|

시장보고서

상품코드

1536979

세계 자동차 엔지니어링 서비스 아웃소싱 시장 - 점유율 분석, 산업 동향과 통계, 성장 예측(2024-2029년)Automotive Engineering Services Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

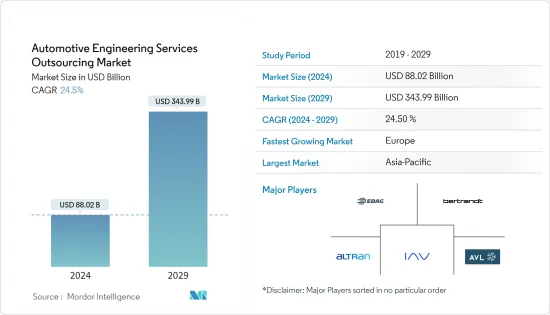

자동차 엔지니어링 서비스의 아웃소싱 시장 규모는 2024년에 880억 2,000만 달러로 추정되고, 2029년에는 3,439억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년)의 CAGR은 24.5%로 성장할 것으로 예상됩니다.

장기적으로 보면 엔지니어링 기업은 비용 절감, 효율화, 능력 향상을 위해 아웃소싱으로 빠르게 전환하고 있습니다. 기업이 엔지니어링 서비스를 아웃소싱하는 이유는 짧은 납기의 필요성, 유연성, 사내 전문가 부족, 예산 제약 등 다양합니다. 게다가 전기차에 대한 수요 증가, 전기차 채용 확대, 차량과 승객의 안전성을 높이는 ADAS 등 자율주행차의 혁신적 기술, 경량화 차량 등은 향후 수년간 시장 성장에 긍정적 영향 줄 수있는 주요 요인입니다.

전기자동차 판매의 성장을 고려하여 공급망의 여러 기업이 차량 부품 설계를 강화하기 위해 파트너십을 맺고 있습니다. 각국 정부는 구매자가 전통적인 자동차보다 전기자동차에 기울이도록 장려하기 위해 세계에서 다양한 계획과 노력을 시작하고 있습니다.

주요 하이라이트

- 전기자동차 구입을 장려하는 이러한 계획 중 하나는 2025년까지 150만대의 전기자동차를 달리게 하는 캘리포니아 ZEV계획입니다.

- 2023년 Capgemini는 자율주행차, 커넥티드카, 전기차, 쉐어드카의 각 영역에서 소프트웨어 개발 및 제품 엔지니어링 등의 주요 전문지식을 구사하여 지속가능하고 안전하며 안심하는 커넥티드 솔루션 을 제공했습니다. Capgemini는 Everest Group ACES Automotive Engineering Services PEAK Matrix Assessment 2023에서 최고의 '비전과 능력' 평가를 받았으며 최고 리더로 지명되었습니다.

유럽은 OEM의 존재와 전기자동차에 대한 소비자의 선호도 변화로 인해 대상 시장에서 크게 성장할 것으로 예상됩니다. 독일과 영국 등의 국가들의 존재도 정부가 실시하는 배출가스에 관한 정책과 정책, 녹색기술의 이용 장려로 시장 성장에 긍정적인 영향을 미칩니다. 북미도 예측 기간 동안 상당한 시장 성장이 예상됩니다.

자동차 엔지니어링 서비스 아웃소싱 시장 동향

승용차가 최고 점유율

승용차는 세련된 디자인, 컴팩트한 크기, 경제적 가치 등의 특징으로 최근 몇 년동안 촉진요인들 사이에서 절대적인 인기를 얻고 있습니다. 승용차는 많은 선진국에서 가장 흔한 교통 수단입니다. 라이프스타일 개선, 구매력 향상, 가처분 소득 증가, 브랜드 인지도 향상, 경제성 개선으로 전 세계적으로 고객의 선호도가 변화하고 승용차 판매량이 증가하고 있습니다.

인도 자동차 공업회에 따르면 2022-2023년 승용차 판매 대수는 14,67,039대에서 17,47,376대로 증가했습니다.

아시아태평양의 전기자동차 수요 증가도 시장 성장을 가져왔습니다. 2023년 1분기 인도의 전기차 판매량은 2022년 동기 대비 2배 증가했습니다.

스포츠용 다목적 차량(SUV) 수요 증가는 시장 선수들에게 유익한 기회를 창출해 세계 승용차 시장 성장의 주요 원동력이 되고 있습니다. 승용차(PV) 판매 전체에서 차지하는 SUV 점유율은 2016년 18%에서 2023년 41%로 상승했습니다.

각 회사는 자동차 공학 분야에서 흥미로운 능력을 개발하고 이동성의 미래에 대한 비전을 공유하는 데 주력하고 있습니다. 또한 이러한 능력과 혁신을 세계로 확대하기 위한 합의에 주력하고 있습니다. 부문에는 전기, 전자, 소프트웨어, 컨설팅 서비스, 테스트, 차량 개발 등이 포함됩니다.

예를 들어 2022년 10월 디지털 변환, 컨설팅, 비즈니스 리엔지니어링 서비스 및 솔루션의 선두 업체인 Tech Mahindra는 모빌리티 업계에서 협업을 촉진하는 오픈 EV 얼라이언스인 Foxconn 주도의 MIH(Mobility) in Harmony) 컨소시엄과의 제휴를 발표했습니다.

따라서 위의 요인은 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

아시아태평양이 자동차 엔지니어링 서비스 아웃소싱 시장에서 큰 점유율을 차지할 전망

아시아태평양은 대상 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 이는 대형 자동차 제조업체가 존재하고 저비용 노동력을 이용할 수 있기 때문에 인도, 한국, 중국 등의 국가들에게 생산과 관련 업무의 아웃소싱을 실시하고 있기 때문입니다. 그 결과 자동차 ESO 제공업체는 이 지역으로 사업을 이전하고 있습니다.

인도는 저비용 국가에서 사용 가능한 노동력의 약 30%를 차지합니다. 유럽, 중남미, 북미 국가에 비해 15-26%의 비용 우위성이 있습니다. 인도는 세계의 다양한 부문의 요구에 부응하는 세계 OEM에게 경쟁력있는 시장을 제공합니다. 기아자동차와 MG는 인도 시장에서 두 가지 새로운 OEM입니다.

인도에는 저비용으로 교육받은 반숙련 노동자들이 있기 때문에 아웃소싱을 요구하는 국제적인 OEM에 매력적인 선택이 되고 있습니다. 지속 가능한 모빌리티 솔루션을 개발하고 모빌리티 업계 소비자에게 가치를 제공할 수 있는 차세대 전기자동차, 자율주행 솔루션, 모빌리티 서비스 용도을 구축하기 위해 여러 기업이 파트너십에 주력하고 있습니다. 예를 들면

- 2022년 8월 인도에 본사를 두고 있는 L&T Technology Services는 BMW Group으로부터 5년간의 인포테인먼트 계약을 획득했으며, 이 회사의 인포테인먼트 스위트에 하이엔드 엔지니어링 서비스를 제공했습니다. BMW Group의 캠퍼스에 가깝기 때문에 LTTS 엔지니어는 다양한 솔루션을 사용하여 실시간으로 서비스를 제공할 수 있습니다.

따라서 위의 요인은 시장 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

자동차 엔지니어링 서비스 아웃소싱 업계 개요

자동차 엔지니어링 서비스의 아웃소싱 시장은 세계 및 지역적으로 확립된 기업에 의해 통합되고 주도되고 있습니다. 이들 기업은 시장에서의 지위를 유지하기 위해 신제품 출시, 제휴, 합병 등의 전략을 채택하고 있습니다. 예를 들면

- 2023년 9월, HCLTech는 독일 자동차 엔지니어링 서비스 제공업체인 ASAP Group의 주식 100%를 2억 7,600만 달러로 취득했습니다. 이 거래는 2023년 9월까지 완료될 예정이었습니다. ASAP는 자율주행, e모빌리티, 커넥티비티 등 분야에서 미래지향적인 자동차 기술에 주력하고 있습니다.

시장을 독점하는 주요 기업으로는 AVL List GmbH, Bertrandt AG, EDAG Engineering GmbH, IAV GmbH, Altran 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 자동차산업의 급격한 성장

- 시장 성장 억제요인

- 자동차 분야에서의 R&D 업무의 디지털화

- 업계의 매력 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 서비스 유형별

- 디자인

- 프로토타이핑

- 시스템 통합

- 테스트

- 로케이션 유형별

- 온쇼어

- 오프쇼어

- 차량 유형

- 승용차

- 상용차

- 추진 유형

- IC 엔진

- 전기 엔진

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 기업 프로파일

- AVL List GmbH

- Bertrandt AG

- EDAG Engineering GmbH

- IAV GmbH

- HORIBA Ltd

- Altran(Capgemini Engineering)

- FEV Group GmbH

- MBtech Group GmbH(A subsidiary of AKKA Technologies)

- Alten GmbH

- P3 Automotive GmbH

- Altair Engineering Inc.

- ITK Engineering GmbH(Robert Bosch GmbH)

- ESG Elektroniksystem-und Logistik-GmbH

- RLE International Group

- ASAP Holding GmbH

- Kistler Holding AG

제7장 시장 기회와 앞으로의 동향

JHS 24.08.29The Automotive Engineering Services Outsourcing Market size is estimated at USD 88.02 billion in 2024, and is expected to reach USD 343.99 billion by 2029, growing at a CAGR of 24.5% during the forecast period (2024-2029).

Over the long term, engineering firms are rapidly shifting to outsourcing to save costs, boost efficiency, or increase competence. Companies outsource engineering services for various reasons, including the need for fast delivery, flexibility, a lack of in-house specialists, and a constrained budget. Additionally, increasing demand for electric vehicles, as well as increasing adoption of electric vehicles, autonomous vehicle innovative technologies such as ADAS for vehicle and passenger safety, and lightweight vehicles, are key factors that may positively impact market growth in the coming years.

Considering the growth in electric vehicle sales, several companies from the supply chain are entering into partnerships to enhance the design of vehicle components. Governments have launched various plans and efforts worldwide to encourage buyers to lean toward electric vehicles over conventional automobiles.

Key Highlights

- One such plan that encourages the purchase of electric vehicles is the California ZEV program, which intends to have 1.5 million electric vehicles on the road by 2025.

- In November 2023, Capgemini offered sustainable, safe, secure, and connected solutions with key expertise such as software development and product engineering in the Autonomous, Connected, Electric, and Shared vehicles domains. It received the highest "Vision and Capability" rating and was designated the top Leader by the Everest Group ACES Automotive Engineering Services PEAK Matrix Assessment 2023.

Europe is expected to grow significantly in the target market, owing to the presence of OEMs and changing consumer preference toward electric vehicles. The presence of countries such as Germany and the United Kingdom also positively impacts the market's growth due to the policies and regulations implemented by their governments related to emissions and encouraging the usage of green technology. North America is also expected to witness considerable market growth during the forecast period.

Automotive Engineering Services Outsourcing Market Trends

Passenger Cars Hold the Highest Share

Passenger cars have gained immense popularity among drivers over the past few years due to features such as stylish design, compact size, and economic value. Passenger cars are the most common mode of transportation in numerous advanced countries. The improving lifestyles, increasing purchasing power, rising disposable incomes, growing brand awareness, and improving economy are leading to a shift in customer preferences worldwide globe, resulting in high sales of passenger cars.

According to the Society of Indian Automobile Manufacturers, sales of passenger cars increased from 14,67,039 to 17,47,376 units during 2022-2023.

The increased demand for electric vehicles in Asia-Pacific also resulted in market growth. In the first quarter of 2023, electric car sales in India doubled compared to the same period in 2022.

The rising demand for sport utility vehicles (SUVs) creates profitable opportunities for market players and acts as a major driving factor for the global passenger car market's growth. The share of SUVs in overall passenger vehicle (PV) sales rose from 18% in 2016 to 41% in 2023.

Companies are focusing on developing some exciting capabilities in automotive engineering and sharing their vision for the future of mobility. They are also focusing on agreements to scale these capabilities and innovations globally. The segments include electric/electronics, software, consulting and service, testing, and vehicle development.

For instance, in October 2022, Tech Mahindra, a leading provider of digital transformation, consulting, and business re-engineering services and solutions, announced a partnership with Foxconn-initiated MIH (Mobility in Harmony) Consortium, an open EV alliance that promotes collaboration in the mobility industry.

Thus, the abovementioned factors are expected to have a positive impact on the market.

Asia-Pacific is Expected to Hold a Major Share in the Automotive Engineering Service Outsourcing Market

Asia-Pacific is likely to have a large share of the target market, attributed to the presence of significant automobile OEMs and the outsourcing of production and associated operations to countries such as India, South Korea, and China due to the availability of low-cost labor. As a result, automotive ESO providers are transferring their operations to this region.

India accounts for roughly 30% of all available manpower among low-cost countries. The country has a 15-26% cost advantage over European, Latin American, and North American countries. India has provided a highly competitive market for global OEMs catering to the needs of various segments worldwide. Kia and MG are two new OEMs in the Indian market.

The availability of low-cost, educated, and semi-skilled labor in India makes it an attractive option for international OEMs seeking to outsource their operations. Several firms focus on partnerships to develop sustainable mobility solutions and build the next generation of electric vehicles, autonomous driving solutions, and mobility service applications that can deliver value for consumers in the mobility industry. For instance,

- In August 2022, L&T Technology Services, headquartered in India, bagged a 5-year infotainment deal from BMW Group to provide high-end engineering services for the company's suite of infotainment. The proximity to BMW Group's campus will enable LTTS' engineers to work on a variety of solutions and offer services in real-time.

Thus, the abovementioned factors are expected to positively impact the market's growth.

Automotive Engineering Services Outsourcing Industry Overview

The automotive engineering services outsourcing market is consolidated and led by globally and regionally established players. These companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions. For instance,

- In September 2023, HCLTech acquired a 100% stake in the German automotive engineering services provider ASAP Group for USD 276 million. The transaction was expected to close by September 2023. ASAP is focused on future-oriented automotive technologies in areas such as autonomous driving, e-mobility, and connectivity.

Some major players dominating the market include AVL List GmbH, Bertrandt AG, EDAG Engineering GmbH, IAV GmbH, and Altran.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Exponential Increase in Automotive Sector

- 4.2 Market Restraints

- 4.2.1 Digitization of R&D Operations in Automotive Sector

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Designing

- 5.1.2 Prototyping

- 5.1.3 System Integration

- 5.1.4 Testing

- 5.2 By Location Type

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 Propulsion Type

- 5.4.1 IC Engine

- 5.4.2 Electric Engine

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE*

- 6.1 Company Profiles

- 6.1.1 AVL List GmbH

- 6.1.2 Bertrandt AG

- 6.1.3 EDAG Engineering GmbH

- 6.1.4 IAV GmbH

- 6.1.5 HORIBA Ltd

- 6.1.6 Altran (Capgemini Engineering)

- 6.1.7 FEV Group GmbH

- 6.1.8 MBtech Group GmbH (A subsidiary of AKKA Technologies)

- 6.1.9 Alten GmbH

- 6.1.10 P3 Automotive GmbH

- 6.1.11 Altair Engineering Inc.

- 6.1.12 ITK Engineering GmbH (Robert Bosch GmbH)

- 6.1.13 ESG Elektroniksystem- und Logistik-GmbH

- 6.1.14 RLE International Group

- 6.1.15 ASAP Holding GmbH

- 6.1.16 Kistler Holding AG