|

시장보고서

상품코드

1432886

세계 밀 종자 처리 시장 : 점유율 분석, 산업 동향, 통계 데이터, 성장 예측(2024-2029년)Global Wheat Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

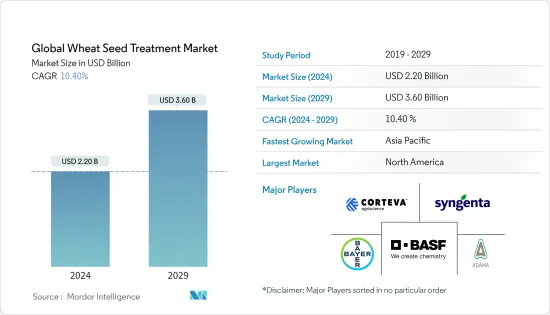

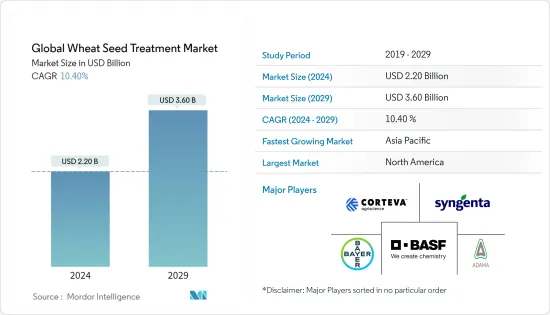

전 세계 밀 종자 처리 시장 규모는 2024년에 22억 달러로 추정되고, 2029년까지 36억 달러에 이를 것으로 예측되며, 예측 기간(2024-2029) 동안 복합 연간 성장률(CAGR) 10.40%로 성장할 전망입니다.

밀 무역 증가, 근본적인 수요 증가, 해충 및 질병의 출현으로 밀 수율을 개선해야 하므로 밀 씨앗에 대한 종자 처리의 사용이 강화되고 씨앗 생산이 촉진됩니다. 되었습니다. 치료 시장.

밀 종자 처리 시장은 북미가 독점하고 있지만 아시아태평양과 남미는 급속한 시장 성장을 보여줍니다. 미국 농무부(USDA)의 2019년 보고서에 따르면 세계 밀 공급량은 2017년에 비해 490만톤 증가했으며, 2018년 세계 생산량은 330만톤으로 증가했습니다. 2018년 인도 생산량은 1억120만톤, 유럽연합(EU) 생산량은 1억5,380만톤이었습니다. 생산량 증가는 기후로부터 씨앗을 보호하는 데 비용 효율적이고 효율적이기 때문에 밀 종자 처리 제품에 대한 수요가 증가하고 있음을 보여줍니다. 역경.

COVID-19 감염의 유행은 농부에게 중요한 중간 투입물의 가용성에 영향을 미쳤습니다. 신형 코로나바이러스가 작제 시즌 직전에 캐나다에 도달했기 때문에 종자나 농약 제품의 배송에 혼란이 발생할 가능성에 대해 우려가 집중되었습니다. 따라서, 농약과 같은 투입물의 가용성이 낮고 및/또는 가격이 높을수록 종자 처리 시장에서도 수율에 무게를 가할 수 있습니다.

밀 종자 처리 시장 동향

종자 처리 증가로 이어지는 불리한 생산 요인

밀의 성장에는 이상적인 기온과 강수량이 범위 내에 있어야하기 때문에 작물의 생산성은 주로 기후 조건에 따라 결정됩니다. 기후 조건 외에도 해충과 질병의 확산이 증가하여 밀 재배 지역에서 심각한 작물 손실이 발생했습니다. 따라서 고품질의 씨앗에 드는 고가의 비용을 고려하여 농부는 작물을 불리한 조건으로부터 보호하기 위해 씨앗 처리를 실천하는 것이 증가하고 있습니다. 이것은 세계적으로 밀 종자 처리 시장 성장을 가속하고 있습니다. 중국은 2020년 주요 작물 해충과 질병 발생으로 작물 손실에 휩쓸려 2019년보다 컸습니다. 특히 밀 흑성병이 대량으로 발생할 수 있습니다.

또한, 가뭄과 기후 변화는 러시아, 우크라, 카자흐스탄(RUK) 지역의 곡물 생산과 세계 식량 안보에 대한 심각한 위협이 되고 있습니다. 심각한 가뭄은이 지역의 밀 생산에 큰 영향을 미칩니다. 세계 수요에 대응하기 위해 밀 생산자는 생산성과 수익 모두에서 밀 수율을 높이는 데 중점을 둡니다. 종자 처리는 토양 매개 해충 및 병원균과 싸우는 가장 중요한 수단 중 하나이며, 밀 종자 처리 세계 시장은 미래 시장 성장 기회가 있으며 종자 처리 제품 수요가 높아질 것으로 예상됩니다. 최적의 작물 생산량을 확보합니다.

북미 - 밀 종자 처리의 가장 큰 시장

북미는 밀종자처리 화학물질의 채용률이 높기 때문에 최대 밀종자처리 시장이 될 것으로 예상되고 있으며 예측기간 동안 견조한 성장률을 기록하고 있습니다. 밀 종자 처리 시장 수요는 세계 수요에 의해 견인되고 있습니다. 밀은 작물 면적, 생산량, 농업 총 수입에서 미국의 농작물 중 옥수수와 콩에 이어 3위를 차지하고 있습니다. USDA의 보고서에 따르면 2019년 밀의 총 생산량은 4,780만 에이커의 농지에서 겨울 밀, 봄 밀, 듀럼 밀 합계 18억 8,400만 부셸이었습니다. 이 지역에서는 밀 녹, 후자리움 속, 선충에 의한 매년 피해가 큰 우려가 있습니다. 작물의 경제적 중요성을 고려하여 많은 기업과 정부 단체들은 새로운 종자 처리 기술의 혁신을 위한 연구 개발에 자금을 제공하는 데 자금을 지출하고 있습니다. 2017년, 신젠타는 종자처리기술의 연구개발을 실시하기 위해 미네소타주 스턴턴에 북미종자관리연구소를 개설했습니다. 신젠타는 이 연구소를 통해 고객의 특정 요구와 농장 및 토양 상태에 적합한 최신 기술을 기반으로 고객에게 맞춤형 솔루션을 제공합니다.

밀 종자 처리 산업 개요

밀 종자 처리 시장은 주로 새로운 개발이 진행되는 유럽 및 북미에 기업이 집중되어 있기 때문에 주요 밀 종자 처리 화학 회사간에 통합되어 있습니다. 또한 모든 대기업은 아시아태평양, 남미, 아프리카의 신흥 시장 획득에도 주력하고 있습니다. 예를 들어, BASF는 2017년에 Stamina F4 시리얼 살균제 씨앗 처리라는 이름의 새로운 밀 종자 처리를 출시하여 보다 일관되고 지속적인 질병 관리를 실현했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자,소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 용도

- 화학

- 바이오

- 기능

- 씨앗 보호

- 씨앗 강화

- 기타 기능

- 용도기술

- 씨앗 코팅

- 종자 펠렛화

- 씨앗 드레싱

- 기타 용도 기술

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 가장 채용된 전략

- 시장 점유율 분석

- 기업 프로파일

- Adama Agricultural Solutions Ltd

- Advanced Biological Marketing Inc

- BASF SE

- Bayer Cropscience AG

- Bioworks Inc.

- Corteva Agriscience

- Germains Seed Technology

- Incotec Group BV

- Nufarm Ltd

- Syngenta International AG

- Valent Biosciences Corp.

- Verdesian Life Sciences

제7장 시장 기회와 앞으로의 동향

제8장 COVID-19가 시장에 미치는 영향

BJH 24.03.05The Global Wheat Seed Treatment Market size is estimated at USD 2.20 billion in 2024, and is expected to reach USD 3.60 billion by 2029, growing at a CAGR of 10.40% during the forecast period (2024-2029).

Owing to the increasing trade of wheat, because of the underlying rise in demand, and the emergence of pests and diseases, there is a need to improve wheat yields, which is driving an enhanced usage of seed treatment on wheat seeds, thus driving the seed treatment market.

North America dominates the wheat seed treatment market, however, Asia-Pacific and South America are showing a rapid pace of market growth. As per the United States Department of Agriculture (USDA) report 2019, global wheat supplies have increased by 4.9 million metric ton and global production increased to 3.3 million metric ton in the year 2018, compared to 2017. In addition, the report estimates the wheat production for India was recorded at 101.2 million metric ton and for European Union (EU) at 153.8 million metric ton in 2018. The increasing production indicates a higher demand for wheat seed treatment products as it is cost-effective and efficient in protecting seeds against climatic adversities.

The COVID-19 pandemic affected the availability of key intermediate inputs for farmers. With COVID reaching Canada just before planting season, concerns were centered on possible disruptions of seeds and crop protection product delivery. Therefore, low availability and/or high prices of inputs such as pesticides could weigh on yields consequently, seed treatment market as well.

Wheat Seed Treatment Market Trends

Unfavorable Production Factors Leading to Increased Practice of Seed Treatment

Crop productivity is primarily determined by climatic conditions because ideal temperatures and precipitation must be in range for wheat growth. In addition to climatic conditions, increasing pest and disease infestation resulted in severe crop loss in wheat-growing regions. Therefore, taking into consideration of high cost involved in quality seeds, farmers are increasingly practicing seed treatment to protect crops against unfavorable conditions. This is driving the growth of the wheat seed treatment market, globally. China has suffered crop loss due to the occurrence of major crop pests and diseases in 2020, heavier than that of 2019. Specifically, wheat scab, which is likely to occur heavily.

Furthermore, droughts and climate change are the significant threats to grain production in the Russia, Ukraine, and Kazakhstan (RUK) region and for global food security. Severe droughts have been significantly affecting wheat production in these regions. To maintain pace with global demand, wheat producers focus on enhancing the wheat yield both in production outcome and revenue. Seed treatment, being one of the most important means of combating soil-borne pests and pathogens, it is anticipated that the global market for wheat seed treatment is anticipated to have the opportunity for future market growth, enhancing demand for seed treatment products, in order to ensure optimal crop output.

North America-Largest Market for Wheat Seed Treatment

North America is anticipated to be the largest wheat seed treatment market, owing to the higher adoption rate of seed treatment chemicals for wheat, recording a robust growth rate during the forecasted period. The demand for the wheat seed treatment market is driven by its global demand . Wheat ranks third among U.S. field crops in planted acreage, production, and gross farm receipts, behind corn and soybeans. As per the USDA report, in 2019 the total production of wheat was 1.884 billion bushels of winter, spring, and durum wheat on 47.8 million acres of cropland. Annual losses due to wheat rust, Fusarium spp, and nematode are a major concern in the region. Taking into account the economic importance of the crop, many companies and government associations are spending funds towards the funding of research and development for innovation of new seed treatment technology. In 2017, Syngenta opened a North American Seedcare Institute in Stanton, Minnesota for doing research and development on seed treatment technology. Through this institute, Syngenta provides customized solutions to customers based on their specific needs and the latest technology suited to the farm and soil condition.

Wheat Seed Treatment Industry Overview

The wheat seed treatment market is consolidated among the major wheat seed treatment chemical companies, owing to a high concentration of companies mainly in Europe and North America, where new developments are taking place. Additionally, all major companies are also focused on capturing the new emerging markets of Asia-Pacific, South America, and Africa. For instance, in 2017, BASF launched a new wheat seed treatment, named, Stamina F4 Cereals fungicide seed treatment, providing more consistent and continuous disease control.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Chemical

- 5.1.2 Biological

- 5.2 Function

- 5.2.1 Seed Protection

- 5.2.2 Seed Enhancement

- 5.2.3 Other Functions

- 5.3 Application Technique

- 5.3.1 Seed Coating

- 5.3.2 Seed Pelleting

- 5.3.3 Seed Dressing

- 5.3.4 Other Application Techniques

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Adama Agricultural Solutions Ltd

- 6.3.2 Advanced Biological Marketing Inc

- 6.3.3 BASF SE

- 6.3.4 Bayer Cropscience AG

- 6.3.5 Bioworks Inc.

- 6.3.6 Corteva Agriscience

- 6.3.7 Germains Seed Technology

- 6.3.8 Incotec Group BV

- 6.3.9 Nufarm Ltd

- 6.3.10 Syngenta International AG

- 6.3.11 Valent Biosciences Corp.

- 6.3.12 Verdesian Life Sciences