|

시장보고서

상품코드

2043966

엔드포인트 및 클라우드 매니지드 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Endpoint And Cloud Managed Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

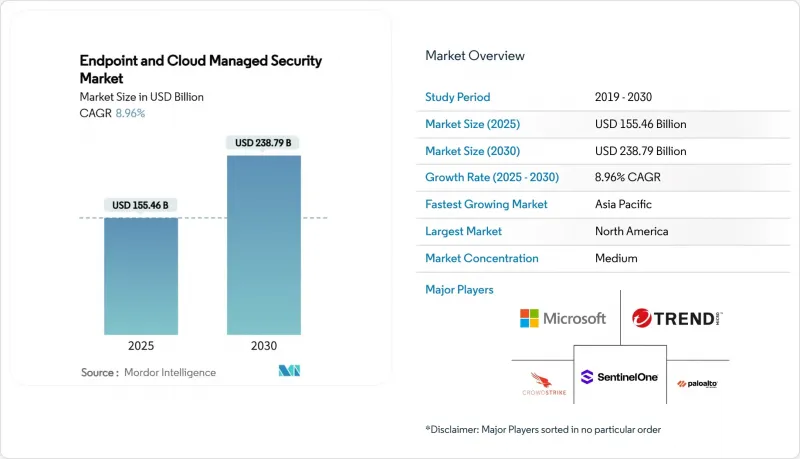

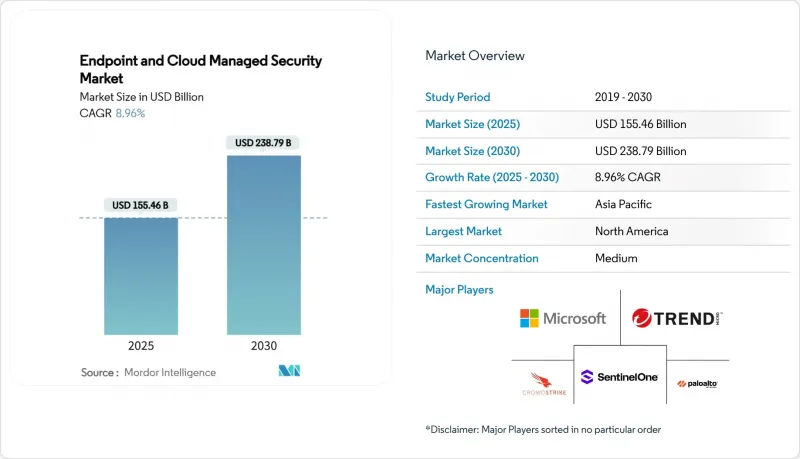

엔드포인트 및 클라우드 매니지드 보안 시장은 2025년에 1,554억 6,000만 달러로 평가되었습니다. 2030년까지 2,387억 9,000만 달러에 이를 것으로 예측되며, 동기 사이에서 CAGR 8.96%를 나타낼 전망입니다.

기업의 사이버 운영 아웃소싱으로의 빠른 전환, 하이브리드 인력의 확대, 클라우드 네이티브 애플리케이션의 성장이 이러한 성장 궤도를 주도하고 있습니다. 사이버 보험 조건의 강화, AI를 활용한 위협 사냥, 지정학적 요인으로 인한 공급망 사고도 MDR(Managed Detection and Response)에 대한 수요를 증가시키고 있습니다. 플랫폼 벤더 간 통합이 공급자의 전략을 재구성하고 있는 가운데, 통합 보안 스택은 구매자가 도구의 난립을 억제하고 총소유비용(TCO)을 절감할 수 있도록 돕고 있습니다.

세계의 엔드포인트 및 클라우드 매니지드 보안 시장 동향 및 인사이트

하이브리드 작업용 엔드포인트 급증

조직이 관리하는 엔드포인트 디바이스의 수는 2020년 이전 대비 3배 증가했으며, 공격 대상 영역의 복잡성이 증가하고 있습니다. 기업용, 개인용, IoT 하드웨어를 통합적으로 모니터링하는 것은 사내 리소스에 부담을 주며, 관리형 보안 파트너로 지출을 유도하고 있습니다. Microsoft의 Security Copilot과 Intune의 통합은 AI 기반 관리가 어떻게 대규모 가시성을 유지하는 데 도움이 될 수 있는지 보여줍니다. 기업들은 하이브리드 모델로 인해 사이버 보안의 복잡성이 40% 증가했다고 보고했으며, 23%만이 충분한 내부 역량을 보유하고 있다고 답했습니다. 따라서 매니지드 서비스는 인력을 크게 늘리지 않고도 일관된 정책, ID 검증, 컴플라이언스를 제공함으로써 엔드포인트 및 클라우드 매니지드 보안 시장의 성장 궤도에 힘을 실어주고 있습니다.

클라우드 네이티브 애플리케이션 도입 급증

현재 기업의 78%가 하이브리드 또는 멀티 클라우드 환경을 운영하고 있으며, 컨테이너, 서버리스, 마이크로서비스 워크로드가 급증하고 있습니다. 포티넷에 따르면, 클라우드 보안 예산은 2027년까지 매년 25%씩 증가하고 있으며, 기술 격차가 확대되는 가운데 관리형 공급자가 그 대부분을 차지하고 있다고 합니다. DevSecOps의 융합은 레거시 엔드포인트에서 최신 클라우드에 이르는 전문성을 요구하고 있으며, 지속적인 워크로드 포지셔닝 관리를 통합한 통합 아웃소싱 계약을 추진하고 있습니다.

거시 경제의 역풍으로 인한 예산 압박

경제 둔화로 인해 위협 증가에도 불구하고 많은 보안 예산이 정체되어 있습니다. 기업 이사회는 기존 대책으로 충분하다고 생각하며 추가 지출에 의문을 제기하고 있습니다. NIS2와 같은 규제 요건으로 인해 최소한의 투자가 여전히 요구되고 있으며, 컴플라이언스 대응이 필수적인 부문에서는 지출이 유지되는 반면, 재량적인 부문에서는 프로젝트가 미뤄지는 양극화된 시장이 형성되고 있습니다. 구매자가 광범위함보다 가치를 추구하는 가운데, ROI를 정량화하고 툴을 통합하는 매니지드 보안 벤더가 우선적으로 선택되고 있습니다.

부문 분석

관리형 엔드포인트 감지 및 대응(EDR) 서비스는 사이버 보험 의무화 및 실시간 텔레메트리의 보급에 힘입어 2024년 엔드포인트 및 클라우드 매니지드 보안 시장 규모에서 28.3%의 압도적인 점유율을 차지했습니다. 컴플라이언스 주도의 도입으로 다른 재량적 카테고리가 둔화되어도 안정적인 수익이 유지되고 있습니다. CAGR 14.8%로 성장하고 있는 관리형 통합 엔드포인트 관리 서비스는 노트북, 모바일 기기, IoT 엔드포인트에 걸친 단일 화면에서 디바이스 거버넌스를 원하는 기업 수요를 반영하고 있습니다.

기능의 융합으로 엔드포인트 관리와 보안의 경계가 모호해지고 있습니다. 현재 공급업체들은 디바이스 관리, 위협 감지, 정책 컴플라이언스를 통합된 구독으로 패키징하고 있으며, 이로 인해 벤더의 수가 줄어들고 있습니다. 기존 안티바이러스 서비스는 상품화가 진행되고 있으며, 벤더들은 행동 분석과 맞춤형 대응 플레이북을 중요시하고 있습니다. 고객이 보호 계층을 확장함에 따라 ID 관리, DLP 및 신흥 모바일 위협 방어 서비스가 포트폴리오를 강화하고 있습니다.

클라우드 기반 제공 형태는 2024년 엔드포인트 및 클라우드 매니지드 보안 시장에서 66.1%의 점유율을 차지하며, 2030년까지 연평균 10.6%의 성장률을 나타낼 것으로 예측됩니다. 특히 AI 분석 워크로드는 지속적인 모델 업데이트가 필요하기 때문에 조직은 고정된 하드웨어보다 탄력적이고 API 기반의 제어를 선호합니다. 규제가 엄격한 산업에서는 여전히 On-Premise 도입이 남아 있지만, 많은 조직이 로컬 센서에서 클라우드 분석으로 데이터를 전송하는 하이브리드형 오버레이를 채택하고 있습니다.

보안 서비스 에지(Security Service Edge)의 도입으로 클라우드 전환이 더욱 가속화되고 있으며, 매니지드 서비스 내에서 네트워크 액세스 제어와 위협 검사가 통합되고 있습니다. 총소유비용(TCO) 조사에 따르면, 인프라 감가상각비, 인건비, 패치 적용에 소요되는 간접비를 고려했을 때, 동급 사내 구축 대비 40-60%의 비용 절감이 가능한 것으로 나타났습니다.

'엔드포인트 및 클라우드 매니지드 보안 시장 보고서'는 서비스 유형(관리형 엔드포인트 감지 및 대응 서비스, 기타), 구축 모드(On-Premise, 클라우드 기반, 하이브리드), 보안 유형(엔드포인트 보안, 클라우드 워크로드 보안, 기타), 조직 규모(중소기업 및 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT, 통신, 의료, 기타), 지역별로 분류하여 분석하였습니다. 클라우드 워크로드 보안, 기타), 조직 규모(중소기업과 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT/통신, 의료, 기타), 지역별로 분류되어 있습니다.

지역별 분석

북미는 클라우드 보안의 조기 도입, 성숙한 사이버 보험 시장, 대규모 정부 아웃소싱 프레임워크에 힘입어 2024년 엔드포인트 및 클라우드 매니지드 보안 시장 규모의 38.7%를 차지했습니다. 미국 재무부의 200억 달러 규모의 지원 계약은 연방정부가 장기적인 관리형 파트너십을 원하고 있음을 보여줍니다. 캐나다의 조직은 미국 표준을 준수하고 있으며, 국경을 초월한 제공업체들은 공통 언어와 규제 유사성을 활용하여 서비스 제공의 효율성을 높이고 있습니다.

CAGR 14.2%를 나타낼 것으로 예측되는 아태지역은 디지털 서비스의 폭발적인 보급과 규제 프레임워크의 확대에 따른 혜택을 누리고 있습니다. 구글 클라우드의 인도네시아 'BerdAIa' 이니셔티브는 현지 데이터센터 내에 AI 지원 SOC 기능을 배치하는 것으로, 현지화 전략을 보여주는 좋은 예가 될 수 있습니다. 사이버 범죄 증가와 기술력 부족으로 인해 아세안 및 남아시아 국가에서 턴키 방식의 매니지드 서비스에 대한 수요가 증가하고 있습니다.

유럽에서는 NIS2, GDPR(EU 개인정보보호규정), 향후 도입될 AI 규제로 인해 컴플라이언스 중심의 아웃소싱이 추진되고 있습니다. ENISA에 따르면, 보안에 대한 지출은 현재 EU IT 예산의 9%를 차지하고 있으며, 전년 대비 증가 추세에 있습니다. 현지 데이터 처리, 다국어 SOC 지원, EU 인증 호스팅을 제공하는 업체는 주권과 운영 민첩성의 균형을 추구하는 기업들을 끌어들이고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Endpoint and Cloud Managed Security Market reached a current market size of USD 155.46 billion in 2025 and is forecast to attain USD 238.79 billion by 2030, registering an 8.96% CAGR over the period.

Rapid enterprise migration to outsourced cyber-operations, hybrid workforce expansion, and cloud-native application growth are steering this trajectory. Heightened cyber-insurance conditions, AI-driven threat-hunting, and geopolitical supply-chain incidents are also intensifying demand for managed detection and response. Consolidation among platform vendors is reshaping provider strategies, while unified security stacks are helping buyers curb tool sprawl and lower total cost of ownership.

Global Endpoint And Cloud Managed Security Market Trends and Insights

Proliferation of Hybrid-Work Endpoints

Organizations now manage triple the endpoint devices compared to pre-2020 levels, increasing attack-surface complexity. Unified monitoring over corporate, personal, and IoT hardware is stretching in-house resources, steering spending toward managed security partners. Microsoft's Security Copilot integration with Intune shows how AI-guided administration helps sustain visibility at scale. Enterprises report a 40% jump in cybersecurity complexity from hybrid models and admit only 23% possess adequate internal capabilities. Managed services thus deliver consistent policies, identity validation, and compliance without ballooning headcount, reinforcing the Endpoint and Cloud Managed Security Market's growth arc.

Surging Cloud-Native Application Adoption

Seventy-eight percent of enterprises now operate hybrid or multi-cloud environments, with container, serverless, and microservice workloads proliferating. Fortinet indicates cloud security budgets are expanding 25% annually to 2027, and managed providers are capturing the lion's share as skills gaps widen. DevSecOps convergence demands expertise spanning legacy endpoints and modern clouds, driving unified outsourcing contracts that embed continuous workload posture management.

Budget Squeeze from Macro Headwinds

Economic slowdowns have stalled many security budgets even as threat volume rises. Corporate boards question incremental spend, believing existing controls should suffice. Regulatory mandates such as NIS2 still force minimum investments, creating a split market where compliance-bound sectors sustain spending while discretionary sectors defer projects. Managed security vendors that quantify ROI and consolidate tools earn preference as buyers seek value over breadth.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Insurance Prerequisites for MDR

- XDR Platform Unification Demand

- MSP Vendor Lock-in Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Endpoint Detection and Response Services held a commanding 28.3% share of the Endpoint and Cloud Managed Security market size in 2024, anchored by cyber-insurance mandates and real-time telemetry gains. Compliance-driven uptake supports steady revenue even when other discretionary categories decelerate. Managed Unified Endpoint Management Services, expanding at 14.8% CAGR, reflect enterprise appetites for single-pane device governance spanning laptops, mobiles, and IoT endpoints.

Functional convergence is blurring the lines between endpoint management and security. Providers now package device administration, threat detection, and policy compliance in a unified subscription, reducing the total vendor count. Traditional antivirus services have commoditized, prompting vendors to emphasize behavioral analytics and tailored response playbooks. Identity, DLP, and emerging mobile-threat defense services round out portfolios as clients broaden protection layers.

Cloud-based delivery captured 66.1% Endpoint and Cloud Managed Security market share in 2024 and is on track for a 10.6% CAGR to 2030. Organizations favor elastic, API-driven controls over fixed hardware, particularly as AI analytics workloads need continuous model refreshes. On-premise installations persist in highly regulated sectors, yet many adopt hybrid overlays where local sensors feed cloud analytics.

Security service edge adoption further tilts uptake toward cloud, combining network access control and threat inspection within managed offerings. Total cost of ownership studies show 40-60% savings compared with equivalent in-house setups after factoring in infrastructure depreciation, staff, and patching overheads.

Endpoint and Cloud Managed Security Market Report is Segmented by Service Type (Managed Endpoint Detection and Response Services, and More), Deployment Mode (On-Premise, Cloud-Based, and Hybrid), Security Type (Endpoint Security, Cloud Workload Security, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), and Geography.

Geography Analysis

North America accounted for 38.7% of the Endpoint and Cloud Managed Security market size in 2024, buoyed by early cloud-security adoption, mature cyber-insurance markets, and sizable government outsourcing frameworks. The U.S. Treasury's USD 20 billion support contract illustrates federal appetite for long-term managed partnerships. Canadian organizations align with U.S. standards, while cross-border providers leverage shared language and regulatory commonalities to streamline service delivery.

Asia-Pacific, forecast to expand at a 14.2% CAGR, benefits from explosive digital-service uptake and widening regulatory frameworks. Google Cloud's Indonesia BerdAIa initiative, which deploys AI-enabled SOC capabilities within local data centers, demonstrates provider localization strategies. Rising cybercrime and skill shortages amplify demand for turnkey managed offerings across ASEAN and South Asian economies.

Europe sustains growth through NIS2, GDPR, and upcoming AI regulations, driving compliance-centric outsourcing. ENISA notes that security now consumes 9% of EU IT budgets, reflecting year-on-year elevation. Providers boasting local-data processing, multi-language SOC support, and EU-certified hosting attract enterprises balancing sovereignty with operational agility.

- CrowdStrike Holdings, Inc.

- Palo Alto Networks, Inc.

- Trend Micro Incorporated

- Sophos Group plc

- SentinelOne, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Secureworks, Inc.

- Arctic Wolf Networks, Inc.

- AT&T Cybersecurity (AT&T Inc.)

- Kaspersky Lab

- ESET, spol. s r.o.

- VMware, Inc. (Broadcom Inc.)

- Rapid7, Inc.

- Cybereason Inc.

- F-Secure Corporation

- Bitdefender SRL

- NCC Group plc

- Trustwave Holdings, Inc. (Singtel)

- Qualys, Inc.

- Elastic N.V.

- Darktrace plc

- Trellix

- Malwarebytes Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of hybrid-work endpoints

- 4.2.2 Surging cloud-native application adoption

- 4.2.3 Cyber-insurance prerequisites for MDR

- 4.2.4 XDR platform unification demand

- 4.2.5 AI-driven threat-hunting advances

- 4.2.6 Geo-political supply-chain attacks escalation

- 4.3 Market Restraints

- 4.3.1 High alert-fatigue and skill shortage

- 4.3.2 Data-sovereignty compliance hurdles

- 4.3.3 Budget squeeze from macro headwinds

- 4.3.4 MSP vendor lock-in concerns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Managed Endpoint Detection and Response Services

- 5.1.2 Managed Antivirus/Antimalware Services

- 5.1.3 Managed Identity and Access Management Services

- 5.1.4 Managed Data Loss Prevention Services

- 5.1.5 Managed Mobile Threat Defense

- 5.1.6 Managed Unified Endpoint Management Services

- 5.1.7 Others

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Security Type

- 5.3.1 Endpoint Security

- 5.3.2 Cloud Workload Security

- 5.3.3 Cloud Access Security Broker (CASB)

- 5.3.4 Cloud Email Security

- 5.3.5 Cloud Web Security

- 5.3.6 Cloud Identity Security

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Government and Defense

- 5.5.7 Energy and Utilities

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CrowdStrike Holdings, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Trend Micro Incorporated

- 6.4.4 Sophos Group plc

- 6.4.5 SentinelOne, Inc.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Check Point Software Technologies Ltd.

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 Secureworks, Inc.

- 6.4.10 Arctic Wolf Networks, Inc.

- 6.4.11 AT&T Cybersecurity (AT&T Inc.)

- 6.4.12 Kaspersky Lab

- 6.4.13 ESET, spol. s r.o.

- 6.4.14 VMware, Inc. (Broadcom Inc.)

- 6.4.15 Rapid7, Inc.

- 6.4.16 Cybereason Inc.

- 6.4.17 F-Secure Corporation

- 6.4.18 Bitdefender SRL

- 6.4.19 NCC Group plc

- 6.4.20 Trustwave Holdings, Inc. (Singtel)

- 6.4.21 Qualys, Inc.

- 6.4.22 Elastic N.V.

- 6.4.23 Darktrace plc

- 6.4.24 Trellix

- 6.4.25 Malwarebytes Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment