|

시장보고서

상품코드

2079667

엔드포인트 보안 시장 예측(-2031년) : 유형(EPP & EDR, UEM, 패치 및 취약성 관리, 자산 탐지 및 관리), 적용 대상별(워크스테이션, 모바일 디바이스, 서버, POS 단말기)Endpoint Security Market by Type (EPP & EDR, UEM, Patch & Vulnerability Management, Asset Discovery & Management), Enforcement Point (Workstations, Mobile Devices, Servers, POS Terminals) - Global Forecast to 2031 |

||||||

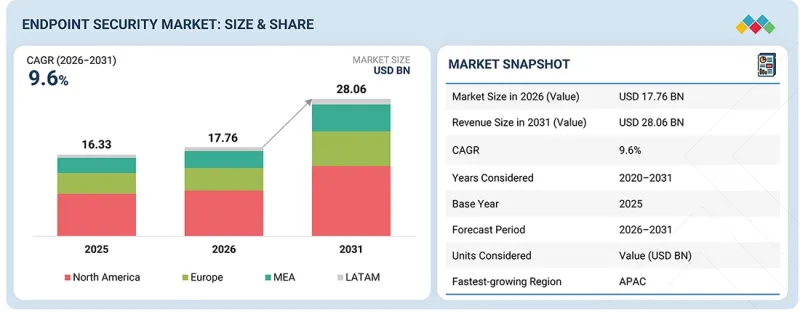

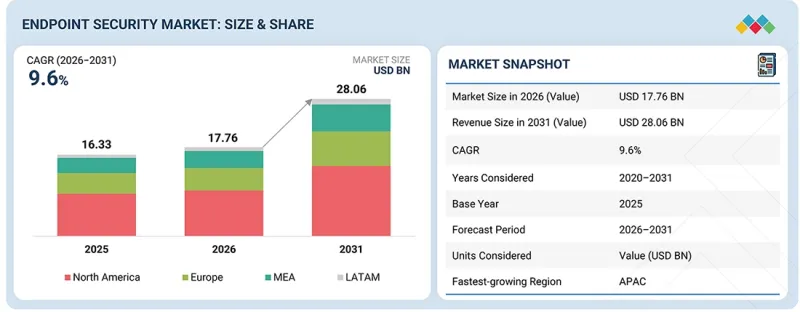

세계의 엔드포인트 보안 시장 규모는 2026년 177억 6,000만 달러에서 2031년에는 280억 6,000만 달러로 성장하며, 예측 기간 중 CAGR은 9.6%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 적용 포인트, 배포 모드, 조직 규모, 업계, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

엔드포인트 보안 시장은 사이버 공격의 고도화, 하이브리드 근무, BYOD, 연결 기기의 보급에 따른 엔드포인트의 공격 대상 영역 확대를 배경으로 강력한 성장을 달성하고 있습니다. 이에 대응하기 위해 기업은 제로 트러스트 보안 프레임워크의 도입을 확대하는 한편, 클라우드 네이티브 엔드포인트 보안 플랫폼, 통합 엔드포인트 관리(UEM), AI 기반 보안 기능에 대한 투자를 강화하여 엔드포인트 가시성을 높이고, 위협 탐지를 자동화하며, 전반적인 사이버 복원력을 강화하고 있습니다. 또한 사이버 보안 및 데이터 개인정보 보호에 관한 규제의 변화 역시 엔드포인트 보안 솔루션의 도입을 지속적으로 가속화하고 있습니다. 반면, 숙련된 사이버 보안 전문가의 부족과 최신 엔드포인트 보안 솔루션을 기존 IT 환경과 통합하는 데 따르는 복잡성으로 인해 시장 성장이 제약을 받고 있습니다.

'유형별로는 EPP 및 EDR 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.'

엔드포인트 보호 플랫폼(EPP)과 엔드포인트 탐지 및 대응(EDR)은 예방적 제어와 지속적인 모니터링, 위협 조사 및 대응 기능을 결합함으로써 현대 엔드포인트 보안의 핵심을 이루고 있습니다. EPP는 차세대 안티바이러스, 안티멀웨어, 호스트 방화벽, 애플리케이션 제어, 디바이스 제어, 익스플로잇 방지, 공격 표면 축소를 통해 첫 번째 방어선을 구축하여, 알려진 위협과 새로운 위협 모두로부터 기업의 엔드포인트를 보호합니다. EDR은 엔드포인트의 텔레메트리 데이터를 지속적으로 수집하고, 행동 지표를 분석하며, 공격의 타임라인을 재구성함으로써 이러한 기능을 보완합니다. 또한 보안 팀이 중앙 관리 콘솔을 통해 침해된 기기를 조사, 격리 및 복구할 수 있도록 합니다. 이러한 기술들을 통합함으로써, 조직은 노트북, 데스크톱 PC, 서버, 가상 데스크톱, 원격 근무자의 기기를 보호하는 동시에, 자동화된 사고 대응 및 위협 탐지 워크플로를 지원할 수 있게 됩니다.

'적용 분야별로는 워크스테이션 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.'

워크스테이션은 기업 환경 전반에서 널리 사용되고 있을 뿐만 아니라, 중요한 비즈니스 애플리케이션 및 기밀 데이터에 대한 접근에서 핵심적인 역할을 수행하고 있으므로 엔드포인트 보안 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 하이브리드 근무 방식이 확산됨에 따라 공격 대상 영역은 더욱 확대되고 있으며, 워크스테이션은 랜섬웨어, 피싱, 인증 정보 탈취 및 기타 엔드포인트 공격의 주요 표적이 되고 있습니다.

'Microsoft Digital Defense Report 2024'에 따르면 2023년 7월부터 2024년 6월 사이에 사람이 수행한 랜섬웨어 공격 건수는 2.75배 증가했으며, 마이크로소프트는 현재 하루 평균 6억 건 이상의 ID 도용 시도를 탐지하고 있습니다. 이러한 진화하는 위협으로 인해 조직은 행동 분석, 공격 표면 축소, 엔드포인트 격리, AI를 활용한 위협 탐지 등 고급 워크스테이션 보안 기능을 도입해야 할 필요에 직면해 있습니다. Microsoft 및 CrowdStrike와 같은 벤더가 제공하는 솔루션은 기업의 모든 워크스테이션에 걸쳐 통합된 보호, 실시간 모니터링, 신속한 사고 대응을 실현합니다.

'북미가 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.'

북미는 성숙한 디지털 인프라, 클라우드의 보급, 사이버 보안에 대한 투자 확대에 힘입어 엔드포인트 보안 시장에서 가장 큰 점유율을 차지하고 있습니다. 2024년 2월 현재, 미국의 인터넷 사용자 수는 약 3억 3,110만 명에 달하며, 인터넷 보급률은 97.1%를 기록하고 있는데, 이는 엔드포인트 환경의 급속한 확대에 기여하고 있습니다. 사이버 사고의 증가는 엔드포인트 보호 플랫폼(EPP), 엔드포인트 탐지 및 대응(EDR), 제로 트러스트 보안 솔루션에 대한 수요를 지속적으로 견인하고 있습니다. RCMP의 사이버 사고나, 여러 차례의 데이터 유출 사태를 계기로 FCC가 T-Mobile에 3,150만 달러의 합의금을 지급한 사례 등, 주목을 받은 정보 유출 사건들은 더욱 강력한 엔드포인트 보호의 필요성을 다시금 일깨워 주었습니다. 또한 SEC의 사이버 보안 공시 규정 및 NIST 사이버 보안 프레임워크 2.0의 도입과 같은 규제상의 조치로 인해 기업의 고도화된 엔드포인트 보안에 대한 투자가 가속화되고 있습니다.

이 보고서에서는 전 세계 엔드포인트 보안 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI별 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 소비자의 상황과 구매 행동

제9장 엔드포인트 보안 시장 : 유형별

제10장 엔드포인트 보안 시장 : 적용 대상별

제11장 엔드포인트 보안 시장 : 배포 모드별

제12장 엔드포인트 보안 시장 : 조직 규모별

제13장 엔드포인트 보안 시장 : 업계별

제14장 엔드포인트 보안 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSAThe global endpoint security market is projected to grow from USD 17.76 billion in 2026 to USD 28.06 billion by 2031, registering a CAGR of 9.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type, Enforcement Point, Deployment Mode, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

The endpoint security market is experiencing strong growth, driven by the increasing sophistication of cyberattacks and the expanding endpoint attack surface resulting from hybrid work, BYOD, and the proliferation of connected devices. In response, organizations are increasingly adopting Zero Trust security frameworks and investing in cloud-native endpoint security platforms, Unified Endpoint Management (UEM), and AI-powered security capabilities to improve endpoint visibility, automate threat detection, and strengthen overall cyber resilience. Additionally, evolving cybersecurity and data privacy regulations continue to accelerate the adoption of endpoint security solutions. However, market growth is constrained by the shortage of skilled cybersecurity professionals and the complexity of integrating modern endpoint security solutions with legacy IT environments.

"By type, the EPP & EDR segment is anticipated to account for the largest market share."

Endpoint Protection Platforms (EPP) and Endpoint Detection and Response (EDR) collectively form the core of modern endpoint security by combining preventive controls with continuous monitoring, threat investigation, and response capabilities. EPP establishes the first line of defense through next-generation antivirus, anti-malware, host firewall, application control, device control, exploit prevention, and attack surface reduction, protecting enterprise endpoints against both known and emerging threats. EDR complements these capabilities by continuously collecting endpoint telemetry, analyzing behavioral indicators, reconstructing attack timelines, and enabling security teams to investigate, isolate, and remediate compromised devices from a centralized console. The integration of these technologies allows organizations to secure laptops, desktops, servers, virtual desktops, and remote workforce devices while supporting automated incident response and threat hunting workflows.

By enforcement point, the workstations segment is anticipated to account for the largest market share.

Workstations hold the largest market share in the endpoint security market due to their widespread use across enterprise environments and their role in accessing critical business applications and sensitive data. The growing adoption of hybrid work has further expanded the attack surface, making workstations a primary target for ransomware, phishing, credential theft, and other endpoint attacks. According to the Microsoft Digital Defense Report 2024, human-operated ransomware encounters increased by 2.75x between July 2023 and June 2024, while Microsoft now detects more than 600 million identity attacks daily. These evolving threats are driving organizations to adopt advanced workstation security capabilities such as behavioral analytics, attack surface reduction, endpoint isolation, and AI-assisted threat detection. Solutions from vendors such as Microsoft and CrowdStrike provide centralized protection, real-time monitoring, and rapid incident response across enterprise workstations.

"North America is anticipated to account for the largest market share.

North America holds the largest share of the endpoint security market, supported by its mature digital infrastructure, widespread cloud adoption, and increasing investments in cybersecurity. In February 2024, the US recorded approximately 331.1 million internet users, representing an internet penetration rate of 97.1%, contributing to a rapidly expanding endpoint landscape. Rising cyber incidents continue to drive demand for Endpoint Protection Platforms (EPP), Endpoint Detection and Response (EDR), and Zero Trust security solutions. High-profile breaches, including the RCMP cyber incident and the FCC's USD 31.5 million settlement with T-Mobile following multiple data breaches, have reinforced the need for stronger endpoint protection. Additionally, regulatory initiatives such as the SEC Cybersecurity Disclosure Rules and the adoption of the NIST Cybersecurity Framework 2.0 are accelerating enterprise investments in advanced endpoint security.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the endpoint security market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level - 40% and Managerial & Other Levels - 60%

- By Region: North America - 35%, Europe - 20%, Asia Pacific - 25%, MEA - 15%, and Latin America - 5%

The endpoint security market comprises major companies, such as Microsoft (US), CrowdStrike (US), SentinelOne (US), Palo Alto Networks (US), Check Point (Israel), Broadcom (US), Elastic (Netherlands), and TrendAI (Trend Micro) (Japan). The study includes an in-depth competitive analysis of these key players in the endpoint security market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for endpoint security market on the basis of type, enforcement point, deployment mode, organization size, vertical, and region and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the endpoint security market.

Key benefits of buying this report

This research report is focused on various levels of analysis-industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the endpoint security market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

- Analysis of Market: Drivers (Growing sophistication and frequency of cyberattacks, Increasing adoption of remote/hybrid work, BYOD, and IoT devices, Rising implementation of Zero Trust security frameworks), restraints (High deployment and operational costs, Complexity of integrating endpoint security with legacy IT environments), opportunities (Growing migration to cloud-based endpoint security and unified endpoint management (UEM), Integration of AI/ML and automation into endpoint security solutions), and challenges (Shortage of skilled cybersecurity professionals, Ensuring consistent security and visibility across distributed endpoint environments) influencing the growth of the endpoint security market

- Market Penetration: Comprehensive information on endpoint security services and solutions offered by top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, product launches, expansions, and acquisitions in the endpoint security market

- Market Development: Comprehensive information about lucrative emerging markets; the report analyzes the markets for endpoint security across regions

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and services of leading players in the endpoint security market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ENDPOINT SECURITY MARKET

- 3.2 ENDPOINT SECURITY MARKET, BY TYPE

- 3.3 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT

- 3.4 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE

- 3.5 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE

- 3.6 ENDPOINT SECURITY MARKET, BY VERTICAL

- 3.7 ENDPOINT SECURITY MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing sophistication and frequency of cyberattacks

- 4.2.1.2 Increasing adoption of remote/hybrid work, BYOD, and IoT devices

- 4.2.1.3 Rising implementation of Zero Trust security frameworks

- 4.2.2 RESTRAINTS

- 4.2.2.1 High deployment and operational costs

- 4.2.2.2 Complexity of integrating endpoint security with legacy IT environments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing migration to cloud-based endpoint security and unified endpoint management (UEM)

- 4.2.3.2 Integration of AI/ML and automation into endpoint security solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of skilled cybersecurity professionals

- 4.2.4.2 Ensuring consistent security and visibility across distributed endpoint environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER -1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 Integration of AI-driven threat detection and autonomous response

- 4.5.2.2 Convergence of endpoint security with unified security platforms

- 4.5.2.3 Expansion of cloud-native endpoint security and Unified Endpoint Management (UEM)

- 4.5.2.4 Growing adoption of risk-based exposure management

- 4.5.2.5 Strengthening Zero Trust and identity-centric endpoint protection

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CYBERSECURITY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH AND DEVELOPMENT

- 5.3.2 PLANNING AND DESIGNING

- 5.3.3 SOLUTION AND SERVICE PROVIDERS

- 5.3.4 SYSTEM INTEGRATORS

- 5.3.5 DISTRIBUTORS/RESELLERS/VARS

- 5.3.6 VERTICALS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY DEPLOYMENT SIZE, 2026

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY VENDOR, 2026

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8523)

- 5.6.2 EXPORT SCENARIO (HS CODE 8523)

- 5.7 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 EUROPE ENERGY PROTECTS CUSTOMER DATA AND MULTIMILLION-EURO TRADING TRANSACTIONS WITH CROWDSTRIKE SOLUTIONS

- 5.10.2 AUSTRALIAN MEDIA LEADER STRENGTHENS CLOUD PUBLISHING SECURITY WITH PALO ALTO NETWORKS PLATFORM

- 5.10.3 UNIVERSITY BOOSTS ENDPOINT SECURITY WITH SYMANTEC MANAGEMENT SUITE

- 5.10.4 SOPHOS INSPIRES HEALTHCARE PROVIDER TO TAKE SECURITY TO ADVANCED LEVEL OF ENDPOINT AND NETWORK PROTECTION

- 5.10.5 STRENGTHENING CYBERSECURITY AT BOLSHOI THEATRE WITH KASPERSKY'S MANAGED DETECTION AND RESPONSE SOLUTION

- 5.11 IMPACT OF 2025 US TARIFF - ENDPOINT SECURITY MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 AI/ML and behavioral analytics

- 6.1.1.2 Endpoint detection and response (EDR) and automated remediation

- 6.1.1.3 Cloud-native endpoint security and unified endpoint management (UEM)

- 6.1.1.4 Exposure, vulnerability, and security posture management

- 6.1.1.5 Security automation and autonomous response

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Cloud analytics and telemetry correlation

- 6.1.2.2 Threat intelligence

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Zero Trust architecture (ZTA)

- 6.1.3.2 Public key infrastructure (PKI)

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | AI-NATIVE ENDPOINT PROTECTION & CLOUD MANAGEMENT

- 6.2.2 MID-TERM (2027-2030) | AUTONOMOUS ENDPOINT OPERATIONS & PLATFORM CONVERGENCE

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, PREDICTIVE, & SELF-ADAPTING ENDPOINT SECURITY

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-DRIVEN AUTONOMOUS ENDPOINT PROTECTION & SELF-HEALING OPERATIONS

- 6.4.2 CONTINUOUS ENDPOINT EXPOSURE MANAGEMENT & PREDICTIVE RISK REDUCTION

- 6.4.3 IDENTITY-AWARE ADAPTIVE ENDPOINT SECURITY (ZERO TRUST ENDPOINT ACCESS)

- 6.4.4 AUTONOMOUS ENDPOINT OPERATIONS & POLICY ORCHESTRATION

- 6.4.5 EDGE, IOT, & AUTONOMOUS DEVICE PROTECTION

- 6.5 IMPACT OF AI/GEN AI ON ENDPOINT SECURITY MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN ENDPOINT SECURITY MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN ENDPOINT SECURITY MARKET

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ENDPOINT SECURITY MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 SENTINELONE - AUTONOMOUS ENDPOINT PROTECTION FOR THOUGHTWORKS

- 6.6.2 CROWDSTRIKE - CLOUD-NATIVE ENDPOINT PROTECTION FOR CONCENTRIX

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CONSUMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 ENDPOINT SECURITY MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 TYPE: MARKET DRIVERS

- 9.2 ENDPOINT PROTECTION PLATFORM (EPP) & ENDPOINT DETECTION AND RESPONSE (EDR)

- 9.2.1 BEHAVIOR-BASED DETECTION ACCELERATES ADOPTION OF INTEGRATED EPP AND EDR SOLUTIONS

- 9.3 PATCH & VULNERABILITY MANAGEMENT

- 9.3.1 CONTINUOUS EXPOSURE MANAGEMENT DRIVES MARKET GROWTH

- 9.4 UNIFIED ENDPOINT MANAGEMENT (UEM)

- 9.4.1 WORKPLACE MOBILITY TRENDS PROPEL UNIFIED ENDPOINT MANAGEMENT DEPLOYMENTS

- 9.5 ASSET DISCOVERY & MANAGEMENT

- 9.5.1 GROWING DEMAND FOR CONTINUOUS ASSET VISIBILITY ACCELERATES MARKET GROWTH

- 9.6 OTHER TYPES

10 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT

- 10.1 INTRODUCTION

- 10.1.1 ENFORCEMENT POINT: MARKET DRIVERS

- 10.2 WORKSTATIONS

- 10.2.1 HYBRID WORK EXPANSION ACCELERATES DEMAND FOR ADVANCED ENDPOINT SECURITY

- 10.3 MOBILE DEVICES

- 10.3.1 RISING MOBILE WORKFORCE EXPANDS DEMAND FOR ENTERPRISE MOBILE ENDPOINT SECURITY

- 10.4 SERVERS

- 10.4.1 INCREASING ATTACKS ON CRITICAL SERVER WORKLOADS FUEL ENDPOINT SECURITY ADOPTION

- 10.5 POS TERMINALS

- 10.5.1 RISING DIGITAL PAYMENT ADOPTION DRIVES DEMAND FOR SECURE POS ENDPOINT PROTECTION

- 10.6 OTHER ENFORCEMENT POINTS

11 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE

- 11.1 INTRODUCTION

- 11.1.1 DEPLOYMENT MODE: MARKET DRIVERS

- 11.2 ON-PREMISES

- 11.2.1 DATA SOVEREIGNTY REQUIREMENTS SUSTAIN DEMAND FOR ON-PREMISES ENDPOINT SECURITY

- 11.3 CLOUD

- 11.3.1 SCALABILITY AND EFFICIENCY DRIVE CLOUD-BASED ENDPOINT SECURITY ADOPTION

12 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.1.1 ORGANIZATION SIZE: MARKET DRIVERS

- 12.2 LARGE ENTERPRISES

- 12.2.1 GROWING IT COMPLEXITY AND SECURITY OPERATIONS DRIVE ENDPOINT SECURITY ADOPTION IN LARGE ENTERPRISES

- 12.3 SMES

- 12.3.1 GROWING CYBERSECURITY AWARENESS AND BUDGET CONSTRAINTS DRIVE ENDPOINT SECURITY ADOPTION AMONG SMES

13 ENDPOINT SECURITY MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 VERTICAL: MARKET DRIVERS

- 13.2 GOVERNMENT

- 13.2.1 EXPANDING DIGITAL GOVERNMENT SERVICES DRIVE DEMAND FOR ENDPOINT SECURITY

- 13.3 BFSI

- 13.3.1 INCREASING CYBERATTACKS DRIVE NEED FOR INTEGRATED SOLUTIONS

- 13.4 IT & ITES

- 13.4.1 GROWING DIGITAL SERVICE DELIVERY DRIVES ENDPOINT SECURITY ADOPTION

- 13.5 HEALTHCARE & LIFE SCIENCES

- 13.5.1 GROWING DIGITAL HEALTHCARE ECOSYSTEMS DRIVE ENDPOINT SECURITY ADOPTION

- 13.6 AEROSPACE & DEFENSE

- 13.6.1 PROTECTION OF MISSION-CRITICAL AEROSPACE AND DEFENSE SYSTEMS DRIVES ENDPOINT SECURITY ADOPTION

- 13.7 RETAIL & E-COMMERCE

- 13.7.1 EXPANSION OF OMNICHANNEL RETAIL AND DIGITAL PAYMENTS DRIVES ENDPOINT SECURITY ADOPTION

- 13.8 MANUFACTURING

- 13.8.1 ENHANCING MANUFACTURING SECURITY WITH ADVANCED ENDPOINT SECURITY

- 13.9 ENERGY & UTILITIES

- 13.9.1 ADOPTION OF ADVANCED TECHNOLOGIES AND MEETING REGULATORY COMPLIANCE

- 13.10 TELECOMMUNICATIONS

- 13.10.1 LEVERAGING ENDPOINT SECURITY SOLUTIONS TO ENSURE UNINTERRUPTED SERVICE

- 13.11 TRANSPORTATION & LOGISTICS

- 13.11.1 GROWING DIGITAL SUPPLY CHAINS AND CONNECTED LOGISTICS NETWORKS DRIVE ENDPOINT SECURITY DEMAND

- 13.12 MEDIA & ENTERTAINMENT

- 13.12.1 GROWING DIGITAL CONTENT PLATFORMS AND ONLINE ENTERTAINMENT SERVICES DRIVE ENDPOINT SECURITY ADOPTION

- 13.13 EDUCATION

- 13.13.1 SAFEGUARDING EDUCATIONAL INSTITUTIONS WITH ADVANCED ENDPOINT SECURITY

- 13.14 OTHER VERTICALS

14 ENDPOINT SECURITY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: MARKET DRIVERS

- 14.2.2 US

- 14.2.2.1 Government initiatives and strategic partnerships to strengthen endpoint security adoption

- 14.2.3 CANADA

- 14.2.3.1 Strategic partnerships and enterprise deployments to accelerate endpoint security modernization

- 14.3 EUROPE

- 14.3.1 EUROPE: MARKET DRIVERS

- 14.3.2 UK

- 14.3.2.1 Rising cyber threats and government initiatives to strengthen endpoint security adoption

- 14.3.3 GERMANY

- 14.3.3.1 Cybersecurity innovations to drive demand for endpoint security across critical infrastructure

- 14.3.4 FRANCE

- 14.3.4.1 Rising cyber threats in critical sectors to drive demand for endpoint protection

- 14.3.5 ITALY

- 14.3.5.1 National cybersecurity initiatives to accelerate endpoint security modernization

- 14.3.6 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: MARKET DRIVERS

- 14.4.2 CHINA

- 14.4.2.1 Rising cyber espionage to strengthen demand for endpoint security solutions

- 14.4.3 JAPAN

- 14.4.3.1 Strategic partnerships and national cybersecurity initiatives to drive market

- 14.4.4 INDIA

- 14.4.4.1 Rapid digital transformation to accelerate endpoint security adoption

- 14.4.5 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: MARKET DRIVERS

- 14.5.2 GULF COOPERATION COUNCIL (GCC) COUNTRIES

- 14.5.2.1 UAE

- 14.5.2.1.1 Cybersecurity initiatives to propel demand for endpoint security

- 14.5.2.2 KSA

- 14.5.2.2.1 Transformative cybersecurity initiatives to drive endpoint security demand

- 14.5.2.3 Rest of GCC countries

- 14.5.2.1 UAE

- 14.5.3 SOUTH AFRICA

- 14.5.3.1 Rising cyber threats and focus on strengthening cyber defense posture to drive market

- 14.5.4 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: MARKET DRIVERS

- 14.6.2 BRAZIL

- 14.6.2.1 Cybersecurity investments and infrastructure expansion to increase endpoint security demand

- 14.6.3 MEXICO

- 14.6.3.1 AWS's strategic investment to create opportunity for endpoint security advancements

- 14.6.4 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2026

- 15.2 REVENUE ANALYSIS, 2020-2025

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 BRAND COMPARISON

- 15.4.1 MICROSOFT

- 15.4.2 CROWDSTRIKE

- 15.4.3 PALO ALTO NETWORKS

- 15.4.4 TRENDAI (TREND MICRO)

- 15.4.5 BROADCOM

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.5.1 COMPANY VALUATION, 2026

- 15.5.2 FINANCIAL METRICS USING EV/EBIDTA, 2026

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Type footprint

- 15.6.5.4 Vertical footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2026

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 15.7.6.1 Region footprint

- 15.7.6.2 Type footprint

- 15.7.6.3 Deployment mode footprint

- 15.7.6.4 Vertical footprint

- 15.8 COMPETITIVE SCENARIO

- 15.8.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 15.8.2 DEALS

- 15.8.3 EXPANSIONS

- 15.8.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 MICROSOFT

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches and enhancements

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 BROADCOM

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches and enhancements

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 PALO ALTO NETWORKS

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches and enhancements

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 CROWDSTRIKE

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 TRENDAI (TREND MICRO)

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches and enhancements

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 FORTINET

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches and enhancements

- 16.1.6.3.2 Deals

- 16.1.7 TRELLIX

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.8 KASPERSKY

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches and enhancements

- 16.1.8.3.2 Deals

- 16.1.8.3.3 Expansions

- 16.1.9 ST ENGINEERING

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.10 SOPHOS

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches and enhancements

- 16.1.10.3.2 Deals

- 16.1.10.3.3 Other developments

- 16.1.11 CHECK POINT

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches and enhancements

- 16.1.11.3.2 Deals

- 16.1.11.3.3 Expansions

- 16.1.12 ESET

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches and enhancements

- 16.1.12.3.2 Deals

- 16.1.13 IBM

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.14 SENTINELONE

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches and enhancements

- 16.1.14.3.2 Deals

- 16.1.15 CISCO

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.16 BLACKBERRY

- 16.1.16.1 Business overview

- 16.1.16.2 Products/Solutions/Services offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Deals

- 16.1.17 ELASTIC

- 16.1.18 OPTIV

- 16.1.19 OMNISSA

- 16.1.1 MICROSOFT

- 16.2 OTHER KEY PLAYERS

- 16.2.1 CORO

- 16.2.2 ACRONIS

- 16.2.3 VIPRE SECURITY GROUP

- 16.2.4 MORPHISEC

- 16.2.5 XCITIUM

- 16.2.6 SECURDEN

- 16.2.7 DEEP INSTINCT

- 16.2.8 CYBEREASON

- 16.2.9 TANIUM

- 16.2.10 42GEARS

- 16.2.11 ADAPTIVA

- 16.2.12 X-PHY INC.

- 16.2.13 FIDELIS SECURITY

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakup of primary profiles

- 17.1.2.2 Key insights from industry experts

- 17.2 DATA TRIANGULATION

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 TOP-DOWN APPROACH

- 17.3.2 BOTTOM-UP APPROACH

- 17.4 MARKET FORECAST

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS