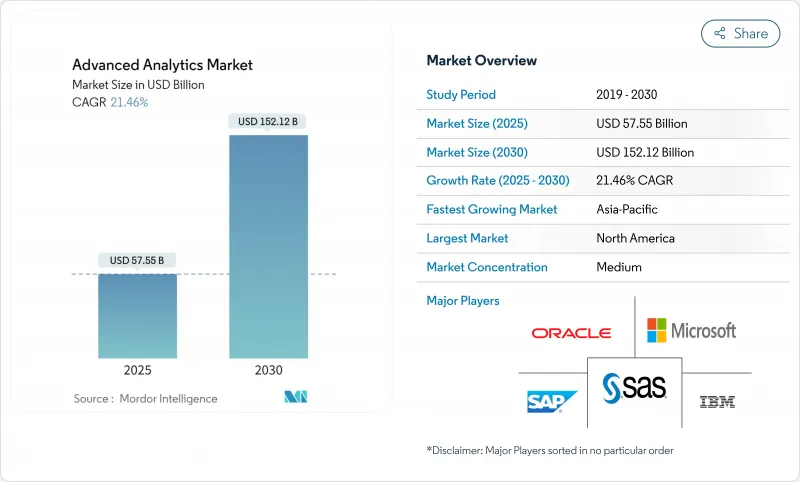

고급 분석 시장은 2025년에 575억 5,000만 달러, 2030년에는 1,522억 2,000만 달러에 이를 것으로 예측되며, 21.46%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

데이터량 급증, AI 인프라 비용 저하, 실시간 의사결정 지원에 대한 긴급 요건에 따라 각 업계에서 채용이 계속 확대되고 있습니다. 부정 행위의 정교화는 예측 분석, 위험 분석 및 그래프 분석에 대한 수요를 가속화하면서 플랫폼 통합을 통해 고객 전환 비용을 줄이고 다기능 도입을 가속화하고 있습니다. 엣지 처리는 현재 자율 시스템 및 산업 자동화와 같은 대기 시간에 민감한 이용 사례에 필수적이며 엣지 분석의 성장을 다른 부문보다 밀어 올리고 있습니다. 동시에 EU의 설명 가능한 AI 규정은 투자를 투명하고 감사할 수 있는 모델로 전환시켜 준거업체에게 선행자 이익을 제공합니다.

세계의 고급 분석 시장의 동향과 인사이트

증가하는 사기 탐지 요구

금융 기관은 규칙 기반 시스템을 능가하는 고도로 정교하고 악의적인 위협에 직면하고 있습니다. 미국의 규제 당국은 AI를 활용한 감시를 촉구하고 있으며, 머신러닝 모델은 이미 오탐지를 반감시키면서 검출 정밀도를 40% 향상시키고 있습니다. IBM의 조사에 따르면 대규모 거래 데이터를 거의 실시간으로 분석한 경우 95%의 분류 정밀도를 얻는 것으로 나타났습니다. 하이브리드 클라우드 엣지 아키텍처는 초보다 짧은 대기 시간 요구 사항을 충족하고 공급자가 불법 분석, 컴플라이언스 대시보드 및 모델 거버넌스를 통합 플랫폼에 번들로 제공할 수 있는 기회를 제공합니다.

빅데이터 양과 복잡성의 폭발적 증가

기업은 2024년에 매일 3억 2,877만TB를 생성하여 기존 BI 도구를 압도하였습니다. 현재 기업의 절반 가까이가 하이브리드 스토리지 및 데이터 패브릭 접근법을 채택하고 사일로화된 소스를 통합하여 고급 분석 시장에 배포하고 있습니다. 2025년까지는 중요한 처리의 50% 이상이 기존 데이터센터 밖에서 이루어질 것으로 예상되며, 자동화된 데이터 준비와 비기술적 비즈니스 사용자에게 인사이트를 제공하는 확장 분석의 필요성이 증가하고 있습니다.

데이터 통합 및 연결성 간극

단편화된 아키텍처는 종종 노후화된 On-Premise, 클라우드 및 운영 기술 시스템에 걸쳐 데이터를 보유하는 경우가 많습니다. 기업은 엔지니어링 시간의 64%를 분석보다 통합에 할당하고 있으며 이는 대규모 프로젝트에 대한 수익을 늦추고 열의를 저하시키고 있습니다. 산업용 기업은 분석 연계를 복잡하게 하는 독자적인 프로토콜과 싸우고 있으며 데이터 패브릭과 코드가 필요 없는 통합 솔루션의 중요성을 높이고 있습니다.

부문 분석

엣지 분석의 2030년까지 연평균 복합 성장률(CAGR)은 28.70%이며 대기 시간이 중요한 IoT 시나리오에서의 역할을 반영합니다. 이와는 대조적으로 예측 분석(Predictive Analytics)은 2024년에 24.22% 시장 점유율을 유지하면서 예측의 주류가 되고 있습니다. 엣지 장치는 현지화된 추론을 수행하고 네트워크 비용을 줄이고 데이터 주권을 확보합니다. 자동차, 에너지, 제조업에서는 이상 감지나 자율 제어 루프를 실현하기 위해 소형 추론 칩을 내장하고 있습니다. 벤더는 원시 데이터를 가져오지 않고 세계 모델을 학습하는 연계 학습 기능으로 차별화를 도모하고 있습니다. 비구조화된 데이터 양이 급증하는 동안 텍스트 및 비주얼 분석은 안정적인 채택을 유지하는 반면, 처방 및 리스크 분석은 최적화와 시나리오 모델링 수요에 따라 성장하고 있습니다.

고급 분석 시장 내 엣지 분석의 규모는 5G의 보급에 따라 급속히 확대될 전망입니다. 중요 인프라 소유자는 중앙 집중식 클라우드에서 터빈, 변전소 및 차량으로 의사결정 로직을 푸시하는 분산형 메시 패브릭으로 이동합니다. 한편, 기존의 예측 플랫폼은 진부화를 피하기 위해 실시간 데이터 스트림을 통합하여 시장이 클라우드와 엣지의 하이브리드 설계로 이동하고 있음을 보여줍니다.

은행과 공공기관에 선호되는 On-Premise 아키텍처는 2024년에는 54%의 매출을 차지하였습니다. 그러나 기업이 탄력적인 스케일링과 종량제의 경제성을 추구함에 따라 클라우드 도입은 CAGR 24.80%로 증가하고 있습니다. 하이퍼스케일러는 GPU 플릿의 확장을 선호하지만, 간헐적인 용량 부족으로 분석에 특화된 클라우드와 코로케이션과 엣지의 하이브리드에 공백이 발생합니다.

보안 향상과 기밀 컴퓨팅 서비스는 고객의 반대를 꾸준히 극복합니다. 클라우드 워크로드의 고급 분석 시장 내 규모는 드리프트 감지, 버전 관리 및 거버넌스를 자동화하는 관리형 모델 옵스 스위트로 더욱 확장됩니다. 하이브리드 시나리오에서는 민감한 On-Premise 데이터 처리와 버스트-투-클라우드 트레이닝 사이클을 결합하여 혁신을 방해하지 않고 컴플라이언스를 보장할 수 있습니다. 지역 데이터 거주에 관한 법률이 공급자의 구축을 형성하고 있으며, 특히 EU와 APAC에서는 국내 존이 개인정보 보호에 관한 법령에 대응하고 있습니다.

지역별 분석

북미는 2024년 고급 분석 시장 매출의 41%를 차지했습니다. 벤처 캐피탈은 인공지능에 1,091억 달러를 투자했으며, 그 중 339억 달러는 발전 모델, 신흥 기업 생태계 확대, 기업 실험에 사용되었습니다. 미국의 하이퍼스케일러는 새로운 GPU 클러스터를 투입함으로써 이전 용량 제약을 다루고 있으며, 아마존의 200억 달러의 펜실베니아 증축은 투자 규모의 크기를 나타냅니다. 규제에 대한 이니셔티브는 다양하지만 여전히 단편적이기 때문에 연방과 주의 다른 요구 사항을 해석하는 거버넌스 애드온에 대한 수요가 증가하고 있습니다.

APAC는 CAGR 23.10%로 가장 높으며, 제조 자동화, 5G의 전개, 정부의 스마트 시티 보조금이 뒷받침하고 있습니다. 중국의 AI 모델 강화는 경쟁력있는 국내 대체 제품을 생산하고 인도의 IT 서비스 수출은 지역 제조업체에 구현 인력을 제공합니다. 일본과 한국은 산업용 로봇과 자율 이동을 위한 엣지 분석 용도에 깊은 노력을 기울이고 있습니다. 총소유비용 저감과 공공 부문의 디지털화 정책은 전자상거래, 핀테크, 물류 플랫폼을 통합하는 동남아시아 국가의 고급 분석 시장을 확대하고 있습니다.

유럽은 엄격하게 진화하는 정책에 따라 꾸준히 성장합니다. EU의 AI 방법은 특히 중요한 분야에서 투명성 규칙을 충족시키기 위해 설명 가능한 플랫폼 구매를 가속화합니다. 독일 자동차 및 기계 기업은 인더스트리 4.0을 위해 예측 및 처방 분석을 채택하고 북유럽 공익 기업은 자연 에너지를 최적화하기 위해 지속가능성 분석을 통합합니다. 영국의 금융기관은 브렉시트 후의 리스크 모델 거버넌스에 투자하고 있습니다. 유럽의 고급 분석 시장의 규모는 가맹국 간의 공유 기준을 조화시키는 국경을 넘어서는 데이터 공간 구상의 혜택을 받고 있지만, 컴플라이언스 작업 부하가 도입 사이클을 장기화하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 높아지는 사기 탐지 요구

- 빅데이터의 양과 복잡성의 폭발

- 기업의 디지털 변혁의 물결

- AI/ML과 클라우드의 급속한 비용 저하

- 실시간 의사결정을 위한 엣지 분석

- 개요 가능한 AI에 대한 규제 강화

- 시장 성장 억제요인

- 데이터 통합과 연결성의 갭

- 데이터 사이언스 인력 부족

- 계산 에너지의 지속가능성 제한

- 하이퍼스케일 클라우드의 공급업체 종속

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 통계 분석

- 텍스트 분석

- 리스크 분석

- 예측 분석

- 처방 분석

- 비주얼 분석

- 네트워크 분석

- 지리공간 분석

- 소셜 미디어 분석

- 엣지 분석

- 기타 유형

- 전개 모드별

- On-Premise

- 클라우드

- 하이브리드

- 컴포넌트별

- 솔루션

- 서비스

- 컨설팅

- 매니지드 서비스

- 비즈니스 기능별

- 판매 및 마케팅

- 재무와 위험

- 운영 및 공급망

- 인적 자원

- 고객지원

- 최종 사용자 업계별

- BFSI

- 소매 및 소비재

- 헬스케어 및 생명과학

- IT 및 통신

- 운송 및 물류

- 정부 및 방위

- 제조업

- 에너지 및 유틸리티

- 미디어 및 엔터테인먼트

- 기타 산업

- 조직 규모별

- 대기업

- 중소기업(SME)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Microsoft Corporation

- SAS Institute Inc.

- SAP SE

- Oracle Corporation

- Amazon Web Services(AWS)

- Google LLC

- Salesforce Inc.(Tableau)

- Teradata Corporation

- QlikTech International AB

- MicroStrategy Incorporated

- Alteryx Inc.

- KNIME AG

- RapidMiner Inc.

- TIBCO Software Inc.

- Altair Engineering Inc.

- Sisense Inc.

- Domo Inc.

- Fair Isaac Corporation(FICO)

- Avanade Inc.

제7장 시장 기회와 미래 전망

CSM 25.11.20The advanced analytics market stands at USD 57.55 billion in 2025 and is forecast to reach USD 152.22 billion by 2030, reflecting a 21.46% CAGR.

Surging data volumes, falling AI infrastructure costs, and urgent requirements for real-time decision support continue to expand adoption across industries. Rising fraud sophistication is accelerating demand for predictive, risk, and graph analytics, while platform consolidation is reducing customer switching costs and encouraging multi-function deployments. Edge processing is now critical for latency-sensitive use cases such as autonomous systems and industrial automation, lifting edge-analytics growth ahead of other segments. Simultaneously, explainable AI regulation in the EU is redirecting investment toward transparent, auditable models, granting compliant vendors an early-mover advantage.

Global Advanced Analytics Market Trends and Insights

Escalating Fraud-Detection Needs

Financial institutions face highly sophisticated fraud threats that outpace rule-based systems. U.S. regulators urge AI-driven monitoring, and machine-learning models already lift detection accuracy by 40% while halving false positives. IBM research shows 95% classification accuracy when large-scale transaction data is analysed in near real time. Hybrid cloud-edge architectures satisfy sub-second latency requirements and create opportunities for providers bundling fraud analytics, compliance dashboards, and model governance into unified platforms.

Big-Data Volume & Complexity Explosion

Enterprises generated 328.77 million TB daily in 2024, overwhelming traditional BI tooling. Nearly half now employ hybrid storage and data-fabric approaches to integrate siloed sources for advanced analytics market deployments. By 2025, more than 50% of critical processing is expected outside conventional data centers, reinforcing the need for automated data preparation and augmented analytics that expose insights to non-technical business users.

Data Integration & Connectivity Gaps

Fragmented architectures often trap data across aging on-premises, cloud, and operational-technology systems. Organizations allocate 64% of engineering time to integration rather than analysis, delaying returns and dampening enthusiasm for large-scale projects. Industrial firms battle proprietary protocols that complicate analytics linkages, reinforcing the premium placed on data-fabric and no-code integration solutions.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Digital-Transformation Wave

- Regulatory Push for Explainable AI

- Shortage of Data-Science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge Analytics owns a 28.70% CAGR to 2030, reflecting its role in latency-critical IoT scenarios. In contrast, Predictive Analytics retained 24.22% advanced analytics market share in 2024 as the mainstream choice for forecasting. Edge devices perform localized inference, cutting network costs and ensuring data sovereignty, which is vital for regulated verticals. Automotive, energy, and manufacturing players are embedding compact inference chips to enable anomaly detection and autonomous control loops. Vendors differentiate through federated-learning capabilities that train global models without raw-data egress. Text and Visual Analytics hold steady adoption as unstructured data volumes balloon, while Prescriptive and Risk Analytics are spurred by demand for optimization and scenario modelling.

The advanced analytics market size for Edge Analytics is poised to expand rapidly as 5G coverage broadens. Critical infrastructure owners shift from centralized clouds to distributed mesh fabrics that push decision logic to turbines, substations, and vehicles. Meanwhile, established predictive platforms are integrating real-time data streams to avoid obsolescence, illustrating the market's pivot toward hybrid cloud-edge designs

On-Premises architectures, favored by banks and public agencies, accounted for 54% revenue in 2024 largely due to data-sovereignty mandates. Still, Cloud deployment is rising at 24.80% CAGR as enterprises pursue elastic scaling and pay-as-you-go economics. Hyperscalers prioritize GPU fleet expansion, though intermittent capacity shortfalls create openings for specialized analytics clouds and colocation-edge hybrids.

Security improvements and confidential-compute services steadily erode customer objections. The advanced analytics market size for cloud workloads gains further lift from managed model-ops suites that automate drift detection, versioning, and governance. Hybrid scenarios blend sensitive on-premises data processing with burst-to-cloud training cycles, ensuring compliance without capping innovation. Regional data-residency laws now shape provider buildouts, particularly in the EU and APAC, where in-country zones address privacy statutes.

The Advanced Analytics Market is Segmented by Type (Statistical Analysis, Text Analytics, and More), Deployment Mode (On-Premises, Cloud, Hybrid), Component (Solutions and Services), Business Function (Sales & Marketing, Finance & Risk, and More), End-User Industry, Organization Size (Large Enterprises, Smes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America continued to command 41% of advanced analytics market revenue in 2024. Venture capital channelled USD 109.1 billion into AI, including USD 33.9 billion for generative models, expanding startup ecosystems and enterprise experimentation. U.S. hyperscalers address prior capacity constraints by injecting new GPU clusters, with Amazon's USD 20 billion Pennsylvania build-out illustrating the scale of investment. Regulatory initiatives, though numerous, remain fragmented, prompting demand for governance add-ons that interpret divergent federal and state requirements.

APAC posts the highest 23.10% CAGR, propelled by manufacturing automation, 5G rollouts, and government smart-city grants. Chinese AI-model enhancements create competitive domestic alternatives, while India's IT-services exports deliver implementation talent to regional manufacturers. Japan and South Korea push deep into edge-analytics applications for industrial robotics and autonomous mobility. Lower total-cost-of-ownership and public-sector digitalization policies expand the advanced analytics market across Southeast Asian nations integrating ecommerce, fintech, and logistics platforms.

Europe grows steadily under rigorously evolving policy. The EU AI Act accelerates purchases of explainable platforms to satisfy transparency rules, especially in critical sectors. Germany's automotive and machinery firms adopt predictive and prescriptive analytics for Industry 4.0, while Nordic utilities embed sustainability analytics to optimize renewables. United Kingdom financial institutions invest in risk-model governance post-Brexit. The advanced analytics market size in Europe benefits from cross-border data-space initiatives that harmonize sharing standards among member states, yet compliance workloads elongate deployment cycles.

- IBM Corporation

- Microsoft Corporation

- SAS Institute Inc.

- SAP SE

- Oracle Corporation

- Amazon Web Services (AWS)

- Google LLC

- Salesforce Inc. (Tableau)

- Teradata Corporation

- QlikTech International AB

- MicroStrategy Incorporated

- Alteryx Inc.

- KNIME AG

- RapidMiner Inc.

- TIBCO Software Inc.

- Altair Engineering Inc.

- Sisense Inc.

- Domo Inc.

- Fair Isaac Corporation (FICO)

- Avanade Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating fraud-detection needs

- 4.2.2 Big-data volume and complexity explosion

- 4.2.3 Enterprise digital-transformation wave

- 4.2.4 Rapid AI/ML and cloud cost declines

- 4.2.5 Edge analytics for real-time decisions

- 4.2.6 Regulatory push for explainable AI

- 4.3 Market Restraints

- 4.3.1 Data integration and connectivity gaps

- 4.3.2 Shortage of data-science talent

- 4.3.3 Sustainability limits on compute energy

- 4.3.4 Vendor lock-in to hyperscale clouds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Statistical Analysis

- 5.1.2 Text Analytics

- 5.1.3 Risk Analytics

- 5.1.4 Predictive Analytics

- 5.1.5 Prescriptive Analytics

- 5.1.6 Visual Analytics

- 5.1.7 Network Analytics

- 5.1.8 Geospatial Analytics

- 5.1.9 Social Media Analytics

- 5.1.10 Edge Analytics

- 5.1.11 Other Types

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Component

- 5.3.1 Solutions

- 5.3.2 Services

- 5.3.2.1 Consulting

- 5.3.2.2 Managed Services

- 5.4 By Business Function

- 5.4.1 Sales and Marketing

- 5.4.2 Finance and Risk

- 5.4.3 Operations and Supply-Chain

- 5.4.4 Human Resources

- 5.4.5 Customer Support

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Retail and Consumer Goods

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 IT and Telecommunication

- 5.5.5 Transportation and Logistics

- 5.5.6 Government and Defense

- 5.5.7 Manufacturing

- 5.5.8 Energy and Utilities

- 5.5.9 Media and Entertainment

- 5.5.10 Other Industries

- 5.6 By Organization Size

- 5.6.1 Large Enterprises

- 5.6.2 Small and Mid-Sized Enterprises (SMEs)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Israel

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAS Institute Inc.

- 6.4.4 SAP SE

- 6.4.5 Oracle Corporation

- 6.4.6 Amazon Web Services (AWS)

- 6.4.7 Google LLC

- 6.4.8 Salesforce Inc. (Tableau)

- 6.4.9 Teradata Corporation

- 6.4.10 QlikTech International AB

- 6.4.11 MicroStrategy Incorporated

- 6.4.12 Alteryx Inc.

- 6.4.13 KNIME AG

- 6.4.14 RapidMiner Inc.

- 6.4.15 TIBCO Software Inc.

- 6.4.16 Altair Engineering Inc.

- 6.4.17 Sisense Inc.

- 6.4.18 Domo Inc.

- 6.4.19 Fair Isaac Corporation (FICO)

- 6.4.20 Avanade Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment